Abstract

In this study, we propose a deep learning related framework to analyze S&P500 stocks using bi-dimensional histogram and autoencoder. The bi-dimensional histogram consisting of daily returns of stock price and stock trading volume is plotted for each stock. Autoencoder is applied to the bi-dimensional histogram to reduce data dimension and extract meaningful features of a stock. The histogram distance matrix for stocks are made of the extracted features of stocks, and stock market network is built by applying Planar Maximally Filtered Graph(PMFG) algorithm to the histogram distance matrix. The constructed stock market network represents the latent space of bi-dimensional histogram, and network analysis is performed to investigate the structural properties of the stock market. we discover that the structural properties of stock market network are related to the dispersion of bi-dimensional histogram. Also, we confirm that the autoencoder is effective in extracting the latent feature of the bi-dimensional histogram. Portfolios using the features of bi-dimensional histogram network are constructed and their investment performance is evaluated in comparison with other benchmark portfolios. We observe that the portfolio consisting of stocks corresponding to the peripheral nodes of bi-dimensional histogram network shows better investment performance than other benchmark stock portfolios.

Keywords

Introduction

Stock markets which fluctuate chaotically are modelled as complex networks formed through the interaction of individual factors [35]. Many studies have used network analysis to investigate the relationship between stocks [35, 53, 34, 20, 11, 23, 42, 19, 41, 40, 28, 16, 44, 29, 57, 26, 6, 24, 51, 52, 17, 13, 49, 37, 38]. Mantegna [34] analyzed stock markets through Minimum Spanning Tree (MST) network for the first time, observing the structure of Dow Jones stock market. MST is a filtered graph connecting all the

In defining interactions between stocks, many studies highlighted stock price time series. However, information on stocks is not only contained in the price, but also in various data such as trading volumes, volatility and accounting variables. In particular, we focus on trading volumes of stocks in addition to their prices. From a practical point of view, trading volumes have much significant information. For example, the increment of trading volume at the floor of stock price is regarded as a signal of upward conversion. Conversely, the decrement of trading volume at the ceiling of stock price is understood as a signal of a downward turn. As such, the trading volume could indicate the direction of stock price. Also, stock return and trading volume interact with each other in the stock market dynamics [27]. Various studies have been conducted to analyze the properties contained in trading volume and its relationship with stock price. As in stock prices, trading volume has multifractal behavior characteristics [3] and auto-correlation patterns [47]. Lee and Swaminathan [27] revealed that the trend of trading volume is related to the persistence of price momentum and magnitude. Chen et al. [7] confirmed that positive correlation exists between the trading volume and the absolute value of stock price return. Various studies have used the stock price and trading volume together to predict the stock price [55, 54, 9, 14, 33]. The positive correlation between the negative skewness of stock price returns and trading volume was verified through previous studies [15, 8]. Trading volume is correlated with the volatility of stock returns, return on equity (ROE) and return on investment (ROI) [45, 18, 12, 46, 22]. Bajo [4] revealed that the trading volume is an efficient proxy of stock information for market participants.

As described above, the trading volume is important to explain the properties of a stock and the stock market in addition to stock price. Our study attempts to analyze the stock market by considering both stock prices and stock trading volumes. Both of stock price and stock trading volume can be analyzed from a multivariate perspective through the RV coefficient, which is a multivariate generalization of the squared Pearson correlation coefficient. However, the RV coefficient has some drawbacks of difficulty in understanding and high computational cost [25]. In this study, we utilize a bi-dimensional histogram to intuitively represent stock trading volume information as well as stock price information.

As the size of bi-dimensional histogram is relatively large, we apply autoencoder to the bi-dimensional histogram for the latent feature extraction from the reduced bi-dimensional histogram data. Autoencoder (AE) is widely used for feature extraction as a method of deep learning [39, 10, 56, 2, 32, 30, 5, 36, 21]. AE, which consists of two neural networks called encoder and decoder, is a nonlinear dimension reduction methodology and an effective method for manifold learning. AE compresses and reproduces data through an encoder and decoder, and effectively extracts the features inherent in the data.

Based on the extracted features, we build the bi-dimensional histogram network of the stock market using the PMFG algorithm, and network analysis is performed to investigate the structural properties of the stock market. The novelty of our research is that we construct a stock market PMFG network using the latent features from autoencoder transformed information of bi-dimensional histogram based on stock prices and trading volumes.

The bi-dimensional histogram network is applied to construct stock investment portfolio. There are many studies incorporating the network topological property into the construction of stock portfolio [44, 58, 59, 31, 29]. Pozzi et al. [44] proposed a measure to quantify the level of the network periphery, and showed that the portfolio of stocks in the periphery of network performs better than that of stocks in the center of network. Based on this property, we investigate the usefulness of a histogram network in terms of portfolio selection.

The paper is organized as follows. Section 2 reviews previous studies of the stock market network, as well as studies of autoencoder in the stock market. Section 3 describes the data, bi-dimensional histogram, autoencoder, stock network, and portfolio application. Section 4 presents the result of our suggested method including the features of bi-dimensional histogram and network analysis. Finally, the summary of our research is provided in Section 5.

Related work

Stock market network

In econophysics, the stock market network plays an important role in analyzing the characteristics of financial markets. After Mantegna’s research [34], which first introduced the network concept through MST to analyze the stock market, many studies have used MST to analyze financial markets. Onnela et al. [42] constructed MST network of S&P500 stocks to study the dynamics of the stock market, finding that normalized tree length of the MST decreases and remains low during the financial crisis. Bonanno et al. [6] revealed that the MST of the stock market has a structured hierarchy. Jung et al. [24] studied the MST of the Korean stock market and found that the characteristics of the Korean stock market differ from that of the US market. However, the drawback of MST is that valuable information about the relationship between stocks is necessarily lost. To complement the drawback of MST, Tumminello et al. [51] proposed a stock market network using PMFG. PMFG is a graph using the planarity property, and loops and cliques are allowed, including MST in the graph. Various studies have demonstrated that PMFG has a more significant and richer structure, stronger robustness, and better dynamical stability than MST [51, 43, 13]. PMFG is a conventional method to build a stock market network and is used in various fields. Zhang and Zhuang [57] built a Chinese stock market network using PMFG and investigated the relationship between network stability and stock market volatility. Musmeci et al. [38] analyzed the NYSE stock market with PMFG. Musmeci et al.[38] investigated meaningful relationships between past changes in the network structure and future changes in the market volatility. Song et al. [50] confirmed that PMFG effectively extracts clusters and hierarchies from complex data sets. Lu et al. [31] proved that PMFG is also useful in portfolio investment.

Autoencoder in the stock market

In this study, we propose a framework for constructing a stock market network from a multivariate perspective using autoencoder and PMFG. As the dimension of the variable increases, the higher dimension variable can lead to redundancy of information and reduce the efficiency and accuracy of algorithms. In this context, autoencoder, a deep learning model, is a method that extracts meaningful features from high-dimensional variables and is also in the spotlight in the finance domain. Lv et al. [32] performed feature extraction of 44 technical indicators for stock using autoencoder and applied it to predicting trading signals. Bao et al. [5] extracted features by compressing daily trading data, technical indicators, and macroeconomic variables with an autoencoder. And [5] verified the usefulness of autoencoder by using compressed features for stock price prediction. Moews and Ibikunle [36] extracted latent features of high-frequency transaction data using autoencoder and used it for stock price movement prediction. Moews and Ibikunle [36] also demonstrated that this approach works even in highly volatile market conditions such as the financial crisis. Huh [21] applied autoencoder to predict the systematic risk of the stock market. In previous studies using autoencoder in the finance domain, features extracted through autoencoder are mainly used for prediction. In this study, we focus on structuring the stock market using features extracted through autoencoder. We transform the stock price and trading volume into a bi-dimensional histogram and perform feature extraction through an autoencoder. Then, we build a stock market network by applying the PMFG algorithm to the latent space of the extracted features. To the best of our knowledge, our approach is the first attempt to use the bi-dimensional histogram and autoencoder to construct the stock market network. Based on the stock market network constructed by our method, we perform network analysis to investigate the structural properties of the stock market. And we utilize the stock market network to construct a stock investment portfolio.

Data and methods

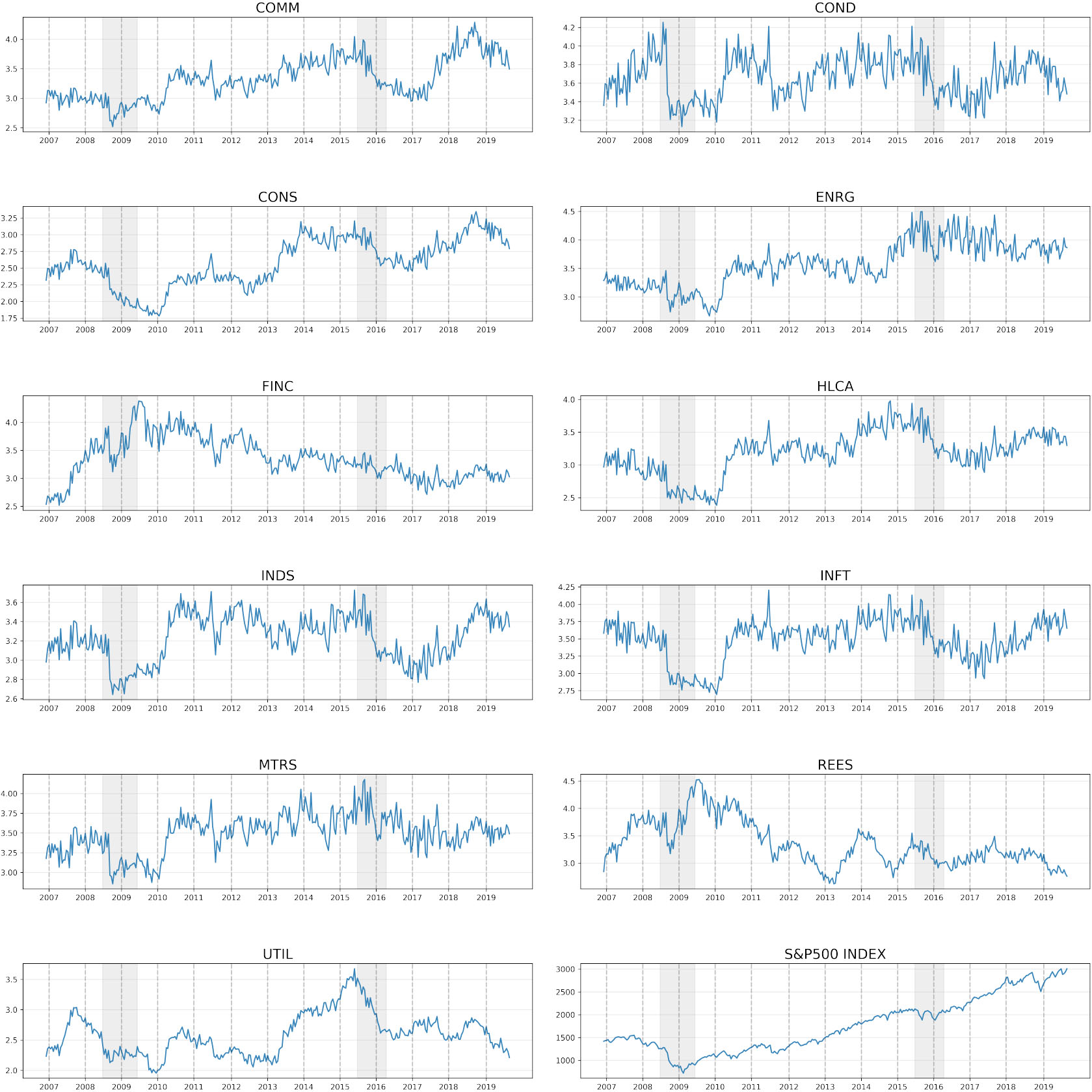

The data in this study is comprised of the daily adjusted stock prices and daily trading volumes of stocks included in S&P500 from January 3, 2006 to September 30, 2019, which amount to 3459 data points. Among the stocks that have been listed in S&P500 over the entire period, the top 400 stocks are selected on the market cap basis. The description of the stocks is provided in appendix. Table 1 is the result of classifying the stocks into 11 sectors according to the Global Industry Classification Standard (GICS) industry category system. Stocks are classified into 11 sectors, Financials (FINC), Industrials (INDS), Consumer Discretionary (COND), Information Technology (INFT), Health Care (HLCA), Consumer Staples (CONS), Real Estate (REES), Utilities (UTIL), Energy (ENRG), Material (MTRS), and Communication Services (CONS). The largest and the smallest industry sectors are the financial sector and the Communicaion Services sector, accounting for 59 stocks (14.75%) and 14 stocks (3.5%), respectively.

Summary of GICS industry classification of stocks

Summary of GICS industry classification of stocks

Bi-dimensional histogram maps pairs of two variables to bi-dimensional grid bins. Given the number of all observation pairs,

When denoting the closing price of

Based on the bin size set above,

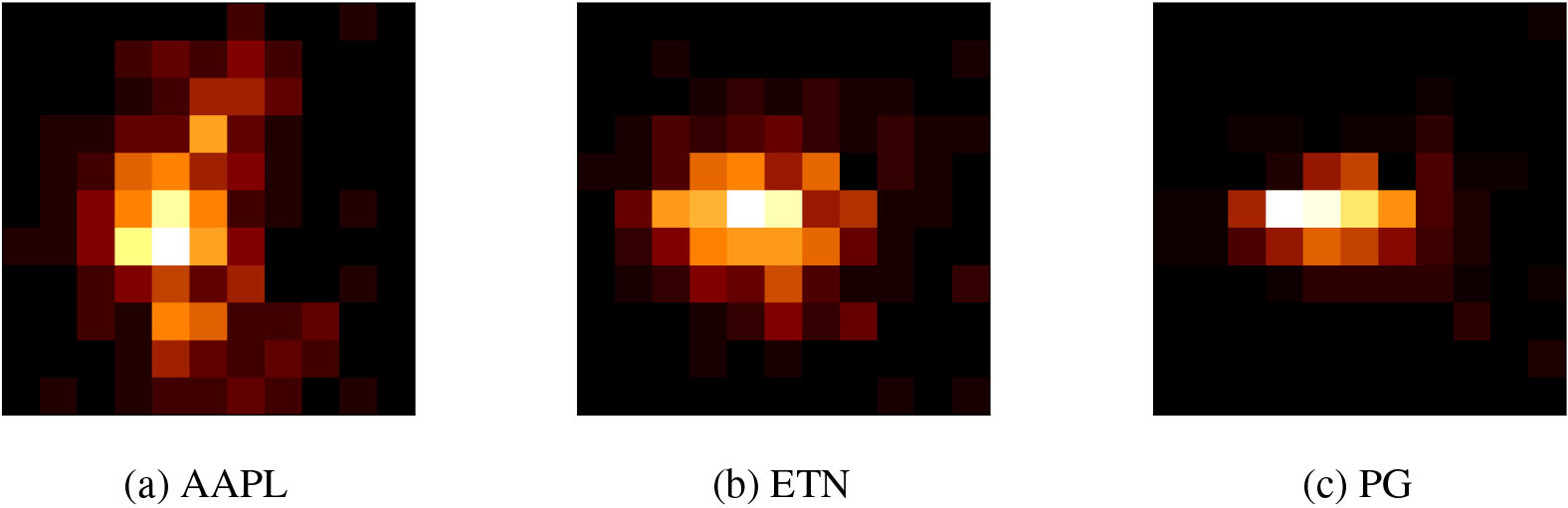

Bi-dimensional histograms of AAPL, ETN and PG.

Figure 1 shows bi-dimensional histograms of AAPL, ETN and PG for the first observation period. We define dispersion

where

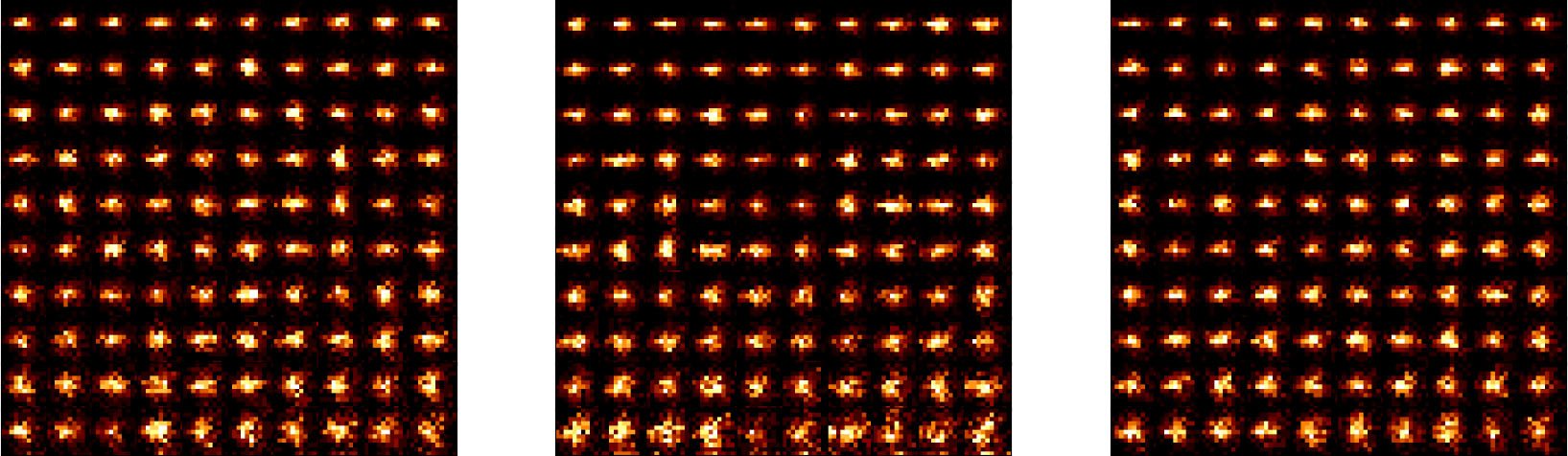

Bi-dimensional histograms sorted in ascending order of

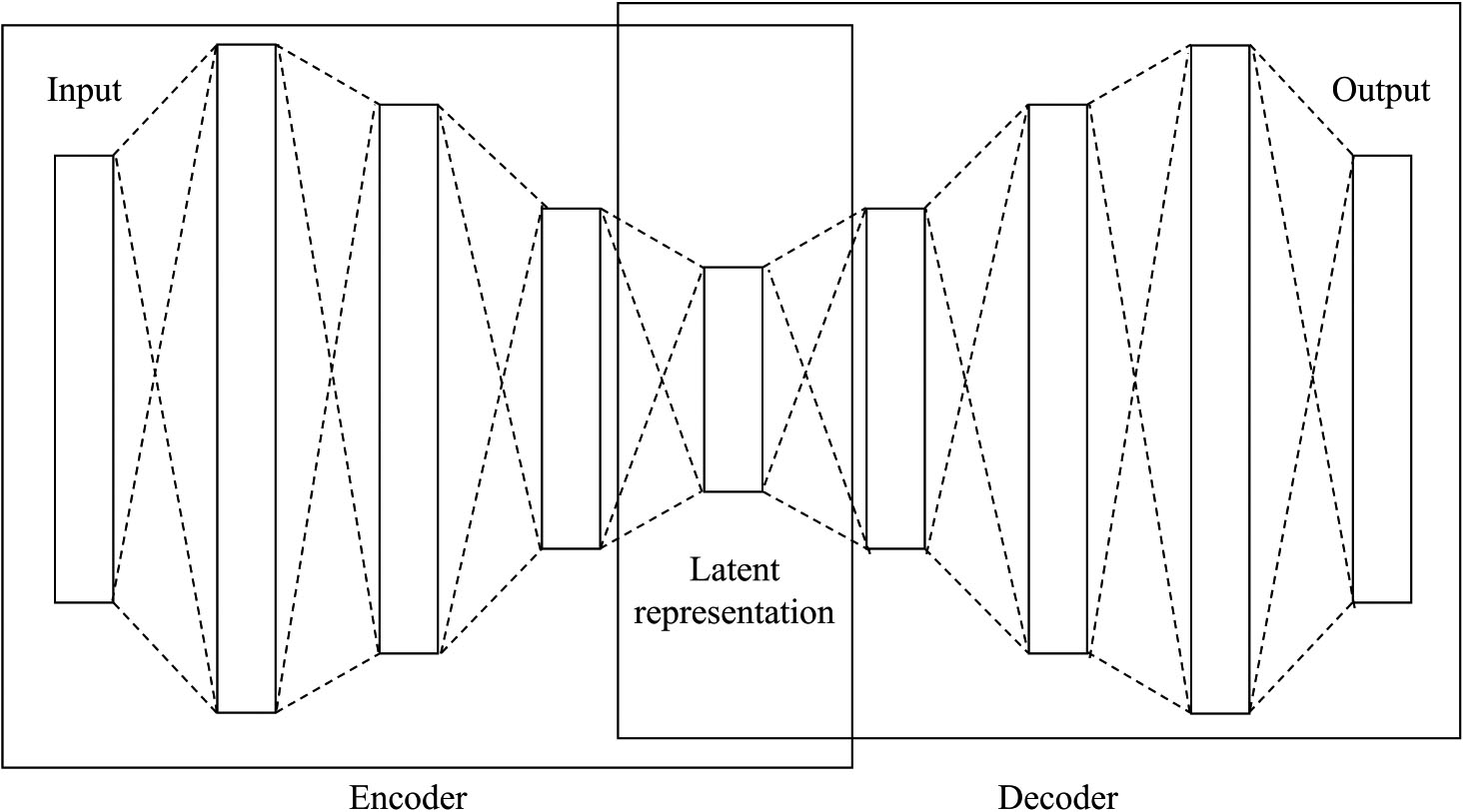

The main purpose of autoencoder (AE) in deep learning is to learn representation in a data set through unsupervised learning. This representation of the input data is depicted as an internal (hidden) layer or latent vector. AE consists of two parts: encoder and decoder. Encoder compresses input to the lower dimensional latent space. Conversely, decoder reconstructs the input. Through the compression and reconstruction process, most relevant aspects of data are contained in the latent space of the AE.

When denoting the input space as

where L is a loss function. As the dimension of

The purpose of the AE in this paper is to learn a bi-dimensional histogram as an input to obtain a latent vector that is a compressed representation of the histogram. The encoder and decoder of the AE are composed of four stages fully connected hidden layers and formulas of the encoder and decoder for the set of parameters

where

We select the set of parameters

Table 2 summarizes the dimensions of each layer constituting the AE model, and Fig. 3 is a schematic diagram of the autoencoder structure described in Table 2.

Dimensions of weight and bias of hidden layers in autoencoder

In this paper, the learning of AE is conducted on a bi-dimensional histogram. For each of 321 observation period, an AE model corresponding to the period is made. However, training a model using only 400 bi-dimensional histograms can cause over-fitting problems. To prevent this, augmentation is performed during data set construction. In each observation period, gaussian noises are added to price and volume series, and bi-dimensional histograms are constructed from the noisy series. For each stock, augmentation is performed 100 times using gaussian noise, and as a result, 40,000 bi-dimensional histograms are revised in the existing data set. We randomly select 80% of the data set for training and 20% for validation. In the training process, the dimension of the latent vector is set to 32 as above which the validation error does not significantly decrease. Also, the model training process proceeds to 250 epochs because the validation error tends to converge at the epoch. Table 3 compares the reconstruction errors between AE and Principal Component Analysis (PCA) which is a conventional method for dimensionality reduction. Reconstruction error is determined as mean squared error (MSE) between the original data and reconstructed data from the model. In our result, AE shows the better performance than PCA in terms of MSE.

Reconstruction error for different algorithms

Structure of autoencoder for feature extraction from bi-dimensional histogram.

We transform the bi-dimensional histogram of each stock into a latent vector through the encoder. In each observation period, the latent vector of the

We define a histogram based distance matrix,

where

Network analysis is performed to identify useful topology information on stocks based on distance matrices

[h!] : PMFG algorithm

We build PMFGs from

The characteristics of individual stock in the network can be quantified in terms of network centrality. In graph theory, network centrality quantifies the relative importance of individual nodes of a network. The network centrality measures used in this paper are as follows. Degree centrality (DC) is the number of edges connected to the node. Betweenness centrality (BC) is the frequency that a node acts as a bridge in the shortest path between two other nodes. Eigenvector centrality (EC) of the

Pozzi et al. [44] proposed a hybrid centrality measure of a node in the network, peripherality (P), which consists of 5 centrality measures described in the above.

where

Constructing a portfolio using peripheral nodes in a price network has an advantage in portfolio performance [44, 29, 31]. Also in the histogram network, a portfolio consisting of peripheral nodes can have distinct features compared to those of central nodes in that peripheral nodes are less related with other nodes in the network. We examine the characteristics of the portfolio according to peripherality on a histogram network. We also investigate whether histogram networks have an advantage over the price network in terms of investment utilization.

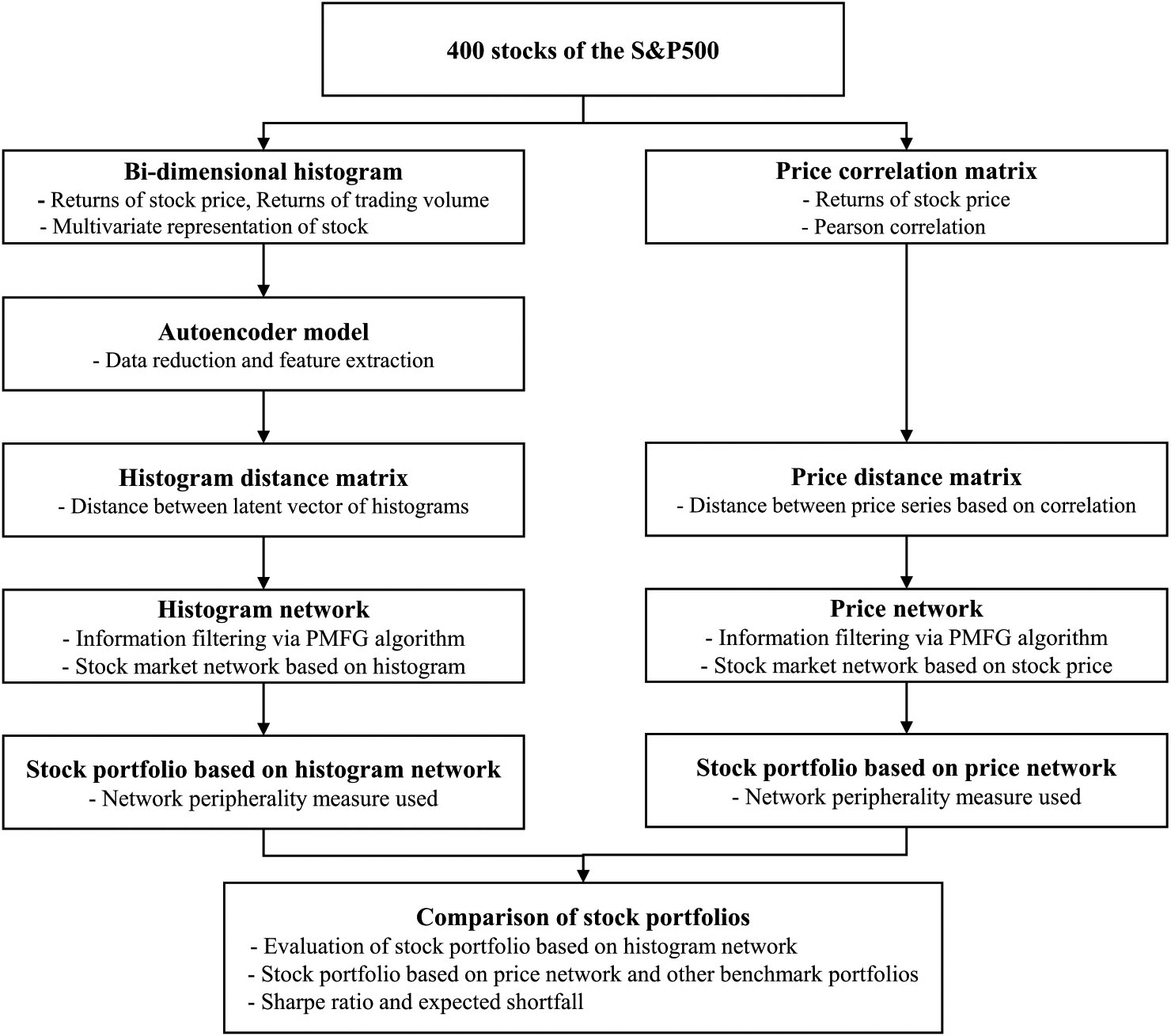

The portfolio investment based on a histogram network is verified as follows. The investment period of 13 years from January 13, 2006 to September 30, 2019, and the same moving window method as in Section 3.1 is performed. For each observation period, AE is applied to the bi-dimensional histogram to extract meaningful features of stock. Then, matrices for histogram and price,

where

Expected Shortfall (ES) is an indicator of portfolio risk, and the average of losses that exceed a certain quantile.

where

For the evaluation of bi-dimensional histogram-based portfolio, we incorporate various benchmarks including network-based and non-network-based portfolios. As the bi-dimensional histogram-based portfolio uses stock trading volume data in addition to stock price data, two network based portfolios, one for stock price returns and the other for stock trading volume returns are included as benchmarks. The non-network-based benchmarks include a market portfolio consisting of uniform weights of all 400 stocks in this study, the mega-cap portfolio ($200 billion and greater) and S&P500 index.

The portfolios based on histogram network and price network are denoted as the histogram portfolio and the price portfolio, respectively. The portfolio based on the network using only volume data is called as the volume portfolio. The overall framework of the experiment is summarized in Fig. 4.

Procedure for the portfolio experiment using the histogram network.

In this section, our experimental results are provided. The characteristics of bi-dimensional histogram for S&P500 stocks are studied. The network topologies are compared between the histogram network and the price network, and the investment usefulness of histogram network is examined.

Properties of bi-dimensional histogram

We analyze properties of the bi-dimensional histogram through

Table 4 presents the descriptive statistics of

Descriptive statistics of

for different periods

Descriptive statistics of

Distribution of

For the analysis of

When focusing on the sub-prime mortgage crisis, the value of

Table 5 shows the correlation of

Evolution of the series of

Correlation between

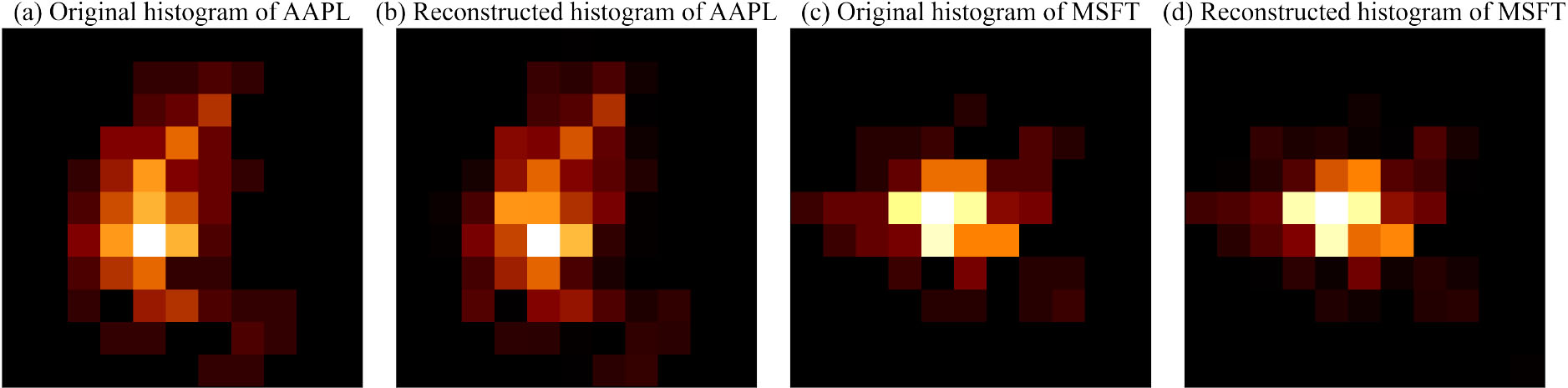

In this study, the Bi-dimensional histograms are 11 by 11 dimensions and have noise and missing values. Bi-dimensional histograms consist of 121 bins, and 50.7% of bins are empty. In addition, the bin whose frequency is less than 1% corresponds to 25% of the total. As such, the bi-dimensional histogram of stock has a large amount of noise. Therefore, we use an autoencoder to extract meaningful information from the bi-dimensional histogram. Figure 7 shows the bi-dimensional histogram of stocks and the reconstructed bi-dimensional histogram. The latent vector of the bi-dimensional histogram is 32 dimensions and has less noise and missing values compared to the bi-dimensional histogram. On average, 22% of the bins of the latent vector are noise. We calculate the distance matrix between latent vectors according to Eq. (6). And then, we apply the PMFG algorithm to the distance matrix to build a stock market network based on latent vector of bi-dimensional histogram. The experimental results for the properties of the bi-dimensional histogram network are continued in the next section.

The original histogram and reconstructed histogram.

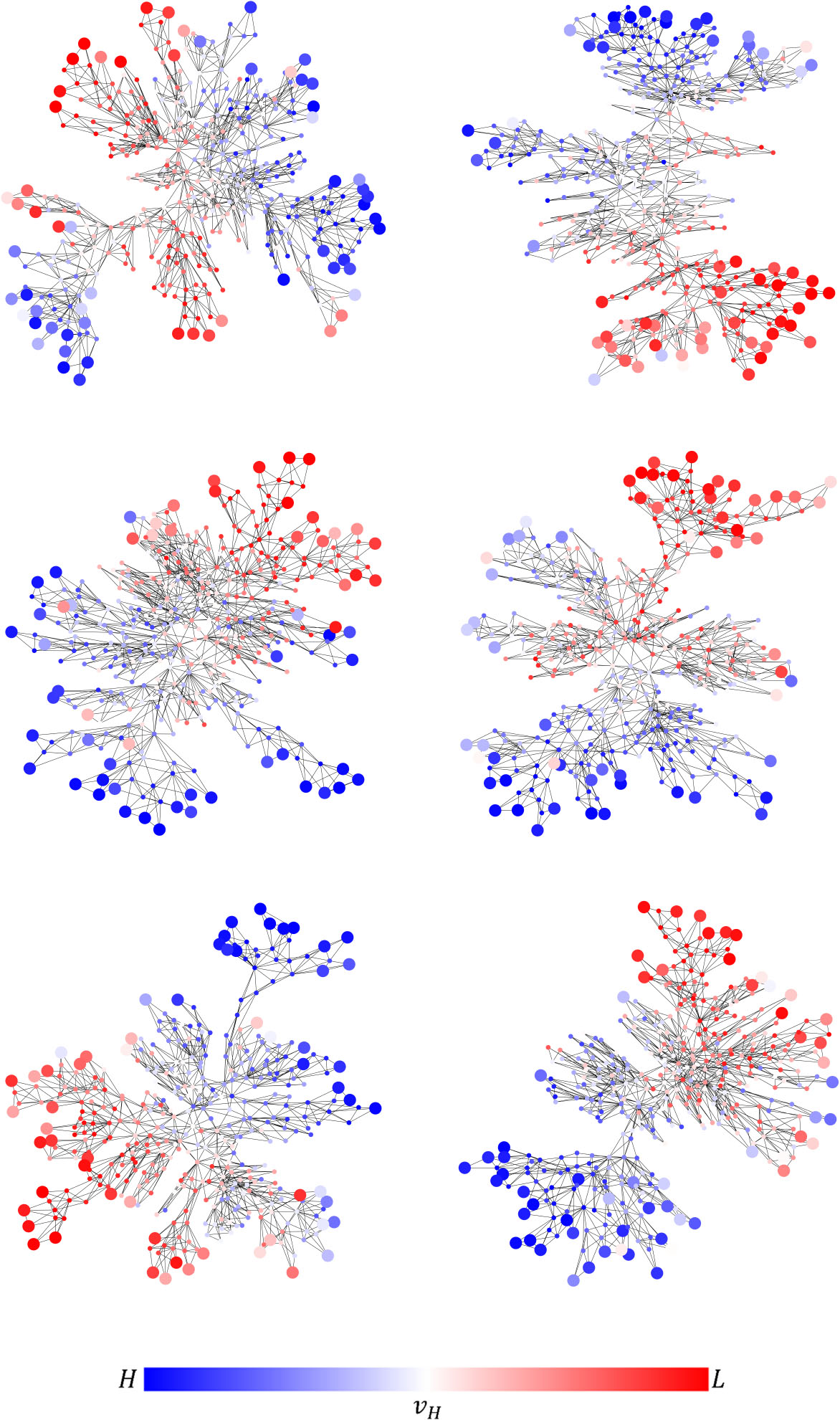

Latent vectors of bi-dimensional histograms for each stock are represented as nodes in the histogram network. Characteristics of each bi-dimensional histograms and their relationships are reflected in the topological structure of histogram network.

Classification of nodes in the histogram network according to the level of

Figure 8 shows 6 snapshots of the histogram network. The colors of node changing from blue to red correspond to the descending values of

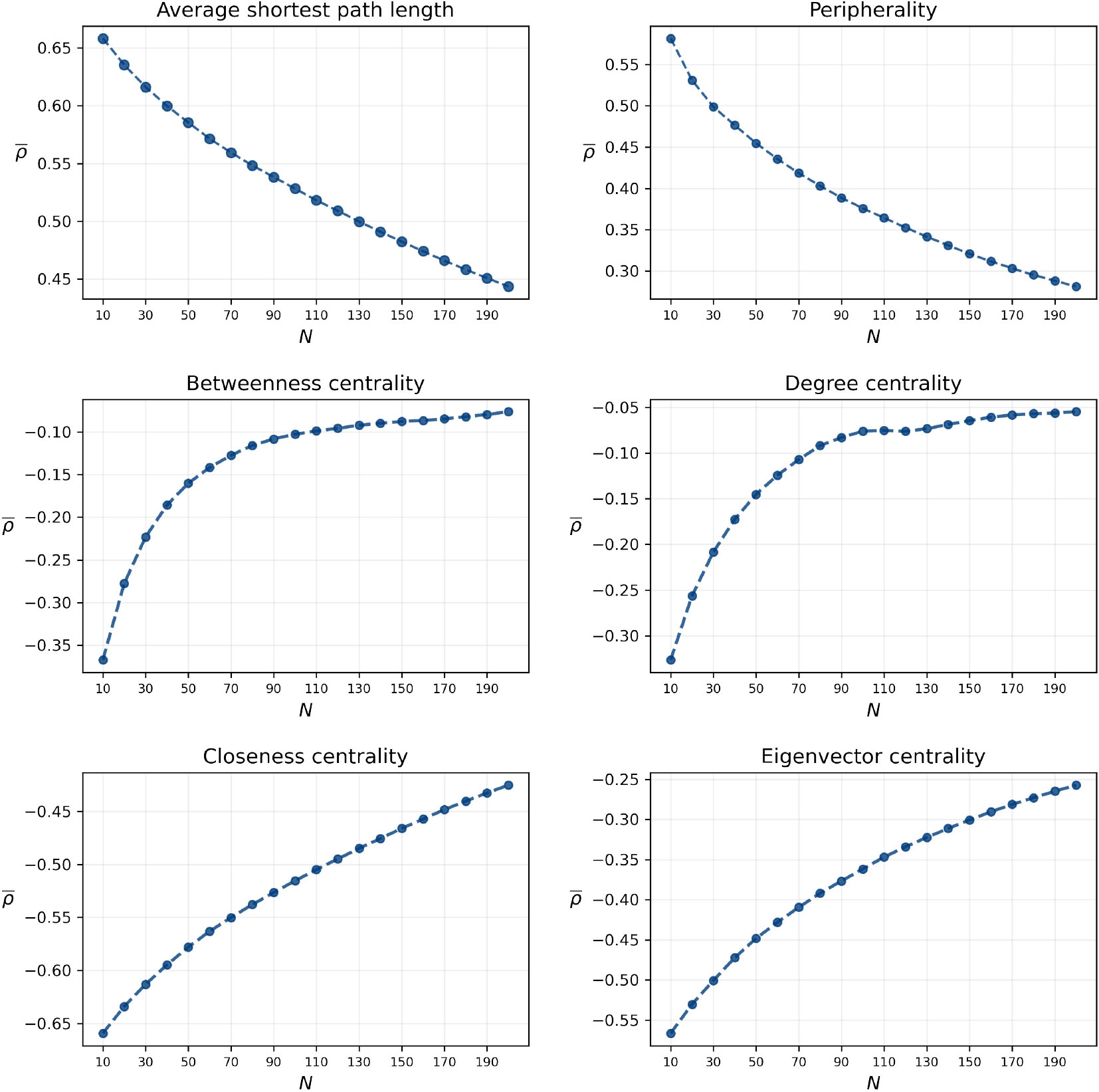

Figure 9 shows the result of correlation analysis between

Correlation between

In Fig. 9 showing the variation of average of

Meanwhile, centrality measures including betweeness centrality (BC), degree centrality (DC), closeness centrality (CC), and eigenvector centrality (EC) are negatively correlated with

The top 20 and the bottom 20 nodes in each network according to peripherality.

This section compares the structural features of histogram network and price network. Figure 10 shows snapshots of histogram network and price network. The coloring nodes in the network indicate top 20 central nodes (circle shape) and top 20 peripheral nodes (rectangular shape), and each color of node refers to the corresponding industry sector. In price networks, the central nodes include FINC and INDS from 2006-01-03 to 2006-12-29 and INDS and INFT from 2008-09-16 to 2009-09-14, which corresponds to the financial crisis period. In the histogram network, the composition of central nodes and peripheral are more diverse than price network.

Table 6 presents the top 10 stock ranks based on the frequencies included in the top 10 central and peripheral nodes, respectively, over entire 321 observation periods. Stocks of the ENRG, INFT, and HLCA sectors are located in the periphery of histogram network mainly. Among them, AMD is most frequently located in the periphery of histogram network, with 53 times (17%). On the other hand, stocks of the UTIL, CONS, and ENRG industry sectors are located in the periphery of the price network.

NRG is most frequently located in the periphery of a price network, with 70 times (22%). In histogram networks, the frequency of a certain stock located in the periphery of network is much higher than that in the center of network. This implies that the characteristics of bi-dimensional histogram can be determined by the property of the peripheral nodes. The frequency that specific stocks are located in the center or periphery of network is much higher in price networks than histogram networks. Especially, the central nodes in price network have more tendency to belong to certain industry sectors. INDS and FINC sector are mainly located in the center of price networks, and ITW is located 92 times (29%) in the center.

The frequency for nodes located in the center and periphery of network

Table 7 presents descriptive statistics of histogram network and price network. The nodes having the most connectivity in histogram network and price network during the entire observation periods have 37 edges and 149 edges, respectively. The standard deviations of the degree of nodes are 3.52 for histogram network, and 5.87 for price network. This implies that a local cluster having the central hub node is more common in price network than histogram network.

For the diameter of the network, the longest path length between nodes, price network has the average diameter of 11.83 and bi-dimensional histogram network has the average diameter of 16.72 which is 41% larger than price network. Assortativity is an index for the network hub which is a node with many edges. If the assortativity of the network is positive, the hubs are clustered together. Conversely, the negative assortativity called a disassortative network means that nodes with few edges tend to be located around the hub. Both bi-dimensional histogram network and price network are disassortative networks, and price networks are more disassortative. According to the above results, the average shortest path length of price network is smaller than that of histogram network.

Descriptive statistics of network topology measure

The proportion of stocks remaining in periphery (a) and center (b) of network after the time interval

Figure 11 shows the proportion of stocks remaining in the top 100 central nodes and the top 100 peripheral nodes after time interval

In this section, we construct portfolios using stocks corresponding to peripheral nodes of network. For the examination of portfolio performance, we use measures introduced in Section 3.3. Detailed results of the portfolio experiment are described in appendix Appendix B. Portfolio experiment results.

Tables B.1 shows the sharpe ratio for each strategy according to the number of stocks in the portfolio and the holding period. In histogram network, a portfolio of peripheral nodes shows the higher sharpe ratio than that of central nodes. This implies that a portfolio consisting of stocks located in the periphery of histogram network can be effective in that stocks have not only high sharp ratio but also few dependency on other stocks. Previous studies [44, 29, 31] also conclude that forming a portfolio using peripheral node stocks is the better strategy than using the central ones for the price network case.

Figure 12 presents the average sharpe ratio in terms of number of stocks,

Sharpe ratio of various portfolios.

Cumulative return of various portfolios.

Table B.2 presents the result of cumulative return of portfolios for each strategy. For the cumulative return of portfolio based on histogram networks, cumulative return of portfolio using peripheral nodes is higher than that of portfolio using central nodes. On the other hand, for the cumulative return of portfolio based on price network, there is no significant difference between the portfolio using peripheral nodes and that using central nodes.

Figure 13 presents the average cumulative return of portfolios against the portfolio size,

1% Expected shortfall of various portfolios.

Finally, Table B.3 provides the results of 1% expected shortfall according to each portfolio strategy. When looking at the expected shortfall of portfolios in Fig. 14, the poorest portfolio in terms of risk is the portfolio of central nodes in price network. The portfolio of peripheral nodes in price network is the best strategy in terms of 1% expected shortfall. For histogram network portfolio, the portfolio of peripheral nodes in trading volume network is more risky than that of peripheral nodes in histogram network. Overall, the portfolio of peripheral nodes in histogram network is more risky in terms of 1% expected shortfall than the market portfolio and the portfolio of peripheral nodes in price network, but it has the best Sharpe ratio and cumulative return.

In this paper, we propose a deep learning related framework to analyze stock market with multidimensional data. We construct a bi-dimensional histogram using the returns of price and trading volume of stocks, and apply autoencoder to the bi-dimensional histogram to extract features, and build a stock market network using the PMFG algorithm. The proposed stock market network represents the latent space of bi-dimensional histogram of stock prices and trading volumes.

Our results show that stocks with larger or smaller histogram dispersion than usual are located in the periphery of histogram network, while stocks with moderate dispersion are located in the center of the network. The nodes of the histogram network are clustered according to the histogram dispersion, implying that the autoencoder is effective in extracting the latent feature of the bi-dimensional histogram.

The dispersion of the bi-dimensional histogram has properties related to market conditions, and tends to decrease when the diversity of stock movements decreases, for example the financial crisis. We examine time varying properties of bi-dimensional histogram of stocks categorized in 11 industry sectors based on GICS, and observe that the dispersion of histogram for each industry sector decreases during the crisis period. In detail, the dispersion of the histogram for stocks in the industry sensitive to economy condition rapidly decreases during the financial crisis period. The industry sector which is insensitive to the economy condition shows low level of dispersion compared to other industry sectors. The dispersion of histogram for stocks in FINC and REES industries are negatively correlated with the dispersion of other industries.

We observe clear structural differences between our suggested histogram network and conventional price network. Histogram network is relatively more assortative than price network. For the composition of stocks for peripheral and center nodes of network, histogram network is distinct from price network. In the price network, stocks of the industrial and financial industries are located in the center, and stocks of utilities, energy and consumer staples industries are located in the periphery. On the other hand, for histogram network stocks of health care and industrial industries are located in the center, and stocks of information technology and energy industries are located in the periphery.

We found that the usage of stock trading volume on top of stock price information can leads to the improvement of stock portfolio performance. The portfolio using the peripheral nodes of histogram network shows a higher Sharpe ratio than the portfolio based on central nodes of histogram network, the market portfolio and other benchmarks including the portfolio using price network. Overall, investment portfolio based on peripheral nodes of histogram network using stock prices and trading volumes outperforms other benchmarks.

As future work, we can extend the bi-dimensional histogram network into the higher dimensional histogram network using more information such as accounting variables in addition to stock price and stock trading volume. We expect that the inclusion of more information on stocks to our framework can improve the performance of stock portfolio based on multi-dimensional histogram network.

Footnotes

Acknowledgments

This work was supported by the National Research Foundation of Korea (NRF) grant funded by the Ministry of Science and ICT (No. 2018R1C1B5043835).

Credit authorship contribution statement

Sungyoun Choi designed the bi-dimensional histogram and developed the auto-encoder model. Choi constructed the bi-dimensional histogram network using histogram distance matrix and the stock portfolio based on the histogram network. Dongkyu Gwak computed the price correlation matrix and price distance matrix. Gwak built the price network and constructed the stock portfolio based on the price network. Jae Wook Song performed the comparison analysis between the stock portfolios. Woojin Chang advised the overall research and experiment procedures.

Appendix

Appendix A. Selected stocks for experiment

We select 400 stocks that have been fully listed in S&P500 from January 3, 2006 to September 30, 2019. The list of stocks selected for the experiment is summarized in Tables A.1 and A.2.

Stock list

GICS sector

Symbol

Security

GICS sector

Symbol

Security

GICS sector

Symbol

Security

Communication

ATVI

Activision Blizzard

Consumer

MO

Altria Group Inc

Financials

COF

Capital One Financial

Services

GOOGL

Alphabet Inc.

Staples

ADM

Archer-Daniels-Midland Co

SCHW

Charles Schwab Corporation

T

AT&T Inc.

BF.B

Brown-Forman Corp.

CB

Chubb Limited

CBS

CBS

CPB

Campbell Soup

CINF

Cincinnati Financial

CTL

CenturyLink Inc

CHD

Church & Dwight

C

Citigroup Inc.

CMCSA

Comcast Corp.

KO

Coca-Cola Company

CME

CME Group Inc.

DISCA

Discovery, Inc.

CL

Colgate-Palmolive

CMA

Comerica Inc.

DISH

Dish Network

CAG

Conagra Brands

ETFC

E*Trade

EA

Electronic Arts

STZ

Constellation Brands

RE

Everest Re Group Ltd.

IPG

Interpublic Group

COST

Costco Wholesale Corp.

FITB

Fifth Third Bancorp

OMC

Omnicom Group

EL

Este Lauder Companies

BEN

Franklin Resources

DIS

The Walt Disney Company

GIS

General Mills

GL

Globe Life Inc.

VZ

Verizon Communications

HRL

Hormel Foods Corp.

GS

Goldman Sachs Group

VIAB

Viacom

SJM

JM Smucker

HIG

Hartford Financial Svc.Gp.

Consumer

AAP

Advance Auto Parts

K

Kellogg Co.

HBAN

Huntington Bancshares

Discretionary

AMZN

Amazon.com Inc.

KMB

Kimberly-Clark

ICE

Intercontinental Exchange

AZO

AutoZone Inc

KR

Kroger Co.

JPM

JPMorgan Chase & Co.

BBY

Best Buy Co. Inc.

MKC

McCormick & Co.

KEY

KeyCorp

BWA

BorgWarner

TAP

Molson Coors Brewing Company

LNC

Lincoln National

KMX

Carmax Inc

MDLZ

Mondelez International

L

Loews Corp.

CCL

Carnival Corp.

MNST

Monster Beverage

MTB

M&T Bank Corp.

DHI

D. R. Horton

PEP

PepsiCo Inc.

MMC

Marsh & McLennan

DRI

Darden Restaurants

PG

Procter & Gamble

MET

MetLife Inc.

DLTR

Dollar Tree

SYY

Sysco Corp.

MCO

Moody’s Corp

EBAY

eBay Inc.

CLX

The Clorox Company

MS

Morgan Stanley

EXPE

Expedia Group

HSY

The Hershey Company

NDAQ

Nasdaq, Inc.

F

Ford Motor Company

TSN

Tyson Foods

NTRS

Northern Trust Corp.

GPS

Gap Inc.

WBA

Walgreens Boots Alliance

PBCT

People’s United Financial

GRMN

Garmin Ltd.

WMT

Walmart

PNC

PNC Financial Services

GPC

Genuine Parts

Energy

APA

Apache Corporation

PFG

Principal Financial Group

HRB

H&R Block

BHGE

BAKER HUGHES

PGR

Progressive Corp.

HOG

Harley-Davidson

COG

Cabot Oil & Gas

PRU

Prudential Financial

HAS

Hasbro Inc.

CVX

Chevron Corp.

RJF

Raymond James Financial Inc.

HD

Home Depot

XEC

Cimarex Energy

RF

Regions Financial Corp.

KSS

Kohl’s Corp.

COP

ConocoPhillips

SPGI

S&P Global, Inc.

LB

L Brands Inc.

DVN

Devon Energy

STT

State Street Corp.

LVS

Las Vegas Sands

EOG

EOG Resources

STI

SunTrust Banks

LEG

Leggett & Platt

XOM

Exxon Mobil Corp.

SIVB

SVB Financial

LEN

Lennar Corp.

HAL

Halliburton Co.

TROW

T. Rowe Price Group

LOW

Lowe’s Cos.

HES

Hess Corporation

BK

The Bank of New York Mellon

M

Macy’s, Inc.

HFC

HollyFrontier Corp

TRV

The Travelers Companies Inc.

MAR

Marriott Int’l.

HP

HP

USB

U.S. Bancorp

MCD

McDonald’s Corp.

MRO

Marathon Oil Corp.

UNM

Unum Group

MGM

MGM Resorts International

NOV

National Oilwell Varco Inc.

WFC

Wells Fargo

MHK

Mohawk Industries

NBL

Noble Energy Inc

WLTW

Willis Towers Watson

NWL

Newell Brands

OXY

Occidental Petroleum

ZION

Zions Bancorp

NKE

Nike

OKE

ONEOK

Health

ABT

Abbott Laboratories

JWN

Nordstrom

PXD

Pioneer Natural Resources

Care

A

Agilent Technologies Inc

NVR

NVR Inc

SLB

Schlumberger Ltd.

AGN

Allergan

ORLY

O’Reilly Automotive

VLO

Valero Energy

ABC

AmerisourceBergen Corp

PHM

PulteGroup

WMB

Williams Cos.

AMGN

Amgen Inc.

RL

Ralph Lauren Corporation

Financials

AFL

AFLAC Inc

ANTM

Anthem

ROST

Ross Stores

ALL

Allstate Corp

BAX

Baxter International Inc.

RCL

Royal Caribbean Cruises Ltd

AXP

American Express Co

BDX

Becton Dickinson

SBUX

Starbucks Corp.

AIG

American International Group

BIIB

Biogen Inc.

TPR

Tapestry, Inc.

AMP

Ameriprise Financial

BSX

Boston Scientific

TGT

Target Corp.

AMG

AMGEN

BMY

Bristol-Myers Squibb

TIF

Tiffany & Co.

AON

Aon plc

CAH

Cardinal Health Inc.

TJX

TJX Companies Inc.

AJG

Arthur J. Gallagher & Co.

CERN

Cerner

TSCO

Tractor Supply Company

AIZ

Assurant

CI

CIGNA Corp.

VFC

V.F. Corp.

BAC

Bank of America Corp

CVS

CVS Health

WHR

Whirlpool Corp.

BBT

BB&T

DHR

Danaher Corp.

WYNN

Wynn Resorts Ltd

BRK.B

Berkshire Hathaway

DVA

DaVita Inc.

YUM

Yum! Brands Inc

BLK

BlackRock

XRAY

Dentsply Sirona

Stock list (continued)

GICS sector

Symbol

Security

GICS sector

Symbol

Security

GICS sector

Symbol

Security

Health

EW

Edwards Lifesciences

Industrials

RSG

Republic Services Inc

Materials

FCX

Freeport-McMoRan Inc.

Care

GILD

Gilead Sciences

RHI

Robert Half International

IP

International Paper

HSIC

Henry Schein

ROK

Rockwell Automation Inc.

IFF

Intl Flavors & Fragrances

HOLX

Hologic

ROP

Roper Technologies

LIN

Linde plc

HUM

Humana Inc.

SNA

Snap-on

MLM

Martin Marietta Materials

IDXX

IDEXX Laboratories

LUV

Southwest Airlines

NEM

Newmont Corporation

ISRG

Intuitive Surgical Inc.

SWK

Stanley Black & Decker

NUE

Nucor Corp.

JNJ

Johnson & Johnson

TXT

Textron Inc.

PKG

Packaging Corporation of America

LH

Laboratory Corp. of America Holding

UNP

Union Pacific Corp

PPG

PPG Industries

LLY

Lilly (Eli) & Co.

UPS

United Parcel Service

SEE

Sealed Air

MCK

McKesson Corp.

URI

United Rentals, Inc.

SHW

Sherwin-Williams

MDT

Medtronic plc

UTX

UNITED TECHNOLOGIES

MOS

The Mosaic Company

MRK

Merck & Co.

WM

Waste Management Inc.

VMC

Vulcan Materials

MTD

Mettler Toledo

Information

ACN

Accenture plc

Real

ARE

Alexandria Real Estate Equities

MYL

Mylan N.V.

Technology

ADBE

Adobe Inc.

Estate

AMT

American Tower Corp.

PKI

PerkinElmer

AMD

Advanced Micro Devices Inc

AIV

Apartment Investment & Management

PFE

Pfizer Inc.

AKAM

Akamai Technologies Inc

AVB

AvalonBay Communities

DGX

Quest Diagnostics

ADS

Alliance Data Systems

BXP

Boston Properties

RMD

ResMed

APH

Amphenol Corp

CBRE

CBRE Group

SYK

Stryker Corp.

ADI

Analog Devices, Inc.

CCI

Crown Castle International Corp.

TFX

Teleflex

AAPL

Apple Inc.

DRE

Duke Realty Corp

COO

The Cooper Companies

AMAT

Applied Materials Inc.

EQR

Equity Residential

TMO

Thermo Fisher Scientific

ADSK

Autodesk Inc.

ESS

Essex Property Trust, Inc.

UNH

United Health Group Inc.

ADP

Automatic Data Processing

FRT

Federal Realty Investment Trust

UHS

Universal Health Services, Inc.

CDNS

Cadence Design Systems

HCP

HCP

VAR

Varian Medical Systems

CSCO

Cisco Systems

HST

Host Hotels & Resorts

VRTX

node Pharmaceuticals Inc

CTXS

Citrix Systems

IRM

Iron Mountain Incorporated

WAT

Waters Corporation

CTSH

Cognizant Technology Solutions

KIM

Kimco Realty

WCG

WELLCARE HEALTH PLANS

GLW

Corning Inc.

MAC

MACERICH

ZBH

Zimmer Biomet Holdings

DXC

DXC Technology

PLD

Prologis

CELG

CELGENE

FFIV

F5 Networks

PSA

Public Storage

Industrials

MMM

3M Company

FIS

Fidelity National Information Services

O

Realty Income Corporation

AME

AMETEK Inc.

FISV

Fiserv Inc

REG

Regency Centers Corporation

ARNC

ARCONIC

FLIR

FLIR Systems

SBAC

SBA Communications

BA

Boeing Company

GPN

Global Payments Inc.

SPG

Simon Property Group Inc

CHRW

C. H. Robinson Worldwide

HPQ

HP Inc.

SLG

SL Green Realty

CAT

Caterpillar Inc.

INTC

Intel Corp.

UDR

UDR, Inc.

CTAS

Cintas Corporation

IBM

International Business Machines

VTR

Ventas Inc

CPRT

Copart Inc

INTU

Intuit Inc.

VNO

Vornado Realty Trust

CSX

CSX Corp.

JKHY

Jack Henry & Associates

WELL

Welltower Inc.

CMI

Cummins Inc.

JNPR

Juniper Networks

WY

Weyerhaeuser

DE

Deere & Co.

KLAC

KLA Corporation

Utilities

AES

AES Corp

DOV

Dover Corporation

LRCX

Lam Research

LNT

Alliant Energy Corp

ETN

Eaton Corporation

MXIM

Maxim Integrated Products Inc

AEE

Ameren Corp

EMR

Emerson Electric Company

MCHP

Microchip Technology

AEP

American Electric Power

EFX

Equifax Inc.

MU

Micron Technology

ATO

Atmos Energy

EXPD

Expeditors

MSFT

Microsoft Corp.

CNP

CenterPoint Energy

FAST

Fastenal Co

MSI

Motorola Solutions Inc.

CMS

CMS Energy

FDX

FedEx Corporation

NTAP

NetApp

ED

Consolidated Edison

FLS

Flowserve Corporation

NVDA

Nvidia Corporation

D

Dominion Energy

GD

General Dynamics

ORCL

Oracle Corp.

DTE

DTE Energy Co.

GE

General Electric

PAYX

Paychex Inc.

DUK

Duke Energy

GWW

Grainger (W.W.) Inc.

QCOM

QUALCOMM Inc.

EIX

Edison Int’l

HON

Honeywell Int’l Inc.

CRM

Salesforce.com

ETR

Entergy Corp.

IEX

IDEX Corporation

STX

Seagate Technology

EVRG

Evergy

ITW

Illinois Tool Works

SYMC

SYMANTEC

ES

Eversource Energy

IR

Ingersoll Rand

SNPS

Synopsys Inc.

EXC

Exelon Corp.

JBHT

J. B. Hunt Transport Services

TXN

Texas Instruments

FE

FirstEnergy Corp

JEC

JACOBS ENGR

VRSN

Verisign Inc.

NEE

NextEra Energy

JCI

Johnson Controls International

WDC

Western Digital

NI

NiSource Inc.

KSU

Kansas City Southern

XRX

Xerox

NRG

NRG Energy

LHX

L3Harris Technologies

XLNX

Xilinx

PNW

Pinnacle West Capital

LMT

Lockheed Martin Corp.

Materials

APD

Air Products & Chemicals Inc

PPL

PPL Corp.

MAS

Masco Corp.

ALB

Albemarle Corp

PEG

Public Serv. Enterprise Inc.

NSC

Norfolk Southern Corp.

AVY

Avery Dennison Corp

SRE

Sempra Energy

NOC

Northrop Grumman

BLL

Ball Corp

SO

Southern Company

PCAR

PACCAR Inc.

CE

Celanese

WEC

WEC Energy Group

PH

Parker-Hannifin

EMN

Eastman Chemical

XEL

Xcel Energy Inc

PNR

Pentair plc

ECL

Ecolab Inc.

RTN

Raytheon Company

FMC

FMC Corporation

Appendix B. Portfolio experiment results

Sharpe Ratio of portfolios

Holding period

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

Mean

Hist peripheral

0.63

0.52

0.54

0.63

0.73

0.58

0.75

0.58

0.66

0.62

0.85

0.45

0.73

0.57

0.49

0.51

0.53

0.58

0.43

0.65

0.70

0.55

0.45

0.49

0.59

0.63

0.60

0.52

0.68

0.66

0.66

0.67

0.61

0.62

0.55

0.74

0.48

0.63

0.54

0.55

0.57

0.53

0.61

0.47

0.53

0.68

0.56

0.46

0.53

0.59

0.62

0.59

0.58

0.68

0.65

0.66

0.71

0.66

0.62

0.62

0.73

0.53

0.62

0.58

0.50

0.62

0.50

0.63

0.54

0.61

0.65

0.57

0.48

0.55

0.60

0.66

0.63

0.60

0.73

0.64

0.67

0.71

0.70

0.63

0.61

0.72

0.56

0.60

0.61

0.54

0.61

0.53

0.63

0.56

0.59

0.67

0.62

0.53

0.59

0.62

0.57

0.58

0.56

0.67

0.61

0.66

0.67

0.65

0.59

0.62

0.69

0.54

0.63

0.62

0.53

0.58

0.53

0.64

0.58

0.61

0.69

0.66

0.52

0.58

0.61

0.59

0.60

0.57

0.67

0.65

0.65

0.69

0.65

0.60

0.62

0.69

0.56

0.60

0.64

0.56

0.58

0.55

0.64

0.57

0.62

0.69

0.65

0.54

0.58

0.61

Hist central

0.50

0.44

0.48

0.34

0.36

0.49

0.45

0.36

0.53

0.48

0.46

0.57

0.51

0.46

0.45

0.39

0.50

0.57

0.62

0.52

0.47

0.35

0.49

0.47

0.47

0.50

0.51

0.49

0.51

0.46

0.43

0.53

0.42

0.57

0.57

0.53

0.56

0.60

0.50

0.50

0.47

0.52

0.56

0.57

0.61

0.54

0.52

0.46

0.54

0.52

0.56

0.55

0.56

0.54

0.46

0.51

0.56

0.48

0.52

0.56

0.49

0.57

0.54

0.54

0.45

0.56

0.54

0.51

0.57

0.61

0.55

0.55

0.44

0.60

0.53

0.54

0.54

0.57

0.51

0.45

0.52

0.55

0.43

0.55

0.53

0.50

0.57

0.56

0.56

0.50

0.50

0.56

0.52

0.57

0.58

0.56

0.58

0.48

0.62

0.54

0.53

0.53

0.56

0.50

0.47

0.50

0.55

0.44

0.55

0.52

0.53

0.56

0.54

0.57

0.53

0.52

0.61

0.50

0.56

0.56

0.56

0.60

0.52

0.61

0.54

0.54

0.54

0.55

0.51

0.46

0.51

0.53

0.45

0.55

0.55

0.52

0.56

0.56

0.57

0.53

0.55

0.60

0.49

0.55

0.57

0.56

0.59

0.51

0.60

0.54

Pearson peripheral

0.51

0.40

0.36

0.51

0.49

0.39

0.53

0.45

0.35

0.63

0.23

0.41

0.23

0.49

0.47

0.42

0.65

0.46

0.37

0.50

0.42

0.39

0.53

0.39

0.44

0.68

0.61

0.53

0.66

0.64

0.45

0.57

0.60

0.49

0.67

0.49

0.44

0.43

0.51

0.61

0.55

0.64

0.51

0.55

0.59

0.43

0.48

0.53

0.42

0.54

0.65

0.68

0.56

0.74

0.58

0.55

0.63

0.60

0.58

0.62

0.55

0.52

0.50

0.53

0.61

0.55

0.66

0.56

0.59

0.57

0.49

0.56

0.47

0.43

0.57

0.62

0.59

0.53

0.62

0.57

0.46

0.62

0.55

0.50

0.56

0.56

0.51

0.60

0.55

0.64

0.55

0.64

0.52

0.63

0.56

0.53

0.59

0.47

0.45

0.56

0.62

0.61

0.56

0.63

0.53

0.49

0.60

0.55

0.50

0.56

0.55

0.52

0.61

0.57

0.59

0.59

0.61

0.54

0.63

0.59

0.53

0.59

0.50

0.48

0.56

0.60

0.59

0.55

0.59

0.58

0.52

0.57

0.56

0.53

0.58

0.60

0.53

0.58

0.55

0.62

0.58

0.57

0.58

0.62

0.58

0.51

0.59

0.51

0.48

0.57

Pearson cental

0.50

0.54

0.56

0.48

0.53

0.43

0.50

0.42

0.46

0.41

0.43

0.39

0.35

0.41

0.54

0.52

0.39

0.35

0.34

0.40

0.45

0.51

0.49

0.47

0.45

0.52

0.51

0.53

0.50

0.50

0.42

0.53

0.45

0.47

0.43

0.46

0.42

0.44

0.42

0.51

0.51

0.41

0.39

0.40

0.46

0.45

0.49

0.45

0.51

0.47

0.55

0.53

0.52

0.50

0.52

0.44

0.52

0.48

0.49

0.47

0.42

0.45

0.44

0.42

0.51

0.52

0.45

0.43

0.40

0.46

0.47

0.43

0.49

0.49

0.47

0.53

0.50

0.52

0.46

0.51

0.47

0.50

0.48

0.48

0.47

0.41

0.46

0.44

0.42

0.50

0.51

0.47

0.41

0.42

0.46

0.50

0.42

0.52

0.50

0.47

0.54

0.51

0.51

0.47

0.52

0.47

0.51

0.47

0.47

0.48

0.42

0.47

0.46

0.44

0.47

0.51

0.47

0.43

0.43

0.47

0.49

0.39

0.50

0.50

0.48

0.51

0.50

0.50

0.48

0.52

0.48

0.50

0.49

0.48

0.50

0.42

0.50

0.47

0.47

0.47

0.51

0.47

0.45

0.44

0.48

0.50

0.42

0.50

0.51

0.48

Volume peripheral

0.71

0.55

0.44

0.44

0.51

0.44

0.53

0.50

0.71

0.52

0.53

0.46

0.63

0.50

0.59

0.43

0.70

0.69

0.62

0.50

0.55

0.41

0.50

0.39

0.54

0.66

0.49

0.48

0.46

0.56

0.49

0.53

0.41

0.60

0.58

0.49

0.58

0.66

0.54

0.56

0.38

0.65

0.56

0.65

0.52

0.58

0.50

0.54

0.52

0.54

0.64

0.53

0.52

0.55

0.60

0.56

0.51

0.48

0.69

0.61

0.56

0.61

0.68

0.54

0.65

0.47

0.66

0.67

0.62

0.62

0.60

0.57

0.65

0.53

0.59

0.61

0.53

0.54

0.54

0.56

0.58

0.51

0.51

0.68

0.60

0.56

0.63

0.64

0.55

0.65

0.51

0.67

0.69

0.65

0.62

0.60

0.55

0.66

0.58

0.59

0.61

0.58

0.54

0.55

0.55

0.57

0.55

0.56

0.66

0.63

0.53

0.67

0.60

0.56

0.59

0.55

0.67

0.67

0.66

0.65

0.59

0.53

0.67

0.60

0.60

0.57

0.58

0.51

0.55

0.56

0.58

0.54

0.57

0.64

0.60

0.55

0.67

0.59

0.53

0.57

0.56

0.69

0.68

0.65

0.65

0.57

0.56

0.68

0.64

0.59

Volume central

0.35

0.41

0.44

0.34

0.45

0.36

0.54

0.37

0.41

0.43

0.35

0.27

0.30

0.48

0.36

0.37

0.33

0.35

0.30

0.35

0.36

0.26

0.39

0.21

0.37

0.46

0.52

0.41

0.43

0.48

0.40

0.49

0.46

0.38

0.46

0.36

0.34

0.44

0.47

0.38

0.40

0.28

0.32

0.32

0.40

0.37

0.36

0.38

0.28

0.40

0.46

0.46

0.37

0.41

0.48

0.35

0.52

0.47

0.40

0.44

0.35

0.32

0.49

0.47

0.42

0.44

0.31

0.34

0.44

0.44

0.39

0.35

0.36

0.31

0.41

0.53

0.46

0.38

0.44

0.50

0.36

0.56

0.46

0.44

0.46

0.33

0.34

0.43

0.46

0.44

0.46

0.32

0.36

0.46

0.41

0.41

0.36

0.36

0.33

0.42

0.54

0.50

0.42

0.44

0.47

0.40

0.54

0.46

0.47

0.45

0.33

0.40

0.44

0.46

0.47

0.49

0.33

0.41

0.46

0.41

0.43

0.38

0.35

0.34

0.43

0.52

0.49

0.44

0.45

0.48

0.39

0.54

0.46

0.48

0.48

0.34

0.41

0.44

0.47

0.50

0.47

0.35

0.42

0.46

0.44

0.43

0.39

0.38

0.35

0.44

Market cap – mega

0.34

0.33

0.35

0.34

0.35

0.34

0.33

0.36

0.38

0.40

0.31

0.34

0.36

0.32

0.40

0.37

0.34

0.34

0.36

0.33

0.34

0.35

0.39

0.37

0.35

0.30

0.31

0.27

0.31

0.30

0.32

0.32

0.33

0.30

0.31

0.25

0.32

0.32

0.32

0.36

0.31

0.34

0.28

0.32

0.35

0.39

0.27

0.33

0.26

0.31

0.44

0.43

0.42

0.40

0.40

0.41

0.44

0.41

0.40

0.39

0.39

0.39

0.41

0.42

0.41

0.42

0.38

0.34

0.41

0.41

0.41

0.39

0.37

0.36

0.40

0.38

0.38

0.36

0.40

0.40

0.37

0.41

0.40

0.38

0.40

0.38

0.37

0.37

0.40

0.42

0.41

0.37

0.33

0.36

0.42

0.42

0.42

0.40

0.38

0.39

0.41

0.41

0.40

0.41

0.40

0.39

0.40

0.40

0.42

0.40

0.40

0.38

0.38

0.40

0.42

0.40

0.39

0.36

0.37

0.43

0.42

0.43

0.40

0.38

0.40

0.41

0.40

0.41

0.42

0.40

0.40

0.43

0.43

0.42

0.42

0.42

0.37

0.38

0.42

0.43

0.44

0.40

0.37

0.38

0.43

0.43

0.43

0.40

0.40

0.41

Market portfolio

0.58

0.58

0.57

0.58

0.58

0.57

0.58

0.58

0.58

0.58

0.57

0.57

0.57

0.57

0.58

0.58

0.57

0.57

0.56

0.58

0.58

0.57

0.57

0.57

0.58

S&P500 index

0.40

0.40

0.39

0.40

0.40

0.39

0.40

0.40

0.40

0.40

0.39

0.38

0.38

0.38

0.40

0.40

0.38

0.38

0.37

0.40

0.40

0.38

0.37

0.38

0.39

Cumulative return of portfolios

Holding period

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

Mean

Hist peripheral

5.22

3.65

4.07

5.00

8.37

4.88

7.16

4.33

5.77

4.42

8.15

2.70

5.94

3.74

2.81

3.07

3.15

3.90

2.92

4.86

6.09

2.99

2.26

3.53

4.54

4.53

4.08

3.36

5.17

5.68

5.22

4.73

4.35

4.41

3.41

5.51

2.84

4.27

3.19

3.04

3.23

3.00

4.14

2.84

3.16

4.71

3.08

2.60

3.59

3.92

4.21

3.92

3.98

4.95

5.20

4.98

4.95

4.69

4.43

4.03

4.88

3.14

4.05

3.36

2.59

3.77

2.60

4.40

3.37

3.63

4.07

2.93

2.60

3.52

3.93

4.68

4.34

4.09

5.61

4.80

4.98

4.91

5.09

4.42

3.82

4.73

3.36

3.69

3.71

2.91

3.70

2.93

4.24

3.36

3.42

4.32

3.21

3.04

3.94

4.05

3.59

3.76

3.59

4.75

4.07

4.67

4.37

4.38

3.93

3.74

4.34

3.15

3.98

3.73

2.77

3.34

2.87

4.28

3.42

3.54

4.35

3.48

2.86

3.74

3.78

3.68

3.86

3.59

4.67

4.52

4.36

4.58

4.30

3.89

3.72

4.38

3.25

3.64

3.90

3.03

3.29

2.96

4.13

3.36

3.48

4.35

3.39

2.94

3.74

3.79

Hist central

2.84

2.40

2.63

1.81

1.97

2.71

2.39

1.89

2.95

2.59

2.56

3.01

3.09

2.50

2.40

2.05

2.38

3.03

3.73

2.76

2.40

1.60

2.48

2.47

2.53

2.75

2.78

2.64

2.76

2.51

2.24

2.86

2.18

3.10

3.19

2.97

2.95

3.51

2.53

2.54

2.53

2.43

2.79

3.22

3.42

2.76

2.60

2.20

3.06

2.77

3.18

3.10

3.19

2.93

2.55

2.80

3.09

2.50

2.83

3.13

2.61

3.10

2.93

2.88

2.26

3.18

2.65

2.71

3.09

3.35

2.89

2.81

2.11

3.46

2.89

3.00

3.01

3.19

2.70

2.40

2.81

3.02

2.25

2.97

2.86

2.72

3.11

3.03

3.04

2.60

2.70

2.81

2.74

3.06

3.12

2.94

2.98

2.37

3.63

2.88

2.95

2.92

3.13

2.69

2.50

2.70

3.00

2.24

2.89

2.77

2.98

3.03

2.83

3.11

2.74

2.87

3.19

2.57

2.93

2.98

2.92

3.15

2.51

3.42

2.88

3.01

2.97

3.04

2.74

2.46

2.67

2.80

2.31

2.89

2.96

2.90

3.03

2.99

3.04

2.73

3.01

3.08

2.51

2.97

3.08

2.91

3.11

2.56

3.45

2.88

Pearson peripheral

2.58

2.02

1.92

2.57

2.56

2.11

2.81

2.36

1.77

3.49

1.38

2.29

1.29

2.40

2.44

2.16

3.77

2.40

1.79

2.47

2.02

1.87

2.61

2.15

2.30

3.83

3.23

2.74

3.53

4.13

2.46

3.10

3.19

2.43

3.57

2.70

2.22

2.11

2.56

3.40

2.78

3.24

2.76

2.90

2.93

2.07

2.07

2.45

2.10

2.85

3.67

3.75

3.09

4.30

3.32

3.09

3.43

3.11

3.04

3.09

2.87

2.62

2.47

2.64

3.23

2.68

3.19

3.16

3.13

2.70

2.35

2.44

2.09

2.10

2.98

3.34

3.06

2.89

3.15

3.29

2.49

3.34

2.79

2.53

2.63

3.02

2.50

3.04

2.78

3.22

2.67

3.09

2.83

3.52

2.62

2.61

2.57

2.07

2.09

2.84

3.29

3.19

3.04

3.26

2.94

2.57

3.23

2.73

2.47

2.65

2.90

2.56

3.04

2.96

2.95

3.07

2.80

2.83

3.40

2.81

2.51

2.65

2.23

2.32

2.85

3.18

3.07

2.94

3.01

3.30

2.82

3.03

2.84

2.63

2.82

3.19

2.62

2.90

2.80

3.06

2.97

2.61

3.02

3.31

2.78

2.46

2.68

2.29

2.35

2.86

Pearson cental

3.35

3.69

3.95

3.08

3.56

2.60

3.08

2.57

2.80

2.33

2.66

2.31

1.86

2.42

3.76

3.52

2.04

1.80

1.76

2.17

2.58

3.28

2.91

2.98

2.79

3.43

3.32

3.52

3.25

3.19

2.54

3.34

2.74

2.91

2.41

2.90

2.50

2.44

2.37

3.22

3.30

2.10

2.02

2.16

2.62

2.53

2.90

2.46

3.19

2.81

3.71

3.44

3.28

3.14

3.27

2.64

3.16

2.88

2.99

2.71

2.45

2.68

2.40

2.34

3.02

3.30

2.37

2.39

2.11

2.63

2.73

2.41

2.74

2.91

2.82

3.37

3.11

3.30

2.75

3.18

2.88

2.97

2.86

2.92

2.72

2.41

2.72

2.41

2.28

2.92

3.15

2.52

2.22

2.23

2.61

2.92

2.25

2.98

2.97

2.78

3.45

3.19

3.14

2.84

3.21

2.80

2.99

2.78

2.79

2.82

2.41

2.79

2.55

2.45

2.63

3.02

2.57

2.42

2.25

2.63

2.85

2.06

2.89

3.09

2.78

3.11

3.00

2.98

2.92

3.22

2.83

2.93

2.91

2.76

2.95

2.45

2.94

2.69

2.62

2.63

3.04

2.53

2.50

2.29

2.72

2.85

2.27

2.82

3.14

2.80

Volume peripheral

6.51

3.82

2.67

2.54

3.53

2.72

3.57

3.11

5.68

3.02

3.85

2.42

4.08

3.09

4.00

2.42

4.27

5.36

3.37

2.76

3.49

2.09

2.55

1.88

3.450

4.98

2.92

2.96

2.65

3.83

2.92

3.20

2.15

3.86

3.35

3.12

3.40

4.30

3.31

3.37

2.00

3.40

3.50

4.27

2.92

3.81

2.63

2.68

3.04

3.273

4.44

3.35

3.17

3.51

3.91

3.58

2.97

2.67

4.35

3.68

3.77

3.75

4.54

3.13

4.09

2.56

3.59

4.38

3.80

4.03

3.80

3.27

3.63

3.35

3.639

4.13

3.34

3.35

3.49

3.59

3.72

3.00

3.08

4.25

3.55

3.75

3.97

4.09

3.27

4.02

2.91

3.76

4.50

4.08

3.91

3.86

3.04

3.68

3.83

3.673

4.08

3.81

3.21

3.50

3.44

3.47

3.31

3.51

4.03

3.77

3.48

4.28

3.57

3.27

3.46

3.20

3.90

4.08

4.11

4.14

3.75

2.98

3.92

3.91

3.674

3.59

3.77

2.94

3.43

3.47

3.54

3.24

3.51

3.84

3.52

3.54

4.24

3.40

3.08

3.31

3.29

4.32

4.30

3.98

4.14

3.57

3.16

4.04

4.23

3.644

Volume central

1.89

2.25

2.43

1.90

2.41

1.99

2.95

1.94

2.15

2.13

1.91

1.44

1.59

2.39

1.79

1.77

1.65

1.84

1.44

1.70

1.80

1.31

1.90

1.16

1.905

2.47

2.84

2.15

2.27

2.47

2.11

2.49

2.38

1.91

2.26

1.84

1.73

2.18

2.24

1.80

1.95

1.43

1.71

1.56

1.91

1.86

1.68

1.79

1.38

2.018

2.45

2.42

1.98

2.13

2.47

1.83

2.70

2.38

2.07

2.19

1.79

1.63

2.40

2.21

2.04

2.16

1.56

1.81

2.33

2.12

1.88

1.64

1.78

1.56

2.064

2.98

2.40

1.99

2.30

2.55

1.84

2.98

2.34

2.30

2.29

1.72

1.73

2.15

2.24

2.14

2.30

1.60

1.87

2.55

2.01

1.94

1.74

1.77

1.64

2.141

3.02

2.62

2.18

2.32

2.38

2.06

2.83

2.35

2.48

2.24

1.72

2.00

2.19

2.23

2.34

2.44

1.63

2.15

2.52

2.01

2.05

1.82

1.77

1.72

2.211

2.87

2.59

2.29

2.33

2.46

2.01

2.83

2.33

2.49

2.44

1.74

2.04

2.16

2.29

2.57

2.35

1.71

2.18

2.44

2.13

2.05

1.83

1.86

1.77

2.239

Market cap – mega

1.71

1.67

1.74

1.76

1.78

1.75

1.69

1.86

1.93

1.95

1.71

1.79

1.81

1.67

1.96

1.96

1.70

1.77

1.81

1.69

1.70

1.72

1.85

1.95

1.79

1.57

1.62

1.49

1.63

1.60

1.65

1.66

1.68

1.65

1.59

1.48

1.63

1.64

1.65

1.76

1.69

1.65

1.56

1.63

1.74

1.89

1.43

1.70

1.53

1.63

2.19

2.17

2.10

2.05

2.07

2.07

2.19

2.09

2.08

1.96

2.08

1.96

2.04

2.06

2.04

2.13

1.90

1.90

1.95

2.05

2.00

1.93

1.82

1.89

2.03

1.91

1.93

1.83

1.99

2.03

1.89

2.05

2.00

1.95

2.02

2.00

1.85

1.91

1.96

2.09

2.06

1.84

1.81

1.77

2.08

2.10

2.03

1.95

1.93

1.96

2.04

2.04

2.00

2.03

2.01

2.00

1.98

1.98

2.15

1.99

2.06

1.88

1.94

1.95

2.05

1.98

1.88

1.91

1.79

2.05

2.05

2.03

1.92

1.92

1.98

2.05

2.02

2.02

2.09

2.04

2.03

2.11

2.12

2.16

2.09

2.16

1.89

1.95

2.02

2.08

2.18

1.94

1.97

1.84

2.09

2.09

2.03

1.91

1.99

2.04

Market portfolio

3.39

3.38

3.21

3.37

3.39

3.22

3.28

3.33

3.27

3.24

3.30

3.16

3.09

3.11

3.14

3.29

3.00

3.21

3.00

3.15

3.17

2.90

2.94

3.21

3.20

S&P500 index

2.12

2.12

2.05

2.12

2.12

2.05

2.10

2.12

2.10

2.12

2.07

1.99

1.99

1.99

2.10

2.12

1.96

1.96

1.89

2.12

2.10

1.99

1.91

1.99

2.05

1% expected shortfall of portfolios

Holding period

10

20

30

40

50

60

70

80

90

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

Mean

Hist

peripheral

Hist

central

Pearson

peripheral

Pearson

cental

Volume

peripheral

Volume

central

Market

cap –

mega

Market

portfolio

S&P500 index