Abstract

In order to improve the logistics operation of food processing enterprises and control the logistics cost, this paper starts from the analysis of the logistics operation process and characteristics of enterprises, analyzes the logistics cost classification and composition of food processing enterprises, puts forward the basic process of applying TD-ABC to control the logistics cost, constructs the logistics cost accounting model of food processing enterprises based on TD-ABC, and puts forward relevant logistics cost control methods including the design of logistics cost control system, the determination of logistics cost control points and specific implementation steps. The typical food processing enterprises are selected for the empirical study of logistics cost accounting and controlling. By comparing the cost accounting results of TD-ABC and ABC, the result shows that TD-ABC (Time-Driven Activity-Based Costing) method can accurately grasp the logistics cost composition, identify inefficient logistics operations and non-value-added operations, and analyze the efficiency of various logistics departments, verify the feasibility and effectiveness of logistics cost accounting model and control method system, and provide some advice for logistics cost control and logistics process transformation of food processing enterprises.

Introduction

Background

Food enterprises are closely related to our lives. The output value of European food industry accounts for 2% of GDP. According to the statistical data of Chinese food industry association, Chinese food manufacturing industry grows by 5.3% in 2019 comparing with other industrial. COVID-19 outbroke around the world in 2020 has had a huge impact on the global economy. According to IMF, the global economy might shrink by 4.4% in 2020, while in the first three quarters of 2020, the economy in China has grown by 0.7%. Chinese economic growth rate has slowed down significantly, which has affected the purchasing power of consumers. Specially in food industry, the problem of food enterprises survival has aroused the concern of the society.

As food enterprises belong to labor-intensive industries, they have low technology content in production, warehousing, distribution and other links, and some sectors are generally controlled manually such as logistics warehousing and distribution links. Therefore, the logistics operation efficiency is low while the cost is high, and there are problems such as incomplete scope of cost statistics, imperfect cost control system, lack of cost control methods and so on. There is a certain gap in logistics cost control of food processing enterprises among China and developed countries [1]. Consequently, the study of logistics cost control method has certain theoretical and practical significance to reduce the total logistics cost of food processing enterprises and their industries.

Literature review

After implementing the reform and opening-up policy for 40 years, the improvement of economy not only enables the Chinese people have a better material life, but also changes their living style. They have stricter requirements for food safety and timeliness. Based on this background, food logistics, as a popular research direction, are concerned by many scholars.

Zhu and Zhu pointed out that establishing and improving the agricultural industrial chain organization can boost suburban agricultural industry [2]. In order to keep the fresh and safety of food product, it is essential to utilize cold chain logistics. Accordingly Di et al. proposed that food cold-chain logistics is a kind of special logistics which requires a lot of refrigeration equipment or facilities and he advocated the whole related party including government, trade association, relevant college and university, third-party logistics enterprise and food producer should play a role in this development [3]. With further researches, Xiong realized that backward logistics facilities, lack of cold chain standards and expensive logistics cost limit the development of Chinese cold chain logistics for agricultural product [4]. Liu et al. advised that building an agricultural product cold chain logistic system which is based on supply chain management can coordinate the interests among agricultural production materials suppliers, farmers, agricultural operators and consumers [5]. Lai et al. invested the willingness to use food chain logistics in Changle district and concluded that cold chain logistics industry still has promotion space [6]. Tang pointed out that many problems like poor rural road conditions, insufficient special vehicles and low utilization rate of electronic information exist in Chinese agricultural product logistics [7].

Chen et al. researched the coordination mechanism of members in supply chain on the basis of the customers’ choice behavior of product with different freshness and taste and it is a way to strengthen the comprehensive international competitiveness of Chinese food industry [8]. Yalunina proposed a modular approach to reduce the costs of logistics services in the activity of the food processing industry [9]. Li and Li suggested reducing the cost of fresh cold chain logistics by cost multimodal transportation, new retail trend, talented staffs, government supervision and policy support [10]. Wang et al. considered that application of Internet 5G and things technology can improve logistics processes, system and practice [11]. Liu and Wang discussed the operating risks existing in cold chain logistics outsourcing of fresh food enterprises through establishing an evolutionary game model [12]. Li et al. used kernel density estimation (KDE), spatial autocorrelation analysis (SAA), and spatial error model (SEM) to illustrate that the spatial distribution of cold storage in China is unbalanced [13]. Li et al. Established a green fresh food logistics with Heterogeneous fleet vehicle route problem (GFLHF-VRP) model to reduce the cost of fresh food logistics [14].

With the practice of many enterprises and the research of scholars, the role of Activity-Based Costing in reducing the logistics cost of enterprises is more and more concerned in academia. The guiding ideology of activity-based costing is: “Cost object consumes activity, activity consumes resource” [15]. Activity based costing treats direct cost and indirect cost (including period cost) as the cost of product (service) consuming activity equally, which widens the scope of cost calculation and makes the calculated product (service) cost more accurate and real.

Sittivangkul and Laosiritaworn took vegetable industry as an example, and calculated logistics cost by using a case study from vegetables processing organization with ABC method and finally eliminated hidden costs to adjust price [16]. Themido et al. suggested that the ABC method can simultaneously reflect the flow of orders and products along the logistic chain and capture the costs at a level of desegregation in order to enable the analysis of profit by type of client, market segment and distribution channel [17]. Suttishe et al. made use of activity-based cost model and computer simulation to solve traffic jam at border and lots of trucks waiting for custom processes, and it provided an access way to identify useless activity in transportation and reduce transportation cost [18]. Sternad determined the cost structure of different types of transport vehicles and the changes of fixed and variable costs in the case of different mileage with using ABC costing methods [19]. Ziyadin et al. created a method for classifying logistics services based on the use of ABC analysis to improve companies’ competitiveness [20].

To sum up, the research on the logistics cost control method and implementation of food processing enterprises is not enough, and there is less research in combining the logistics process characteristics, cost composition and logistics cost control method of food processing enterprises with practical application [21].

Comparing with other similar works, this paper contributes time driven activity-based costing method to help company managers to detect and control their cost more scientifically and targeted. Moreover, TD-ABC uses how much time spent in each activity as the basis of collecting costs, which is relatively novel with other ABC method.

On the basis of studying the current situation of logistics cost control of food processing enterprises, this paper studies the characteristics of logistics operation and the occurrence of logistics cost, analyzes the occurrence process of logistics cost and measures its cost, constructs the logistics cost control model of food processing enterprises based on time driven activity-based costing, and constructs the logistics cost accounting control system of food processing enterprises, research the feasibility of logistics cost accounting and control in food processing enterprises empirically Using “time driven activity-based costing” to control the logistics cost of food processing enterprises and dividing the value-added and non value-added activities of the empirical enterprises,can provide the basis for enterprises to control logistics cost and optimize logistics process.

Logistics cost problems of food processing enterprises

Logistics costs of food processing enterprise mostly occur in the storage, distribution, transportation, and the logistics activity process mainly include “production, product into warehouse, product in stock, product out of warehouse, and product in transportation”. Specifically, the logistics activities include production logistics activity, product into warehouse logistics activity, product in stock management logistics activity, product out of warehouse logistics activity, and logistics activities those are after out of warehouse like distribution, transportation, etc. are included. Product in stock management activity include stocktaking at the end and beginning of each month.

The problems in the logistics cost control of food processing enterprises are as follows:

The statistics method of logistics cost is simple and the scope of statistics is incomplete. The logistics cost report only counts the transportation costs paid to the external. There is lacking of reasonable and effective method to calculate logistics cost. Most enterprises choose to analyze the logistics cost through the existing financial data, a few enterprises use the annual sales of enterprises to estimate the logistics cost. The accounting method of logistics cost is simple, the rate of accuracy and timeliness is not high. Effective integration of logistics information is lack off. Food processing enterprises pay attention to the input of information system but lack of effective integration of logistics information and data. There is lacking of practical logistics cost report. The existing logistics cost report of food processing enterprises is not quite practical, or the content of logistics cost report is not comprehensive.

Composition of logistics costs of food processing enterprises

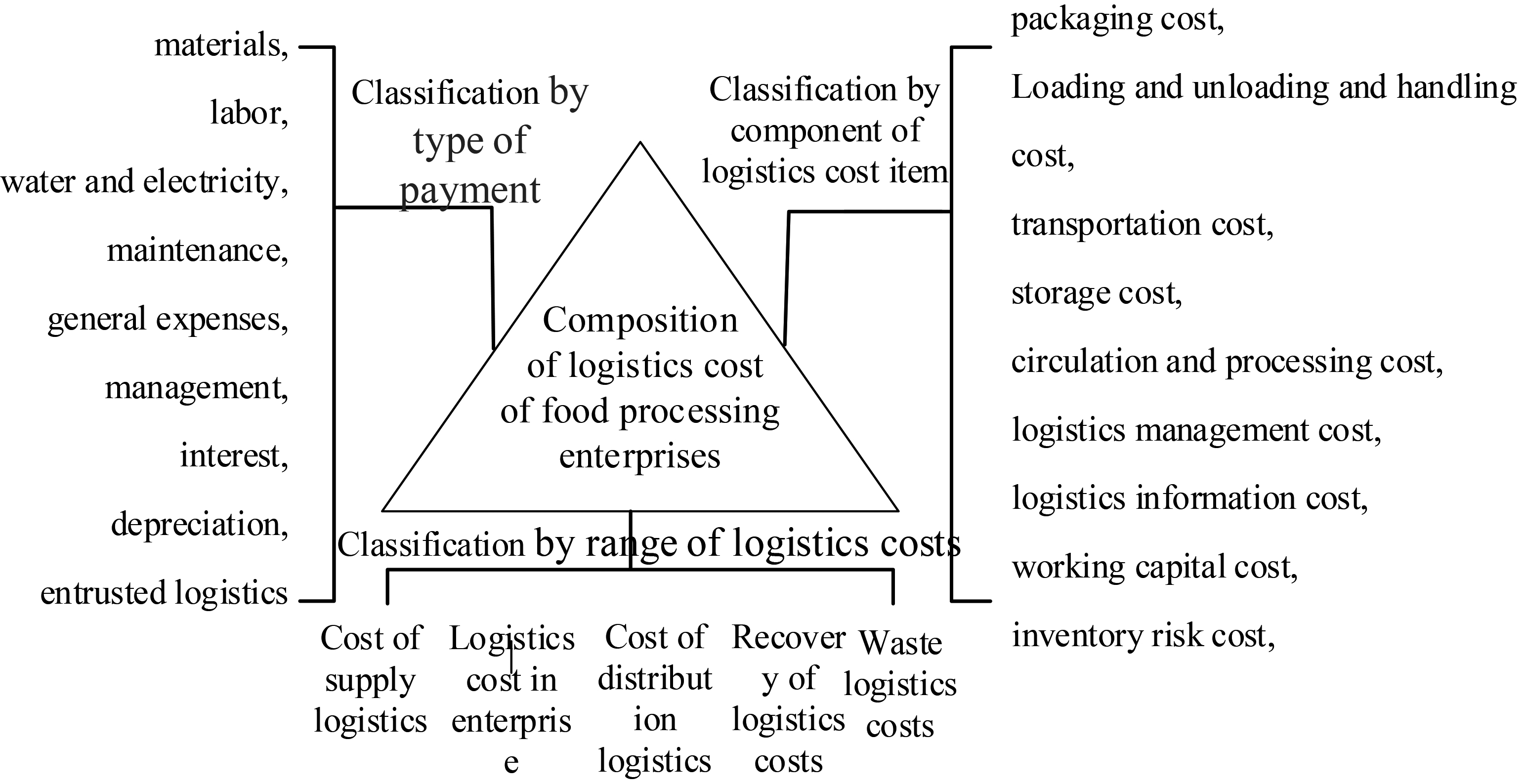

The logistics cost of food processing enterprise refers to the monetary sum expended in materialized and living labor occurred in food products’ space transfer and storage activities in enterprises. That is, the food processing enterprise logistics costs mainly consist of the sum of labor, material and financial expenditures in the transportation, packing, loading and unloading, storage, distribution, logistics information and management of logistics activities.

Classification and composition of logistics cost of food processing enterprises.

According to relevant national standards and logistics activities, the logistics cost components of food processing enterprises are classified based on three standards: logistics cost items, cost scope, and payment type. As shown in Fig. 1, the cost items on the left are classified according to payment mode. Right cost items are classified according to the composition of logistics cost items, where inventory-related costs include working capital occupation cost, inventory risk cost and inventory insurance cost. The cost items below are classified according to the logistics cost scope. Logistics costs are mainly concentrated in the food processing enterprises’ storage, distribution, transportation and other departments.

Time-Driven Activity-Based Costing (TD-ABC, Time-Driven Activity-Based Costing) is based on the characteristics of different enterprises of different industries and resource consumption etc. The cost is decomposed into different assignments and specific operations. Taking time as the basis of allocating resources costs, the management researchers estimate unit actual cost of each activity and unit operation actual time needed, then calculate the unit cost of different activities.

It can turn a wide range of working procedure cost into an easy implementation and promotion of simple method, avoiding difficult problems of activity-based costing method in the process of implementation. That is the reason why this method is chosen.

Using TD-ABC method, logistics cost can be divided into two parts: time cost and activity cost.

Specific steps for food processing enterprises to implement TD-ABC

Determine the operation center (namely the resource repository) Determine the work items in the logistics process of food processing enterprises and the identify the main logistics department as the operation center, for example, the operation centers are divided into warehousing logistics department, order processing department, sales logistics department etc. Determine activity-based cost items The activity-based cost items of logistics service are determined according to the divided activities. Calculate the TD-ABC logistics cost

Identify resources and divide it into direct and indirect resources Logistics resources refer to the cost that support logistics operations and sources of related expenses, and they are also the costs and expense items that occur in logistics activities of an enterprise during a certain period, or the price for performing logistics operation cost, usually include labor cost, packaging cost, energy consumption, logistics facilities acquisition fee, logistics project capital occupation cost etc. Estimate effective working time Combined with practical experience, the logistics manager can effectively estimate the actual time consumption in different stages and operation states of logistics, in other words, the effective working time. Calculate productivity cost per unit of time First, calculate the standard cost per unit of productive time. Secondly, the time quota of each logistics operation is determined, among which the time quota of logistics activities is used to reflect the time consumption of each logistics operation involved in the enterprise logistics process. Finally, productivity cost per unit of time According to different time drivers identified, collect the time cost and activity cost consumed by each specific time logistics activity and allocate them to products (or logistics services). Allocate the direct logistics cost to the final product (or logistics service) together with the indirect logistics cost allocated according to unit time productive cost and time cost driver rate, and issue the cost report of related logistics cost.

Determine the model

The basic equation of TD-ABC method is: the cost of resources supplied

Accounting steps

Determine the operation center, namely the resource repository Estimate the cost of each repository, divide direct resource cost and indirect resource cost. Assuming that the total resource cost supplied by the logistics activities of food processing enterprises is RC, the resource cost of the used logistics activities is URC, the direct cost of the used logistics activities resources is DURC, the indirect cost of the used logistics activities resources is IURC, and the cost of excess production capacity is UNURC, then:

Estimate the actual capacity of providing resources by each resource repository. That is the ratio of the total output of the operation to logistics resources, which is mean how much the actual logistics resources play the role of logistics services. Enterprise managers and department heads estimate the actual capacity utilization rate and effective working time of each department based on experience. Assuming that NE is the number of employees, ND is the number of working days per month, DH is the number of working hours per day, and ECU is the effective capacity utilization rate of resource repository, then EWT is effective working minutes of each department:

Calculate the unit resource capacity cost for each resource repository Supposing that the food processing enterprise has

In the equation:

Standard productivity operation per unit of No.

In the equation:

The enterprise unit activity cost of No.

In the equation:

Gather the time consumed by logistics activities at each specific time based on different time drivers. In the logistics activities of food processing enterprises, the time consumed by the same operation under different distribution volume is different. In order to solve the problem of different time consumption in different situations, a basic time equation is set up to reflect the time spent in different situations. Supposing that in the logistics activities of food processing enterprises. The unit estimated consumed time of No.

Supposing that the number of time drivers required to complete activity

Therefore, the unit indirect operating cost of item

Considering the capital occupation cost, supposing that the logistics business of food processing enterprises should occupy a certain capital cost, the unit capital cost of the

In the formula:

Calculate the cost of logistics activities used by food enterprises. The unit operating cost of

The sum of unit cost of No.

The integrated logistics costs of logistics activities used by food processing enterprises are:

Design of logistics cost control system

The cost factors involved in the logistics process are reasonably set up and regulated. Finally, through the post-analysis, the optimized logistics process is found out, and the logistics cost of food processing enterprises is controlled from the overall point of view. In the process of logistics cost control, it is necessary to explore the influence of each cost factor on total logistics cost control and control it pointedly, and then logistics links that need to be improved and optimized in logistics cost control are found out to improve logistics management and improve logistics service level.

Determination of logistics cost control point

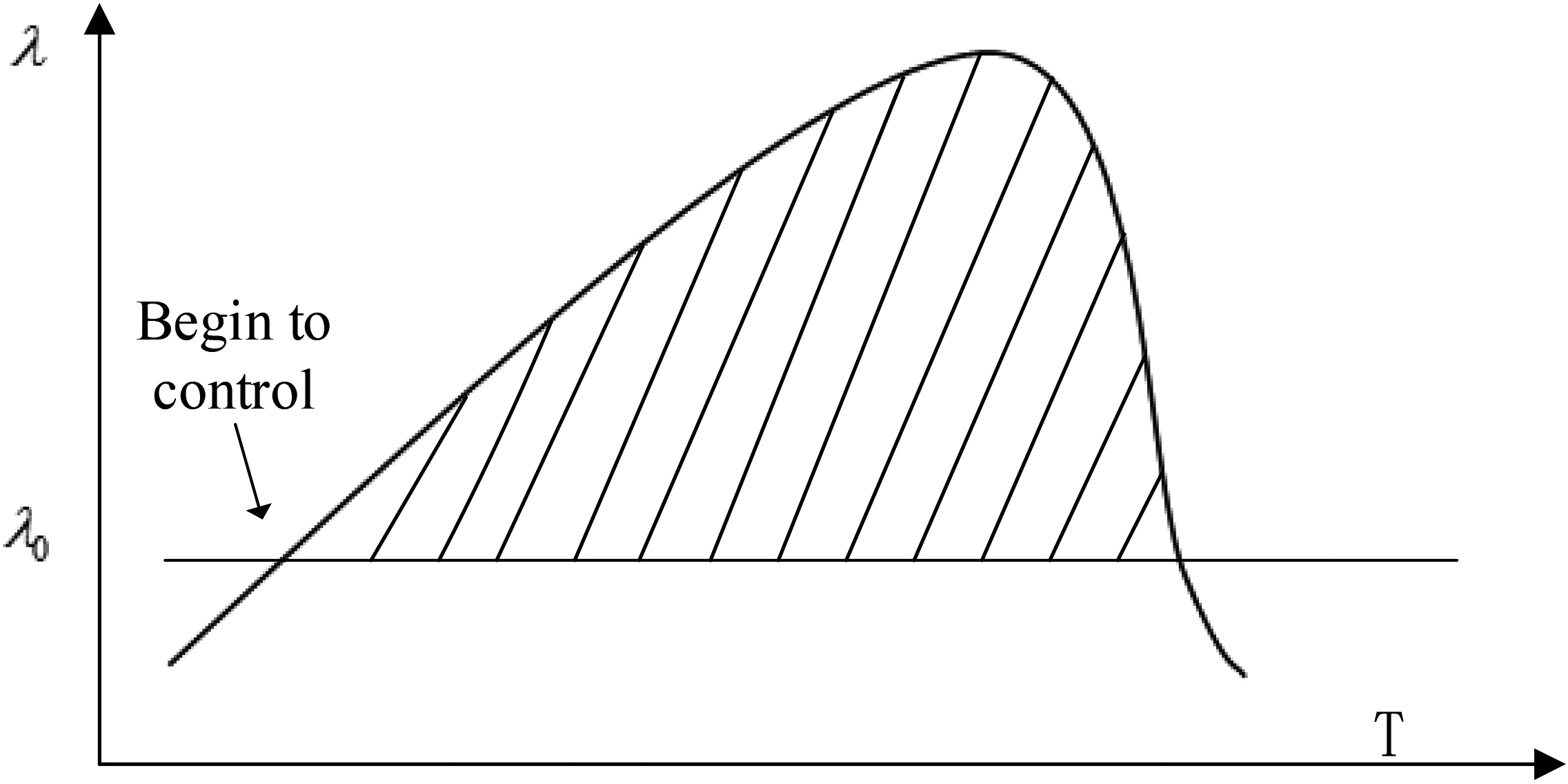

Different enterprises in the food processing enterprise group have different acceptance of logistics cost change, and after the use of the TD-ABC to calculate the logistics cost of each cycle, enterprises can not determine whether cost control should be carried out or which department should be controlled according to the value of total cost. In order to find out the reasons for the increase of logistics cost more accurately, the corresponding methods of controlling logistics cost are worked out by seeking the time point and the breakthrough point of logistics cost control.

Determination of logistics cost control time points According to the change of logistics cost data monthly, judging when to make logistics cost control decision and plan is helpful to maximize the overall economic benefit of the enterprise. The steps of controlling time point are determined as follows:

Assume that one month is an accounting cycle of logistics cost, and the quality of logistics cost control has a certain impact on the change of profits. Because logistics costs affect the profits of enterprises, there is the following relationship: First of all, set the standard logistics cost of

In the formula:

Secondly, the objective cost is assumed:

In the formula:

The total cost of t month

In the formula:

Suppose a food processing enterprise sets an evaluation index

Time points controlled by a food processing enterprise. As shown in Fig. 2. Identification of the breakthrough points for logistics cost control After determining the control time point, the cost items should be overall analyzed to find out the key logistics activity items that affects the logistics cost control, which can help the food processing enterprises to control the logistics cost in time and effectively. The monthly

Compare and analyze logistics cost data in the month: each column in the corresponding matrix of the change of numerical value is needed to be observed, and when the Compare and analyze the logistics cost data of each month of the enterprise: the Comprehensive analysis of enterprise logistics costs: combined with 3.19 and 3.20, the change of each value is analyzed. When the

Set standard activity costs and target costs Whether the logistics activities of food processing enterprises can bring benefits to enterprises depends on value-added operations. The goal of logistics control is to reduce the costs caused by value-added operations and to avoid the costs of non-value-added activities at the same time. Therefore, it is necessary to continuously improve the standard cost of value-added operations to meet customer needs as much as possible and reduce or maintain the logistics costs of enterprises. Suppose ZBQ represents the standard number of value-added logistics activities, BVC is the standard unit variable cost, BFC represents the standard unit fixed cost. Then the value-added logistics activity cost ZBC standard calculation formula is:

Non-value-added logistics activities can not bring positive benefits to enterprises, so the ideal standard cost should be 0. Assuming that RQ represents the number of actual logistics operations, the formula for calculating the standard cost BFC of non-value-added logistics activities is:

According to the reasonable standard established by the food processing enterprise, they can compare their own logistics with the advanced logistics activity index of large food processing enterprises when analyzing the logistics cost information and controlling the logistics cost to find problematic activities and take measures to improve the activity, improve their own logistics cost control benchmark continuously, and make real-time adjustment of their target costs. Performance appraisal and variance analysis After the actual logistics activity cost statistics is completed, it is compared with the target cost of the month and the previous period, and the causes of the cost difference are comprehensively analyzed and found out. Compared with the previous logistics operation mode, whether the existing operation will reduce the cost and increase the benefit needs feasible performance evaluation system to guide the continuous improvement of the logistics cost control mode. Determining whether logistics activity is a value-added activity After performance evaluation, value-added and non-value-added activities are distinguished, which provides the basis for further optimization of operations and improvement of logistics processes. Non-value-added activities are operations that can be avoided or reduced without affecting the quality of customer service. Value-added logistics activities are the key activities of food processing enterprises’ logistics activities, which can save resources and bring profits for food processing enterprises. Activity optimization and process improvement On the basis of difference analysis, performance evaluation, judgment of operation nature, logistics activities are optimized or various logistics activities from the level of logistics activity are redesigned and organized which make logistics cost control develop to the best condition. In addition, considering that logistics operations are interrelated and multiple activities operated by multiple logistics departments are involved, the staff of each department need to take effort and cooperate actively.

The process of a food processing enterprises’ logistics cost

Logistics cost process analysis in supply stage

A food processing enterprises mainly has three processing factories A1, A2, A3. In the supply and production stage, after inspection, cleaning and other pre-processes, the raw materials are entered into the assembly line for processing and production, and deliver out of the warehouse with unified packaging. The logistics costs incurred consist of such as raw materials transportation costs, product packaging costs, etc. These costs are directly included in the production costs of company’s product and are not reflected in detail.

Internal logistics cost process

After products are manufactured, A food processing company stores their products in the distribution center warehouses a1, a2, and a3. According to the logistics costs occurred by food processing companies of payment characters, they are classified into material costs, labor costs, water and electricity costs, etc., which can be directly extracted from the corporate financial data. The basic situation of each storage center is summarized in Table 1, which shows that at this stage, the logistics costs of this company are mainly the storage cost of the product in the warehousing, the capital occupation cost of the warehouse, the inventory management cost and other logistics costs occurred in the warehousing department.

A basic status of annual warehousing of food processing enterprise

A basic status of annual warehousing of food processing enterprise

The sales logistics costs of A food processing companies are: Firstly, according to the payment characters, the company’s self-operated transportation and distribution of goods logistics costs can be classified into labor costs, fixed assets depreciation fee, vehicle maintenance fees, Vehicle and vessel usage tax, insurance, maintenance and repair costs, road and bridge fees, fuel costs, various fines and other costs. Sorting out financial data and warehouse receipts and self-operated transportation costs are shown as Table 2.

Annual self-operated costs for enterprises

Annual self-operated costs for enterprises

The second is the logistics cost of products outsourced to third-party logistics company. The number can be extracted directly from the corporate financial statements and the transaction statements with various logistics companies. The annual sales process logistics costs paid to the third-party logistics companies are 21 552 532 yuan, accounting for 11.8% of the total sales.

The logistics activities in the recovery stage mainly are those recycling logistics activities generated in the purchase, production, packaging, and sales. They mainly occur in departments like production, purchasing, customer service, and warehousing department, but the proportion of occurrence is relatively small. The reason of that is the products’ value is not high.

Process analysis of logistics cost in waste stage

The logistics activities in the waste stage mainly are those waste logistics activities generated in the purchase, production, packaging, storage and transportation. They mainly occur in departments like purchase, production, warehousing and transportation departments. Those logistics costs are mainly loss and expenditure. Most of them are directly included in the production cost of the product, and it is impossible to obtain detailed and accurate logistics cost loss. A small part of these costs goes directly to the sales cost or management cost of the product, and the remaining part of the waste logistics cost is undertaken by the customers.

Application of logistics cost accounting model of a food processing enterprises

Application of TD-ABC logistics cost accounting

TD-ABC is used to calculate the logistics costs of enterprises, and the following simplifications and assumptions are made:

All data are rounded on the basis of the real financial data of the enterprise and the statistical data of the logistics department. Because the logistics cost of the procurement and production stage is relatively low compared with the overall logistics cost of the enterprise. It is difficult to accurately count, so it is not considered. The order quantity and order volume in October are relatively average, and the logistics cost data in October is selected as the basis for relevant analysis. The cost categories and activity centers of logistics activities are adjusted simply.

Determine the logistics activity center (resource repository) The three main logistics-related departments of the enterprise are used as resource repositories (also called activity centers) for logistics activities, namely, order processing department, warehousing management department, and sales logistics department. The warehousing management department includes 3 sub-activity centers, namely A1, A2, and A3 warehouses. The sales logistics department, that is, the transportation department, includes 2 sub-activity centers, which are the self-operated logistics department and the outsourced logistics department. Determine the cost item Division of specific activities and sub-activities and determination of the product’s operation cost items are shown in Table 3. Worksheet and time drivers

TD-ABC logistics cost calculation

Division of direct and indirect logistics resources In enterprise logistics activities, labor costs and material costs that can be directly traced back to the cost of the order is quite diminished, while the costs paid to third-party logistics companies are much more. Thus, assuming that they are calculated as direct logistics costs and not allocated as indirect costs. Determination of the effective working hours of each department Managers who are familiar with the business estimate the actual working time involved in TD-ABC and the unit working time of various operations. The effective working hours of the company are shown in Table 4. Effective working hours

References