Abstract

This research combines the Fuzzy Analytic Hierarchy Process (FAHP) with Case-Based Reasoning (CBR) to evaluate the intention of adoption of web ATM services. Compared with physical ATM service, web ATM allows users to perform financial transactions over the internet conveniently. Based on literature and considering the characteristics of web ATM, this study constructs a model for web ATM adoption that comprises three dimensions: The knowledge, the potential value, and the security. 222 valid user questionnaires are collected, and factor analysis is used to verify the factor structure of the decision hierarchy. FAHP is then used to calculate the weights of criteria with six experts through pairwise comparisons. Finally, FAHP weights are integrated into a CBR prediction mechanism for evaluating a user’s adoption intention toward web ATM. The results are helpful for financial institutions to understand and to evaluate the user behavior toward internet banking service adoption.

Introduction

The financial institutions in Taiwan have focused on developing internet banking, which is not limited to location-based banking services or self-service terminals, such as ATM. Innovative information services have increased consumers’ choice of methods for conducting financial transactions. When people are increasingly relying on the internet, internet-based transactions including e-auctions, e-cash, e-payments, and e-bidding are becoming more diversified and convenient for the users. Therefore, the multi-channel strategy has become the most popular business model for banks [15, 43].

According to a MIC online-shopping consumer survey in 2016, the most frequently used payment method is credit cards (75.7%), followed by the collection at convenience stores (66.4%), and automatic teller machines (ATM) payment (25.2%) [28]. ATM payments can be made via physical ATM by using ATM cards with a fund transfer function, or consumers can use online transfer via web ATM with a card reader. A web ATM is an online interface for ATM card banking that provides all the usual ATM functions without withdrawing cash. According to the InsightXploer survey, netizens in Taiwan use ATM (11.5%) vs. web ATM (7.8%) as a payment method for online shopping in 2016 [17].

Although most banks in Taiwan provide these online services, what are the factors influencing the decision of user adoption intention toward web ATM services? While many prior studies have investigated the factors influencing user acceptance of Internet banking [7, 47], little research has been conducted on the factor affecting user adoption of Web ATM. Thus, the objective of this study is to identify and evaluate the decision factors and to predict web ATM adoption. It is hoped that the results of this study will contribute to our understanding of the user decision toward web ATM adoption. The factors examined here could serve as the basis for a study in explaining the adoption of internet banking services.

The article is structured as follows. The first section deals with the theoretical foundations for the development of the research model of web ATM adoption based on the innovation adoption literature. After which research methodology is presented, with user questionnaire and factor analysis used to verify the factor structure of the decision hierarchy. FAHP is then used to calculate the weights of criteria, which are applied to the CBR prediction mechanism to evaluate the user intention toward web ATM adoption. Finally, results are discussed and conclusions are drawn.

Web ATM adoption model

The world’s first cash machine landed installed on a north London of Barclays branch in Enfield, transforming everyday banking for millions of people all over the globe [42], the use of cash dispensers (CDs) and ATM spread rapidly across the world. However, Taiwan has one Automated Teller Machine (ATM) per 826 residents, giving the island country the highest ATM density in the world [38].

In a content analysis of innovation definitions, “Innovation is the multi-stage process whereby organizations transform ideas into new/improved products, service or processes, in order to advance, compete and differentiate themselves successfully in their marketplace [2].” Evolved from ATM, web ATM is an Internet-based ATM is an online ATM terminal that does not give out cash bills. the flexibility represented by an ATM operating over the Internet, with instantaneous customer personalization, payment options, pricing alternatives and similar customized feature/functionality can be combined with speed, flexibility and lower cost of operational support, the Web ATM may prove to be a key ingredient in realizing the long term potential of the lowly “banker in a box” [1].

As the online banking services of various financial institutions are continually being updated, web ATM provide more personalized services for cardholders than physical ATM, such as common account editing, transaction message notification, and et al. Web ATM offer Internet-based banking services, for which user adoption of web ATM and their attitudes toward the use of web ATM can be seen as an innovation adoption. Brand and Huizingh proposed five factors that influence future intention to adopt e-commerce: knowledge, potential value, implementation, satisfaction, and adoption level [4]. Among them, knowledge refers to the e-commerce knowledge that a company possesses, such as knowledge of technology and customer needs of e-commerce. Potential value involves two aspects, the potential benefits and the costs of innovation adoption, and is similar to the concepts of relative advantage and perceived benefits. Adoption level refers to the level of e-commerce use in sales, purchasing, and customer service. Implementation refers to the complete integration and use of existing e-commerce software and hardware. Satisfaction refers to the results that emerge from the potential value variable of e-commerce.

This study develops a research model for user intentions regarding web ATM adoption. Based on the adoption model proposed by Brand and Huizingh, the knowledge and potential value dimensions are included in this study; whereas satisfaction, fulfillment, and adoption level are excluded because the target subjects include potential users who have not previously used web ATM [4]. This study also includes the security dimension which refers to the elimination of threats, risk, and suspicion through methods including physical security, financial security, and privacy protection in the model of service quality proposed by Zeithaml et al. [49]. Besides, Sukkar and Hasan reported that customers in developing countries are concerned about the security issues for the acceptance of internet banking [36]. This concern may affect their willingness to use Internet banking services, and reasons for not using internet banking services include a lack of customer trust, sound government policies, and regulatory protection. In summary, this study proposed three dimensions in the decision hierarchy of web ATM adoption: the knowledge, the potential value, and the security.

The knowledge criteria were primarily established to determine whether users possess sufficient knowledge of the hardware and software and whether users are familiar with the software operation. The knowledge criteria include knowledge regarding security component installation, installation of chip reader, the specification of required hardware, the need for browser version or above, and high compatibility.

The potential value criteria primarily emphasize user recognition of the value and potential benefits of web ATM. The potential value criteria include preferable handling fees, time savings, greater service capability, higher selectivity, no time restrictions, and easier financial management compared to physical ATM. The security criteria primarily emphasize the security considerations concerning transaction activities when using web ATM. So the security criteria include criteria such as leakage of transaction data, transaction errors, computer viruses, authentication method, and safety of transaction platform.

Research method

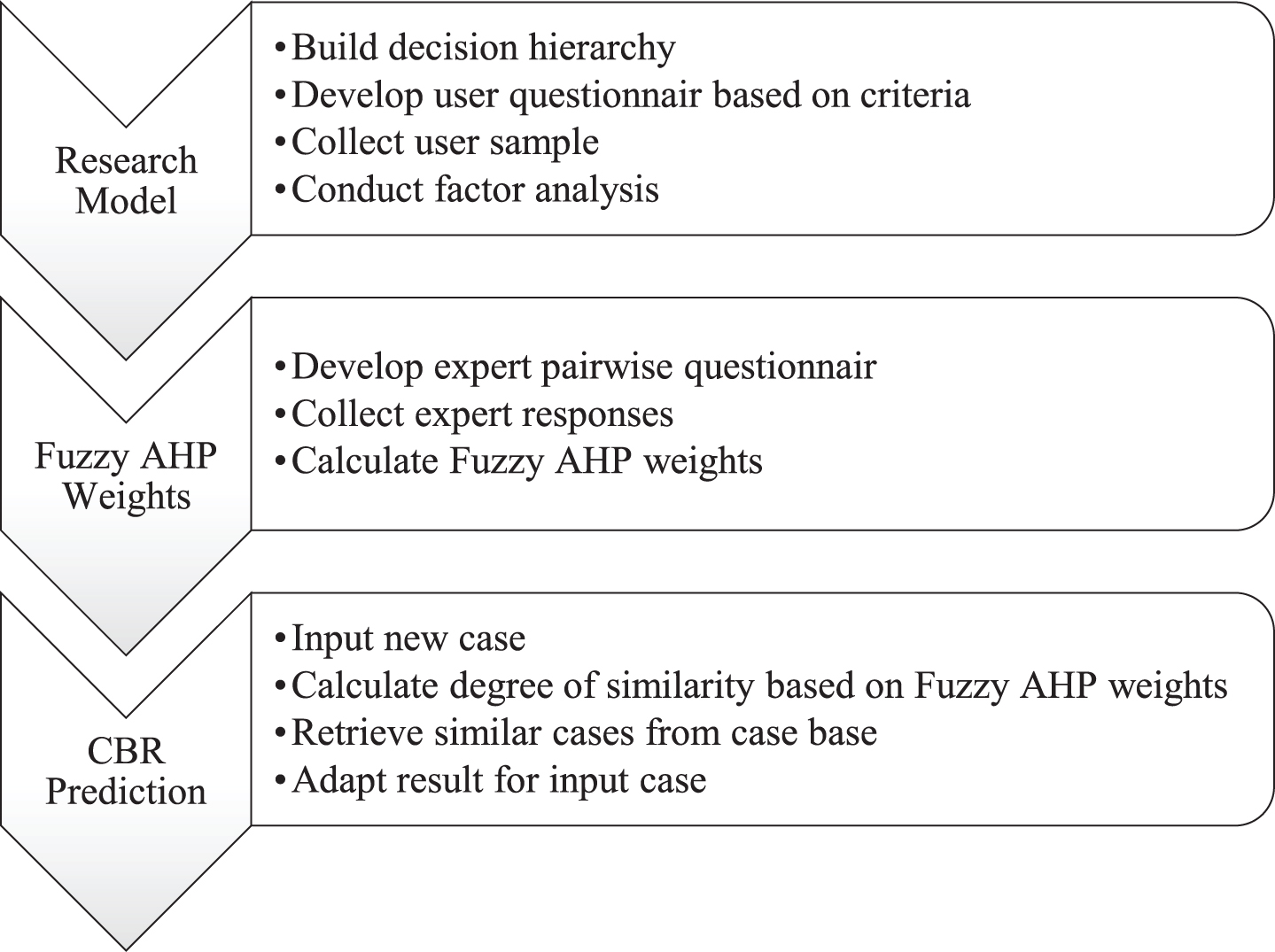

Research process

The research process is shown in Fig. 1. First, based on the literature, the research model of web ATM adoption is developed with three dimensions. The questionnaire items for general ATM users are developed based on the criteria in the model. 222 valid user samples are collected. Factor analysis is then used to verify the factor structure of the decision hierarchy. Second, this study adopts FAHP to constructs matrices for calculating a set of expert pairwise comparison. Six expert responses were collected and used to calculate the relative FAHP weight of the criteria to each level, and then structures the decision hierarchy as Fig. 2. Finally, this study employs Visual Studio.Net as the development tool to develop a prototype combining FAHP weights with CBR prediction.

The research process.

The research model of web ATM adoption.

The AHP was developed by Saaty in the 1970 s to define priorities and support decision making. To deal with the complexity of decision-making, the factors that affect the decision need to be identified and organized in a hierarchical structure. It is a method of measurement through pairwise comparisons which rely on the judgments of experts to determine priority scales to show how many times more important one element is over another element with respect to the criterion [32].

Alternative methods are reported such as Analytic Network Process (ANP), Technique for Order of Preference by Similarity to Ideal Solution (TOPSIS) and et al. [31]. ANP is an extension of AHP which adopts a network structure to present the relationship between criteria and alternatives. Reisi et al. applied ANP and AHP to the decision for industrial site selection [30]. Lin et al. applying the ANP and linear programming (LP) methods to provide the solution for green supplier selection and resolve the problem of order allocation for each vendor [23]. TOPSIS identifies solutions from a set of alternatives, in which the geometric distance between each alternative and the ideal alternative is calculated. Zyoud and Fuchs-Hanusch conducted a bibliometric survey on AHP and TOPSIS researches [50].

The AHP method can be extended and integrated with different techniques. Fuzzy theory combined with AHP to form fuzzy AHP or FAHP [44]. To deal with the vagueness of human thought, Zadeh first introduced the fuzzy set theory [48], which was oriented to the rationality of uncertainty due to imprecision or vagueness. A fuzzy set is a class of objects with a continuum of grades of membership. Such a set is characterized by a membership (characteristic) function, which assigns to each object a grade of membership ranging between zero and one [3]. A tilde “∼” is placed above a symbol if the symbol represents a fuzzy set. Therefore,

Fuzzy semantic variables based on Likert.

A triangular fuzzy number (TFN),

A triangular fuzzy number,

Each TFN has linear representations on its left and right side such that its membership function can be defined as:

A fuzzy number can always be given by its corresponding left and right representation of each degree of membership:

According to Brasil et al. [5], “Many decision-making and problem-solving tasks are too complex to be understood quantitatively, however, people succeed by using knowledge that is imprecise rather than precise.” Fuzzy set theory mirrors personal reasoning in its use of approximate information and uncertainty to make the human-like decision making. Fuzzy set theory encompasses fuzzy logic, fuzzy arithmetic, fuzzy mathematical programming, fuzzy topology, fuzzy graph theory, and fuzzy data analysis. However, the term fuzzy logic is often used to describe all of these.

The analytic hierarchy process (AHP) is one of the extensively used multi-criteria decision-making methods. One of the main advantages of this method is the relative ease with which it handles multiple criteria. In addition to this, AHP is easier to understand, and it can effectively handle both qualitative and quantitative data. AHP involves the principles of decomposition, pair-wise comparisons, and priority vector generation and synthesis. Though the purpose of AHP is to capture the expert’s knowledge, the conventional AHP still cannot reflect the human thinking style. Therefore, fuzzy AHP, a fuzzy extension of AHP, was developed to solve the hierarchical fuzzy problems [14].

Samuel et al. used FAHP technique to compute the weights of the attributes which were applied to train an Artificial Neural Network (ANN) classifier to predict heart failure risks in patients [35]. Tavana et al. integrated AHP, Adaptive Neuro Fuzzy Inference System (ANFIS), and ANN to predict and rank the suppliers’ performance [41]. FAHP is widely used by researchers to present a variety of problems and to evaluate criteria. There are systematic reviews of FAHP applications [8, 39]. Researchers mainly used literature to build the criteria, and FAHP to calculate their weights [31].

This study adopts FAHP to calculate criteria weights. The steps of generating FAHP weights are as follows: the positive reciprocal matrix was converted into a fuzzy positive reciprocal matrix; followed by group integration; then the fuzzy weights were calculated; and finally, the data were defuzzified and normalized.

First, the assessed value of the relative importance between the two criteria judged by experts using semantic variables was compiled according to group judgments. These semantic variables can be expressed using a triangular fuzzy number, which then uses the mean to integrate the judges of various experts as shown in Equation 3.

After establishing the positive reciprocal matrix by integrating all the experts’ judgments, as shown in Equation 4 to Equation 6, a fuzzy positive reciprocal matrix can be established, where T is the fuzzy positive reciprocal matrix.

According to the fuzzy weights calculated using the fuzzy positive reciprocal matrix, as indicated in a study by Buckley, the calculation of fuzzy weight is accomplished using the row vector of geometric mean; which can not only obtain the fuzzy weight of the fuzzy positive reciprocal matrix, but can also achieve normalization as an objective [6]. Fuzzy weight is calculated as shown in Equation 7 and Equation 8.

Where i is the row number, n is the column number (the assessment index number of the layer),

Where

Since these calculated weights are fuzzy weights, they need to go through the defuzzification process to obtain the critical success factors or these weights. When the weight of the triangular fuzzy number is

CBR is a computer reasoning method that is consistent with the analogical decision making in everyday human problem-solving. CBR use past experiences to address new situations [20]. CBR defines the description of the problem as a new case at the beginning. To address a new situation, the new case is compared with older cases in the case base to retrieve the most similar ones and find a suggested solution among them [20]. The solution is later validated through feedback from the user or the environment. Finally, the validated solution can be retained in the case base for use in future problem-solving if appropriate.

Research have applied CBR to a variety of domains ranging from pattern classification [46], to cost estimate [29], identifying knowledge leader within online community [37], diagnostic decision support system for healthcare-associated infections [12]. To design an appropriate case-matching mechanism in the retrieval stage, Yan et al. proposed using the learning pseudo metrics (LPM) to replace the widely used Euclidean distance in similarity function [46]. A similarity function or functions are used to compute the degree of match between the input case and the target case. The LPM-based retrieval method has been demonstrated improving the quality and learning ability of CBR classifiers.

Instead of focusing on measuring the degree of feature match in similarity functions, this study determines a set of expert weights for the case features. In a case-based approach representing a case with features tied to a context at an operational level is an important issue. Every feature in the input case is matched to a corresponding feature in the retrieved case. A weight is usually assigned to each case feature representing the importance of that feature to the match.

Hsu et al. pointed out that the feature weights can be assigned to a set of prior known fixed values or all set equal if no arbitrary priorities are determined. Usually, cases with higher degrees of match are retrieved and adapted to generate a solution [16]. However, the solution cannot be guaranteed if the weights are determined using arbitrary human judgment. A systematic mechanism for determining a set of expert weights can improve case retrieval effectiveness. Qin et al. found that CBR was an effective method in cost estimating and that AHP weights are better than equal weight and gradient descent method [29]. Wu et al. proposed a fuzzy CBR retrieving mechanism in which FAHP was used to determine weights for retrieve product-ideas that tend to enhance the functions of the baseline product [45].

The CBR prediction using FAHP weights can be considered as a four-step reasoning process. First, the new case is inputted into the prototype system. Second, CBR uses the similarity function to locate cases in the case base that are most similar to the input case. The new case is compared with each case in the case base to calculate the degree of similarity based on the FAHP weights. Third, the top k number of similar cases are retrieved based on the degree of similarity. Finally, the retrieved cases are adapted to generate the prediction result for the input case.

In web ATM adoption context, the case base is consisted of the user sample. A nearest-neighbor matching function containing the weights in the formula is shown in Equation 9.

Where f

I

is the input case;

A survey instrument was used to assess the factors and verify the proposed model. We first focus on measurement, the criteria reflecting the factors in the model were generated based on related literature and web ATM characteristics. A 5-point Likert scale was used for all measures to provide consistency for responses. The scales ranged from 1 indicating “Strongly Disagree” to 5 denoting “Strongly Agree.” In preparation for large-scale data collection, the survey instrument was pretested. These items were first reviewed for content by one experienced web ATM expert, one web ATM user, and one physical ATM user without the usage experience of web ATM. The respondents were asked to report encountered problems regarding the comprehensiveness of the instrument. The instrument was modified based on this feedback.

The revised questionnaire with the refined measurement was then used for a survey. A total of 248 surveys were delivered. The completeness of each received questionnaire was carefully examined. 26 questionnaires were thus dropped resulting in 222 valid ones, yielding a valid response rate of 89.52%. The descriptive respondent characteristic statistics are shown in Table 1. Ninety-one of them have experience using web ATM.

Descriptive statistics of respondents’ characteristics (n = 222)

Descriptive statistics of respondents’ characteristics (n = 222)

The gender and background distributions were as follows: ninety-three respondents were female (42%) and 129 respondents were male (58%); 53 respondents were from the military, civil servant, and teacher background (24%), followed by 41 respondents from the information and communication industry (18%) and 37 student respondents (17%); 169 respondents had online shopping experience (76%); 152 respondents had online auction experience (68%); and 91 respondents had experience using web ATM (41%).

The sample was used for exploratory factor analysis to identify the factor structure hidden in the data collected. SPSS was used for the analysis. All the 16 items were used to run factor analysis; principal components were adopted, and varimax was used to turn the axle. Kaiser-Meyer-Olkin (KMO) test is a measure of how suited the data is for factor analysis. The test measures sampling adequacy for each criterion in the model and for the complete model. As shown in Table 2, the KMO measure is 0.886 (>0.8), which is considered meritorious for conducting a factor analysis with the data [19].

Results of factor analysis (KMO:0.886)

According to the eigenvalue rule, a three-factor structure emerged. Those factors with eigenvalues greater than one were selected. Criterion with factor loading higher than 0.50 was used for the identification of the factor [13]. All criteria in the model were loaded on their respective factors, and no criterion loaded higher on factors they were not intended to measure.

Reliability of each factor was assessed by Cronbach’s α. There are different reports suggested the acceptable values of alpha, ranging from 0.70 to 0.95 [40]. As shown in Table 2, the value of alpha associated with each factor is at an acceptable level, ranging from 0.915 to 0.947. In addition, the factors are listed in the order of the variance they explain. The first factor, potential value, explains 27.023% of the variance in the data; the second factor is knowledge (25.177%); the third factor is security (23.612%). The results of factor analysis support the three-factor structure proposed in the research model.

Subsequently, FAHP methods was used for calculating the weights for CBR prediction. Six expert responses were collected from one senior manager and one manager in online banking department, one clerk handling ATM services in customer service department at banks; one R&D department manager, one manager and one assistant manager in IT department at ATM service companies. They are inquired to determine priority scales through pairwise comparisons.

The Expert Choice and Microsoft Excel software was adopted to obtain the FAHP weights using the judgments of six experts. Table 3 shows the resulted FAHP weights in the criteria level. The consistency index (CI) value of criteria is 0.01 (< =0.1), and the consistency ratio (CR) value is 0.02 (< =0.1) which indicated the expert judgments were consistent [33].

FAHP weights

The mean average errors (MAE) for CBR prediction are shown in Table 4. It is indicated that FAHP+CBR outperforms AHP+CBR in all the MAE results for k = 1 to 10. Also, the average MAE of FAHP+CBR is 0.40 and AHP+CBR 0.44. The CBR predictions made using FAHP weights were more accurate than those using AHP weights, regardless of the number of similar cases retrieved.

Mean average error (n = 222)

Web ATM is a convenient internet banking service instead of the physical ATM and a significant payment channel for e-commerce in Taiwan. This study develops the web ATM adoption model which is further used in predicting user intentions to adopt web ATM. There are three factors and 16 criteria in the model. According to the values of FAHP weights from the expert view of point, the factors sorted by priorities concerning web ATM adoption are (1) web ATM security, (2) web ATM knowledge, and (3) web ATM potential value. The six experts consistently agree that security is an essential issue for users to adopt web ATM services. The factor of web ATM security includes transaction data leakage, transaction errors, and computer viruses; whether using the “chip card and password” method to authenticate web ATM security is considered safe; and whether users consider the web ATM on financial transaction websites to be safe.

On the other hand, according to the Eigenvalues of factor analysis from the user view of point, the factors sorted by the explained variance concerning web ATM adoption are (1) web ATM potential value, (2) web ATM knowledge, and (3) web ATM security. This indicates the potential value of web ATM is more contribution to explain users’ intention to adopt web ATM. The factor of web ATM potential value includes whether web ATM save time, provide a variety of services rapidly, offer easier financial management and favorable transaction fees, have higher service capability compared to physical ATM, limit use time, and can provide services from multiple banks simultaneously with a broader range of selectivity.

User knowledge of web ATM is also a decision factor of web ATM adoption, including (1) Users’ awareness of the need to install security components when connecting to the web ATM transaction platform. When accessing the web ATM platform of financial institutions, users are instructed to install security components such as ActiveX, which is a communication component that bridges a remote (bank side) web ATM system with the user’s computer system. (2) Users’ awareness of the installation process of chip card readers (driver installation), because a computer typically cannot recognize a new device, installing drivers is necessary for the chip card reader to establish a link to the computer for communication. (3) Users’ awareness of the hardware specifications required for web ATM use (computer hard disk space, processing speed, memory size, and card reader specifications). (4) Users’ awareness of the browser version specifications required for web ATM use to display content correctly. (5) Users’ awareness of web ATM can run on various computer systems and are highly compatible. The web ATM transaction platform provided by financial institutions in Taiwan supports operating systems such as Windows, Mac, and Linux. If the computer environment is MAC OS X or Linux operating system, users need to install the relevant plugin to execute normally.

AHP is a structured technique method for analyzing multi-attribute decisions. The method dependents on the experts’ point of view. FAHP uses fuzziness to change the values in the scale of expert judgments. Although Saaty and Tran indicates that uncertainty in AHP can be solved by using intermediate values in the 1–9 scale combined with the verbal scale [34], FAHP weights seem to work better in CBR prediction to obtain accurate results than AHP weights in this application. Research such as Wang et al. shows that FAHP and CBR applications are feasible and effective for extracting the style of the product [11]. However, the objective of this research is not to assess the use of the two methods.

According to the values of FAHP weights, the first five important criteria in the three factors are (1) the security concerning “transaction data leakage”, (2) the security concerning “transaction platform safety”, (3) the users’ awareness regarding “authentication process”, (4) the problem concerning “transaction errors” and (5) “computer viruses”. Noteworthy, all concern the security aspect of web ATM, which is consistent with the research indicating the role of perceived risk as a predictor of intention to adopt internet banking [27].

This study developed the web ATM adoption model based on the literature and verified the factor structure of the decision hierarchy from the users’ perspective. This study further proposes a mechanism which integrates CBR with FAHP weights measured by expert pairwise judgments to predict web ATM adoption. The results are helpful for financial institutions to understand the user decision toward web ATM adoption and to further predict the user behavior by referring to expert opinions. This study adopts FAHP to calculate weights for decision criteria, CBR with other weighting methods for the prediction of innovative internet banking services can also be examined in the future.