Abstract

The financial supply chain is affected by many factors, so an artificial intelligence model is needed to identify supply chain risk factors. This article combines the actual situation of the financial supply chain, improves the traditional machine learning algorithm, and takes the actual company as an example to build a corresponding risk factor recognition model. From the perspective of optimizing the supply chain financial model, this paper combines the functions of the Internet of Things technology and the characteristics of the supply chain financial inventory pledge financing model to design a new type of inventory pledge financing model. The new model makes up for the defects of the original model through the functions of intelligent identification, visual tracking and cloud computing big data processing of the Internet of Things technology. In addition, this study verifies the performance of the system, uses a large amount of data in Internet finance as an object, and obtains the corresponding results through mathematical statistical analysis. The research results show that the model proposed in this paper has a certain effect on the identification and analysis of financial supply chain risk factors.

Introduction

With the continuous upgrading of my country’s industrial development, competition between enterprises has changed from competition between single enterprises to competition between the entire industry chain. More and more core enterprises rely on their resources to integrate their upstream and downstream industries, reduce production costs, financing costs, and improve production efficiency. The entire industry chain is inseparable from the support of supply chain finance. It can be said that in the entire industrial chain, whether the effective use of supply chain finance determines the competitiveness of the industrial chain to a certain extent. The traditional supply chain finance led by bank financial institutions has created three basic models for supply chain financing. According to different types of collateral, it can be divided into prepayment mode, movable property mortgage mode and account receivable mode. With the penetration of Internet technology into the financial industry, the sales channels of financial products have been broadened and the services have been personalized and standardized. The investment threshold has been lowered, some financial services are no longer patents for banking financial institutions, and general financial institutions have access opportunities. Moreover, information sharing can be effectively realized, which breaks the information closed situation of enterprises, and big data cloud computing can be used. For the supply chain finance that belongs to the financial industry, the Internet also brings a greatly improved risk control level and the convenience of capital docking. Industrial development will definitely bring about model updates [1].

According to the traditional model, the Internet supply chain finance has undergone a model change, and different industry participants have begun to redefine their own supply chain finance model definitions in subdivided fields. However, high income in the industry must be accompanied by high risks. Although the Internet makes risk control more convenient and effective, these conveniences also bring new legal compliance, risk control and evaluation challenges. How to conduct reliable data screening and analysis based on massive big data, how to reduce the occurrence of false information and network running events, how to establish an effective evaluation model for different companies, and how to operate better among many competitors cannot be ignored. The core issue is the risk assessment of Internet supply chain finance. At present, domestic scholars have not formed a systematic and perfect system on this issue [2]. Internet-based supply chain finance has made financial innovations to the original traditional supply chain finance model. Its main role is to make the financial market environment more perfect, promote the industry to move forward, and solve the problem of difficulty in obtaining loans during the operation of small and medium-sized enterprises in the supply chain. Under the new environment, “Internet + Supply Chain Finance “ is the “new normal “ of the supply chain finance industry and a sustainable development model of the Internet lending industry. Under the traditional model, due to the strict control of corporate credit by bank financial institutions, most SMEs have difficulty obtaining financing from bank financial institutions. The Internet has brought opportunities. With the support of policies, ordinary financial institutions and traditional core enterprises have been able to start supply chain financial business with the help of big data and platform resources and expand and extend their business scope. Moreover, they can more effectively assess the risks of financing enterprises from multiple aspects, so as to share the large profit space in the industry with banking financial institutions. To some extent, their advantage of using resources and flexibility may even make them go further than the traditional banking industry in the future supply chain financing industry [3].

Of course, banking financial institutions will not easily give up this cake, they are also connected with the Internet in the new era to realize the service platform, and spawn online supply chain finance. At the same time, the business of banking financial institutions is constantly carrying out internal resource integration, staff training, system upgrades, and the establishment of Internet finance related departments. However, no matter how innovative each financial institution or platform is, it will eventually continue to benefit from advantageous customers, and it will gradually expand its business scope to small and medium-sized enterprises and stabilize its supply chain finance industry position.

Related works

Currently, there is no standard definition of supply chain finance. Due to the different development backgrounds at home and abroad, people’s understanding of supply chain finance also has certain differences. In foreign countries, scholars are more inclined to regard it as a financing solution based on electronic technology, through which it can realize the promotion and verification of data information flows such as orders and invoices and provide financing for supply chain members. However, Chinese scholars believe that it is a “1 + N “ model customized by financial institutions in the supply chain for supply chain participants, aiming to help them get rid of financing difficulties. Supply chain finance is very different from traditional finance, and its business is mainly based on the financing needs of the participants in the supply chain. On the one hand, due to the lack of fixed assets for mortgages and the imperfect financial system, it is difficult for participants in the supply chain to obtain financing from financial institutions through traditional channels, and the amount of financing is also huge. On the other hand, the traditional financial market is fiercely competitive, and relevant institutions have made meager profits. Compared with other financial businesses, China’s supply chain financial business prefers the credit of participating entities, as well as the risk prevention methods and technologies of their financing or credit ownership [4].

In terms of credit risk theory research, the literature [5] believed that t while recognizing the success of expert systems and neural networks in mortgage and credit card fraud detection, it is also necessary to recognize that artificial intelligence and neural networks have not yet achieved substantial breakthroughs in evaluating customer credit applications. The literature [6] used new technologies such as multilayer perceptrons and modular neural networks, as well as traditional techniques such as linear discriminant analysis and logistic regression, to investigate the performance of general models and compare them with custom models. The literature [7] divided credit risk assessment into two categories and assisted the credit decision-making process through these two models. The first decision that creditors must face is to grant credit to new applicants (credit score), and the second is how to adjust credit restrictions or marketing efforts (behavior score) for current customers. The literature [8] confirmed that experiments conducted in Bolivia and Colombia have shown that the implementation of credit scoring has improved the judgment of credit risk, thereby avoiding a lot of losses every year. The literature [9] regarded credit risk prediction as a machine learning (ME) problem. In terms of the construction of credit risk assessment system, the literature [10] designed a neural network consumer credit scoring system for financial institutions. Moreover, the literature used extensive accounting data for each financial institution’s customer transactions and account balances. The literature [12] constructed a consumer loan default prediction system by studying the unsecured consumer customers of a financial institution and used the borrower’s demographic variables and currency attitudes as discriminant information. The literature [13] used a credit evaluation system based on back-propagation supervision, and used the German bank credit data set as a discrimination case. The literature [14] used the behavior score data set provided by ExperianUK and revolving credit suppliers as an evaluation system to establish a basic case. The literature [15] used an inductive learning method for data indexing, used the nearest neighbor matching algorithm to retrieve similar content, provided better user interpretation capabilities, and conducted research on the credit score of the microfinance industry. The article constructed multiple non-parametric credit scoring models based on the multilayer perceptron method (MLP). The results show that the MLP model is superior to other classical techniques in terms of area under receiver and operating characteristic curve (AUC) and misclassification cost.

For support vector machine technology, researchers have done a lot of work. The literature [16] proposed FSVM, which considers each sample to be classified as bad. FSVM allows FS and M to provide higher generalization capabilities without losing the advantage of being insensitive to outliers. Moreover, on this basis, the literature introduced a relatively new machine learning technology, namely support vector machine (SVM), and attempted to provide a model with better explanatory power through SVM. The literature [17] believed that the biggest advantage of support vector machines is that it does not appear to be overfitting problems in neural network systems, so it can solve more complex problems, and it can also be applied to more fields and is well promoted. The purpose of combining the concept of fuzzy sets is to increase the generalization ability and insensitivity to outliers, and at the same time use the least square method to reduce the computational complexity. At present, the research on genetic algorithms is very mature. Literature [18] has also tried genetic algorithms in the field of credit scoring, investigating that the total data owned by banks can be used as predictive borrower credit data.Moreover, the literature found that hybrid systems with genetic algorithms are competitive, can be used as feature selection techniques, and found the most important features for determining default risk. In order to benefit from the reduction of potential risks in the credit industry, literature [19] developed a hybrid credit scoring model (HCsM), which handles the credit scoring problem by fusing the advantages of genetic coding technology and support vector machine technology. The literature [20] used data mining technology to construct a credit scoring model and obtained results. The results show that neural networks are the most accurate in bank credit prediction, followed by linear discriminant analysis, logistic regression, and decision trees.

Credit risk transmission model of inventory pledge financing

The model studies the problem that the retailer encounters insufficient funds and thus generates financing needs, in a transaction process between supplier B and retailer A. Commercial banks allocate a certain amount of loans to logistics enterprises, and logistics enterprises carry out inventory pledge financing business. The SME A retailer applying for financing uses the company’s funds to purchase goods, and the model company constructed in this paper is called the Q group. Moreover, the purchased goods are used as collateral to apply for loans to the financing organization Q Group, and the goods need to be handed over to the logistics company Q Group for subsequent management. Q Group is responsible for the acceptance and value evaluation of the pledged inventory, and provides the evaluation report to the bank, and supervises the inventory after the bank agrees. After a commercial bank has conducted a risk assessment of SMEs and the core enterprise B supplier that provides guarantees to SMEs, logistics company Q Group provides loan services to SMEs based on the inventory assessment report and an understanding of the operation status of the entire supply chain. Moreover, it makes relevant decisions on the basis of improving company performance and obtaining more profits. After obtaining financial support, SMEs purchase products again, sell the purchased products as soon as possible, and repay the loans. SMEs send the goods to a closed and exclusive account, and logistics supervision enterprises release the goods in proportion. If SMEs cannot repay within the agreed time, Q Group may require core companies to repurchase collateral to ensure the return of funds. The market demand for this product is subject to the typical newsboy model, that is, the market demand is random during the inventory pledge financing, and the retail price of the product remains unchanged.

Based on the above analysis, a two-layer Stackelberg game model is constructed. In the first stage, the logistics company Q Group plays a game with the SME A retailer. In the second stage, in the secondary supply chain, the core enterprise B supplier plays a game with the A retailer. The decision made by each participant of inventory pledge financing under the premise of profit maximization is analyzed, and the model is applied to analyze the relationship between the pledge rate and inventory quantity established by Q Group and its impact on the profit of each participant.

The basic assumptions are as follows: The information among SME A, core enterprise B, bank Z, and logistics enterprise Q group is shared, and the information is symmetrical. Product demand is uncertain and sensitive to market changes. The retail price is fixed within the single-period inventory pledge financing period. The supplier signs a sales contract with the retailer to repurchase the product when the market demand is less than the retailer’s initial order quantity. The density function F(x) is subject to IFR (decreasing failure rate).

p is the sales price of the product during the inventory pledge period, c is the purchase price of the product purchased by the retailer A from the supplier B, c0 is the repurchase price of supplier B’s repurchased product at the end of the inventory pledge financing period, c1 is the cost price of the product produced by supplier B, and c2 is the processing price of the product. Moreover, ξ (0 < ξ < 1) is the market demand for products, which subject to the distribution function F (X) = p{ ξ < X }, f (X) = F′ (X) is the density function, and I represents the income paid by the Q group to the bank.

In the process of carrying out inventory pledge financing business, the occurrence of credit risk may be related not only to the profit of the borrowing company, but also to the value of the pledge and the credit performance of the financing company. Logistics companies should make financing decisions and formulate pledge rates based on product sales, retailer credit status, and supplier repurchase behavior. Next, through the establishment of the Stackelberg game model, discuss the factors that logistics companies need to consider when determining the pledge rate, as the core company’s suppliers to determine the wholesale price, and retailers to determine the order quantity [21].

(1) Risk Analysis

Before playing a game against the various parties involved in inventory pledge financing, we need to first analyze the profit of retailer B, the main source of risk. Moreover, profit is the main source of retailer B’s repayment. According to the assumption that within the single-period inventory pledge business cycle, the products sold by retailer B will not change, and demand will become the biggest factor affecting risk.

Proposition 1: When

Certification: When ξ = 0, the pledge rate set by the J logistics enterprise is

If c0q0 ⩾ cq (1 + α), that is

Therefore, there is no credit risk for retailer B. At this time, the profit of retailer B is:

Proposition 2: When

Certification: When

When 0 ⩽ ξ < q0 + q, the retailer’s profit when repaying is:

The retailer’s profit when not paying is:

When the repayment profit is greater than the non-repayment profit, the retailer will choose to repay, and it can be concluded that:

We set:

Three situations can be introduced:

When ξ0 ⩽ ξ < q0 + q, the retailer will not incur credit risk, and the retailer’s profit is shown in formula (2).

When 0 ⩽ ξ < ξ0, the probability of the retailer defaulting is very high and there is credit risk. The retailer’s profit is as shown in formula (3).

When ξ ⩾ q0 + q, the retailer will not default, at this time the retailer’s profit is:

In summary, the expected profit of retailer A in the single-period inventory pledge financing business is:

The profit of Q Group is divided into two cases: whether the loaned SME repays the loan on time. From the analysis of the retailer’s profit, it can be seen that the factor that induces credit risk is mainly the market’s demand for the inventory sold by the retailer. Based on this, the profit of Q Group’s single-period inventory pledge financing business is analyzed [23].

When ξ < ξ0, the retailer has credit risk and there is a possibility of non-payment, while when ξ > ξ0, the retailer will repay on time. For these two situations, the profits of logistics companies are:

Therefore, the expected profit of logistics enterprises is:

When the supplier’s repurchase behavior is used to portray the supplier as the core company’s guarantee to the retailer in the inventory pledge financing business, the supplier’s profit is:

The Stackelberg game model is divided into two stages. The first stage is the game between Q Group as a loan provider and A retailer in the supply chain seeking financing assistance, and Q Group is the leader. The second stage is the game between the retailer A and the core company B supplier in the supply chain, and the core company is the leader.

Proposition 3: In the first stage of the game, under the premise of maximizing their respective profits, Q Group determines the pledge rate for providing loans to Retailer A, and then Retailer A determines the amount of inventory and Q Group makes the best decision. The best decision of the retailer A is as follows:

Certification: Through formula (10), the first-order partial derivatives and second-order partial derivatives of q are obtained:

It can be known from f (ξ0) > 0,

From

Among them:

is certified.

Proposition 4: In the second stage of the game, supplier B makes the best order price, and retailer A makes the decision to select the optimal reorder quantity. When analyzing the game in the supply chain, the reverse induction solution is used. The optimal order quantity of the retailer A is calculated first, and then the optimal order price of the supplier B is calculated. The results are as follows:

Best order price:

The optimal order quantity is q*, and q* satisfies:

Certification: When

The profit of retailer A at

It can be seen from the assumption that the product demand is subject to the newsboy model during the inventory pledge period, and the product price remains unchanged.

Therefore, p > c0,

It satisfies:

The supplier’s order price at this time is:

After substituting this formula into supplier B’s expected profit formula (10), the following result is obtained:

The first derivative is solved:

Because the demand distribution function F (ξ) satisfies the monotonous decrease of IFR, by setting

In summary, the optimal re-order price of the supplier of core enterprise B is:

Through numerical simulation, the linear relationship between the initial inventory and the pledge rate is analyzed. On the basis of field research, the following assumptions are made in conjunction with the actual transaction price. The pledge rate is a major indicator of the financing group, and the amount of initial inventory determines whether the loan can be obtained.

The market demand faced by retailers follows an exponential distribution with an expectation of 10.

Figure 1 shows that when retailer A’s initial inventory exceeds 0.492, inventory pledge financing business will not occur, and when it is less than 0.318, retailer A cannot obtain sufficient loan amount. Between 0.318 and 0.492, whether retailer A can obtain sufficient loans is determined by the pledge rate set by logistics company Q Group.

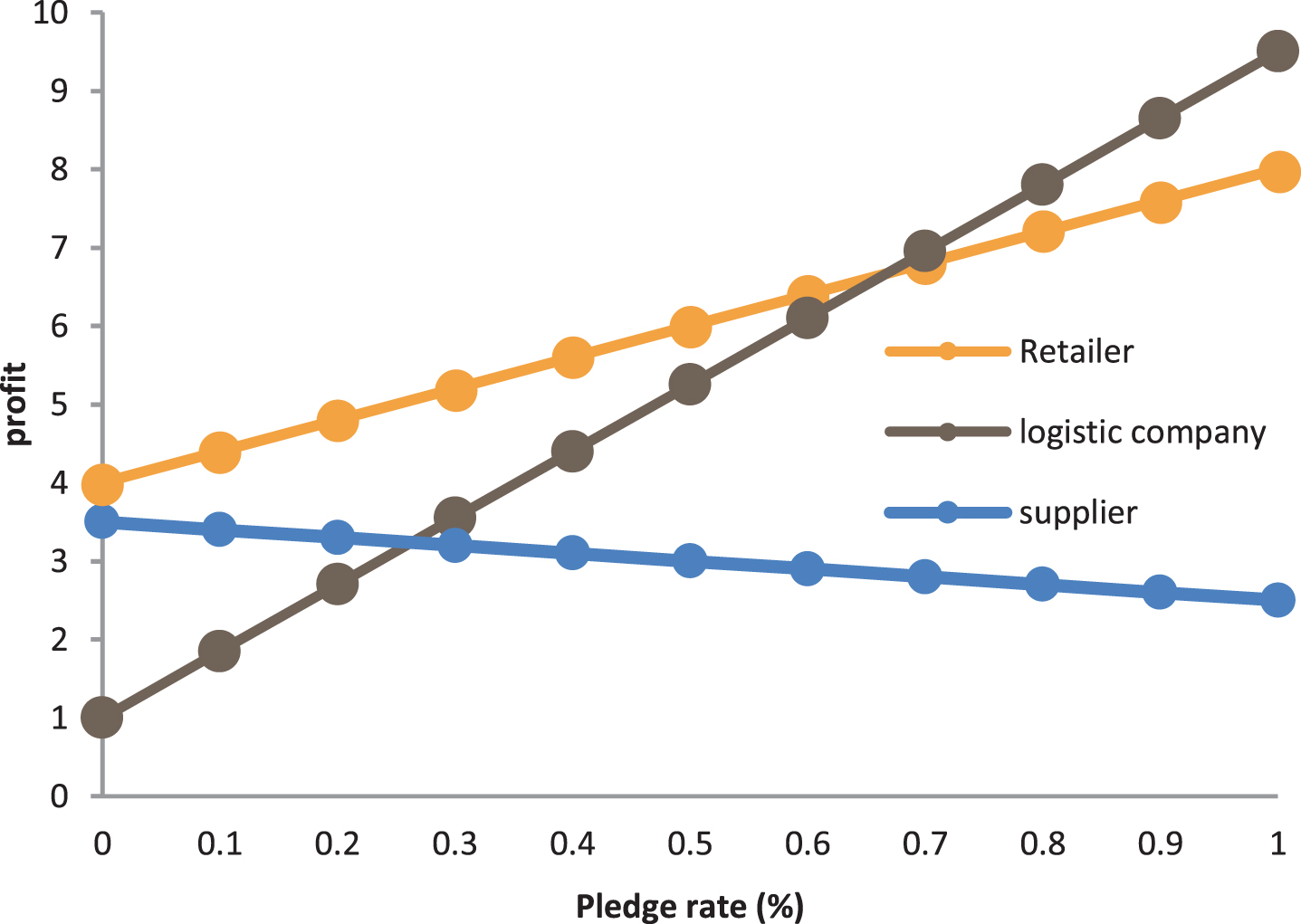

Relationship diagram between pledge rate ω and m q0.

It can be seen from Fig. 2 that the profits of supplier B and retailer A increase with the increase of the pledge rate, and at the same time, the profits of logistics companies show a downward trend. For the logistics company Q Group, a lower pledge rate will result in higher profits, but financing companies may not accept it, because the lower pledge rate does not reflect the value of the pledge. When the pledge rate is 0, the profit of the logistics enterprise reaches the highest, but no financing business will occur at this time. When the pledge rate reaches 1, retailers and suppliers have the highest profits. The model proves that when the pledge rate is greater than 0.544, the logistics enterprise will face the default risk that the financing enterprise will not repay, and the income obtained by the logistics enterprise does not match the risk. When the pledge rate is greater than 0.652, the profit of the retailer will exceed that of the supplier. Therefore, after the Q group has established the pledge rate, the retailer and the supplier can make a reasonable profit distribution to achieve the purpose of supply chain coordination.

The effect of the pledge rate on the profit of participants in inventory pledge financing.

From the analysis of the above models and examples, it can be seen that the credit risk of inventory pledge financing originates from the retailer’s market demand. When the market demand is less than the quantity of inventory, retailer A has no credit risk of default. When the market demand is greater than the inventory, the degree of credit risk of retailer A is also different due to the difference in the amount of reordering. At this time, the credit risk of retailer A is passed to supplier B through reordering. The supply chain supplier signs an agreement with the repurchase as a guarantee, and logistics company Q Group as the financing institution provides financing service to retailer A. Supplier B mitigates some of the risks brought by retailer A by setting reasonable reorder prices. Credit risk is transmitted through the secondary supply chain of supplier B and retailer A. After determining the reorder quantity, logistics company Q Group provides financing services. At this time, the credit risk is transmitted to the logistics company, and the logistics company Q Group eases its own credit risk through the formulation of the pledge rate.

The Internet of Things is a network technology that implements intelligent identification, tracking and supervision by comprehensively using various sensing technologies to connect items to the Internet for information exchange and communication under the agreed protocol. The working principle of the Internet of Things is shown in Fig. 3:

The working principle of the Internet of Things.

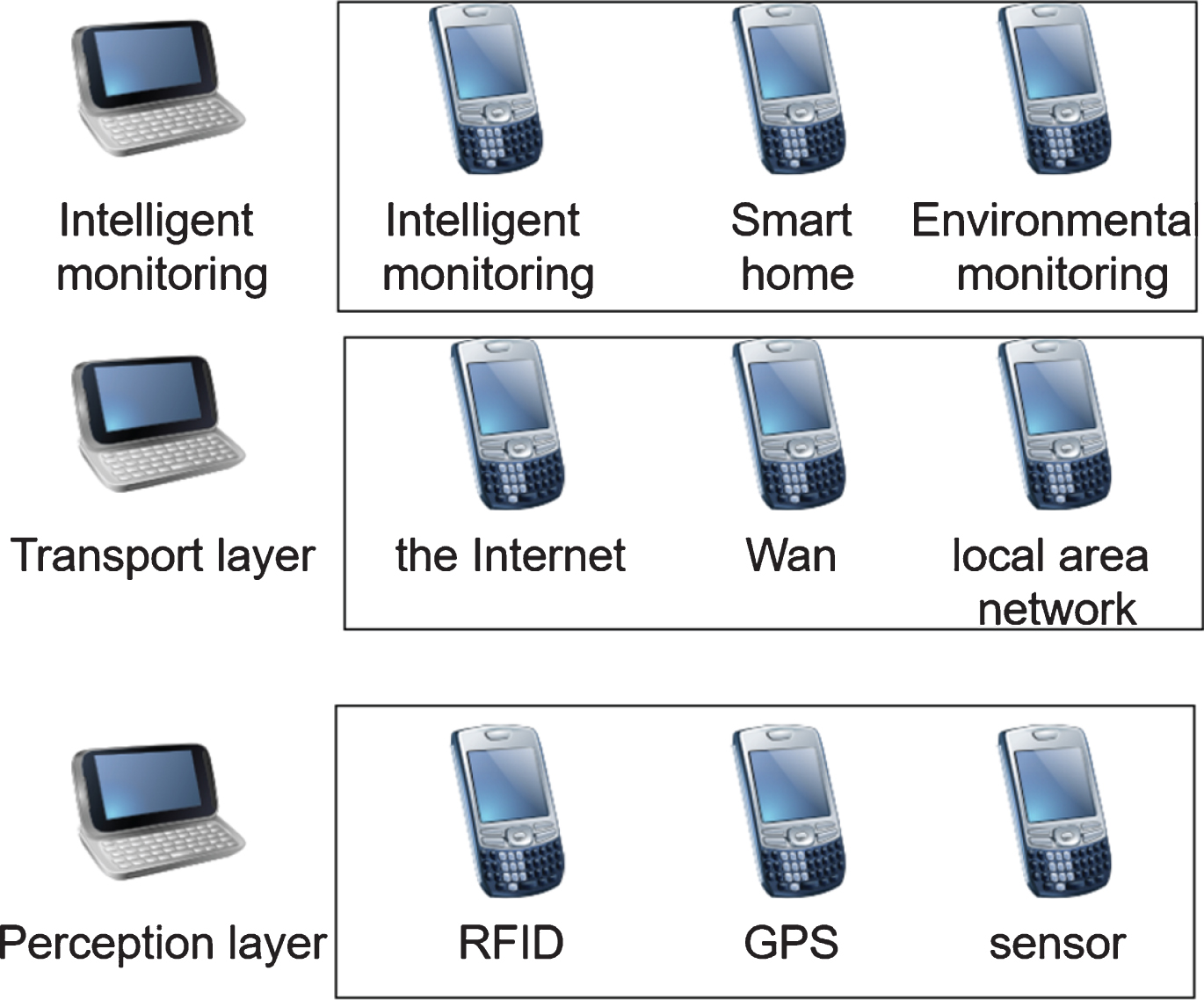

The Internet of Things consists of a three-tier architecture, as shown in Fig. 4. The first level is the perception layer, which mainly realizes the identification and tracking of objects through RFID, GPS, camera and other sensing technologies, and reads the relevant information of the objects in real time. The second layer is the network transport layer. Through the use of electronic product codes EPC, WAN, Internet, and communication networks, it transfers the information and data acquired by the perception layer to users with links to achieve information interaction and sharing between each other. The third layer is the application layer, which implements intelligent processing and application of the acquired data and related information on the basis of the first two levels. The IoT technology can be applied in a wide range of neighborhoods in practice, such as environmental monitoring, smart grid, smart monitoring, and so on.

IoT architecture diagram.

In the inventory pledge financing model based on the Internet of Things technology, the visual real-time tracking of pledges has improved the supervision and operation capabilities of logistics enterprises. Real-time and accurate warehousing information is effectively transmitted among the participating entities, which increases the transparency of financing business development, and real-time data sharing enhances the bank’s regulatory capabilities and reduces capital risks. The “four streams in one” in the new model is shown in Fig. 5:

“Four streams in one” under the new model.

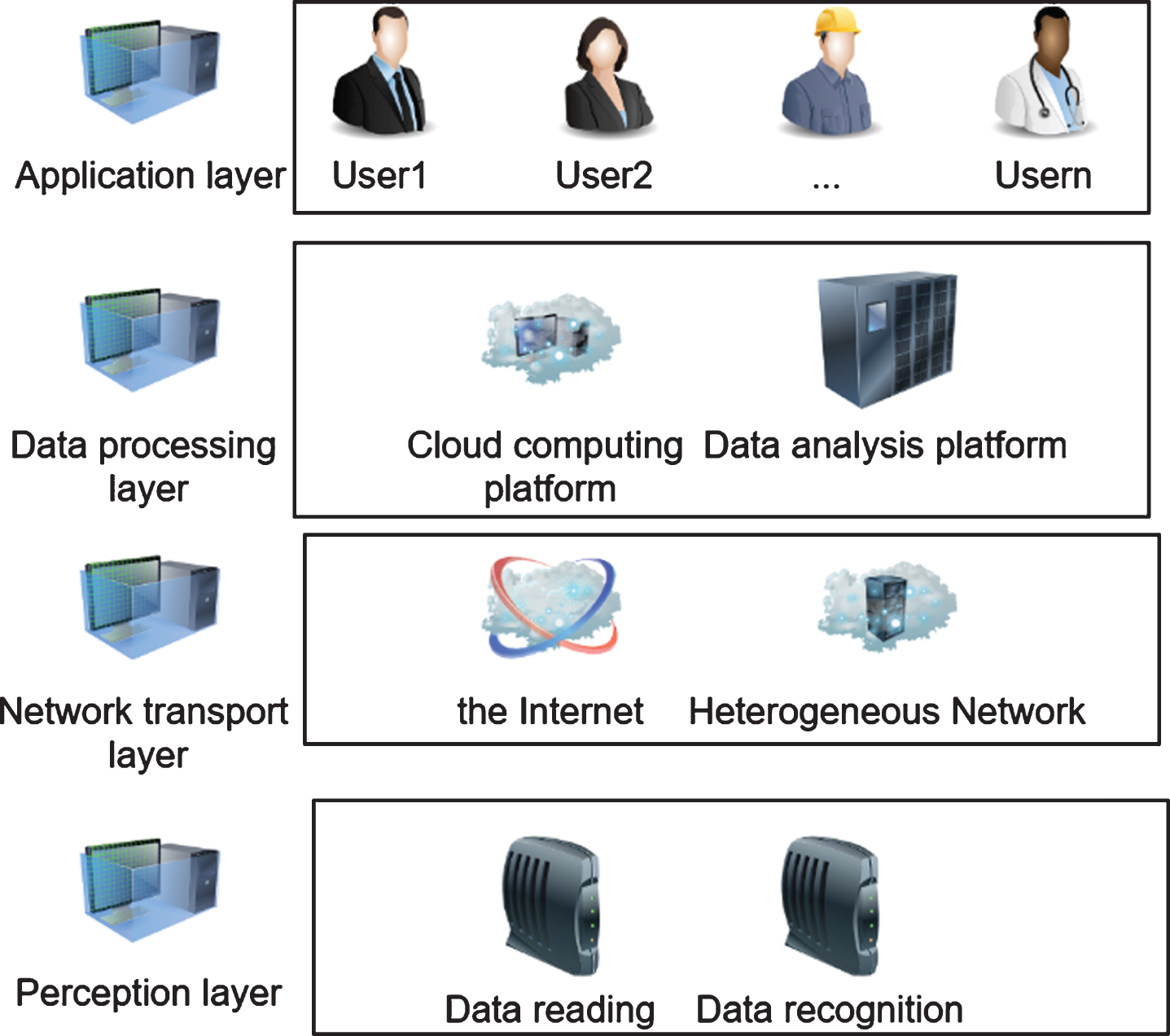

The starting point of this paper is to optimize the existing financing model of supply chain finance with the help of the application of Internet of Things technology. The inventory pledge financing model based on the Internet of Things technology hopes to prevent the occurrence of fraud through real-time monitoring of the pledge, and conduct mark-to-market management through the data processing capabilities of the Internet of Things cloud computing platform to avoid the risk of pledge price fluctuations caused by similar competition in the market. Finally, the information on the development of the entire business is transparent among the participants in the supply chain finance. Therefore, based on the working principle of the Internet of Things and the characteristics of the inventory pledge financing business, an IoT system architecture based on the inventory pledge financing business is designed. The architecture includes four layers: perception layer, network transmission layer, data processing layer and application layer, as shown in Fig. 6:

IoT system architecture based on inventory pledge financing model.

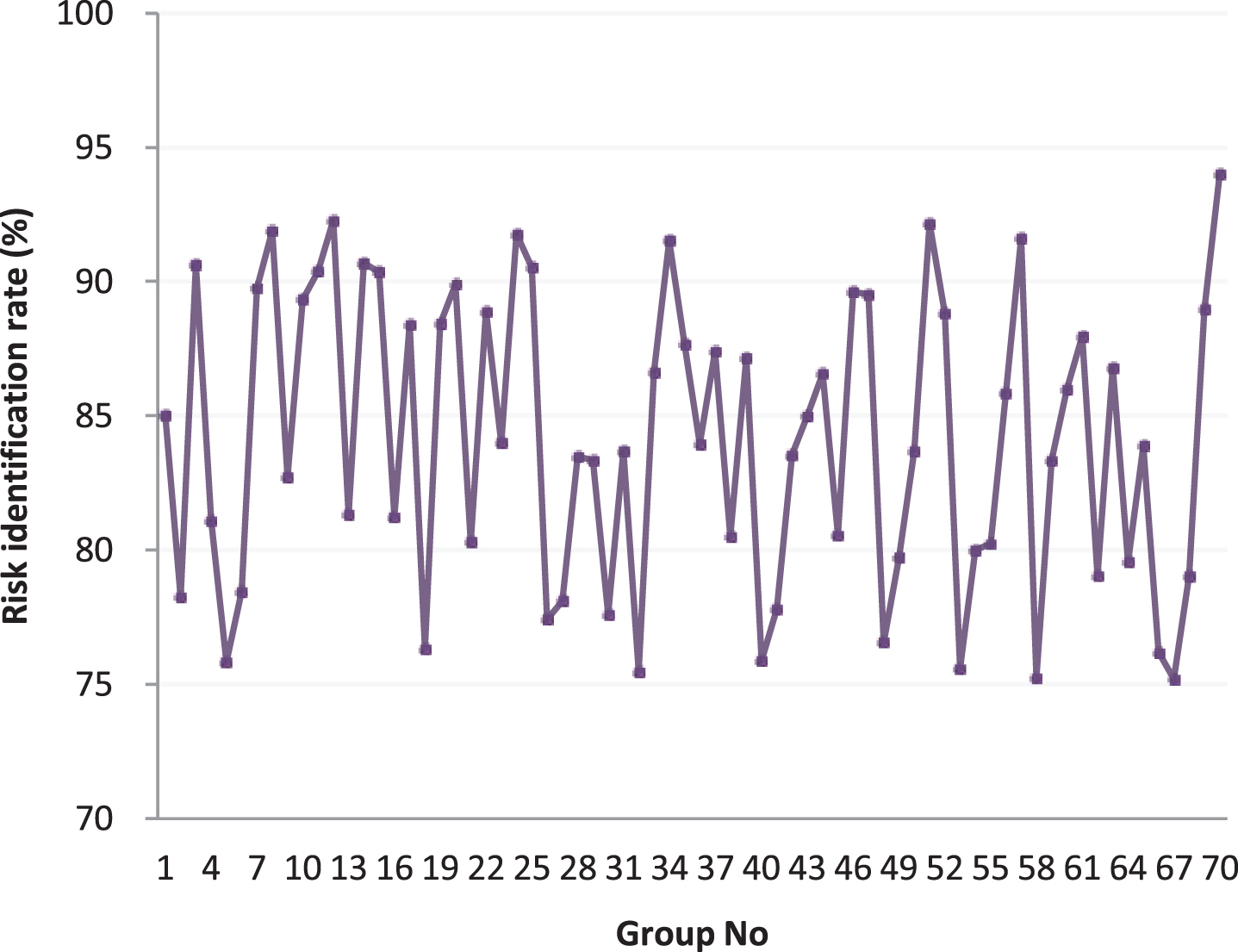

Based on the construction of the above model, the system performance is verified, and a large amount of data in Internet finance is used as verification. The data obtained is data that has been used in the past, so the risk factors have been exposed. Based on this analysis of risk factors, the results can be directly compared with the existing actual situation. There are 70 sets of data in this article, and the risk identification rate is shown in Table 1 and Fig. 7.

Statistical table of risk rate identification rate of financial supply chain

Statistical diagram of risk rate identification rate of financial supply chain.

From the above chart, we can see that the recognition rate of the risk factor analysis model of financial supply chain constructed in this paper is above 75%, and the highest recognition rate can reach 95%, and the recognition rate is high. Next, we examine the system’s ability to identify risk factors in the financial supply chain. In this paper, the risk factors of the financial supply chain are mixed with some non-risk factors, and the risk recognition is carried out through the model. The correct recognition is recorded as 1, and the error is recorded as 2. The obtained results are shown in Table 2 and Fig. 8.

Statistical table of risk identification results

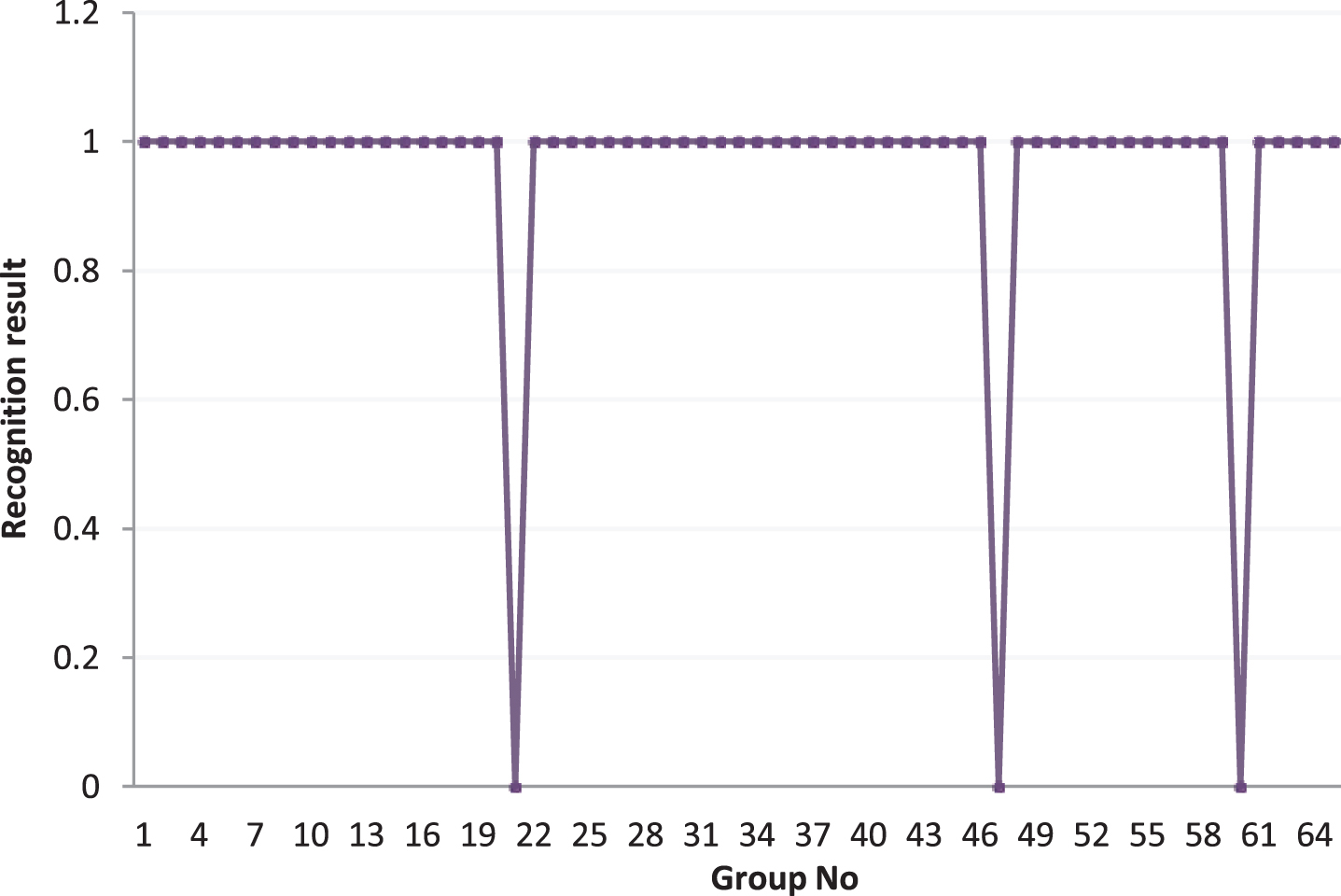

Statistical diagram of risk identification results.

As shown in Fig. 8, among the 79 sets of data set, only three sets of risks have not been identified. It can be seen that the model constructed in this paper has a good effect on the identification of financial supply chain risk factors.

The credit risk of supply chain finance is a typical non-systemic risk, which is also the primary risk faced by supply chain finance. The risk factors are mainly macro-environmental factors, supply chain characteristic factors, financing enterprise qualification factors, core enterprise qualification factors and credit support asset characteristic factors. Guided by supply chain finance theory and financial risk transmission theory, this paper combines machine learning algorithms to construct a financial supply chain risk factor recognition model and takes a company as an example to analyze the model performance. Moreover, this study combines with the Internet of Things to build an IoT structure model based on and learning, and then establishes a comprehensive evaluation model of the risk factors of the supply chain financial credit risk. In addition, this study combines the actual cases of the bank for application analysis and uses qualitative and quantitative analysis to study the performance of the model constructed in this article. The results show that the performance of the model constructed in this paper is relatively good.