Abstract

Abstract

This paper characterizes the set of equilibria in the first price auction with multiple bidders—specifically three bidders, each of whose type space is multi-dimensional, incorporating a bidder’s beliefs about others’ valuations. In this auction, each bidder independently and privately learns the other two opponents’ valuations with some probability. This paper derives closed form solutions for equilibrium bidding behaviours parameterized by the degree of information when the bidder has homogeneous beliefs regarding each opponent. This paper demonstrates how much the level of information affects the bidding behaviours of the informed bidders. In addition, this paper extends the model into

JEL Classification: D44, D82, D83

Introduction

The standard assumption of private value auctions that bidders only observe their own valuations but have no further information regarding an opponent’s valuation, other than the distribution from which the valuation is drawn, is unrealistic. Bidders may have private observations, perfectly or imperfectly with noise, of their opponents’ valuations. As noted by Bergemann, Brooks, and Morris (2017), these observations are largely influential to the bidders’ optimal bidding strategies since information about others’ private values will set the boundaries of bidding supports for equilibrium. This is more significant in a first price auction (FPA) environment because an equilibrium bidding strategy in a FPA depends on a bidder’s beliefs about the valuations of other bidders. Based on this motivation, this paper studies a model of multiple-bidder FPA and explores the equilibrium bidding behaviours among bidders who are affected by information. Through this research, this paper analyses the marginal value of information as more information becomes available to the bidders.

In this paper, I consider a multi-dimensional private value model with three bidders in which each bidder has a binary valuation and gains probabilistic, yet perfect information regarding the other bidders’ valuations. This paper contributes to the literature on auctions with information by introducing a novel construction regarding the information space and its structure: multi-dimensional type space and several informed bidders characterized by observation likelihood. I specifically define the informed bidders given any information level regarding each opponent and derive closed form solutions parameterized by the information level. By deriving the bidding intervals generated by each information level, it is possible to obtain the value of information a bidder may have. I explore how the bidding behaviours of an informed bidder change as more information is available. Moreover, throughout this paper, by computing the bidding thresholds for the bidders I demonstrate how much a bidder’s information contributes to the auction environment as the number of participants increases.

This model is closely related to Fang and Morris (2006), in that (a) each bidder has one of two discrete valuation types, (b) private information is added to a bidder’s type space and (c) an equilibrium analysis on multidimensional FPA is performed. However, regarding equilibrium analysis, Fang and Morris (2006) only present a two-bidder case, while this paper considers a three-bidder auction environment, followed by an

As in Fang and Morris (2006), the typical type space of a Bayesian game in FPA models is no more than two-dimensional. In the current paper with three bidders, the type space for a bidder extends to three dimensions: own valuation, information on the first opponent and information on the second opponent. When there are two possible types, low or high, 1

While a continuous valuation may seem more realistic, a discrete valuation environment is actually more so; real-life auctions have a finite valuation choice since any monetary value for an object can only have finitely many values between 0 and some maximum. The binary valuation model can be utilized to simulate a real-life auction of finite valuations because a high value bidder could adjust his bid to match that of the second-highest value bidder in the FPA environment.

For example, it is identical for an informed high value bidder to face against (high type, low type) or (low type, high type) in that one of them is a high type bidder and the other a low type regardless of order.

In equilibrium, low value bidders bid their true value regardless of their information about the other bidders. However, high value bidders, except the fully informed one who faces two low value bidders, randomize over bid intervals according to certain bid distributions. In this case, the equilibrium bidding strategy is varied depending on the level of information. A contribution of this paper is characterizing the complex relationship between bid distributions and information. Specifically, as there is more information available, the supports of the distributions from which uninformed bidders randomize decrease, whereas the supports of the distributions from which informed bidders randomize increase. When the bidders obtain more information regarding the other bidders’ valuations, the more likely they rely on the second distribution. This paper characterizes the relationship between bidding behaviours and information for a general model of

Beyond the two papers directly related to the main topic of this paper, there are other research works on information structure: Azacis and Vida (2015) suggest certain signal structures of information to improve bidders’ payoff in FPA. The study by Bergemann et al. (2017) specifically focuses on correlated private information in FPA. When information is correlated, the minimum winning-bid distributions can be constructed from each model’s information structure in which the lower bound is attained. Similarly, Bergemann and Morris (2013, 2016) show that the range of these can be described in general game settings by a correlated equilibrium under incomplete information. The work of robust mechanism design by Brooks (2013) also has this direction.

The Model

Three risk neutral bidders,

Therefore, there is no noise regarding the opponent’s type in the model.

All bidders submit their bids simultaneously and a highest bidder wins the object. The winner

A tie will be broken in favour of high value bidders when there are multiple highest bids. The tie breaking rule will be random with equal probability if there are multiple highest bidders with the same valuation.

In the model, each bidder has a three-dimensional type space. One is for a bidder’s own valuation

where

Characterization of Equilibrium

Equilibrium Bidding Strategy without Information

First, assume that there is no information regarding the other two bidders’ valuations:

Although the formal proof is presented in the Appendix, deriving the bidding interval is an important step towards the main theorem presented in the next section. To derive the bidding interval of the proposition, I first conjecture that a high value bidder without information randomizes over a certain interval, and then I determine the interval’s domain and the distribution over it.

The function

The three-bidder model without information is extended to the case of

The first term

I further conjecture that there is no mass point at

The upper bound of the support should satisfy

Hence, the upper bound

The non-trivial bidding interval is

Equilibrium Bidding Strategy with Information

Let us modify the model so that there exists information with positive probability regarding an opponent’s type. Bidder

These are (a) the high value bidder is uninformed of one of his opponents but knows that the other bidder’s valuation is high; (b) the high value bidder is uninformed of one of his opponents, but knows that the other bidder’s valuation is low.

For the necessity of obtaining a closed form solution, I assume that

For heterogeneous beliefs, the Equations (5), (6), (7) or equivalently (8), (9), (10) will be modified to:

Not only are these equations unsolvable for closed form solutions but also, given a constant

and

I utilize the following conjecture to derive the bidding intervals of the proposition, and then I present a formal proof.

I first construct the necessary conditions for the three types of bidders to support an equilibrium based on the following notion: an informed high value bidder facing a high type bids according to

The high value bidder will randomize over each support so that a bid from the support will make the identical payoff when the bid is drawn from either distribution

Related to the note 6, the two cases that include one unknown valuation are

If the high value bidder is uninformed of both of his opponents, he is indifferent among all the elements of supports of the distribution

If the high value bidder knows that both of his opponents are high value bidders, then there must be a constant

If the high value bidder knows that his opponents have different valuations each other, then there must be a constant

Rearranging the Equations (5), (6) and (7) to get

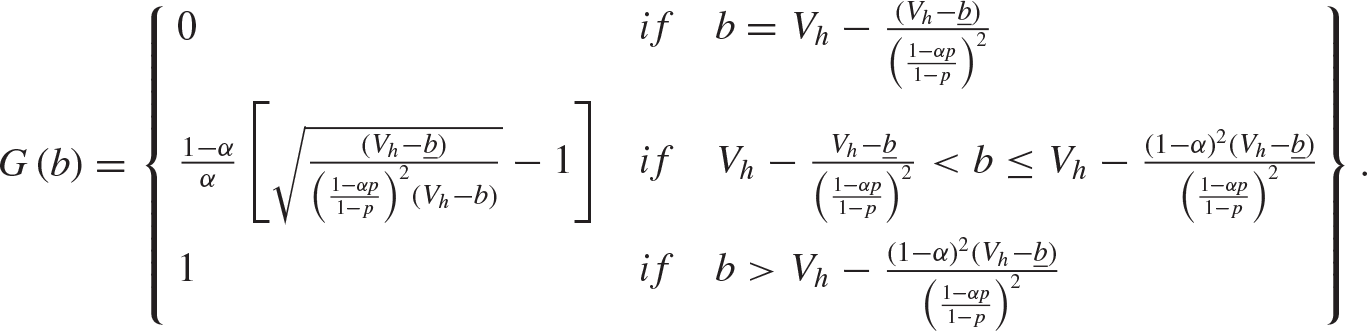

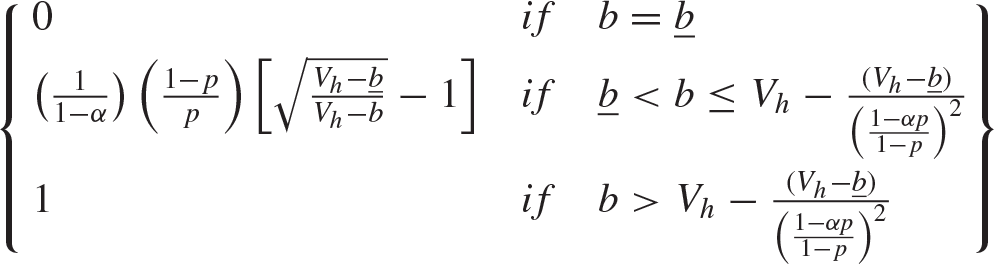

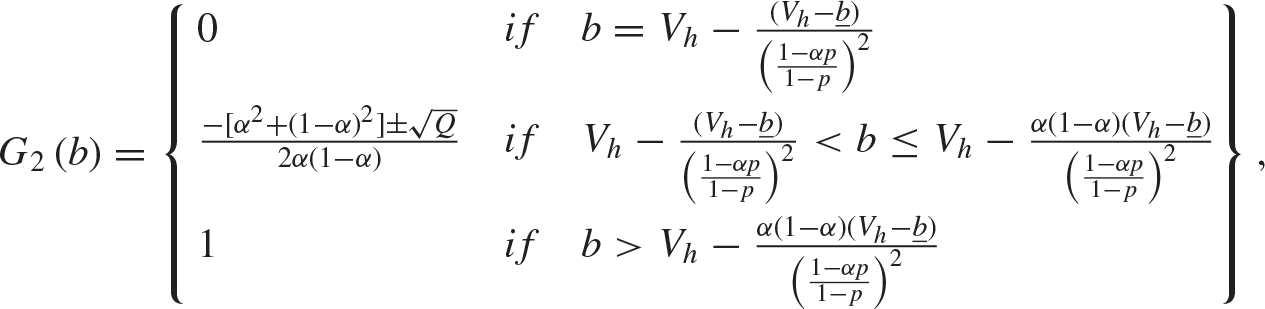

From the Equations (8), (9) and (10), the distribution functions are derived as follows

Because the two cases of high value bidders described in Equations (9) and (10) are mutually exclusive, the conjecture is verified using a set of conditions from Equations (11) and (12) and another set from Equations (11) and (13). To determine

The assumption that there is no mass point at

First, for

The upper bound of the support for

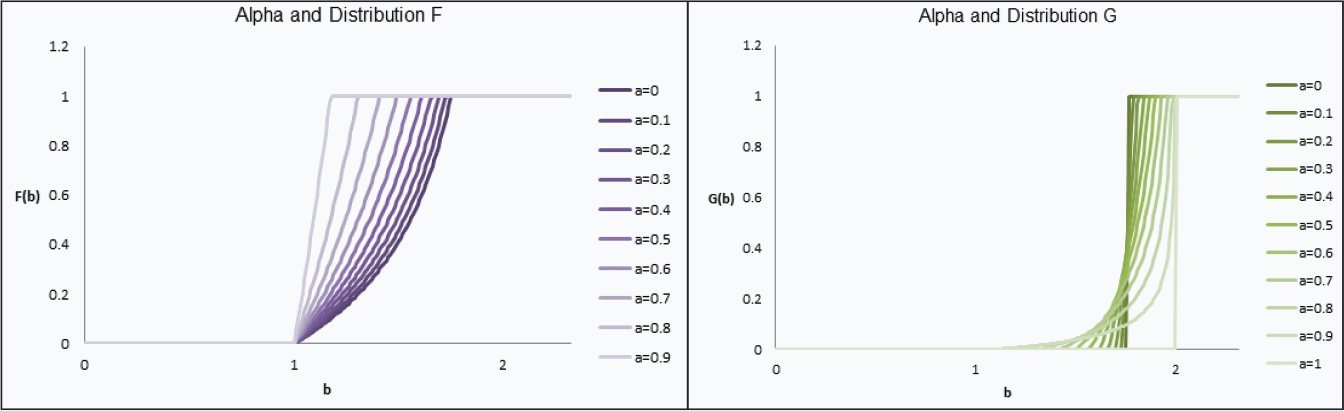

Figure.3. Alpha and Distributions

and

in the Three-bidder Model

From the conjecture about the upper bound,

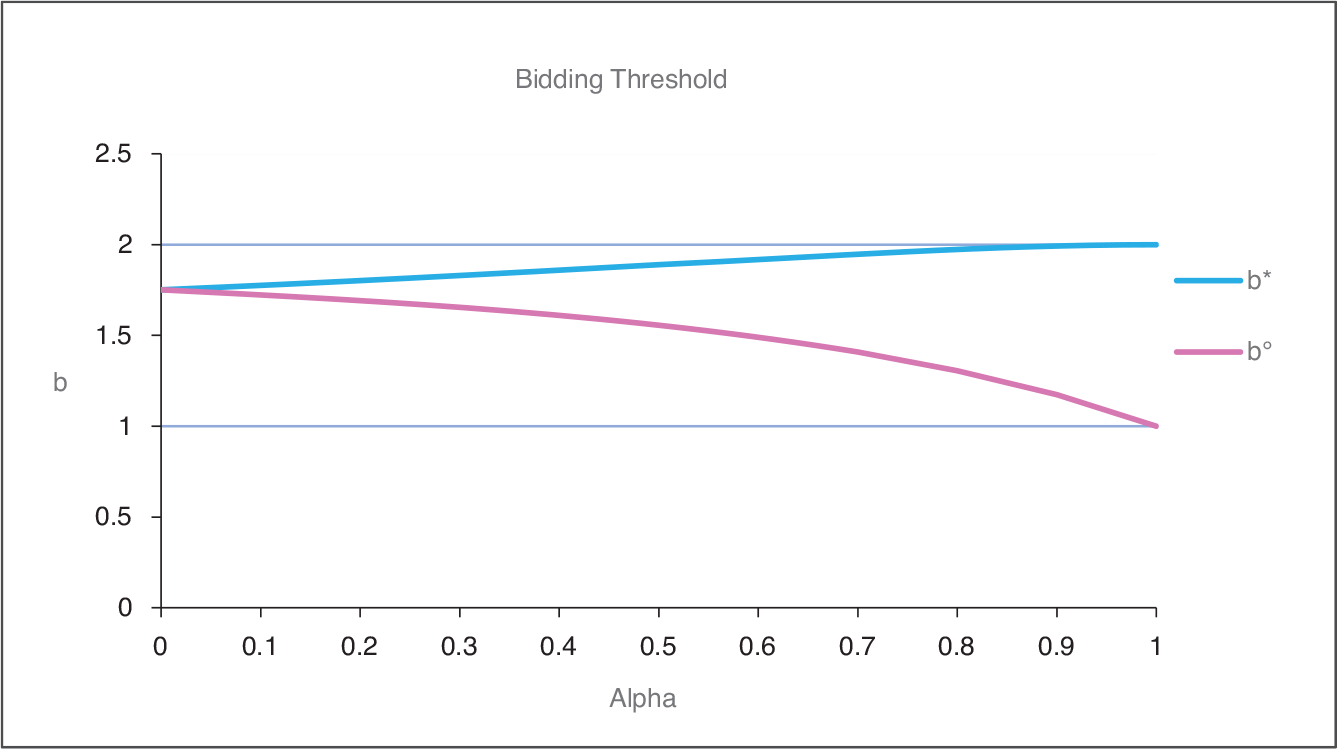

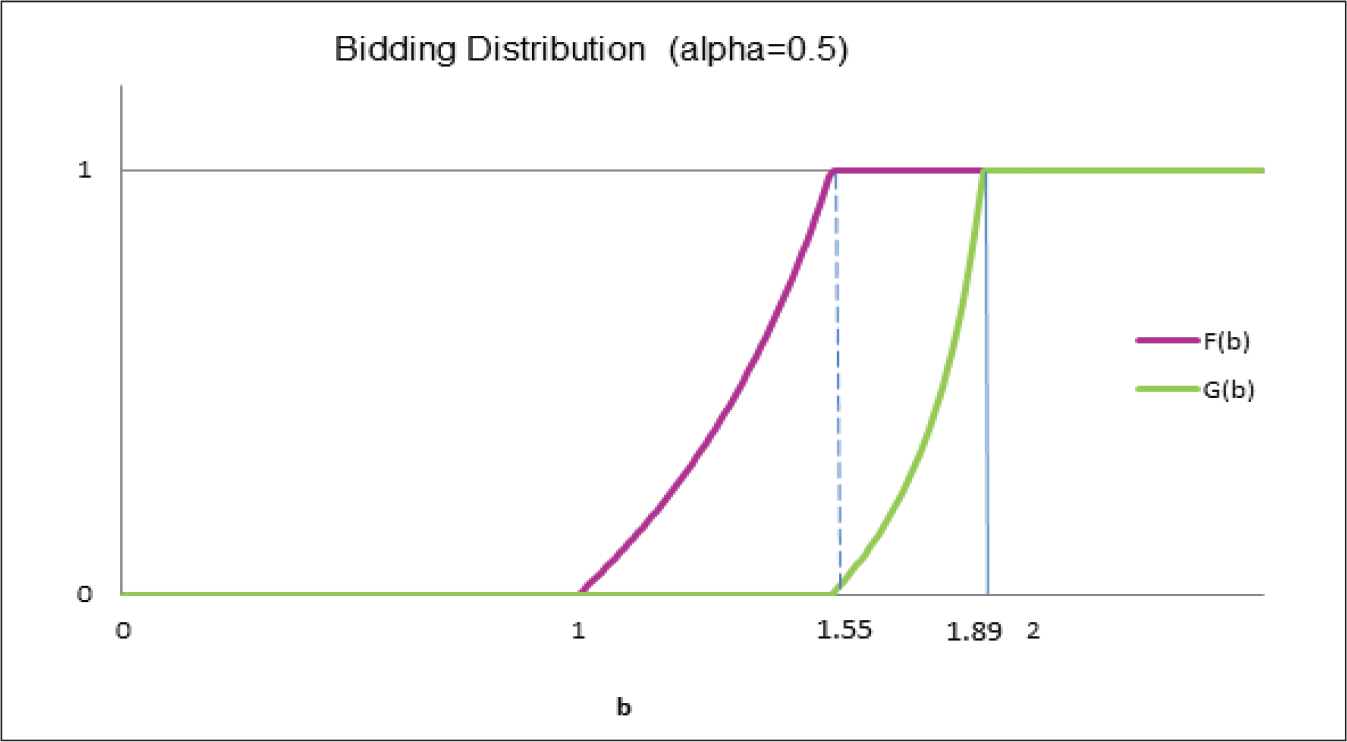

Figure 2 shows the bidding thresholds,

This finding is confirmed by Figure 3 which demonstrates the relationship between

Figure 4 shows the two distribution functions,

and

with

With the conjecture

Comparison and Extension

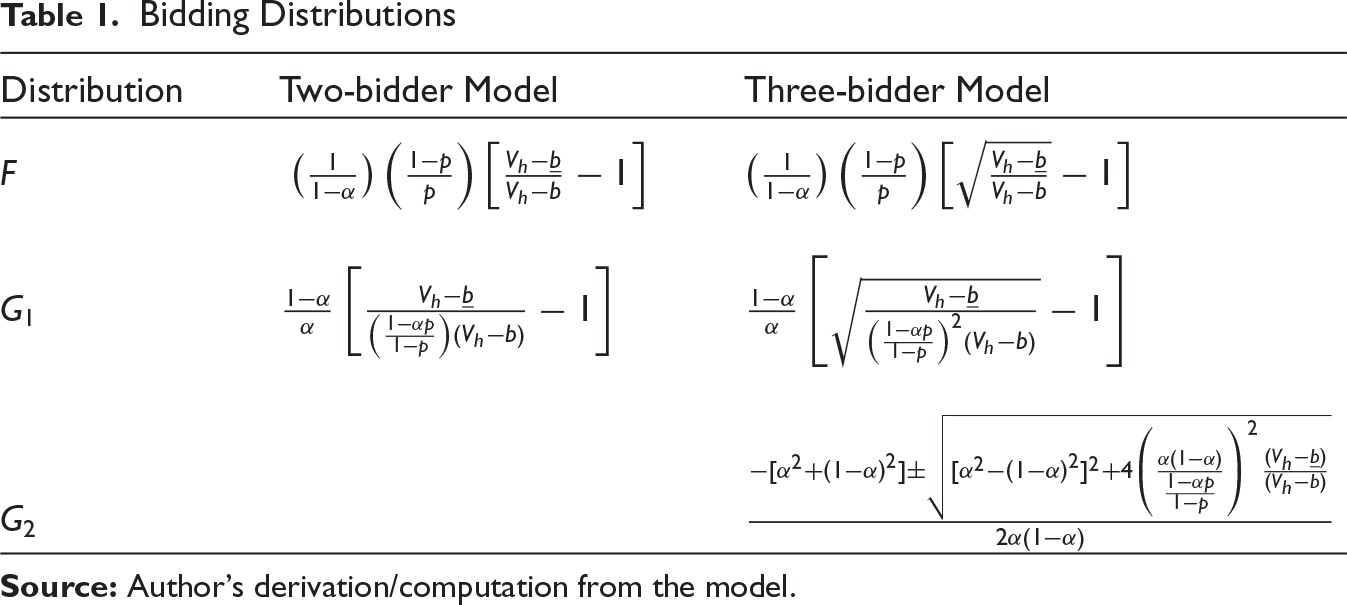

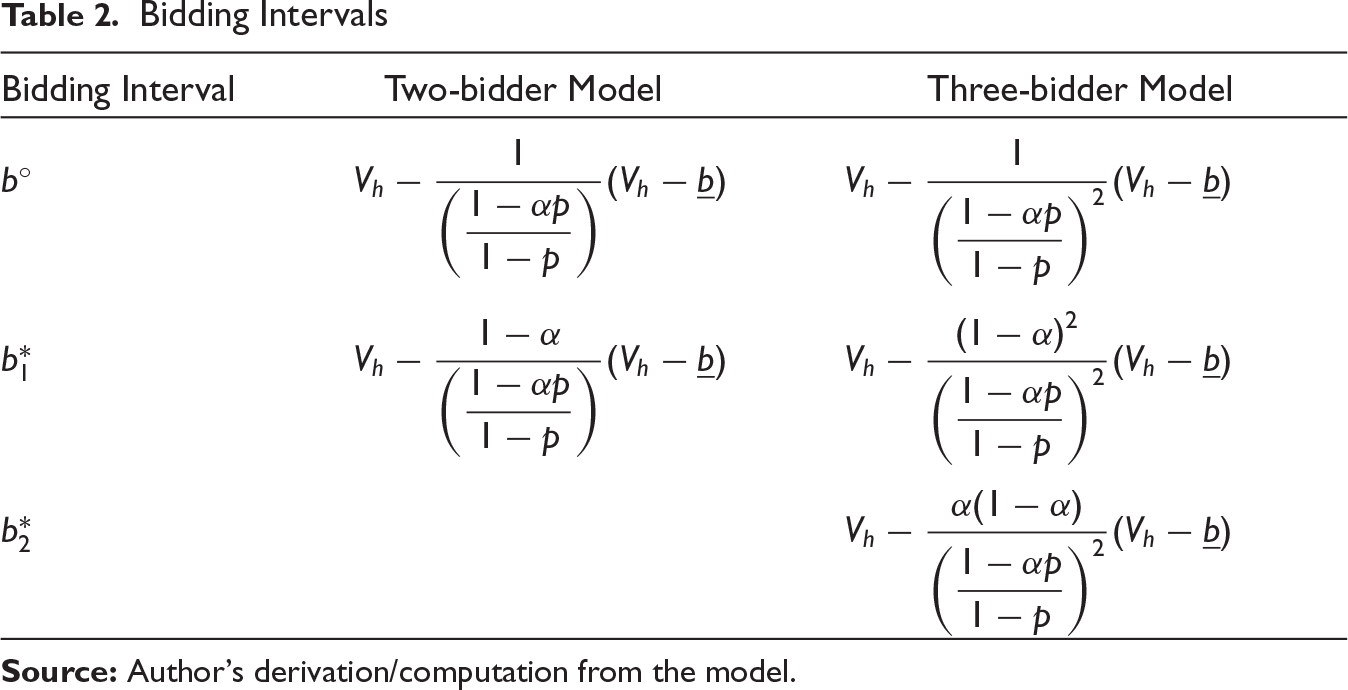

The following two tables summarize the main finding. The tables also include the simplest two-bidder case for comparison. Table 1 shows the bidding distribution functions for the case of the two-bidder model and the three-bidder model. Table 2 shows the bidding intervals to support these.

One may notice the pattern of the distribution functions and the bid intervals over the number of bidders. For any number of bidders

Bidding Distributions

Bidding Intervals

and

Conjecturing

Therefore,

Figure.5.

and Distribution

and G

Figure 5 shows the relationship between the numbers of bidders

Concluding Remarks

The degree of information a high value bidder has access to is crucial to the bidder’s optimal bidding behaviour. Under the assumption that a high type bidder has equal beliefs regarding the opponents’ types, this paper derives closed form solutions for the equilibrium bidding behaviours parametrized by the degree of information. Given a fixed number of bidders, the bidder’s winning bid is increased as more information about potential high type bidders is available. With more information, the support of the distribution function designed for an uninformed high value bidder decreases, while that of the distribution of an informed high value bidder increases. This implies that the bidders not only tend to bid more aggressively but also utilize wider bidding ranges for mixed strategies.

Introducing more bidders with beliefs into a FPA environment would produce a more realistic bidding case. However, as the number of bidders increases, the supports of the distribution functions for an uninformed high value bidder increase, whereas those of the distributions of an informed high value bidder decrease. This implies that the value of information may be limited by the number of participants: the greater the number of participants, the less the value of information about high type opponents. As such, under this environment, the informed high value bidder’s utility decreases along with it.

Comparing with second price auction (SPA), note that to the bidders, FPA with information is more beneficial than SPA because bidders in FPA can utilize information to their advantage. On the other hand, the FPA is worse for the seller’s revenue, since bidders take advantage of available information. Naturally, the revenue equivalence does not hold. Generally, in this model setting with information, the FPA offers the seller no greater expected revenue than the SPA in any equilibrium.

Although the equilibrium in FPA with multiple valuations is likely to be inefficient in a general setting, or perhaps may not exist at all, there may exist systematic approaches which can analytically characterize the multi-valuation auctions with overlapping distributions. This is still an open question to explore in proper detail.

Appendix

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.