Abstract

With the development of technology and artificial intelligence(AI), financial leasing is used frequently in China’s equipment manufacturing industries, especially after 2008, which attracts our attention. This paper focuses on the problem. A theoretical model is provided in the paper to explain the motivation that why financial leasing is used in equipment manufacturing industries. In this paper, we employ multi-level fuzzy linear regression model to analyze data of manufacturing equipment industry of China in order to discover impact between sales revenue and financial leasing. We also discover credit sale forecasting using this model. We discover that economic leasing has a constructive important effect on sales revenue in total samples, which is consistent with the theoretical framework. However, the results are different in sub-industries, which shows that economic leasing has a constructive and important effect on sales profits in some sub-industries, but some of them are not. Furthermore, we also find that asset characteristics has a substantial effect on financial leasing decision. The outcome demonstrates that the more precise the asset, the easier it can be leased.

Keywords

Introduction

In current literatures, credit sales play an important role on enterprises [1]. Generally speaking, there are three aspects on the study. The first is from demand side [2], the second is from supply side [3–6] and the last is from both sides [7–9].

Some papers provide theoretical model of a supplier’s expected demand for its input [10], explaining that why most manufacturers offer credit sales. The scholars [11] studied that the sales effort of manufacturers gives them informational advantages in assessing their customers’ credit risk [12, 13]. Credit sales can change demand and reduce the production fluctuations [14, 15].

As a way of credit sales, financial leasing has broadened the sales channels of manufacturers [15]. In China, as the AI develops, especially after the 2008 financial crisis, more and more listed companies have set up financial leasing companies. Most listed companies with leasing business are not financial companies but listed companies in the equipment manufacturing industry. For the companies, technology is used to provide more marketing methods to improve service efficiency. However, leasing decisions are different from sub-industry to sub-industry [16–18]. A question needs to be answered is that how to test the leasing effect in China’s equipment manufacturing industry empirically.

In this study, we contribute in the following ways. First, we employ multi-level fuzzy linear regression model to analyze and examine the leasing effect in the total sample. Second we discover credit sale forecasting using this model. Third, we test the effect in different sub industries1 separately. From the result, we can see that what types of asset can be leased.

The remainder of the paper is structured as follows: Section 2 gives the detailed description about material and method used. Performance evaluation and result analysis is depicted in Section 3. Discussion of proposed work is presented in Section 4, while concluding remark with future recommendation is mention in section 5.

Material and method

Theoretical model

On the basis of study in [19, 20], we try to analyze the motivation of one kind of credit sales, which is financial leasing. This part is divided into the following cases: a) The users purchase products with loans from banks; b) The users purchase products with loans from the bank and with credit sales from the manufacturer.

Case a. Suppose that there are L manufacturers in the equipment manufacturing industry and M company (users). For simplicity, we divide the model into two periods [21]. The first period is that the user loans money from the bank. If the bank is willing to loan money, the loan rate is r. In the second period, two results may occur: the users pay on time or default. The company that pays on time is recorded as “safe”enterprise S, otherwise the company is recorded as “default” D. Although the bank can’t predict whether a company is a “safe” company, the proportion of “safe” enterprises is a and the proportion of “default” enterprises is 1 - a on the basis of past transactions.

C is denoted as the credit standard of the company, and Dis s (C) is assumed to represent the distribution of the “safe” enterprise under its credit standard conditions. In this paper, it is supposed to be a standard distribution, with mean value mn s and variance value of ϑ2. Suppose the distribution of “default”company under their credit standard conditions C, ND D (C) is also assumed to be normal distribution, with mean mn D and variance ϑ2. On average, the mean of the “safe”company is greater than that of the “default”company, that is mn s > mn D .

Whether to loan to the company depends on the credit standard of the company. If the credit standard C of the company is greater than the standard mandatory by the bank, the bank may consider the company as “safe” and is willing to loan money to the company. On the contrary, if the credit standard C of a company is lower, the bank will reject the company and doesn’t provide the company, it easily can be seen that the loan interest rate r, which is a function of C. If the company defaults, the bank takes back the collateral, and the return on assets is denoted as γ. Prob (S|C) denotes the probability of “safe”company under the credit standard δ and Prob (D|C) denotes the probability of “default”company under the credit standard C. Therefore, the expected income per unit of the bank is given by

If the company credit standard required by bank loan is supposed as C B , then the probability of obtaining bank loan is

The expectation of companys that obtain bank loans is

This means only M B companies are offered loans and purchase products from the manufacturers.

Suppose for the jthcompany, the cash flow generated by the product produced by the ith manufacturer is cf

ij

, where cf

j

= (cf1j,cf2j,…,cfLj,), j = 1, 2, ⋯ , M

B

. Suppose cf

j

(j = 1, 2, ⋯ , M

B

) is independent of each other, F (w

j

) is the distribution task of cf

j

, and function f (cf

j

) is the probability density function of cf

j

. Assuming that pc = (pc1, ⋯ pc

i

, ⋯ , pc

L

) is the product price of L manufacturers, each company tries to maximize its present value.

Where pc i is the product price of the ith manufacturer.

For the jthcompany, if δ ij ⩾ δ kj , that is cf kj ⩽ pc k - pc i + cf ij , the company will choose the product produced by the ith manufacturer, and the probability is

Since the present value of each user company is considered to be independent and identically distributed (i.i.d.), if the company buys the products of the ith manufacturer, it needs to satisfy.

In order to get the probability, we first need to calculate

Where,

So we figure out the company’s demand for product i:

So the expected revenue for ith producer is going to be:

Case b. bank loan coexists with vendor promotion

Companys get loans from banks and then buy product from manufacturers, from which manufacturers can make a profit. If the manufacturer wants to make a better profit, it can sell the product in the form of credit sales to those companys that cannot obtain loans from banks. Suppose the manufacturer requires C

C

as the credit standard of the company in financial leasing business. Obviously, if the manufacturer wants to gain more profits, the credit standard C

C

must be less than the credit standard C

B

set by the bank loan. In addition, the upper limit of interest rate of bank loan is set as

Generally speaking, if C ⩾ C

B

, the company chooses to loan money from the bank. If C

C

⩽ C < C

B

, the company chooses credit sales from the manufacturer. In the way of vendor leasing, the probability of user default is given by [15]:

Therefore, we can calculate the average income per unit of the manufacturer:

So the income of the ith producer is:

Where D c is the demand for product i.

Since C

B

is higher than δ

C

, so

So we can get,

In comparison, we can see that when manufacturers use credit to sell promotional products, they can get more revenue, which is also the reason why manufacturers are willing to use credit sales tools.

According to the above mention analysis, we propose the hypothesis:

Hypothesis 1: For equipment manufacturing enterprises, economic leasing has a constructive and important effect on sales profits.

Sample and data sources

In this study, A-share listed equipment manufacturing companies in China are selected as samples between 2008 and 2014. We extract the data from the database of CSMAR (China Stock Market and Accounting Research database) and Wind. The sample contains a total of 2681 observations.

Selection of variable and model for finance leasing effect and credit sale forecasting

Table 1 shows the variables and definitions in this study. For equipment manufacturing industries, Research and development (R&D) plays a very important role in the sales revenue. It can be said that R&D is the cornerstone of its survival. With R&D, companies can allocate internal resources more reasonably, grasp some new technology and apply them to improve the competitiveness of the company, and the innovation ability of the enterprise [10].

Variable Description

Variable Description

Marketing expenses also has an impact on the sales revenue. At the beginning, marketing will increase the expenditure of the company, the profitability will also be increased [12]. This is because users are easily affected by marketing activities.

Profitability also has an impact on sales revenue. Generally speaking, profit is the source of Research and development investment, which affects the income of companys. The lag of the first order of profit has a constructive and important effect on sales profits.

Industrial value added is the newly added value of industrial enterprises in the production process during a reporting period, which reflects the contribution of the production sector to the GNP. Therefore, the added value of an industry can reflect the input-output and economic benefits of enterprises, and can also provide reference for the production and operation of industrial enterprises.

Concept of fuzzy linear regression model

In this section, we use credit sale forecasting based financial leasing using fuzzy linear regression model [28]. This model generates non-fuzzy output based the non-fuzzy inputs. The base regression model is supposed to be a function of fuzzy linear regression and is defined as follow:

Where, B

k

(k = 1, 2, 3, …, n) represent fuzzy coefficient and is defined as (m

k

, w

k

) in which m

k

represent middle and w

k

represent width or spread and this fuzzy coefficient is represented in the form of membership function as show in Fig. 1, using following equation:

Fuzzy Coefficient

After Extension Principle application, fuzzy linear regression model expressed in the form of membership function with L-type fuzzy number [16] using following equation:

Using Equation (16), Equation (18) can be modified as follows:

The width or spread of

Subject to

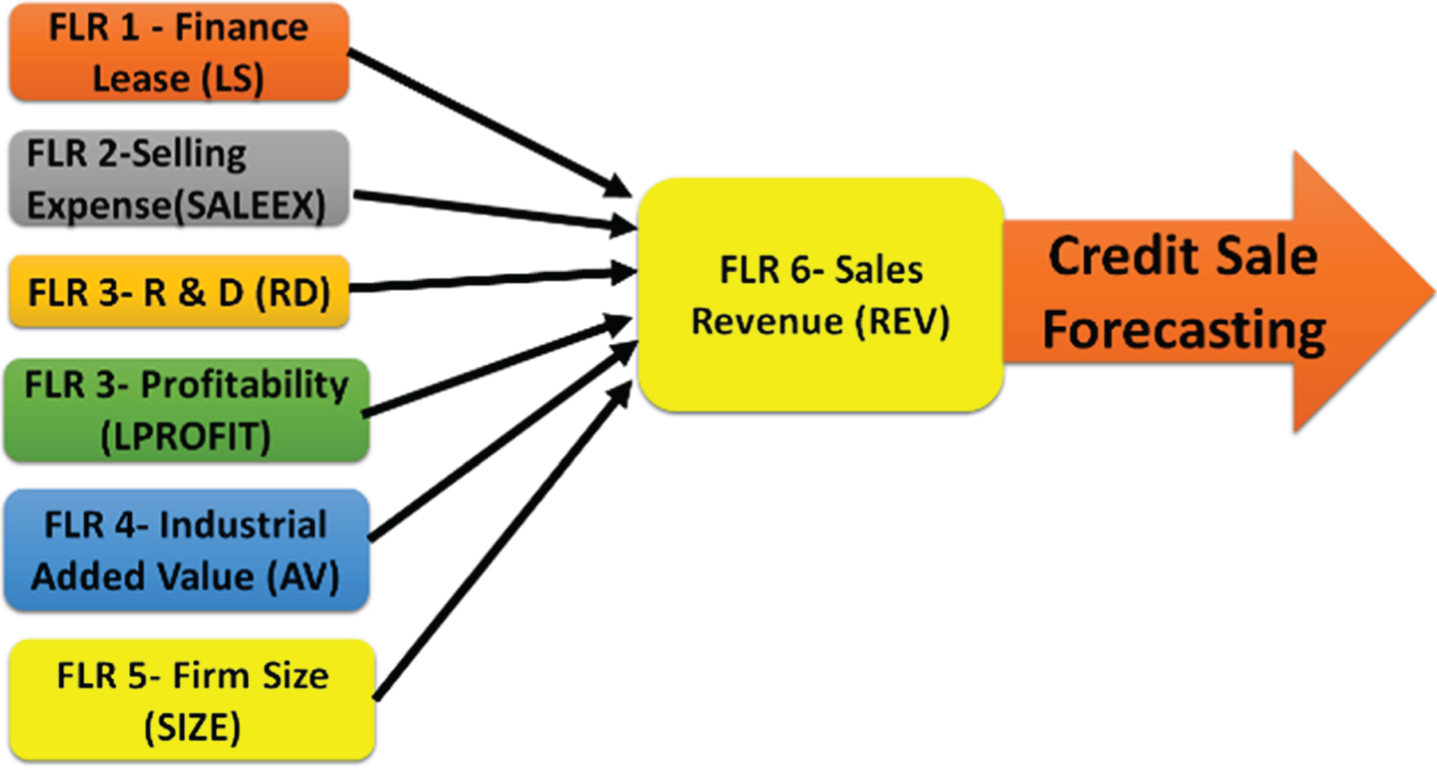

In this section credit sales revenue is forecasted from 2015 to 2020 using a multi-level fuzzy based linear regression model [21]. The framework architecture of multi-level fuzzy based linear regression model is shown in Fig. 2.

Multi-Level Fuzzy Based Linear Regression Model for Credit Sale Forecasting.

By using data from A-share listed equipment manufacturing companies in China between 2008 and 2014, fuzzy linear regression model for credit sale revenue forecast is defined as follows:

For credit sale forecasting in future Finance Lease, selling expense, R & D, profitability, industrial added value, and company size are forecasted. Then the fuzzy linear regression models are employed to forecast Finance Lease, selling expense, R & D, profitability, industrial added value, and company size from 2015 to 2020.

Results analysis over total sample

Fuzzy based linear regression (FLR)model outcome for total sample of model (1) is presented in Table 2. We can see that the coefficient of LS is significantly positive. It means the company’s income is 21.51% higher than the companys without financial leasing business. This result shows that financial leasing is an effective way of credit sales. The sales expenses are significantly positive, which means 1-unit increase of SALEEX will lead to an increase of 7.549 unit of REV. As part of the sales expenses, the advertising expenses can enable more customers to know the price, quality and various services related to the products, so as to arouse customers’ interest in buying the product, and the sales revenue increased [22]. In [23] it was concluded that enterprises with high income also have high expenditure on advertising. Furthermore, R&D has a positive impact on REV, which means 1 unit increase of R&D will lead to an increase of 2.699 unit of REV. In addition, profitability has a significant positive impact on REV, which means 1 unit increase of profitability will lead to 2.922 units increase of REV.

Regression results

Regression results

Note: Numbers in the parentheses “()” are t-values.*Signify implication at the level of 10%.**Signify implication at the level of 5%. ***Signify implication at the level of 1%.

From result analysis of FLR model from (2)to (8), we discover that in 1st, 4th, and 5th industriesfinancial and economic leasing rises sales revenue considerably, while 2nd, 3rd and 7th industry gain positive financial leasing effect on sales profits, it is not substantial. It is observed that diverse businesses have an excessive effect on the decision of financial leasing, which is consistent with many literatures. Many researchers believed that the exclusivity of industry products, the difference of investment credit and tax exemption in the industry [24, 31], the difficulty of product mortgage, the second-hand equipment market of the industry, the marginal tax rate of the industry and the liability capacity of the industry may affect the financial leasing decisions [25].

On the other hand, the assets of properties also have a huge effect on the decision of financial leasing [32]. Generally speaking, companys are more willing to lease equipment with strong flexibility. The later on it was found that there was a negative relationship between financial leasing and asset exclusivity [26, 27]. In [28] the lessee was reluctant to lease the equipment with strong exclusivity, because when the equipment was highly exclusive, the monopoly problem would increase the conflict and agency cost between the lessor and lessee. The durable the liquidness of properties, the easier the properties are to be leased [32].

Discussion

Financial lease is widely used in equipment manufacturing industries, but not in financial companies [33]. That how to test the leasing effect needs to be answered. In the present study, we have established a theoretical model to analyze the motivation of financial lease. Furthermore, we tested the impact of financial lease on sales revenue in total samples and sub samples empirically [34]. It suggested that the assets were easily to be leased if its liquidity is strong.

Our results were consistent with some previous studies. The exclusivity of industry products affected the financial leasing decisions [36, 37]. To be specific, the relationship between financial leasing and asset exclusivity was negative, which means manufacturers tended to lease products with stronger flexibility.

Conclusion

This research work is encouraged by a special spectacle that numerous Chinese industrialists occupy leasing commercial. The application of artificial intelligence in financial leasing business broadens the traditional marketing model and risk control model and improves the service efficiency [35]. The empirical analysis of result outcome demonstrates that total sample of economic and financial leasing has a constructive and important effect on sales profits.

This study takes a step forward in containing sub-industries. From the results of sub-samples, in sub-industries 1,4 and 5, financial lease have a significant positive impact on sales, and in sub-industries 2,3,6 and 7, there is no significant impact on sales. This shows that the characteristics of assets have an important impact on the financial lease decision of manufacturers. The more versatile the equipment, the easier it is to rent. This can provide a reference for whether the manufacturer is engaged in financial lease business. If its products have good liquidity, it can consider trying to use financial lease to sell equipment. On the contrary, if the manufacturer’s equipment is highly proprietary, financial lease may not be the best means of promotion.

Footnotes

1

According to China Securities Regulatory Commission, the equipment manufacturing industry is divided into seven categories. We use 1–7 to represent computer, communication and other electronic equipment manufacturing industry, metal products industry, automobile manufacturing industry, railway, ship, aerospace and other transport equipment manufacturing industry, general equipment manufacturing industry, instrument manufacturing industry, and special equipment manufacturing industry separately.

Acknowledgments

This research is supported by the Research Foundation for Talents of Hefei University (No. 18-19RC65), and also supported by Humanities and Social Science Project of Anhui Provincial Education Department (No. SK2019A0693).