Abstract

India and the world went through a public health and humanitarian crisis due to the outbreak of the COVID-19 pandemic in 2020. This article aims to understand the various instruments deployed for tackling the economic side of the crisis and their impacts. It discusses the monetary policy measures that could have been appropriate to tackle the pandemic and the policies deployed by the Reserve Bank of India (RBI) in conjunction with the fiscal stimulus by the government. Subsequently, it discusses fiscal stimulus packages, the need to direct them from the suppliers’ end, and other subsistence policy measures such as food crop transfers and adjustments in federal fund allocations. Policy recommendations discuss the role and importance of stakeholder engagement and investment in the healthcare sector for capacity enhancement and job creation as a short-term relief plan and for a post-pandemic sustainable exit for appropriately handling the pandemics that may follow in the future, respectively. The conclusion advocates the adoption of a policy mix. Then it discusses further challenges, such as the non-availability of literature on the impact of non-traditional policy solutions and the establishment of mechanisms to quickly test policies’ operational feasibility. It culminates with the emphasis on the paradigm shift in the joint approach of the government and the RBI to put the economy back on the trajectory of high growth, which was severely impacted by the sudden and unanticipated pandemic shock, and the way ahead toward becoming a global economic superpower.

Introduction

India reported its first confirmed case of the COVID-19 pandemic (‘pandemic’ hereinafter) on January 30, 2020. This marked the beginning of the humanitarian crisis, which recorded 4.49 crore confirmed cases and 5.31 lakh deaths (World Health Organization, 2023), making the country suffer for the next few years. Major industries, factories, retail shops, medium and small enterprises (MSMEs), and a host of other businesses had shut operations, while only essential services and e-commerce websites delivering necessities were operational. What ensued next was an exodus of these informal sector workers from their cities of employment in the urban pockets of India to their villages—often by foot for the lack of better transport facilities, as is the picture associated with India’s initial lockdown in the minds of many (Renganathan & Mishra, 2021). Imposition of office shutdown, restrictions in travel, and social distancing measures resulted in disruptions in supply chains, reduced consumer demand, and led to widespread unemployment. Albeit deeply symbolic of what was to follow, the Indian economy began slowing down even more than what it had in 2019. Production activity in the country had come to an awful sluggishness if not a complete halt, and the Indian economy was reeling under tremendous pressure. Many small and medium businesses forced shut, manufacturing-related factories that relied on workers’ close proximity with machinery and raw materials came to a grinding halt (more so due to global supply chain disruptions), the services sector changed face, and the digital economy boomed in India, as in other parts of the world. International agencies like Moody’s had already cut India’s projected growth forecast from the already low 5.8 to 2.5 percent in 2020. Goldman Sachs predicted a growth level of 1.6 percent, and Fitch Ratings expected growth to settle at close to 2 percent (Nahata, 2020). Agricultural food prices also suffered during this period of lockdown. Industry analysts predicted large-scale layoffs, debt defaults, bankruptcies, and even loss in investor confidence. Just when the economy was opening and seemed to be moving slowly toward its normal operations between January and March 2021, the most disastrous second wave spearheaded by the delta variant struck the country in early April 2021. The next two months wreaked havoc for the people, which was visible in the rapid spread of the contagious virus, huge shortage of beds for infected patients, and large number of deaths across the country. It did not even spare the population residing in the hinterlands of our country. The government had no time to plan but act swiftly to minimize the widespread damage. Large temporary facilities were set up, with public places and hotels converted to medical centers. The government also quickly jumped on to expand the immunization policy by covering people above 18 years of age who were not prioritized in the initial phase. This definitely was effective in preventing the spread of infection and also made the virus feeble, thereby not impacting the infected severely in future waves. All these problems had severely impacted the foundation of the economy and left the MSME and, especially, the unorganized sector in a very bad shape. This was evident in the closing down of operations by a huge chunk of start-ups operating in the ecosystem. No one had anticipated such a global shock with such dire consequences. Additionally, what loomed large at the Government of India’s (GoI) head was the question of welfare because the pandemic hit India when the country was already grappling with pre-existing economic challenges. With the informal sector making up the larger chunk of the economy, digitization a faraway call, and other developmental gaps, how was India going to navigate unemployment, hunger, depressed wages, and related challenges that the pandemic was expected to bring (Chandra & Mansoor, 2022)?

As an impending recession looked India in the face, the challenge for the government was to adopt the right kind of economic policies to deliver on the targeted V-shaped recovery, which conceivably is an expected negative growth for around a quarter or two, before making a pragmatic shift toward growth. Taking a cue from major global financial crises, many experts argued for the central bank to dive right in and adopt adequate monetary policy measures to help cushion economic losses for India and also put it on the path to recovery. However, on deeper evaluation it had been observed that central banks of countries have only limited power to pull out economies from a crisis of the nature of COVID-19. Usage of monetary policy alone, as had been pointed out by various industry experts, was inept at dealing with the entire nature of the crisis at hand and may also would have led to this crisis, paving the way for a different kind of problem in the long run.

To address the economic fallout, India’s strategy stood out—it planned and implemented a right mix of monetary and fiscal policy measures rather than being heavily inclined toward one. That coupled with the other onslaughts the globe suffered as a whole in the period between when the pandemic first struck and the present—such as the Russia–Ukraine war, climate crisis, change in government and economic structures, etc.—helped the country navigate a period of extreme uncertainty with some amount of caution and grace. The World Bank reported that India’s GDP (measured as the market value of all goods and services produced within a country during a particular year) growth rate fell from 3.7 percent in 2019 to −6.6 percent in 2020 (recovering to a steady 8.7 percent in 2021 (Figure 1), which we will discuss later) (World Bank Open Data). Agricultural prices began rising soon after, as did debt defaults and bankruptcies. Yet, India’s path toward recovery remained steady, notwithstanding the occasional bumps. Jumping to the present, after deep contractions in 2020 caused by the pandemic, we witnessed accelerated growth in 2022 as well as in 2023, with real GDP growth expectation for FY2022–2023 as high as 7.0 percent year-on-year (S&P, 2023). This article aims to study the evolution of policy measures that helped India achieve this trend from the pandemic to 2023.

India’s Approach to Policymaking in Response to the Pandemic

During the rise of the pandemic, all available switches for economic stabilization were used including fiscal, monetary, and prudential measures to keep the economy afloat post-contraction in economic activity during the lockdown. A significant portion of resources had to be allocated to address the increasing healthcare expenses and sustain the livelihood of the workforce. In the immediate aftermath of the crisis, the primary challenge for national authorities was to revive economic activity. Financial markets encountered significant pressure due to the extreme volatility in equity markets and the capital outflows from emerging market economies, leading to currency pressures. Consequently, maintaining sufficient liquidity and ensuring financial stability emerged as the two primary concerns. As a result, both monetary and fiscal policies worked in conjunction to provide support for economic growth. In the subsequent sections, we present a broad overview of some of the policies announced by the government and the Reserve Bank of India (RBI) since the onset of the pandemic (BIS, 2022).

Monetary Policy Measures and Their Impact

The aim of the monetary policy changed from enhancing liquidity and stabilizing the economy during 2020 to boosting real economic growth in 2022–2023 and beyond. The Indian government had been looking at monetary policy measures to handle the liquidity crisis in India through a variety of measures. The RBI had been doling out a plethora of financial options that could serve as paths to be taken to cushion the monetary impact of the COVID-19 outbreak that had stalled economic activity. Often defined as the lender of last resort, the RBI’s objective of stepping in was to simply increase liquidity in the economy, which was at that time at an all-time low, given the economy’s sluggish growth. Market research studies showed how the final consumer demand for non-essential products had fallen in comparison to items of necessity. In addition, with the lockdown in place, services such as salons, restaurants, transport, tourism, etc., were also hit, and the demand for intermediate goods that arises from these units in the economy was also observed to reduce. Production processes had been hit and wages too. The GDP, which measures the final value of goods and services produced in the country in a given year, was expected to take a serious hit as described above and, hence, infusion of liquidity in the economy was crucial to keep its gears greased.

During the pandemic, the RBI undertook several crucial monetary policy measures to tackle the economic challenges and maintain stability in financial markets. The primary objective was to ensure stability and liquidity in the economy, while addressing capital outflows, managing government borrowing, and supporting growth.

RBI deployed the tools of open market operations (OMOs) and changes in the repo rate to achieve that objective by increasing money supply in the economy. The definition of money supply that the RBI uses has broadly two components—currency notes with the public and other deposits, with RBI adjusting for items such as net monetary liabilities of the government to the public, National Savings Certificate, net bank credit to government, net foreign exchange assets of the banking sector, etc., (RBI, 2007). For the sake of simplicity, we can simply assume that the two types of components of money supply are cash based and credit/savings based. The credit component is included in money supply since the deposit of savings with commercial banks helps them create subsequent rounds of credit by the lending process and the rate at which the initial batch of deposits leads to creation of more deposits (called multiplier) helps increase money supply in the economy manifold times.

One of the ways that the RBI was looking at increasing money supply was by purchasing government securities from the open market in exchange for money. The rise in COVID-19 infections had resulted in tighter financial conditions in several sectors of the economy. The manifestations of the drying of liquidity were visible in the form of wider interest spreads and hardened yields. This was the most propelling reason to induce RBI to resort to OMO for liquidity infusion to maintain the financial health of the cash-strapped sectors. RBI had conducted three tranches of OMO in March 2020. The first one, on March 20, 2020, was worth ₹10,000 crore; the second, on March 24, 2020, was worth ₹15,000 crore; and the third tranche, on March 30, 2020, was worth ₹15,000 crore (The Economic Times, 2020). The second of the above-mentioned tools was that of changes in the repo rate set by the RBI to directly affect the credit component of money supply. The repo rate refers to the rate at which commercial banks, which deal directly with the general public, borrow funds from the RBI. It was reduced by 75 basis points from 5.15 to 4.40 percent. The idea was that a lower rate of lending to commercial banks would induce them to reduce interest rates on loans that they further extend to the general public, thereby increasing the amount of money available with public as currency or deposits. The marginal standing facility (MSF) margin was also reduced simultaneously from 5.40 to 4.65 percent. A similar idea for increasing commercial banks’ lending capacity was the reason behind this move as well (RBI, 2020).

Implications of Reduced Interest Rates

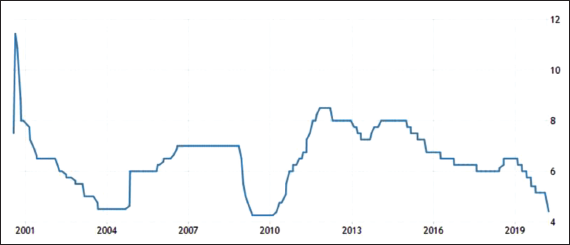

The Indian Monetary Policy Committee unanimously voted in late March 2020 for a repo rate stashing by the RBI for mitigating the impact of COVID-19 outbreak on the economy and reviving growth. The repo rate was stashed by 75 basis points from 5.15 to 4.4 percent in March 2020, the lowest rate recorded in RBI’s history in this century since the year 2000 (Figure 2). Alongside, it also fixed the reverse repo rate, which sets the floor for the liquidity adjustment facility (LAF) corridor, stashing it by 90 basis points to settle at 4.0 percent. This asymmetric corridor was created to ensure commercial banks deposit minimal funds with the RBI and instead lend them out.

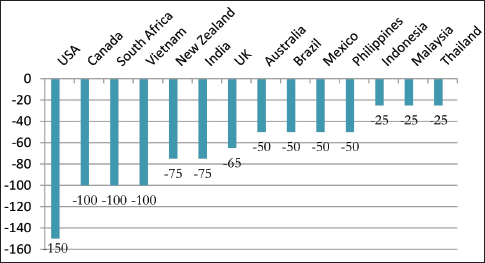

The economic pain of the crisis was being felt globally, and high-income and low to middle income economies alike were making substantial rate cuts for a cushioning in fall (Figure 3). India was far from being the only one resorting to extreme rate cuts. People’s Bank of China cut the interest rate on reverse repurchase agreements by up to 20 basis points in March, the lowest in five years, from 2.40 to 2.20 percent. The central bank in New Zealand also cut rates by 75 basis points like India, and countries like Australia injected major amounts into the economy through OMOs. USA had meanwhile joined the ranks of countries slashing the interest rate maximum.

The prevailing lower domestic interest in the economy presented an added benefit of inducing the investors to ramp up investment in the economy, besides the added liquidity from RBI’s operations. However, this may not have been very effective in improving the situation in the economy. Some of the major problems that can be attributed to lowering of interest rates can be described as follows: First, an understanding of the economic impact of the current situation helps aide the understanding of the requirement for relief packages. Production process can be understood as the result of culmination of four factors—fixed capital such as land and machinery, variable factor like labor, monetary capital, and entrepreneurship skills offered by the manager or authority. With the COVID-19-prevention-based lockdown in place, barriers to production were largely stemming from a lack of availability of sufficient labor and to some extent monetary capital. A reduction in the interest rate payable on loans availed by investors in the economy had been proven to imply increased investment. However, assuming that this investment would in most parts be toward infrastructure development as prior studies had indicated, the need for it was almost negligible. The coronavirus global pandemic had not implied any significant depreciation or loss in capital in the economy, and hence, a boost to capital by the incentive from reduced interest rates was not expected to help in damage repair.

A second point to be noted in the case against the effectiveness of reduced interest rates to help the economy is the distinction between domestic and foreign investment. Interest rates payable on bonds or other financial instruments through which investors invest and interest loans to be paid back on loans availed by investors/capital creators differ by the amount of spread that accounts for items like the profit of the intermediary institutions, taxes, etc. Generally, the former is less than the latter. Putting this in the context of the above-mentioned policy undertaken by the RBI, the conclusion that follows is that while reduced domestic interest rates may imply higher domestic investment, they are the reason behind reduced investment in India from abroad. Reduced interest rates in India may also lead to flight of existing capital in India and even that of Indian investors to investment options abroad as Indian interest rates on investment might fall below that of the world average. Assuming a hypothetical condition in the future when this happens, it would lead to India’s exchange rate depreciating against the US dollar. If we take into account the results of empirical studies that indicate a slower adjustment of volume effect to exchange rate changes (J-curve), it implies that in the short run, a higher exchange rate for the Indian currency would translate into a higher value of Indian imports, pushing our GDP figure further lower down.

A last point toward this end is that reducing interest rates might have led to the transformation of the nature of the pandemic crisis, thereby laying the foundation for another one. The coronavirus crisis can be described as an exogenous crisis, one that hits the economy like an absolutely external factor, a meteor strike on earth. This, namely, an endogenous crisis that arises out of endogenous market responses of market participants itself, like the crisis of 2008, had very different consequences and repair measures (Danielsson, Macrae, Vayanos, & Zigrand, 2020). The 2008 crisis stemmed largely from the sub-prime mortgage security problem and the boom in the housing sector. This crisis was a systemic one and could be repaired adequately by monetary policy measures to a great extent. However, solely deploying monetary policy to deal with the crisis would have only exposed the economy to a subsequent systemic crisis. The objective of the RBI was to increase the amount of loans issued, which was expected to be served by the reduced interest rates. With banks in the country functioning at minimal capacity during the pandemic, something that was expected to be the same in the time of staggered exit from the lockdown too, commercial banks were severely understaffed to monitor and regulate the huge volumes of loan issues, thereby opening up the Indian banking sector to the moral hazard problem. To add to this, factoring in that the Indian government had already considered redefining periods after which an asset is classified as an NPA, the risk of moral hazard would be compounded even further and we would potentially be looking at a credit boom (and a subsequent crash) in the face. NBFCs and private sector banks could similarly not be relied upon totally to not get trapped in this problem, especially with the stock market swings. Lower interest rates had potentially opened up the economy for consequences arising out of the domino effect from systemic risks.

Challenges of Financing the Deficit

As per a report from Oxford Economics, the GoI was expected to incur an expenditure of $18 million to sufficiently deal with the ongoing crisis. This was inclusive of cash handouts of ₹5,000 ($65.8) a month for 50 million workers for a quarter, which would entail an outgo of ₹750 billion and all other expenditure on food transfers. Economists at Bloomberg had suggested that India would need about 1 percent of its GDP to successfully manage the crisis, nearly amounting to $30 million (Nag, 2020b). A fiscal stimulus package of ₹1.7 lakh crore (nearly $22.5 billion) had already been doled out by the Indian finance minister, Shrimati Nirmala Sitharaman.

The Fiscal Responsibility and Budget Management (FRBM) Act permitted India’s fiscal deficit to remain within 3.5 percent of the GDP, but at that time the deficit was estimated to be pushed to as high as 6.2 percent as per reports from Fitch Ratings (Nag, 2020a).

The obvious challenge then was to understand how GoI would finance the deficit. The two routes discussed in the following sections were the expected paths for the same, along with the further challenges that both presented.

Deficit Financing

Since the economy was facing liquidity crunch, borrowing money from the public was not a viable option for the government. This left the government with the other option of borrowing from the lender of the last resort. This path required the GoI to borrow from RBI, which in turn would lend by printing currency notes. As explained in the previous section, when the government would inject the additional money into the economy either through OMO or a higher amount of loans given, the immediate effect would be a registered rise in the domestic money supply and lower interest rates. The effect of this was expected to unfold in two stages. In the short run, since the commodities and services market adjusts slower than the money/asset market, the aggregate price level in the economy in the short run would not have been very volatile. However, in the long run, with the aggregate supply already shrinking due to the lockdown barriers, increasing money supply would have led to inflationary pressures as deflation of the lockdown would have formed adverse expectations in the minds of the suppliers. With a rise in inflation, real money supply would have also contracted, pushing the price level downward. This heightened price volatility was not expected to do well to an economy that was already struggling to recover after being brought to its knees.

Additionally, given the lockdown, the problem would have been severely exacerbated since the goods and services market was more sluggish than ever to adjust. Experts who argued that inflation was not a concern for the government at that time must have taken into account that while the lockdown (and for that matter any social-distancing measure other than a full-scale lockdown) was in place, inflation might not have been such a big concern. However, once scaling down of social-distancing measures began and the economy started to open up, the goods and services market began affecting the price level in the economy sharply. A V-shaped recovery in such a scenario would look extremely difficult as the rate of recovery was being curtailed by the growing inflation, with a magnitude depending on the economy’s price elasticity and resilience.

Borrowing from Foreign Agencies

If the government borrowed from foreign governments, the liability to pay back in the future with an interest might have again led to inflationary pressures and the same conclusion as mentioned above. Foreign unconditional grants received from international agencies might not pressurize the government in terms of inflation but could finance current consumption needs at the cost of capital the government might have required at later stages of recovery for investment and capacity enhancement purposes in the economy. Thus, it raised the major issue of intergenerational cost spreading.

Therefore, the traditional monetary policy was in itself inept at preventing further economic losses for India as it battled the coronavirus pandemic and at being the driver for India’s recovery from it.

The government had, however, also been looking at other measures simultaneously to avoid India from slipping into the economic distress by managing its costs and looking at means to increase the amount available for expenditure. The central government had been diverting funds from other expenditures to finance the current requirements in the public health emergency. For instance, it suspended the Member of Parliament Local Area Development (MPLAD) Scheme for two years, 2020–2021 and 2021–2022, which was expected to leave an estimated ₹7,900 crore with the government for expenditure. Alongside, cuts in dearness allowances (DA) of government employees, a 60 percent cut in the expenditure of government ministries, and cuts in salaries of ministers were some of the other ways the government was reducing its expenditure (Bhattacharjee, 2020). The cut in expenditure was almost mandatory for the government in light of the crunches in both tax and non-tax revenues for the government.

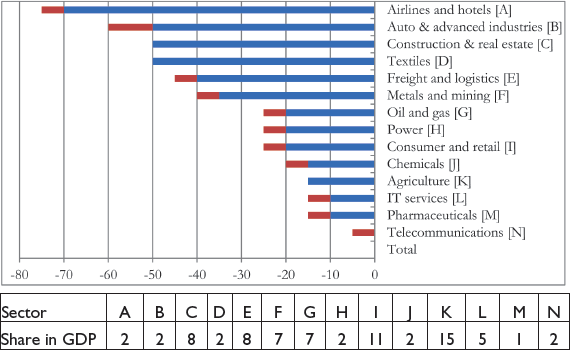

The past crisis had led to a deep impact on various sectors of the economy, and effects were expected to continue to show up. The output in that financial year was expected to register highly differentiated year-on-year growth rates across various sectors. It was expected that the maximum burden of the lockdown would be borne by sectors such as aviation, travel and tourism, automobiles, hospitality, and traditional entertainment industry. Service sectors and essentials were faring better, yet even enabling services such as IT, which required physical proximity, were taking a cut (Figure 4).

Other Policy Measures

The exogenous nature of the coronavirus pandemic and the associated economic crisis called for countries all over the globe to consider other policy measures.

Putting the past situation in perspective, due to restrictions on movement and reduced or negligible operation timings for retail shops, the economy was facing deflationary pressures (OECD, 2020). The amount of goods and services traded in the economy was significantly lower than usual since on the demand side consumers were restricted from spending on items like eating out, salon services, travel and tourism, etc. On the supply side, the lockdown had prevented easy access of plants and factories for labor, besides the breakdown of traditional supply chains and easy access to raw materials. With help from circular economy models, it could therefore be understood that since the total value of the output of goods and services produced and exchanged in the economy was below par (or what economists would call optimal/full employment level of output), income and employment in the economy were also falling short. Objectives of all policy measures were, thus, to ensure to bring the economy to the optimal level of the above-mentioned parameters.

To alleviate volatility and stabilize global financial markets, the RBI employed foreign exchange swaps as an effective mechanism to manage the impact of capital flows. In early 2020, the Indian rupee (₹) reached its lowest level at ₹76.81 per USD. However, when compared to several other emerging market currencies, the depreciation of the Indian rupee was relatively moderate. These measures played a pivotal role in maintaining stability amid uncertainties, prioritizing the overarching objective of the RBI. Adopting a comprehensive approach, the RBI focused on enhancing liquidity across all market segments. Measures such as long-term repo operations, OMOs, and widening of the monetary policy corridor were implemented to infuse liquidity into the system. These, along with purchases of foreign exchange, successfully expanded liquidity, as visible from average daily net liquidity absorptions under the liquidity adjustment facility (LAF), from ₹3.43 lakh crore at the end of January 2020 to ₹5.47 lakh crore in January 2021. By facilitating the smooth functioning of financial markets, these actions aimed to bolster overall economic stability, aligning with the primary objective of the RBI (GoI, 2021). Recognizing the economic downturn caused by the pandemic, the RBI’s Monetary Policy Committee (MPC) took decisive steps to stimulate economic activity. Through rate reductions, MPC aimed to encourage borrowing and investment, supporting the broader goal of ensuring stability and liquidity in the economy. With a cumulative reduction of 250 basis points (inclusive policy rate cuts since February 2019), these measures were intended to provide vital support for economic growth. To ensure the smooth functioning of the financial system, the RBI conducted outright OMOs and “Operation Twist” operations. These operations provided liquidity to the system and facilitated efficient pricing, thereby managing the government borrowing program effectively. In addition, the RBI introduced the Standing Deposit Facility (SDF) in April 2022, allowing banks to deposit excess funds without the need for collateral in the form of government securities. This measure not only enhanced liquidity management but also promoted efficient utilization of resources. Moreover, the RBI increased the limits for temporary Ways and Means Advances (WMAs), providing short-term credit facilities to central and state governments. This increase in limits helped meet the growing demand for funds during the pandemic, supporting government initiatives and ensuring the availability of fiscal resources. Recognizing the challenges faced by small enterprises, the RBI allowed lending institutions to restructure their debt. This step provided borrowers with flexibility in managing their financial difficulties and helped sustain their operations. Furthermore, the RBI implemented sector-specific policies to maintain the flow of funds and support key sectors. It established additional liquidity facilities for institutions such as NABARD, SIDBI, NHB, and EXIM, addressing their specific funding requirements and aiding their functioning. In light of the contraction in foreign trade, the RBI implemented measures to boost export credit and extended the time for payment for importers from 6 to 12 months. These actions aimed to support the foreign trade sector, which faced significant challenges due to the pandemic-induced disruptions. The steps taken by the RBI exemplified its commitment to ensuring liquidity in the financial system and supporting the overall economy during the unprecedented crisis. These measures were designed to alleviate financial pressures, stimulate economic growth, and maintain stability. By adopting a proactive approach and implementing targeted policies, the RBI played a crucial role in mitigating the adverse impact of the pandemic and supporting the recovery process (BIS, 2022).

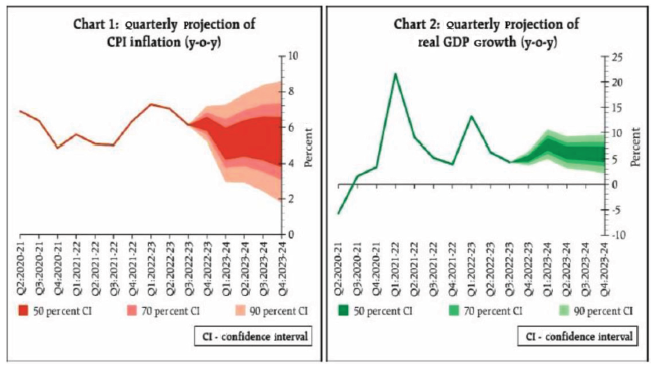

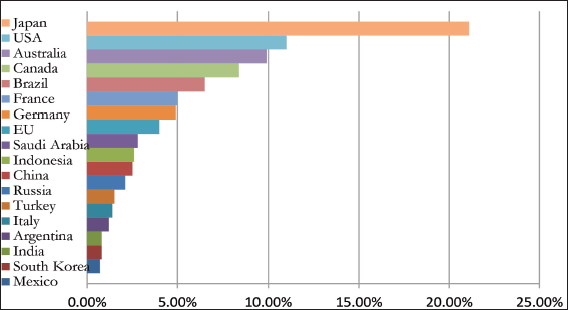

As stated earlier, post-pandemic, the objective of RBI transitioned to supporting sustainable economic growth. With regard to the same, recently, the RBI has given a green signal to the early stages of the monetary tightening cycle, as it aims to balance supporting economic growth while gradually withdrawing the accommodative measures. Since the past two years, the Indian economy has made a remarkable recovery from the impact of the pandemic (Figure 5). It has surpassed many other countries (Table 1) and is on track to return to the pre-pandemic growth path (GoI, 2022).

Global Economic Challenges Led to a Downward Revision in Growth Forecasts Across Countries.

However, India has faced the challenge of managing inflation, which has been intensified by the economic turmoil in Europe. The government and the RBI have taken measures to control inflation, and the easing of global commodity prices has helped bring retail inflation within the RBI’s target range by November 2022. Despite the Indian rupee performing relatively well compared to other currencies, it still faces the challenge of depreciation, especially considering the possibility of interest rate hikes by the US Federal Reserve. The current account deficit (CAD) may also widen due to elevated global commodity prices and the strong growth momentum of the Indian economy. Additionally, there is a potential loss of export stimulus as global growth slows down and the size of the global market shrinks in the latter half of the year. In FY23, inflationary pressures have dominated the global economic landscape. The increase in prices, along with the economic recovery, was initially seen as temporary and expected to subside as supply chains normalized. However, the conflict in Europe that erupted in February 2022 caused commodity prices to skyrocket, adding to the existing inflationary pressures. This situation has led to a significant and coordinated tightening of monetary policies. Between May 2020 and February 2022, the MPC kept the policy repo rate unchanged, following a reduction of 115 basis points (bps) between March 2020 and May 2020 (Figure 6). However, retail inflation surpassed the upper limit of RBI’s tolerance band starting in January 2022 (Figure 7). Recognizing the substantial risk to price stability, the RBI initiated a monetary tightening cycle. In April 2022, during their meeting, the committee introduced the SDF as a collateral-free method for banks to deposit excess funds with the RBI. The SDF facilitated efficient liquidity management, primarily for overnight deposits, while allowing the RBI the flexibility to absorb surplus liquidity of longer tenors if needed, with appropriate pricing. The SDF, with an interest rate of 3.75 percent, replaced the reverse repo rate as the new floor of the LAF corridor (Figure 6). Furthermore, during the meeting, the MPC signaled a shift in stance from “Accommodative” to “Accommodative and focused on the withdrawal of accommodation, while supporting growth.” This indicated the onset of the monetary tightening cycle, as the RBI aimed to strike a balance between supporting economic growth and gradually scaling back the accommodative measures (GoI, 2022).

In the MPC meeting on April 6, 2023, based on current and evolving macroeconomic situations, it was decided to keep the repo rate under LAF unchanged from the last change made in February 2023. As of the writing of this article, the repo rate stands at 6.5 percent, SDF at 6.25 percent, reverse report at 3.35 percent, and bank rate at 6.75 percent (RBI, 2023). The RBI has adopted a strategy to stimulate economic growth by adjusting key interest rates. In this endeavor, the RBI has increased the repo rate while keeping the reverse repo rate stable. This move aims to incentivize lending by making loans more attractive, without impacting the interest rates offered on deposits. The repo rate is the rate at which commercial banks borrow funds from the RBI, and an increase in this rate implies that banks will have to pay higher interest when accessing funds from the central bank. By raising the repo rate, the RBI aims to make borrowing costs higher for commercial banks. This, in turn, prompts banks to increase the interest rates they charge on loans to consumers and businesses. The objective is to discourage excessive borrowing and spending, which can lead to inflationary pressures in the economy. Higher interest rates on loans encourage individuals and businesses to be more cautious in their borrowing decisions, promoting a more sustainable and balanced growth trajectory. At the same time, the RBI has chosen to keep the reverse repo rate stable. The reverse repo rate is the rate at which the RBI borrows funds from commercial banks. By maintaining this rate, the RBI ensures stability in the interest rates offered on deposits. This strategy helps preserve the attractiveness of saving and encourages individuals to continue depositing their funds in banks, fostering a stable financial environment. The combination of increasing the repo rate and keeping the reverse repo rate stable creates a conducive environment for economic growth. The higher interest rates on loans incentivize responsible borrowing and discourage excessive debt accumulation, which can fuel inflationary pressures. At the same time, stable deposit rates provide confidence to savers, ensuring the availability of funds for productive investments and lending activities (RBI, 2023)

Boosting real GDP is one of the primary objectives of RBI’s monetary policy. By influencing interest rates, the central bank aims to strike a balance between promoting economic growth and maintaining price stability. A healthy and sustainable GDP growth rate contributes to overall economic development, job creation, and improved living standards for the population. RBI’s strategic approach of increasing the repo rate and keeping the reverse repo rate stable is designed to support this objective and foster a favorable economic environment in the country.

Fiscal Policy Measures and Their Impact

Fiscal policy can be defined as the stimulus package that the government provides as an injection (or leakage, as per need) into the economy to drive the economic parameters to their optimal value.

The government’s budget can be loosely described as the statement of anticipated revenues (total tax and non-tax revenues) and expenditure of the government. Lower aggregate income levels in the economy due to the crisis had also led to reduced tax and non-tax revenues for the state. Disinvestment targets of GoI, such as that for its national carrier Air India, etc., were already bleak in the third quarter of FY2019–2020, and then they seemed to have plunged deeper down (The Hindu, 2020).

Amid all this, one ray of hope seemed to be the historic fall in global oil prices. West Texas Intermediate (WTI) oil prices had gone below $0 per barrel for the first time in April 2020 since oil futures were due for delivery around that time. With extremely low global demand and inadequate storage facilities for storing oil barrels on delivery, oil future traders had begun to stash them and hence the negative pricing. India as a net importer of oil stood to gain financially from the situation in terms of the reduced value of its imports, which gave larger room for the government to impose fuel taxes and also keep inflation in check (Sharma, 2020).

In the pandemic scenario, the most affected parameters ranged from wages, real output/GDP, price level, and employment. While from an economic perspective a multi-pronged approach to tackle all of those parameters was essential as well as desirable, a crucial point to be understood was that since the fiscal policy is part of the government policy, it often reflects the need and understanding of politicians. In politics, economic recovery translates into generating more jobs, followed by inflation targeting rather than based on bringing output back to its original equilibrium level. To that extent, politicians are willing to add stimulus, fiscal (higher government spending and lowered taxes) as well as monetary (lower short-term interest rates), so jobs start reappearing (Rajan, 2010). Hence, the need of the hour was for the government to deploy fiscal policy stimulus measures to ensure job security. Many economists had argued that this stimulus measure was needed to be given in the form of wage subsidies to employers to retain their laborers and to ensure that the production process did not take a downswing soon. The Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) was an effective policy tool in the hands of the government that could have been used to provide guaranteed wage income to casual laborers. Effective stakeholder engagement programs could have been also deployed to ensure the twin objectives of containment of the deadly virus and economic recovery so that the objective of job creation could be met.

The Organization for Economic Co-operation and Development had estimated that containment measures would lead to a decline in output level by 20 to 25 percent in many economies, and the International Monetary Fund (IMF) projected negative global growth in 2020, citing a global slowdown worse than the Great Depression (Segal & Gerstel, 2020). Governments around the world had announced fiscal stimulus measures to lessen the negative impacts of the COVID-19 outbreak and associated lockdowns (Figure 8). At a March 26 virtual summit, leaders of the Group of Twenty (G20) major economies announced they were spending over $5 trillion, equivalent to 7.4 percent of 2019 G20 countries’ GDP, to “counteract the social, economic, and financial impacts of the pandemic” (Stephanie & Dylan, 2020).

The largest component of the stimulus package was expected to be used for providing financing to businesses. The combined economic injection amounting to nearly $200 billion was believed to be higher than even the support provided in 2008 at the time of the global financial crisis. A major point to be noted, however, is that high-income countries still make up the leading share, while emerging economies lag behind.

Subsistence-based Policy Measures

Across the country, many sections of the society such as migrant workers, laborers, pastoralists, rag pickers, sex workers, and the poor and the destitute were facing risks of extreme starvation as their source of livelihoods had been abruptly dismantled by the lockdown. In fact, a major challenge before the Indian government was the trade-off between saving lives from the deadly virus by imposing social-distancing measures like the lockdown and preventing people from succumbing to starvation and lack of medical intervention for other diseases while the lockdown was in place. As aggregate national savings had fallen at that time of humanitarian crisis, the poor and lowest in the social strata were again the worst hit, since fractions of income saved were anyway lower in these groups. Without adequate savings, it had become difficult for these groups to even access basic necessities and nutritional requirements. Scores of migrant laborers who tried returning to their hometowns had also been adversely hit given the lockdown imposed on transport facilities as well. So then the whole question was for the welfare state to devise immediate policies to tackle the situation at hand.

One of the policy measures that was strongly recommended for the government was to ensure unconditional food transfers and insurance covers at least for the population identified as needy. Food transfers were not just necessary but also within the affordability scope of the government. The Food Corporation of India (FCI) was holding 77 million tons of food grain stocks at that time, more than twice the amount stipulated by buffer stock norms of 24 million tons. Further, it was expected that FCI could procure another 40 million tons from the rabi harvest at that time. As a study by Ghosh, Patnaik, and Mander (2020) pointed out, if universal provisioning of 10 kg of food grain per person per month is undertaken, it is most likely to be availed by around 80 percent of the 1.3 billion population of India, amounting to a total of nearly 62.4 million tons of grain. This 62.4 million was well within capacity of the Indian government to provide and would have helped a massive chunk of the population to evade starvation.

Increasing money allocations for states and union territories given by the center was also one of the ways in which expenditure could be made more efficient. Centralized and customized policies generate wasteful expenditure if differences in state requirements and models are not factored in. For instance, the Agra (Uttar Pradesh), Bhilwara (Rajasthan) and Pathanamthitta (Kerela) models varied in their containment and impact parameters. These models were based on localized community transmission only within hotspots, “ruthless” containment strategy, and technology as strategies, respectively. Allowing respective states to manage their fiscal relief packages as per the situation would have avoided wasteful expenditure in the wrong directions. Aligning with this, the RBI had adopted the policy of increasing the Ways and Means Advances (WMA) limit for states by 60 percent. The WMA are short-term advances that the central bank gave to the states to tide over their temporary mismatches in cash flows. This short-term policy was applicable until September 2020, which was also the time by when the virus was expected to start phasing away.

Similar policies of debt repayment easing and others like increasing special drawing limits could have also been adopted to ensure that the cyclical policy measures could have been effectively taken to draw out the economy from downswings.

India’s fiscal policies have undergone a significant transformation in response to the pandemic, transitioning from a pre-pandemic focus on stabilization to a post-pandemic emphasis on growth-oriented measures (Figure 9). This shift reflects a strategic recalibration of the government’s aims and objectives in the realm of fiscal policy.

Prior to the pandemic, India’s fiscal policies were primarily around stabilizing the economy and maintaining macroeconomic equilibrium. The focus was on ensuring fiscal discipline, controlling inflation, and managing fiscal deficits. The aim was to create a stable economic environment that would attract investments and promote sustainable growth over the long term. However, during the unprecedented pandemic, the GoI swiftly implemented a series of fiscal policy measures to mitigate the economic impact and provide crucial support to households, businesses, and key sectors of the economy. Measures such as economic aid for the poor, free cash dispensation, rationing for the poor, and tax relaxation from the major industries are the important steps taken by the government to provide immediate relief and laying the foundation for a resilient and inclusive recovery (Sengupta, 2020).

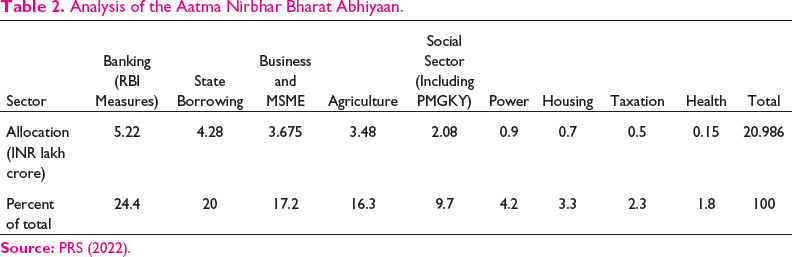

In April 2020, the government introduced targeted cash transfers to support impoverished households and distributed free food grains to address immediate socioeconomic needs. These measures aimed to alleviate the financial strain on vulnerable segments of society and ensure their basic well-being during the crisis (ADB, 2021). Recognizing the importance of the foreign trade sector, the government implemented initiatives to enhance export credit and extend payment timelines for importers. These steps were taken to bolster businesses engaged in international trade, enabling them to overcome the challenges posed by disrupted global supply chains and maintain their competitiveness (OECD, 2022). To ease the financial burden faced by vulnerable small enterprises, the government permitted lending institutions to restructure their debt. This measure aimed to provide relief to these enterprises, allowing them to manage their financial obligations more effectively and sustain their operations during a period of economic uncertainty. Additionally, the government introduced the Atma Nirbhar Bharat (self-reliant India) package (Table 2), which encompassed comprehensive measures to support various sectors, including MSMEs, farmers, and reforms in the energy sector and labor regulations. The package focused on providing liquidity support and encouraging investment to promote economic recovery and self-reliance in specific areas of agriculture, technology, and human capital.

Analysis of the Aatma Nirbhar Bharat Abhiyaan.

As the fiscal stimulus progressed, there was a strategic emphasis on increasing capital expenditure. During April to November 2020/2021, capital expenditure witnessed significant double-digit growth, while revenue expenditure grew moderately. This shift in expenditure prioritization aimed to stimulate economic growth over the medium term by channeling resources into productive sectors (PIB, 2022).

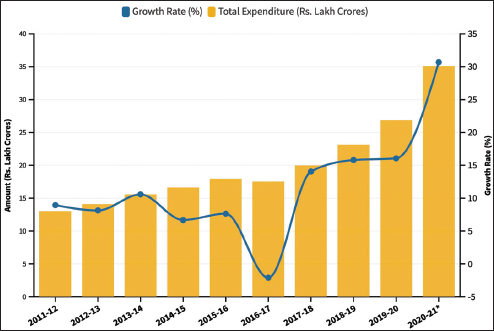

The fiscal policy measures undertaken by the GoI during the pandemic demonstrated a proactive approach to address immediate needs, provide sector-specific support, and pave the way for a resilient economic recovery. These initiatives, ranging from targeted cash transfers and trade facilitation to debt restructuring and capital expenditure, were designed to safeguard the well-being of individuals, sustain businesses, and lay the groundwork for a more self-reliant and robust economy in the face of unprecedented challenges. As per Table 3, a significant contributor to this is the increased expenditure for “central sector schemes” in 2020–2021, compared to the initial BE for that year. The RE for central schemes was ₹8.7 lakh crores compared to the BE of ₹4.97 lakh crores. This is also significantly higher than the actual expenditure incurred in 2019–2020 for “central sector schemes.” This was due to various schemes and support measures announced by the GoI to provide relief from the pandemic. The comparative higher revenue expenditure in April, June, and July coincides with the relief measures announced during the lockdown period. The higher expenditure in the later months can be attributed to the implementation of the various schemes and the continued support in the wake of the pandemic (Faqtly, 2021)

Summary of Expenditure.

As part of this post-pandemic fiscal strategy, the government adopted a three-pronged approach. First, there was a renewed emphasis on protectionism, aimed at safeguarding domestic industries and markets. This involved implementing measures such as tariffs, import restrictions, and domestic procurement policies to shield Indian businesses from foreign competition and foster self-reliance. Second, the government introduced production incentives to stimulate manufacturing and production activities. These incentives included schemes to boost productivity, research and development, and technological advancements. The objective was to encourage businesses to increase their production capacity, innovate, and contribute to economic growth. Lastly, there was a strong focus on infrastructure development as a catalyst for economic recovery and long-term growth. The government embarked on ambitious projects to improve transportation networks, digital infrastructure, and social infrastructure. These infrastructure investments aimed to enhance connectivity, reduce logistical bottlenecks, and create an enabling environment for businesses to flourish (RAI, 2022).

Overall, the post-pandemic fiscal policies of India demonstrate a shift from stabilization-oriented measures to a more growth-oriented approach. The aim now is not only to achieve macroeconomic stability but also to actively stimulate economic activity, generate employment, and attract investments. This strategic recalibration reflects the government’s commitment to overcoming the challenges posed by the pandemic and setting India on a path of resilient and sustainable growth in the post-pandemic era.

Stakeholder Engagement

In metro cities like Delhi, notorious for its relationship with real estate, a fair policy proposition to make is that the Delhi Real Estate Regulatory Authority (RERA) should have joined hands with the government to direct incomplete properties or those midway through construction to be doubled up as shelters for migrants who were on their way to leaving the city or were forced to stay on despite the relief the government had offered to them to help them return home. However, what was needed to be understood was that laborers proved to be potential public health hazards as they had grouped up on railway platforms and bus terminals in huge numbers to leave, which sanitization of public areas with disinfectants to curb the spread of the virus, had missed too. Plus, their returning home and coming in contact with the elderly, children, and those less immune had also meant that it was a major force behind the spread of the contagion in rural areas, where public health facilities were already in a crumpled state, sufficient only for a very few people. With borders of a host of Delhi’s neighboring states sealed, many migrant workers had been left mid-track not knowing where to go. This was such a big issue that it attracted the attention of filmmakers, and the grim situation of the returning laborers was very aptly presented in a movie titled Bheed in 2023. In such a scenario, the ideal proposition would have been for unfinished property projects to serve as temporary shelters for workers and isolation wards for those suspected sick. Concentration of state and central government efforts to provide food and basic necessities to workers housed in such manners could have been a more efficiently targeted manner of going about it, with the side benefit of course of reducing costs of the program. The economics of this proposition would have held tight too. In an already slowing economy, it takes not much to figure out that once the lockdown was over, India would be looking at a bad recession in its face. Most of the manufacturing sector was reeling under the blow that the pandemic and lockdown had thrown at it. Moreover, with the IMF’s prediction for Indian recession, layoffs were a common scenario, and again the worst hit were the migrant workers and self-employed. The welfare state could have, however, intervened to ensure a more pleasant post-pandemic picture. The economy was running a liquidity crisis, which could have aggravated as production would have been hit very sharply, if nothing was done to ensure otherwise. Policymakers around the country could have opted for options such as MGNREGA and cash transfers to increase post-pandemic liquidity. MGNREGA might have been effective as a bridging tool for RERA authorities and central and state policymakers to come together. Possibly, government authorities could have considered options of tying up with Delhi and other state RERA to offer jobs to the same migrant laborers housed in builders’ properties to resume construction work once situations started easing out. The wages of these workers, for a stipulated time period, could have been covered under MGNREGA work, thereby channeling government’s fiscal stimulus package to boost both production activity and real wages in the hands of migrant workers. Germany’s Kurzarbeit, or short work subsidy, is a good case point to take example from. The German program allowed for workers to remain on paid leaves and practice social distancing while also allowing for companies to avoid laying them off meanwhile.

Investment in Healthcare for Economic Growth

India only spends about 1.28 percent of its GDP as public expenditure on health care (National Health Profile, 2019). The pandemic-induced crisis had brought into focus more than ever the fault lines in the system. From lack of proper infrastructure to under-provisioning of medical equipment and inadequate testing labs and other facilities, the Indian healthcare system was overwhelmed with this public health crisis.

One crucial policy measure India must undertake for a sustainable exit from the pandemic and preparedness for the future pandemics emphasized by the World Health Organization (WHO) and economic underdevelopment at large is promotion of the healthcare sector in India. Unconditional cash transfers from international agencies, if not availed in full at that time, can be availed later by the GoI for investment expenditure in improving healthcare infrastructure in India, while also simultaneously skilling new and additional workforce in the sector. Three pertinent fundamental challenges that the government can seek to target are as follows. First, the universal immunization program “Mission Indradhanush” has achieved considerable success but still has a long way to go owing to obstacles of low awareness and high cost of delivery. Second, health insurance in India is a major upcoming segment in the insurance sector. Ayushman Bharat Mission–National Health Protection Mission or Pradhan Mantri Jan Arogya Yojana (PMJAY), announced in the Union Budget 2018–2019, is an initiative for expanding the health insurance net, targeting 10 crore poor and deprived rural population. The government should continue to ensure that funds to these programs are channeled appropriately and newer schemes to complement them are in place.

Moreover, at the local level, healthcare improvement policies are expected to not just be a means for employment generation but can also go a long way toward cultivating more acceptance for modern medication and best practices of health care. Funds can be channeled by state/UT governments to the municipality or Gram Panchayat blocks to conduct skilling programs for the youth for jobs such as those of general duty attendants and Anganwadi workers. The coronavirus crisis and the associated social-distancing measures also had a deep negative impact on the nutritional status of women and children among the migrant labor population. It was also estimated that for the lowest strata of the society, access and affordability of professional healthcare services would become more difficult if these two aspects continue to remain largely functions of income levels. By targeting the availability aspect, the government can then expect to ensure at least the non-worsening of these two aspects in the short run and move on to looking at sustainable policy solutions to cover them in the long run. Strengthening local bodies for providing proper immunization, nutritious diets and vitamin supplements, support to pregnant and lactating mothers, etc., appear to be crucial measures based on which fiscal and program support by the government can put India on the path to achieve economic recovery and improved development indicators simultaneously.

Concluding Remarks

This article discusses three policies: (a) monetary policy through its major components; (b) fiscal policy, and (c) other subsistence-based policies. The general conclusion that follows is that monetary policy alone was inept at managing the entire spread of the crisis and was equally likely to have consequences that might have made India’s V-shaped recovery from the crisis difficult. A policy mix is thus proposed to comprise the recovery package for a crisis of the scale of COVID-19 pandemic. Additionally, two policy recommendations based on stakeholder engagement for immediate relief and healthcare investment for long-term growth, respectively, have been proposed for dealing appropriately with such pandemics in future, as WHO has predicted repetition of pandemics even worse than COVID-19.

Existing theoretical policy frameworks have proven to be inadequate to provide a commensurate policy solution to the crisis in the past. The above-mentioned policies have their own set of challenges that are yet not tested for success rate and applicability to the new world order as it stands today and is expected to arise once this global pandemic is a thing of the past.

For instance, there is dire need for literature and a sophisticated framework within which we can determine government policy approach. For example, a study in the United States points at the need for understanding how to provide social safety net support in a way that encourages consistent individual expenditure on the “right” things such as essentials and moves it away from the “wrong” ones that compromise on social-distancing norms in times of coronavirus epidemic (Hafiz, Oei, Ring, & Shnister, 2020). Behavioral policy nudges, an understanding of updated consumer psychology, and the vulnerabilities of the modern world are things as important as technological advances that need to be studied but have yet not generated significant interest in the minds of academicians required for the production of support literature for policymakers around the globe.

A second challenge that presents itself is that of policy applicability. The coronavirus crisis originated in an East Asian country, eventually spreading to Europe, the Americas, Asia, and elsewhere and has recorded very high death rates in different countries in terms of demographics, policies, leadership, etc. At the same time, in the age of interconnectedness, supply chains of production processes in countries are closely interlinked with each other, and the crisis has yet again reinforced the interdependency of countries on each other, this time by means of supply chains and medical equipment. These two aspects indicate the differentiated but universal nature of the crisis. Thus, it is vital to ensure that the nature of policy implementation is as dynamic and flexible as the changing world. Among the policy solutions presented in the previous sections of this article, the major challenge for implementation is regarding policy targeting. For instance, should social security measures would have been provided then at the individual level based on social security numbers (or Adhaar in India) or by employers and other aggregators, and should they have been targeted to reduce unnecessary mounting of government expenditure due to universal applicability of fiscal support measures to eliminate positive exclusion bias? An inherent challenge is of policy testing in times of crisis. Ideally, these differentiated targeting techniques should be pre-tested for maximum efficiency. Clearly, however, this is not possible for policymakers during the crisis even at the cost of incurring wasteful expenditure on account of lack of policy impact studies. To avoid similar situations from arising in the future, it is imperative that empirical testing of most polices be undertaken rapidly and that mechanisms be established so that testing can be done in different ways to quickly establish operational feasibility of new policies. What followed with respect to the policy measures was commendable with respect to the unanticipated nature and scale of the pandemic for any government at helm of affairs. A multi-pronged strategy was seen at the top and its effective implementation on the ground to strengthen the worn-out knees of the economy due to the dual strike of the world economy slowdown of 2019 and the COVID-19 pandemic of 2020–2022. Thus, a larger shift in the fiscal and monetary policy approach was inevitable to bring back the economy on its path to becoming the global economic superpower. In light of this background, India’s fiscal policies have witnessed a notable shift post-pandemic, transitioning from a focus on stabilization to a more growth-oriented approach. The objective now extends beyond achieving macroeconomic stability to actively stimulate economic activity, generate employment, and attract investments. This shift in fiscal policy reflects the government’s commitment to driving economic growth and fostering resilience in the face of challenges. Similarly, the monetary policy of India has undergone a shift in its goals. While the focus in 2020 was on enhancing liquidity and stabilizing the economy amid the pandemic, the emphasis has now shifted towards promoting real economic growth in the post pandemic time period to embark on the path of becoming the largest economy by 2050. This adjustment in monetary policy aligns with the evolving needs of the economy and supports the broader objective of sustainable growth.

Maintaining a balance between fiscal and monetary policy measures is crucial for effective economic management. The RBI plays a pivotal role in achieving this balance. By coordinating with the government, the RBI ensures that fiscal and monetary policies work in tandem, maximizing their impact on the economy. This collaborative approach has been instrumental in shaping the current state of the Indian economy, where fiscal measures drive growth and RBI’s monetary policy supports these initiatives. Furthermore, in the context of potential deviations from fiscal rules, it is important to consider the ideal approach during a recession triggered by a once-in-a-century global crisis. In such challenging times, a recommended strategy would involve implementing a sustained and productive program of permanent stimulus, aimed at directing investments toward both physical and human capital. This approach recognizes the need for long-term investments in key areas to support economic recovery, build resilience, and foster sustainable development. By prioritizing public investment in critical sectors, including infrastructure and human resources, India can lay a strong foundation for future growth and ensure the well-being of its citizens (Krugman, 2020).

Through proactive measures and strategic alignment with fiscal policies, the RBI has played a crucial role in steering the Indian economy toward its present state. This coordinated approach between fiscal and monetary policies optimizes the effectiveness of both instruments and contributes to the desired economic outcomes. RBI’s efforts have been instrumental in fostering growth, stability, and resilience in the Indian economy, paving the way for long-term prosperity.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.