Abstract

Cryptocurrencies have emerged in the last decade as a new asset class unlikely to disappear despite its extraordinary volatility. Futures contracts on Bitcoins were introduced in December 2017 by the Chicago Mercantile Exchange followed by options in January 2020. Our goal in this paper is threefold: (i) present the main features of cryptocurrency spot and derivative markets; (ii) argue that the custody recently granted by large financial institutions to their large customers for their bitcoins shows that Bitcoins are very similar to commodities, allowing the extension to bitcoins of the convenience yield introduced by Working (American Economic Review, vol. 39, 1949, pp. 1254–1262) in the Theory of Storage; (iii) use the prices of options traded on the Deribit Exchange to build the volatility smiles and skews observed at different dates of 2019 for short and long dated maturities and compare them to smiles/skews of equity options.

Keywords

Introduction

Since the famous paper by Satoshi Nakamoto [10] which brought to light the blockchain technology and the trading of Bitcoins, many other cryptocurrencies have been created and national cryptocurrencies are being discussed, as in Sweden.

Financially settled Futures contracts were introduced in December 2017 by the Chicago Mercantile Exchange. ICE (Intercontinental Exchange Incorporated), the parent company of the New York Stock Exchange, started trading bitcoin Futures in its Bakkt unit in December, 2019 after getting the green light of the US Commodities Futures Trading Commission (CFTC). For the first time, these Futures will be physically settled in Bitcoins, adding to the similarities between bitcoins and commodities. At the same time, the CME asked the CFTC to allow its clients to double their open bitcoin Futures positions, up to a monthly limit of 2,000 contracts (instead of the previous 1,000) per maturity. Cryptocurrency Exchange Binance launched in September 2019 Futures written on its in-house token.

Call options give buyers the possibility of getting a financial exposure to Bitcoins without paying their full price while puts provide the classical downside protection to those owning the cryptocurrency. The exchange called Deribit gives a trading platform for options on Bitcoins with a fairly large liquidity and will be used for our option prices. Our goal in this paper is threefold: (i) present some features of cryptocurrency spot markets and explain why the storage devices, old and new, ensure the existence of a convenience yield, a key parameter in the risk-neutral drift of the spot price dynamics; (ii) propose for this continuously traded asset class a Black Scholes type approach to the valuation of options on Bitcoins; (iii) use the prices quoted on the Deribit exchange to infer implied volatilities and build smiles and skews.

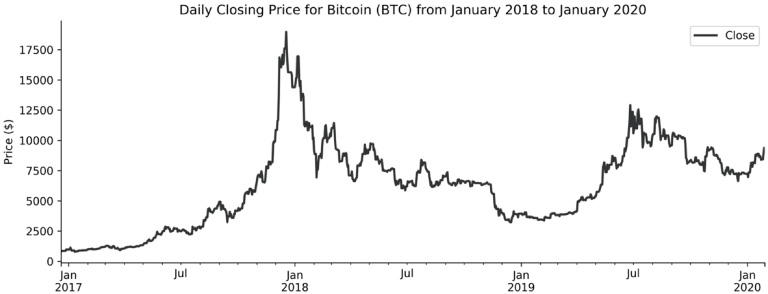

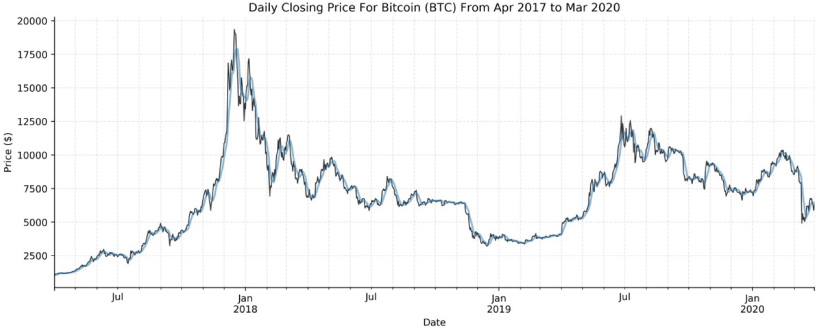

Price trajectory of Bitcoin – January 2017 to January 2020.

The remainder of the paper goes as follows: Section 2 presents some features of cryptocurrencies in recent years and discusses the Bitcoin Futures contracts already introduced. Section 3 makes the case for a continuous diffusion driving the price; its risk-neutral drift is derived from traded Future prices and discusses the prices of options on Bitcoins traded on the Deribit Exchange. In Section 4, smiles and skews of implied volatilities are displayed for options of different dates, together with the corresponding forward curves. Section 5 concludes.

Some properties of Bitcoin spot prices

Bitcoins appeared in October 2008 with the famous paper of Satoshi Nakamoto advocating for “a fully peer-to-peer electronic cash system”. Bitcoin trading requires the necessary prerequisite; a blockchain, which is a secured platform and a ledger, and is currently developed for a variety of applications unrelated to the trading of cryptos. The total market capitalization of all cryptocurrencies was 828 billion dollars in January 2018 (just after two Exchanges launched Futures), 200 billion in August 2018 and 272 billion in September 2019, 68% being Bitcoins.

The price trajectory of Bitcoins displays the remarkable rise related to enthusiastic investors during 2017. As of December 2017, the bearish ones were finally able to express their sentiment by taking short positions in Future contracts. A cautious comparison can be made with gold which experienced a 50% drop over two years after Futures were introduced on the COMEX in December 1974, the highest value reached by the ounce of gold being the day before gold Futures started trading (see [7]).

To our best knowledge, this is the first paper which discusses the relationship between Bitcoin spot and Futures prices and infer an ownership yield from the convenience yield and cost of insurance for the custody of bitcoins currently offered by large financial institutions.

The total market capitalization of all cryptocurrencies was 828 billion dollars in January 2018 (just after two Exchanges launched futures), 200 billion in August 2018 and 272 billion in September 2019. Note that the fraction of bitcoin in the total market capitalization was 86% in January 2017, went to 34% in January 2018 and back to 68% in September 2019.

Looking at the price trajectory of Bitcoins, one can argue that the remarkable rise during the year 2017 was related to enthusiastic investors betting on an irresistible increase in its value. As of December 2017, those who had an opposite view were finally able to express their sentiment by taking positions in Future contracts. A cautious comparison can be made with gold which experienced a 50% drop over two years after Futures were introduced on the COMEX in December 1974; the highest value reached by the ounce of gold up to that moment was exactly the day before gold Futures started trading (see [7]).

To our best knowledge, this is the first paper which provides a tentative arbitrage approach to the valuation of bitcoin derivatives and the consistency between Futures and option prices.

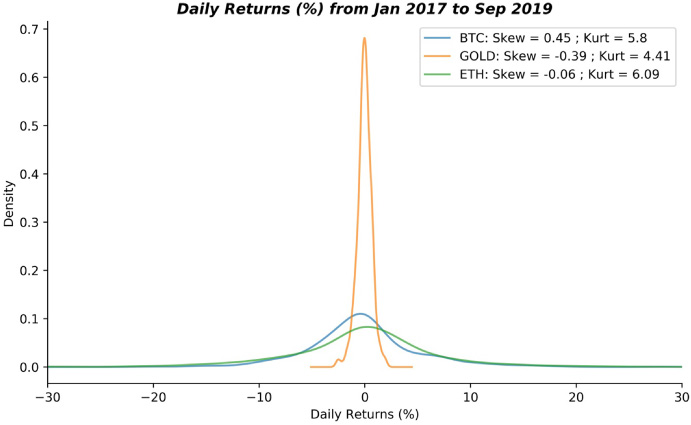

Daily returns distribution on Bitcoin, Ethereum and Gold.

The price magnitude reduction in the vertical scale of Fig. 1 displays the very large price changes over a fairly short time period. In July 2019, the famous Winkerbros brothers’ 65-million investment in Bitcoins generated by the sale of their rights in Facebook went over $1.45 billion.

We plot in Fig. 2 the daily returns on Bitcoins together with those of the popular cryptocureency Ethereum as well as gold returns.

The first group of Futures contracts was created by the Chicago Mercantile Exchange (CME) and launched in December 2017. They have a financial settlement in dollars at maturity, like the S&P 500 Futures contracts and in contrast to the “physical” delivery of the underlying asset which prevails for most commodities. CME Futures are subject to significant regulatory oversight by the Commodity Futures Trading Commission (CFTC), and are protected from counterparty risk by the Clearing House of the Exchange - a desirable feature since more than 36 cryptocurrency trading venues had closed by the end of December 2018. Moreover, they partly allow avoiding the fragmentation that sometimes prevailed in the Bitcoin spot market: during periods of high volatility, prices observed for Bitcoins on different platforms over identical time periods could diverge by more than 10%.

The CME settles its contracts against an index called BRR (Bitcoin Reference Rate) which is an average of spot prices quoted on different exchanges. The CME contracts size is five Bitcoins.

As of their launch in December 2017, the CME Bitcoin Futures have required a remarkably high initial margin of 44% of the previous day settlement price (compared to 3% for crude oil Futures) and 40% of this number for maintenance margins. Moreover, these margins change daily (floating margins), a feature which is unique to Bitcoins like the size of the margins itself.

Volume of nearby traded futures contracts on the CME from Dec 2017 to Sept 2019.

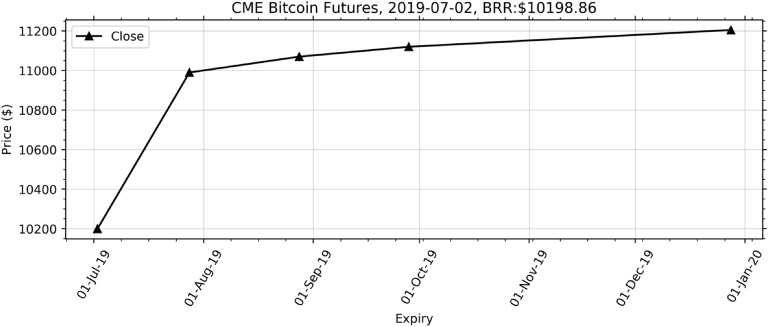

CME forward curve observed on July 2nd, 2019.

Volumes of Futures Contracts on the CME since launch, On May 13th, 2019, approx. 33,600 contracts (168,000 Bitcoin). Comparative Opening Volumes: CME: approx. 5,000 BTC; CBOE: Approx. 4,000 BTC; Bakkt: 72 BTC.

Other Futures Exchanges

There are four major exchanges offering futures, other than the CME. Bitmex, Deribit, Okex and Kraken, with Okex and Kraken launched Futures in 2019. Bitmex and Deribit have been trading for many years, Bitmex with high liquidity; for example the XBTH20 contract peak volume was $165 Million on the 14th of January 2019.

Cryptocurrencies have taken a further step in the direction of commodities with the emergence of cold storage. Cold storage means generating and storing the crypto coins private keys in an offline environment in order to avoid the online vulnerability to hacking. The most popular cold storage options are: (a) a paper wallet that contains a pair of private/public keys printed on a piece of paper, with keys generated offline securely; (b) A hardware wallet, which is an electronic device, but the most robust cold storage choice for cryptos. For non-institutional clients, three popular options offered on the market are Ledger Nano, Trezor and Keepkey. A USB stick can also be used for limited security. Hardware Security Modules (HSMs) as used in other industries. Multi-signature wallets require a quorum number of signatures to provide a valid authorisation to transfer funds, mostly this is Ledger based. MPC (multi-party computation security) can be ledger neutral and derived from cryptographically splitting the private key.

At the same time, a platform called Coinbase where users can buy and sell Bitcoins and other cryptocurrencies is launching a program for institutional investors that will pay them a set interest rate for certain currencies likely to be between 5 and 8% - when they keep their coins in its custody service, a further evidence of the storability of physical cryptocurrencies.

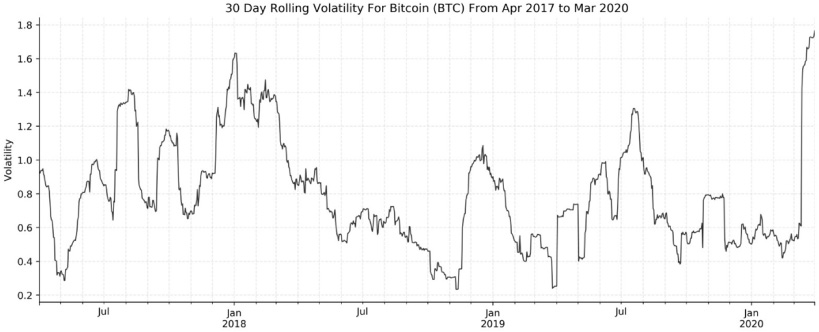

30-day volatility for Bitcoin.

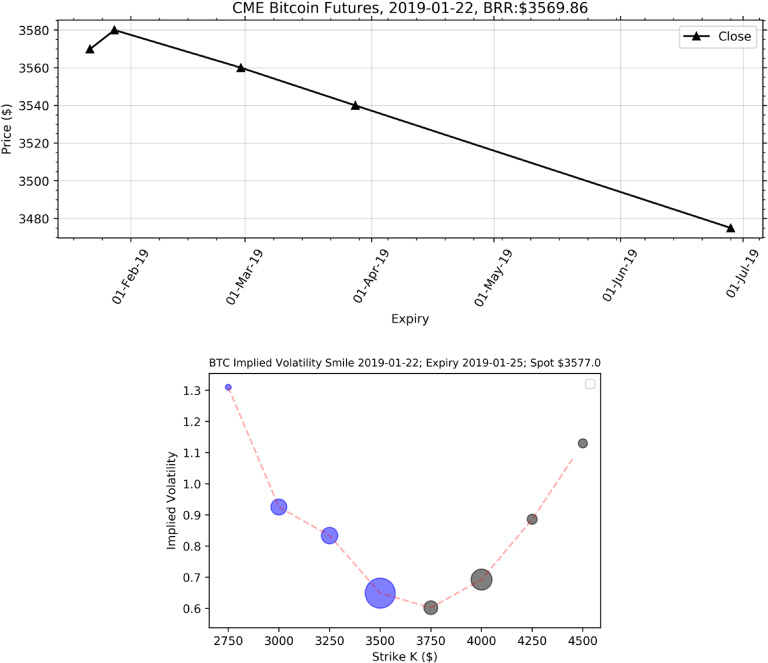

CME Futures curves and Deribit implied volatility smile on 2019-01-22. See a).

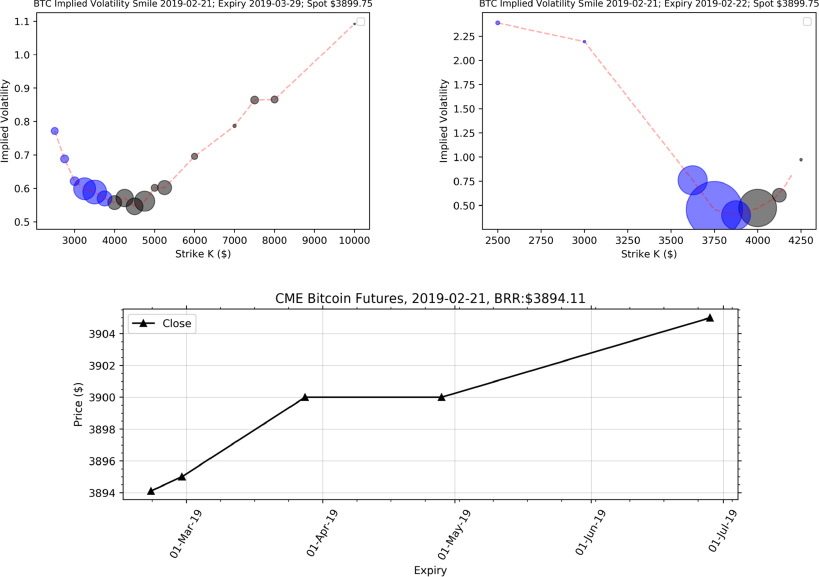

CME Futures curves and Deribit implied volatility smile on 2019-02-21 for long and short expiry. See b).

CME Futures curves and Deribit implied volatility smile on 2019-04-04. See c).

We argue that cryptocurrencies have taken a further step in the direction of commodities with the emergence of ‘cold storage’ (see [5]) and propose to extend to cryptocurrencies the convenience yield proposed by famous economists like Working [13] to represent the virtue of owning a physical commodity as opposed to a derivative/financial contract written on it. We argue that holding physical Bitcoins presents a benefit because of illiquidity and frictions in the purchase of spot Bitcoins, hence that a convenience yield deserves to be introduced. We denote y this convenience yield (defined as benefit minus storage cost) and write the spot- forward relationship for cryptocurrencies, namely:

CME Futures 2019-04-18 curves and Deribit implied volatility smile on 2019-04-19. See d).

It is important to notice that this relationship prevails also for currencies and equities, namely all asset classes that have been alternatively proposed to represent Bitcoins; it has the remarkable property of being independent of the choice of a given stochastic process for the spot price (see [4]).

The storability and spot-forward provide us with an easy way to short bitcoins and repeat the replication argument (see [12]) introduced in the famous papers of [2,8] to price options on Bitcoins.

We argue that the dynamics of the spot price is represented by a diffusion because Bitcoin is a truly continuously traded asset; most market participants assume for simplicity that all other assumptions of the Black Scholes Merton [8] model hold. The fact that liquid options are short dated makes this approach acceptable and implied Volatilities are going to be computed accordingly. Our Smiles and Skews are built using data from Deribit, which is by far the most popular Exchange to trade Bitcoin options.

Bitcoin options started trading on 13th of January 2020, with each contract representing 1 Bitcoin Futures contract (which is 5 Bitcoins). The option settles on the last Friday of the contract month at 4.pm London time, same time as the Future contract. These are European options on Futures. Bakkt launched it options on the 6th of December but has seen less volume.

Volumes for Bitcoin options for CME, January 2020

Volumes for Bitcoin options for CME, January 2020

The general setting

Options on Bitcoin offer buyers the usual benefits of options, calls giving, in particular, the positive exposure to the spot price without paying the full price of the underlying.

We argue in favour of a diffusion to represent the evolution of the cryptocurrencies, because of their unique property of being continuously traded, - erasing, in particular, the problems created by the overnight closure of equity markets. Moreover, we choose the geometric Brownian motion often proposed in the literature and an acceptable model for the average lifetime of traded options.

Hence, the price process (S(t)) is driven under the risk-adjusted measure Q by the stochastic differential equation:

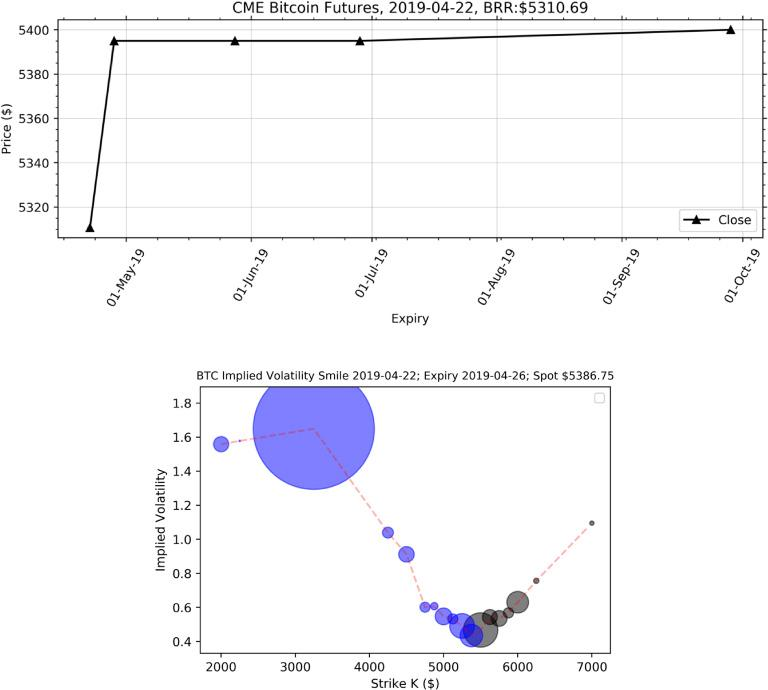

Take as an example the forward curve observed on April 22, Exhibit 10, when the spot was $5310. It was increasing, indicating that the investors were optimistic, possibly because it was the time when Libra, the cryptocurrency proposed by Facebook, was first discussed.

CME Futures curves and Deribit implied volatility smile on 2019-04-22.

CME Futures curves and Deribit implied volatility smile on 2019-05-06.

From the spot-forward relationship, Exhibit 10, written for the maturity T = September 30, 2019, we have that T − t = 5∕12, and we derive from f(t, T) = $5400 that r − y = 0.68%, hence y = 1.32% for a short-term rate r = 2%.

The cost of insuring bitcoin storage currently quoted by Coinbase, the largest bitcoin warehousing provider with $7 billion worth of bitcoins in custody, is c = 50 basis points or 0.5%; remembering that y is the convenience yield net of storage cost y = b − c, we obtain that the pure benefit b perceived by the market in the ownership of a physical bitcoin is of the order of 1.82% per bitcoin per year.

After Futures contracts, options on Bitcoins are obviously the next class of derivatives to be analysed. We know from commodities that the Merton [8] formula would easily provide the price as long as the crucial quantity (r − y) deservedly discussed above is identified. The transparency in option prices that will prevail after the introduction of options by the CME in January 2019 will let us know whether the other assumptions of the Black–Scholes–Merton model, in particular the one constant volatility for the spot, will be validated by the market. In all cases, the deep understanding of the Futures prices (a challenging exercise) is a necessary step to option pricing, in particular in the case of complex underlyings as explained by Taleb [11].

The forward curve provides us with the quantity (r − y), which is our targeted risk-neutral drift and does not need to be broken into the two components, thus avoiding any numerical assumption on the proper risk-free rate for bitcoins.

Lastly, under constant interest rates - an assumption already made above and certainly acceptable for short-dated options, the forward price f(t, T) and the Future price (quantity observed on the Exchange) of the same maturity F(t, T) are equal.

The other key parameter is the volatility parameter in the diffusion process driving S(t); we propose to use the (annualized) volatility computed over m days of observation and given by the formula

Exhibit 5 shows that the volatility is not constant over the period May 2018 to May 2019 and has a pattern that is mean reverting to the level of 60%, with extreme values of 22% and 100%. Note that the highest values of the volatility were never observed in equities or ordinary commodities, but only in electricity markets in the early days of deregulation (see [6]) – interestingly, electricity is a continuously consumed commodity. This is an agreement with our view of Bitcoin as some extension of electricity electrons, and their status as a hybrid of equities and commodities as we argued before.

We consider as date 0 May 8, 2019. The spot price of Bitcoin was S(0) = $5750. We choose for maturity date September 27, 2019, meaning that T = 142∕365 since Bitcoin traded every calendar day. The Future price for maturity T is $5815 (see Fig. 4), and we can derive from the spot-forward relationship the value x = 2.8%. We consider a strike K of $6,000 and use the Merton [8] formula established for stocks paying a continuous dividend and extended to a convenience yield (see [4]).

Volatility uncertainty, bitcoin market incompleteness and option price bounds

The property of increasing monotonicity of European calls and puts with respect to the volatility parameter as expressed by a strictly positive vega in the Black–Scholes model leads to the natural intuition that bounds on volatility provide market participants with bounds on option prices. This result is mathematically not straightforward – and does not hold if the bounds are themselves stochastic - is quite useful as volatility is not constant over the lifetime of the option in the case of Bitcoin (see Exhibit 5), as in all asset classes.

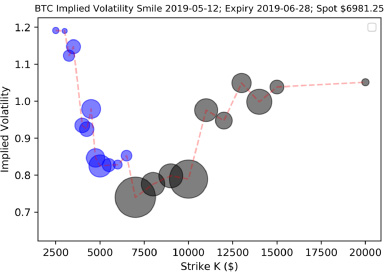

Deribit implied volatility smile on 2019-05-12. See g).

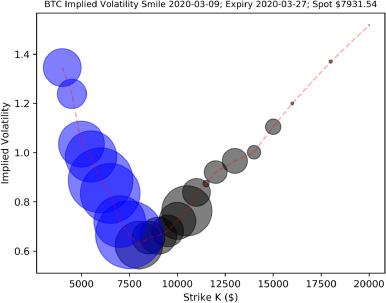

BTC smile on March 9, 2020.

In their [1] paper, Avellaneda et al. formally addressed this issue when pricing and hedging options in an environment of uncertain volatility. Assuming that this volatility lies between bounds denoted by l and L, the authors validate our intuition that the option price is comprised between the numbers obtained for l and L. They also observe that l and L could be inferred from observed implied volatilities of option prices or from high-low peaks in historical volatilities. Accordingly, a rational agent would try to sell the option using the upper bound value of the volatility and buy at the lower bound value.

We use the classical rule of puts for strikes below the At the Money (ATM) value and calls for strikes above in order to plot the implied volatility extracted from option prices traded on the Deribit exchange as a function of the strike; the circles are proportional to traded volumes throughout all graphs and closing prices are used for the options.

(a) On January 22, Exhibit 5, for maturity January 25, the smile was symmetric around the ATM value of $3577. The three forward curves (high, close, low) are mildly declining, indicating that the market is not anticipating big moves of Bitcoin prices; the volatility is high, however, comprised between 60% and 110%.

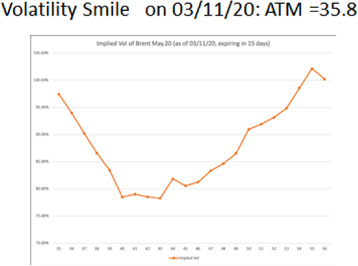

Volatility smile for crude oil on March 11, 2020.

Trajectory up to the end of March 2020.

The unprecedented volatility spike in March 2020.

(b) On February 21, Exhibit 6, for maturity Feb 22nd, essentially the same property prevails for the shape and the volume around the ATM price of $3899, probably because of the 8.7% price increase since January 22.The three forward curves are increasing and 5 weeks to expiry the smile is skewed to the right, indicating that market participants are buying calls for price exposure.

(c) On April 4, Exhibit 7, the spot was at $5019; the high forward curve is markedly increasing while the close and low are moderately decreasing. The neutral view of the investors is reflected in a fairly symmetric smile for the maturity of April 26, except for the large volume of puts with strike $3500, which seems to indicate that someone holding a long position was hedging by buying out- of- the-money puts on that day.

(d) On April 19, Exhibit 8, and for a time - to - maturity of 7 days, we observe again a remarkably symmetric smile and prudently conclude that close to maturity, the smile is fairly symmetric, indicating that investors do not generally anticipate a big collapse of Bitcoin prices within one or two days; still, the skew is more to the left, like in Equities. The forward curve was mildly positive, indicating a fairly positive sentiment in the market.

(e) On April 22, Exhibit 10, the spot had gone up to $5307 and from the forward curve shape, investors look optimistic. The volatility smile for a two-day duration is fairly symmetric as observed earlier for very short dated options; a large put buyer disrupts the symmetry with an implied volatility of 160% compared to a 40% volatility at-the-money.

(f) On May 6, Exhibit 11, the spot was higher at $5650; the investors continued to be positive and the forward curve increasing. The options maturing on September 27 exhibited a large volume on the side of the buyers of calls with a regular consistency in prices while the put’s buyers were more dispersed. Note that we observe a gain a skew to the right for ‘long’ dated options.

(g) Turning to the date of May 12, the spot price had gone up to $6981 from $5319 on May 5, meaning an increase of 28%. Remarkably, the liquidity was essentially located in calls - signalling buyers who wanted positive exposure to Bitcoins and prepared to pay the high implied volatilities that ranging from 70% to 100% for the calls (and 120% for the puts that some were purchasing to protect existing long positions they had). Note that on May 6, spot prices were lower and the lowest volatility was 60%, a large difference with 70%.

We can conclude from this section that there is indeed consistency between the forward curves and option smiles/skews. It also appears that the shapes observed for the latter ones at this point in time bring Bitcoins close to the asset classes of equities and commodities.

On March 9, 2020, in the middle of the financial crash, Bitcoin price somewhat resisted in a first stage. Figure 13 shows that the implied volatility was comprised between 60% and 140%, with a skew to the left indicating that buyers of puts were prepared to pay a large premium to get a downside protection for the 18 following days.

As a comparison, on March 11, the implied volatility in Crude Oil was comprised between 78% and 100% (numbers fairly similar) in a situation of market turmoil aggravated in the case of crude oil by a geopolitical crisis between Russia and Saudi Arabia.

After March 11, 2020

On March 12 2020, Bitcoin experienced the third sharpest collapse of its history, 38%, while the stock market was also collapsing because of the full development of the terrible news around the Coronavirus; the other big falls had taken place on April 11, 2013 (minus 47%) and June 11, 2011 (minus 39%). $876 million worth of derivative positions were liquidated on the Bitmex platform on March 12, 2020. Between March 9 and 16 2020, 70% of the Bitcoins sold on exchanges were coming from portfolios of 10 to 1000 bitcoins and 10% from portfolios containing more than 1,000 bitcoins After the massive amounts of money promised by the Federal Reserve to the economy, Tyler Winklevoss, a key figure in the world of Bitcoins, declared that Bitcoins gave protection against money printing.

We have investigated in this paper a number of bitcoin properties, in particular the storability and convenience yield, which allows us to write the valuable spot-forward relationship. We extracted from options traded on the Deribit exchange smiles and skews that we compare to forward curves on the same dates of analysis to check whether there was consistency between the views of the traders of Futures and those trading options. Even though large discussions are taking place around Libra and other proposed national cryptocurrencies as means of payments, it seems that market participants still view Bitcoin as an investment vehicle similar to stocks and the options written on it as a way to get exposure to this new asset class. The events of March 2020 confirmed the fact that Bitcoin has become a standard asset class, mostly different by its volatility.