Abstract

In actuarial science related to pension systems, it is widely assumed that the rate at which the reserves cover the payment of annuities (calculated for a given number of lives) is equal to the expected rate of return of the portfolios in which such reserves are invested. Given this assumption, pension fund managers may take greater risks to realize higher returns and subsequently reduce their pension liabilities. This study demonstrates that the discount rate used to calculate a two-life annuity and the expected return on the portfolio are not necessarily equal. A stochastic-based model is used to determine the proper discount rate for calculating the two-life annuity. The model includes fluctuations of both the interest rate and the payments made by the annuity. In general, this study contributes to the stability of pension systems by determining the appropriate discount rate when computing required actuarial reserves or the portfolio’s required rate of return given a reserve.

Introduction

How to calculate the actuarial reserve that is required to cover the payments of a two-life annuity is a fundamental issue for a pension system and for insurance companies. In actuarial science, this reserve is computed as the sum of the present values of all future feasible payments. This calculation involves variables such as the life expectancy of the individuals, inflation rates, ages, the amount of the future payments, and the discount rate known as the technical interest rate, defined as the minimum rate at which a portfolio yields positive returns (also known as the warranted rate). In an empirical study, Eling and Holder [1] compare the way in which regulators set maximum technical interest rates in life insurance in Germany, Austria, Sweden, the UK, and the United States. They state that the German method is the most popular; it is based on the calculation of the historical rate paid on government bonds, given that it is assumed that the technical interest rate is the minimum rate that a fund manager can commit to providing with the insurance company. The regulators in Austria, Sweden, the UK, and the United States include some adjustments in estimating the technical rate that make their computations more flexible in the face of macroeconomic shocks.

The calculation of the reserve required to cover the payments of a two-life annuity, which has been the most common annuity in the market, directly impacts the stability and coverage of pension systems, and consequently the quality of life of individuals, independently of the model followed to calculate such a reserve and its derived benefits.

Battocchio and Menoncin [2] suggest that there are basically two kinds of pension plans. First, there are defined-benefits plans, in which the benefits are previously determined by the pension fund manager and the contributions to the plan are adjusted to keep the fund balanced. In the second kind, defined-contribution plans are characterized by fixed contributions and the future benefits depend on the portfolio returns. Battocchio and Menoncin [2] state that most plans are defined-contribution plans, which transfer most of the default risk to the workers.

As described by Bodie and Crane [3], defined-contribution plans are more popular because they allow employees to know at any time the value of their retirement account and because this sort of plan is much easier to manage than a defined-benefits plan.

The actuarial science on annuities assumes that the discount rate used to compute the required reserves is the same as the expected rate of return of the portfolios in which such reserves are invested [4, 5]. This assumption is orthogonal to the distinction between defined-contribution and defined-benefit plans. Consequently, the problem of choosing the best investment strategy to manage the pension funds is becoming more and more relevant in these sorts of portfolios [6].

It is a widely accepted practice to use the expected discount rate of the portfolio in which the funds are invested as the discount rate in computing the required reserves. According to Merton [7], such a practice may drive pension fund managers to take excessive risks to earn greater profits and to reduce their liabilities positions. Additionally, Cairns [8] suggests that deterministic models are suitable for estimating future cash flows and valuation, while stochastic models allow one to investigate the dynamics of pension funds over time. Cairns [9] uses a similar theoretical framework by adding uncertainty in the estimation of the parameters. Specifically, he uses stochastic interest rates as an application to an insurance of single payment and based on this he estimates the parameters of the feasible distributions of the accrued interest rate. However, Cairns [8, 9] does not make any difference about the annual return that the actuarial reserve should have. Similarly, Nielsen, Sandmann and Schlögl [10] develop the needed equations to calculate the return guarantee in an equity-linked pension scheme, but constraining the model to the existence of a retirement system that guarantees such minimum rate.

Battocchio and Menoncin [2] specify the behavior of the stochastic variables using the most common functional forms adopted in the literature. Particularly, they model the term structure of the interest rate according to Cox, Ingersoll and Ross [11]; that model does not return negative interest rates as in the model suggested by Vasicek [12]. Additionally, by using stochastic models of interest rates and volatility, the recent work of Luo, Metawa, Yuan and Elhoseny [13] analyze optimal investment strategies for insurance companies, while Liu, Yang, Zhai and Bai [14] analyze such variables for pension funds by including uncertainty in the portfolio rate of return and in the wages of workers. In the same line, the approach followed by Devolder, Bosch Princep and Dominguez Fabian [15], Gerrard, Højgaard and Vigna [16], Josa-Fombellida and Rincón-Zapatero [17], and Konicz and Mulvey [18] uses the stochastic optimal-control tool to find out the optimal investment strategy, without including in the constraints a minimum portfolio return. These authors take for granted that the technical discount rate must be equal to the risk-free rate, which is used to discount the future payments of the annuity. The major drawback of this approach is that the optimal strategy could change if it is demonstrated that the discount rate and the technical rate are not necessarily the same.

This paper demonstrates that if one abandons the assumption of constant interest rates, it is not suitable to assume that the discount rate used to cover the payment of the joint-and-survivor annuities is equal to the expected rate of return of the portfolios in which such funds are invested. The suggested model is built upon an equation that describes the required reserve for this two-life annuity, with certain ages and with its respective change in the face of stochastic behavior of the technical interest rate. The dynamics of the interest rates are modeled according to the equation provided by Cox, Ingersoll and Ross [11], while the future payments are modeled based on Brownian motion.

The next section introduces the suggested model; the subsequent section describes its application to the Pension Fund of the Territorial Entities of Colombia (Fondo de Pensiones de las Entidades Territoriales de Colombia), and finally the article presents its major conclusions and remarks.

Model

Preliminaries

Survival function and probabilities

Let S (π) be a survivor function that indicates the likelihood that the age of death (Π) of a person will be higher than a certain age, π. Hence,

Therefore,

For the case of joint-and-survivor annuities, considered as independent and with ages ϕ and γ, respectively, the probability that at least one of them will survive for at least t years is defined as follows:

Required reserve for a two-life annuity

The required reserve for the annuity payment will be the sum of the expected present values of the feasible payments [20]. The model assumes an annuity payment (x) with compensation that increases at the same rate as the consumer price index in the case in which the person does not die and zero (0) otherwise.

Where x t is defined as the amount of the monthly payment at moment t; r is the nominal interest rate; ρ is the percentage change in the general level of prices; ϕ, γ are the current ages of the insured people; w - min(ϕ, γ) is the maximum time that the youngest insured person can live; R N is the required reserve for the payment of the annuity.

This equation, expressed in continuity, is as follows:

Change in the required actuarial reserve with the stochastic interest rate

Suppose a certain country’s interest rate follows a Cox, Ingersoll and Ross [11] process such as the following:

The amount of the monthly payment x (t) follows the stochastic process known as the Itô process:

Further, Cov (dW t , dU t ) = ρ * dt.

Therefore, the Itô [21] lemma applied to the required reserve R N defines the change in the reserve before changes in the interest rates in the monthly payments and over time.

Hull [22] demonstrates that the change in the price of the financial derivative—whose price depends on many underlying variables that follow their own stochastic process—can be modified as follows.

If G depends on x and y at timet,

This is true so long as the change in each variable is such that

According to this condition, if R

Nt

depends on r

t

and x

t

.,

Required technical interest rate

Suppose that the change in the constituted reserve R

C

is described according to the following stochastic differential Equation [23]:

The condition dR

Ct

= dR

Nt

is needed to maintain the equilibrium of the actuarial structure [24]. This implies the following:

Therefore,

In this case, the following is true:

Solving r (t) is the interest rate at which the annuity reserve must be calculated.

Therefore, the required reserve for the two-life annuity payment will be as follows:

Regarding the sensitivity of μ

t

relative to each of the parameters, as expected, there is a direct relationship between this variable and the amount of the monthly payment x, the trend of amount m, and its volatility n.

The same direct relationship is observed with the volatility of the interest rate, v.

Consistent with the previous result, the faster the reversion to the mean (α), the higher the required return (μ

t

) to keep the pension system in equilibrium:

A comparable effect, although with a different magnitude, is observed in the actuarial reserve.

Application

Pension funds of the territorial entities of Colombia

Until 1993, in Colombia, there were diverse pension plan schemes. One of them benefited the civil servants of the national territorial divisions, such as departments and municipalities, by providing them annuities upon working a certain number of years.

In this context, in 1999, the government created the National Pension Funds of the Territorial Entities (FONPET is the Spanish acronym), which is under the supervision of the Ministry of Finance and Public Credit. The goal of this fund is to unify and concentrate the actuarial reserves of each of the territorial divisions under a single administration. FONPET is defined as “a fund without legal status administered by the Ministry of Finance and Public Credit, which aims to collect and allocate resources to the accounts of territorial entities and administer resources through autonomous assets” [25]. Currently, FONPET manages more than US$16 billion, and social security is a constitutional right in Colombia. Hence, the financial stability of the departments, municipalities, and country depends substantially on the responsible management of such funds.

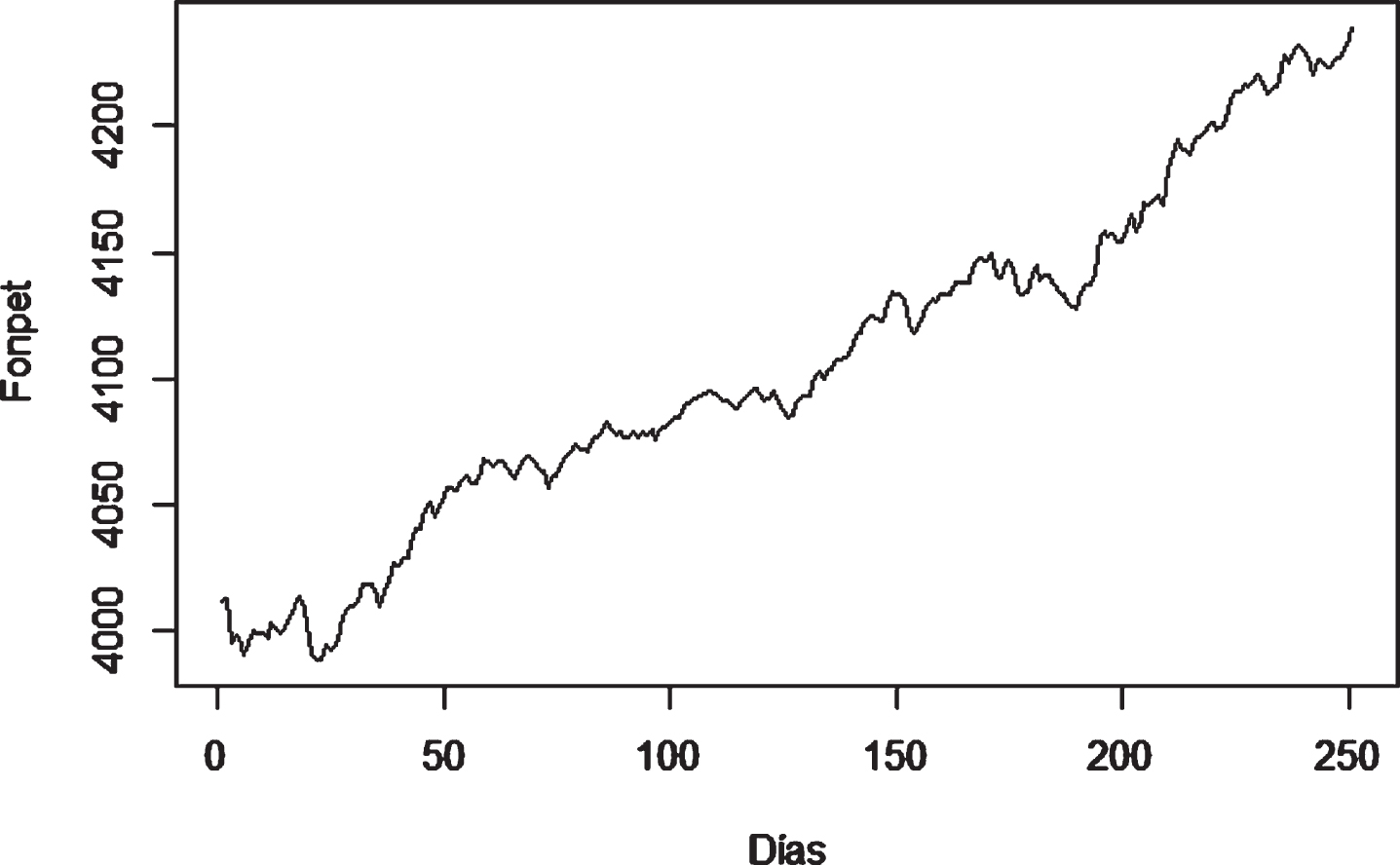

Figure 1 exhibits the evolution of the price per unit of FONPET from February 1, 2018, until January 31, 2019. The annual rate of return of the fund was 3.81% with an associated annual volatility of 1.19%. The stochastic differential equation that follows the price per unit is as follows:

Value of a unit of FONPET (2/1/2018–1/31/2019). Source: Authors’ elaboration with data from FONPET, R-Project.

In this section, this article considers a pension holder (62 years old) and a beneficiary (57 years old). The hypothetical pension holder earned during his working life 175,080,164.36 Colombian pesos. Using the actuarial calculation of the joint-and-survivor pension according to the methodology suggested by Bowers, Gerber, Hickman, Jones and Nesbitt [26], daily pension payments are equal to 26,666.67 Colombian pesos. The annual nominal interest rate used in the computation was 6%, and the mortality tables used to estimate the probabilities correspond to those published by the Financial Superintendency of Colombia [27].

In order to develop this application, it is assumed that the interest rate of the 10-year government bonds issued by the Ministry of Finance and Public Credit of the Republic of Colombia follows the Cox-Ingersoll-Ross stochastic process. Using the daily data for the same period used in FONPET, the Hessian method as suggested by Remillard [28], and the est.cir function of R-Project, the following equation is obtained:

Additionally, it is assumed that Cov (dU

t

, dW

t

) = -0.5dt. Therefore, the portfolio rate of return is given by the following:

Hence, the minimum annual rate of return (μ t ) the portfolio must have is 2.34%.

Sensitivity to changes in age

This article’s major finding concerns the portfolio minimum rate of return at which the actuarial reserve of a 62-year-old and a 57-year-old beneficiary is invested.

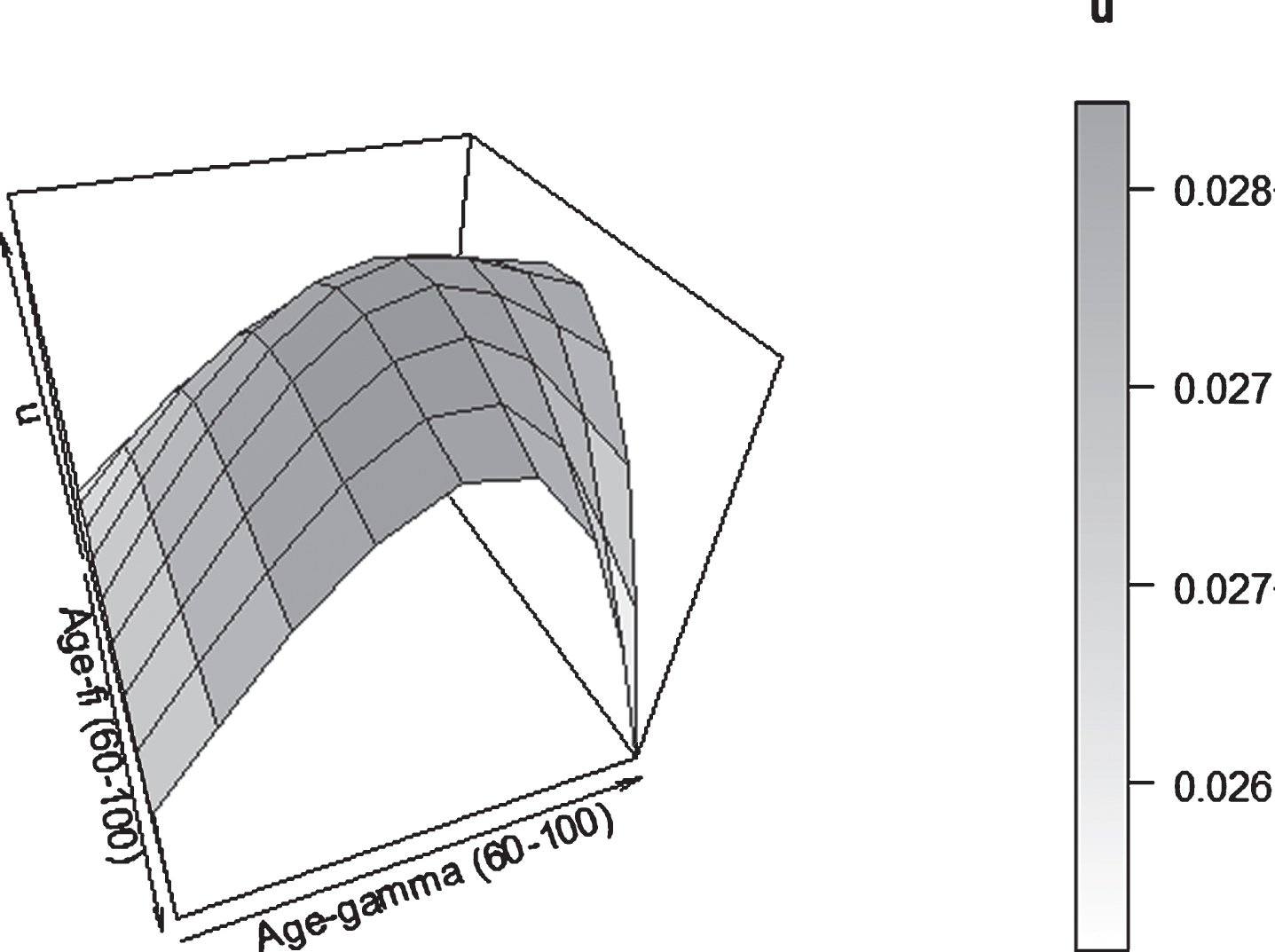

In this section, the response of such a rate of return to changes in the age of both the pension holder and the beneficiary is analyzed. In order to do this, the partial derivatives were simulated for individuals between 60 and 100 years old with beneficiaries of the opposite gender in the same age range.

As observed in Fig. 2, the combinations exhibit a certain stability in the portfolio’s minimum rate of return. The highest rate is observed when the pension holder and the beneficiary are 85 years old (μ t = 2.8281 %). In contrast, the lowest rate is achieved when both are 100 years old (μ t = 2.4995 %).

Minimum rate of return of the portfolio by age of the pension holder (ϕ) and the beneficiary (γ).

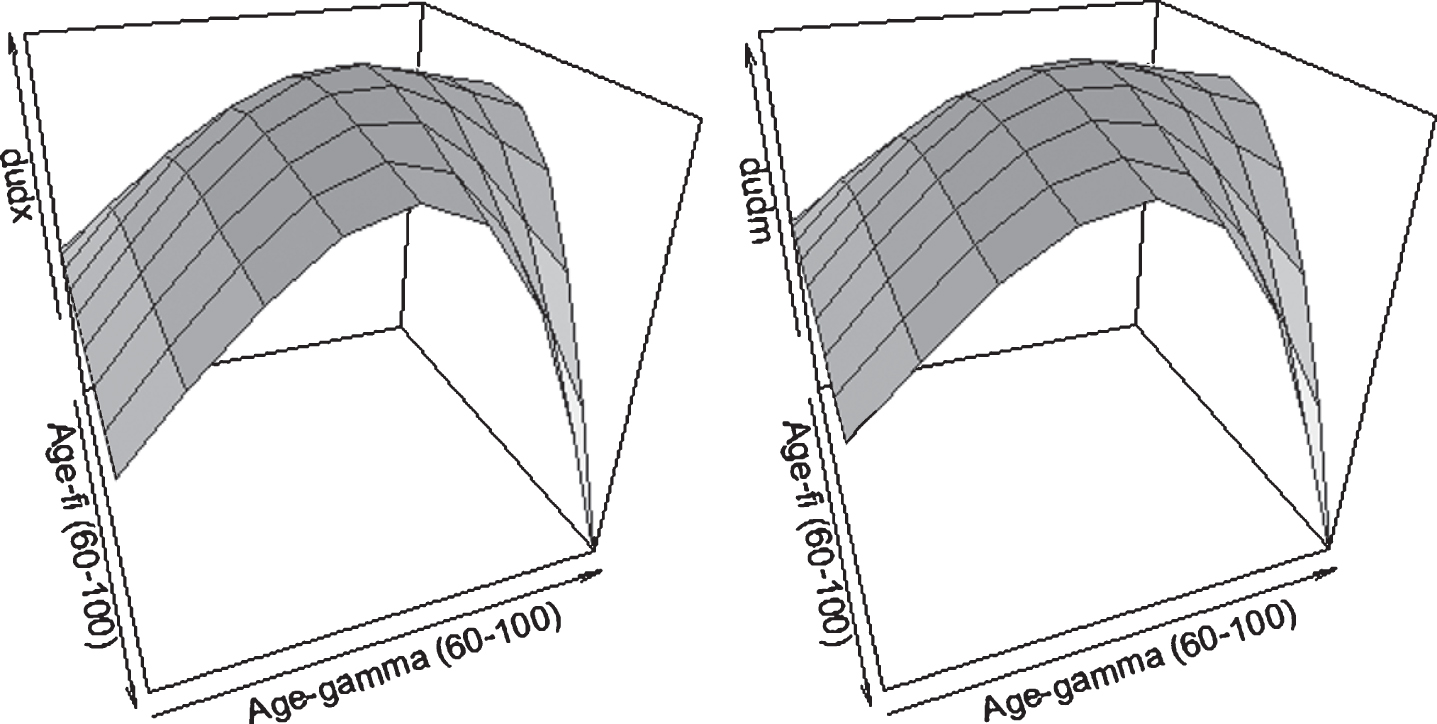

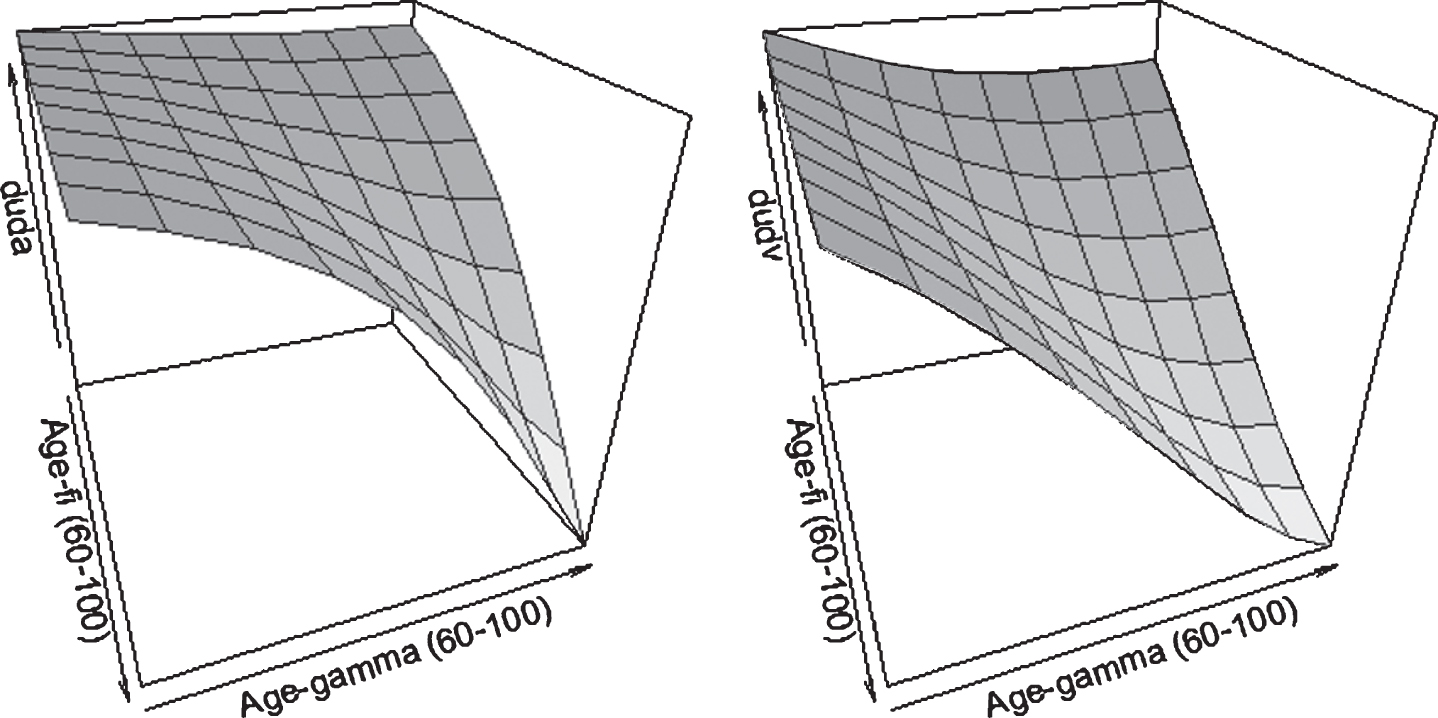

Similar behavior, although at different magnitude, is shown by the derivatives of μ t relative to the amount of the payments x and their trend m. Figure 3 shows the behavior of such derivatives in response to changes in the age of the pension holder and beneficiary.

Changes in the portfolio’s minimum rate of return in response to changes in the amount of the payment x t and in the parameter of the payment trend m, by ages of the pension holder (ϕ) and beneficiary (γ).

In both cases, the highest derivative corresponds to the ages of 80 for the pension holder and 85 for the beneficiary:

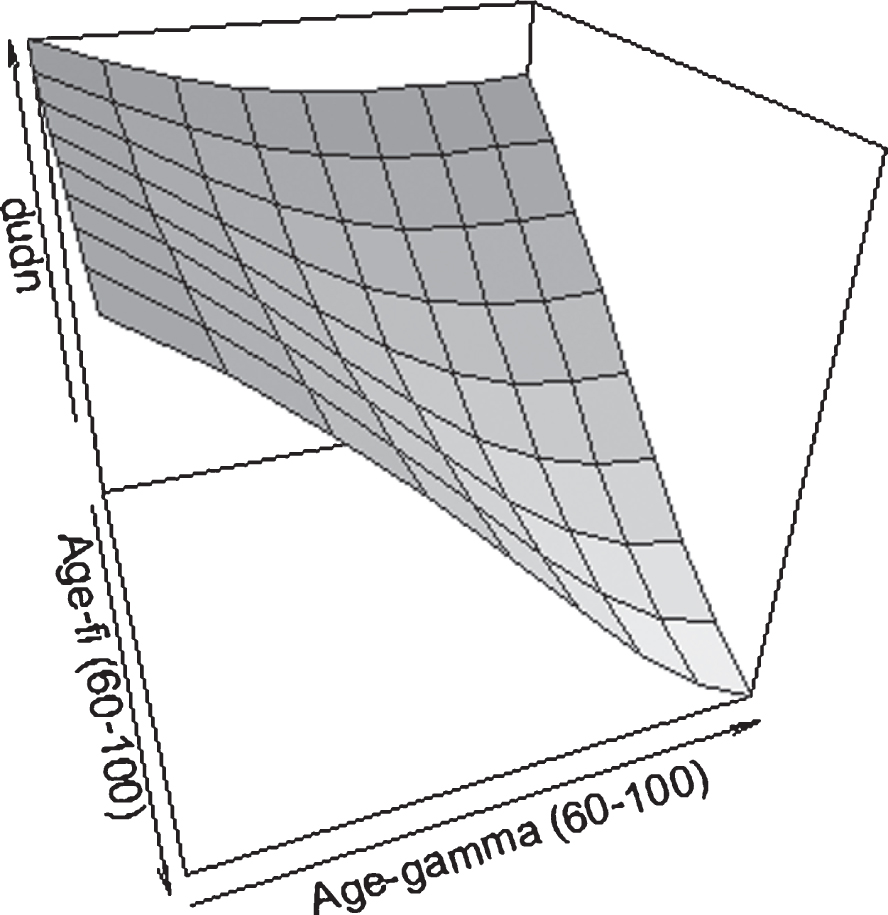

Regarding the impact of changes in the volatility of the payments, it is observed that as both the pension holder and the beneficiary get older, the impact on volatility decreases. The minimum change is 1, 255596 * 10-7, while the maximum change is 6, 806854 * 10-7, as exhibited in Fig. 4.

Changes in the portfolio’s minimum rate of return in response to changes in the parameter of payment volatility n, by ages of the pension holder (ϕ) and beneficiary (γ).

Moreover, as displayed in Fig. 5, changes in the parameters associated with the interest rates (a and ν) have less impact on the required rate of return as ages increase.

Changes in the portfolio’s minimum rate of return in response to changes in the parameter of the speed of reversion to the mean (a) and in the parameter of payment volatility (ν), by ages of the pension holder (ϕ) and beneficiary (γ).

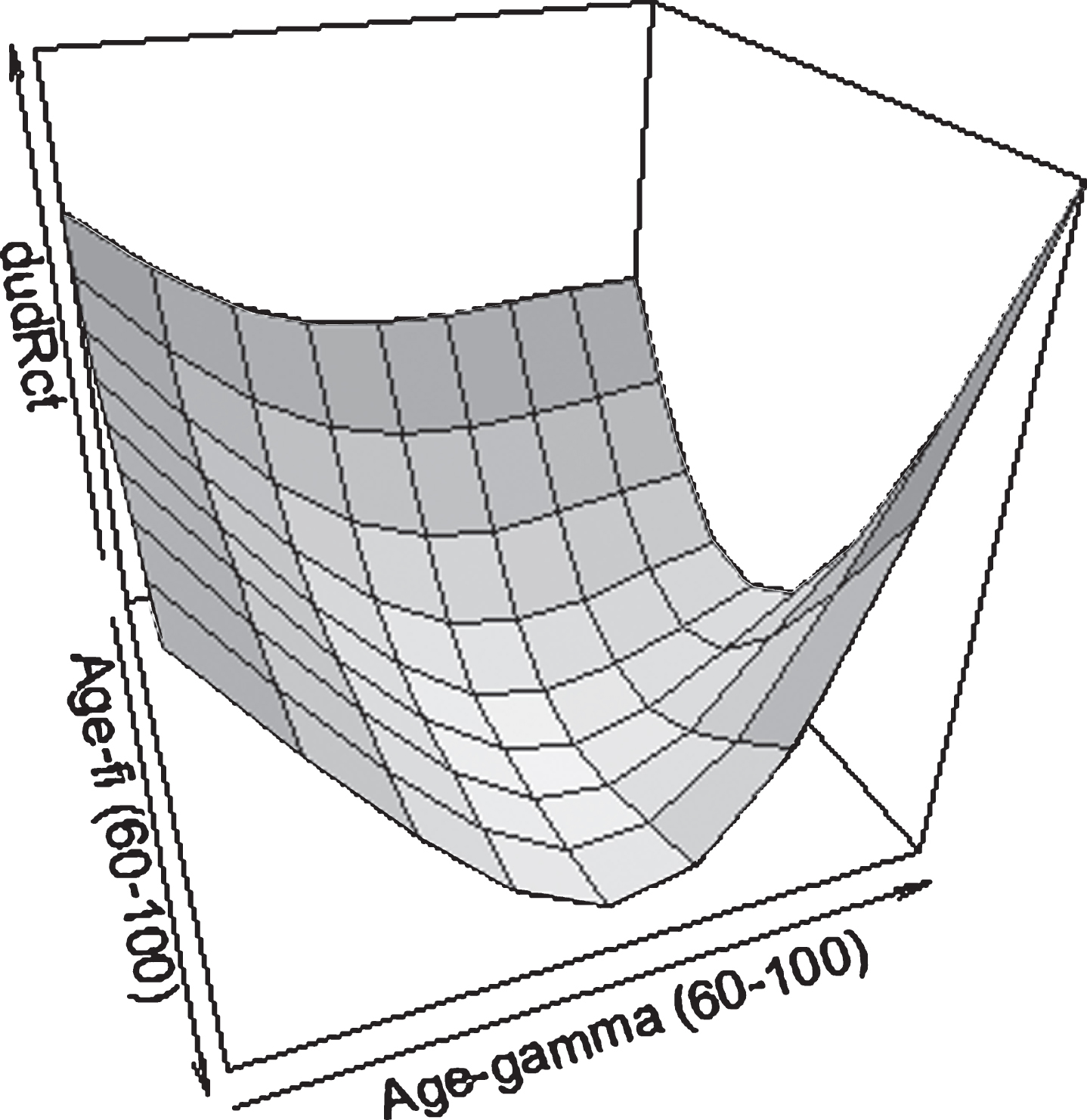

Finally, increases in the balance of the portfolio R Ct represent decreases in the minimum required rates of return, as expected. This effect is particularly pronounced when both the pension holder and the beneficiary are 85 years old, as displayed in Fig. 6.

Changes in the portfolio’s minimum rate of return in response to changes in the portfolio balance (R Ct ), by ages of the pension holder (ϕ) and beneficiary (γ).

This paper has developed a model that computed the technical interest rate, or the required yield, for a portfolio’s actuarial reserve for a joint-and-survivor annuity (or two-life annuity). The model considered the stochastic movement of the interest rate modeled by the Cox, Ingersoll and Ross [11] process and the Itô process for the derived payments. The findings have demonstrated that, through the stochastic calculations, the technical interest rate is a function of the rate of return the portfolio can yield (where both rates are not necessarily equal, despite what is suggested by the previous literature), the age of the annuity holder and beneficiary, the portfolio’s return volatility, and the parameters of tendency, volatility, and reversion to the mean of the market interest rate.

This is presented as an alternative approach to the traditional and unrealistic method that assumes that the constant discount rate is equal to the long-term portfolio’s expected rate of return. Given the inconvenience of assuming a constant interest rate [7], this article’s proposal presents an alternative for the calculation of the actuarial reserve. It is suggested that an analysis of the practical and legal consequences of computing the pension liabilities is an avenue for future research. Additionally, it is proposed that one should analyze the impact that the suggested estimation would have when combined with dynamic survivorship models, such as those proposed by Pitacco [29], in contrast with other proposals of estimation of the technical interest rates, such as the one of Olivares Aguayo, Agudelo Torres, Franco Arbeláez and Téllez Pérez [30].

With this understanding, this research outlines recommendations for policy makers to modify the regulation that includes the assumption of a technical interest rate equal to the minimum required rate or a function that depends solely on that rate. Similarly, practitioners must not assume the technical interest rate to be a target yield for their portfolio, but a variable that helps, together with other variables, to determine the required rate of return. In fact, each pair of buyers (the annuity holder and beneficiary) has a specific return for its actuarial reserve.

Footnotes

Acknowledgment

We appreciate the research support of Allison Kittleson, Harry David, and an anonymous referee and the valuable comments and suggestions of the participants at ICONIS 2019, Concepción, Chile.