Abstract

The International Public Sector Accounting Standards have been seen as a path towards the modernization of governmental accounting, and many countries have made efforts to adopt them. The purpose of this article is to analyse the stimuli and barriers to the adoption of International Public Sector Accounting Standards, as well as their main benefits, using a structural equation model. The research methodology is based on a questionnaire sent to American and European Union countries that has been used to construct a structural model, and our results show that comparability and modernization are direct benefits of International Public Sector Accounting Standards implementation, and that both adopter and non-adopter countries value these positive impacts. This justifies the process of harmonization that the European Commission recently started.

Points for practitioners

The analysis of the impact of International Public Sector Accounting Standards in the international context shows to what extent the adoption of International Public Sector Accounting Standards are useful for modernizing governmental accounting and achieving accounting comparability. Describing the experience of countries that have adopted International Public Sector Accounting Standards can help practitioners and professionals who participate in modernizing accounting systems, such as the European Union. Many countries are now moving towards International Public Sector Accounting Standards and the experiences of pioneer countries can serve as a learning process. This article shows that introducing International Public Sector Accounting Standards can have many advantages in practice and that countries that have implemented these standards consider that they allow an increase in transparency and accountability.

Keywords

Introduction

Over the last few decades, there have been profound cultural changes in public sector entities. They have taken place in two fields: the theory of New Public Management (NPM) and the principles of good governance (Hood, 1995; Lapsley, 1999). NPM involves reducing the public sector through privatization, downsizing and reorganizing it with customer-oriented mechanisms, and adopting private sector management techniques to improve performance and accountability. The principles of good governance include openness, integrity and accountability (IFAC-PSC, 2001), which should be exercised with a focus on the organization's purpose and on the outcomes for citizens and service users (CIPFA, 2004).

This more open approach to good governance, together with the influence of NPM, has led to a consensus on the necessity of extending the accountability of public sector entities and reforming the language used. Accounting systems have been reformed in most countries to improve accountability and transparency and, at the same time, to restore citizens' trust in governments.

The depth of the reforms has been very varied, and, in most cases, they have been carried out at all levels: national, regional and local. In these processes of reform, the International Public Sector Accounting Standards (IPSASs) issued by the International Public Sector Accounting Standards Board (IPSASB) have played an important role (Adhikari and Mellemvik, 2010; Alesani et al., 2012; Bergmann, 2012; Gómez and Montesinos, 2012; Navarro and Rodríguez, 2007, 2011). In fact, a variety of international governmental organizations, such as the United Nations (UN), the Organisation for Economic Co-operation and Development (OECD) and the European Commission (Grossi and Soverchia, 2011), have committed substantial resources to the adoption of IPSASs, and a mimetic effect has emerged. Other international governmental organizations have directly promoted the adoption of IPSASs, such as the World Bank, International Monetary Fund (IMF), OECD and Asian Development Bank. Countries all around the world have carried out initiatives for adopting IPSASs (Christiaens et al., 2010, 2015; Jones and Caruana, 2014). However, only single-country studies have been carried out about the factors and effects of IPSASs adoption (Gómez and Montesinos, 2012; IPSASB, 2014a; Sour, 2012).

The objective of this article is to analyse the drivers and stimuli for countries to adopt IPSASs, as well as to identify the barriers that make the process difficult at the moment. Furthermore, we aim to show the reported benefits of IPSASs. Through a questionnaire answered by 19 European Union countries and 18 American continental countries, we empirically analyse the perceived benefits of IPSASs adoption by using a structural model based on the stimuli and barriers identified in our theoretical part. One of the main contributions of our study is that it includes American continental and European Union countries together and analyses both the stimuli for and barriers to the adoption of IPSASs and their importance for accountability purposes.

This article is structured as follows. After the introduction, we review the previous literature and identify the stimuli and barriers that will be used as variables in our empirical study. In the next section, the research model is outlined, describing the aims, propositions, data and method used. After that, we show the results obtained in the empirical analysis and discuss the main implications and conclusions.

The path for adopting IPSASs: stimuli and barriers

IPSASs aim to improve the quality of general purpose financial reporting by public sector entities, increasing transparency and accountability in the public sector and enhancing the comparability of financial statements around the world (IPSASB, 2014b). In this article, the benefits of IPSASs, with respect to local or national standards, for achieving the comparability of financial reporting is a key point as the adoption of IPSASs will lead to international harmonization of governmental accounting. The success of the IPSASB's efforts is dependent upon the recognition of and support for its work from many different interested groups acting within the limits of their own jurisdictions.

At the moment, many countries, as well as most international public organizations, have ongoing processes for adopting IPSASs. Using Humphrey et al.’s (2009) terminology, we can say that an international public sector accounting architecture has emerged, which refers to the framework and process that can help to attain the comparability of public sector accounting in the international arena. The approach to international harmonization and convergence can become a reality through the adoption of IPSASs at the national level. ‘Adoption’ can be defined as a process that implies the incorporation of the criteria of international standards in local regulation (Pacter, 2005). It assumes the coexistence of different sets of standards but with criteria ‘converging’ towards the same principles. This process can require step-by-step changes and an incremental approach (Bietenhader and Bergmann, 2010).

In such an approach, there are some variables and conditions that influence the process. Considering the contingency model (Lüder, 2002), we focus on the following contextual variables:

Stimuli: events that occur at the initial stage of the process and create a positive impact for the adoption of IPSASs by national governments. Adoption barriers: environmental conditions that create a negative impact on the process of adoption.

Stimuli for adopting IPSASs

Based on the analysis of official material, the web pages of the International Federation of Accountants (IFAC) and national standard-setters, and accounting literature, eight stimuli are identified for a national government's decision to adopt IPSASs: (1) the issuing process for the standards; (2) the closeness of IPSASs to business accounting standards; (3) the consideration of issues of particular significance to public sector entities; (4) the IPSASB's active role; (5) the international governmental organizations' role; (6) the sovereign debt crisis and IPSASs; (7) the global perspective and the awareness of the importance of international accounting harmonization; and (8) the harmonization of financial reporting with national and statistical information.

The issuing process for the standards

The process of issuing IPSASs can itself be considered an important factor in the legitimization process. Before standards are approved, it is usual to hold a public consultation with the aim of gathering opinions and views from stakeholders. The most recent consultation was about IPSASB strategy and governance (IPSASB, 2014b, 2014c).

In its origins, the IFAC Public Sector Committee (IFAC-PSC), later renamed the International Public Sector Accounting Standards Board (IPSASB), published not only the standards, but also studies and research reports in order to interest many actors in public sector reform. At the moment, the IPSASB issues recommended practice guidelines (RPG) that represent good practice that public sector entities are encouraged to follow.

Furthermore, the IPSASB adapts the standard setting to the needs of different environments (IPSASB, 2014c), trying to address the issues of greatest concern to public sector entities in the international context. Examples of this are the projects carried out recently: reporting service performance information; service concession arrangements; and reporting on financial sustainability.

The closeness of IPSASs to business accounting

From the beginning, the IFAC-PSC chose the business accounting model as a reference, considering that the financial reporting of public administrations can be prepared with the same criteria as those for business entities. Therefore, since their origins, the standards have been based on the International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), with the required adjustments to adapt them to the public sector context. The aim is not to divide efforts, but to focus them on a single set of pronouncements with common roots with the standards issued by the International Accounting Standards Board (IASB).

Another positive output is that big public administration audit and consultancy firms have most of their technical, organizational and cultural background in the business enterprise field. As a consequence, these firms clearly tend towards business accounting standards as the basic reference and framework for public sector entities (Christensen and Skaerbaek, 2010).

This has helped some countries to adapt their public sector systems to IPSASs because what they have really done is to apply IFRS to both the business and public sector entities as their tradition has been marked by not setting specific rules for the public sector. The result is that the final rules applicable to public sector entities are consistent with IPSASs in many countries. Australia, New Zealand and the UK can be mentioned as examples.

In Australia, the Australian Accounting Standards Board (AASB) has issued Australian equivalents to the IFRS (A-IFRS), with certain amendments to the IASB pronouncements that apply to public sector reporting. New Zealand initially took the same approach of adopting IFRS with some public sector amendments, but this has been superseded by a New Zealand version of IPSASs. In the UK, standards are contained in the Financial Reporting Guidance for the UK public sector, an IFRS-based accounting guidance, but broadly consistent with IPSASs.

At the same time, IPSASs can take advantage of European Union support for IFRS (Brusca et al., 2013). In fact, an important development that brought many actors close to the IPSASB vision of adopting international standards was the decision of the European Union to require listed companies in its member states to report with IFRS in 2005. As Christiaens et al. (2010) state, a number of jurisdictions do not adopt IPSASs because they transfer their own local business accounting standards to the public sector. If they are based on IFRS, they will eventually be compatible with IPSASs.

The consideration of issues of particular significance to public sector entities

Originally, these IPSASs clearly transferred the generally accepted accounting principles of business accounting to public sector accounting. However, there are many critics, both academics and professionals, who think that public administrations have characteristics that may require care in adapting accounting systems to those of business (Ellwood and Newberry, 2007; Newberry, 2014). Recognizing this, in 2002, the IFAC-PSC initiated the second phase of the standards programme, addressing issues of particular significance to the public sector, such as accounting for the social policies of government and accounting for non-exchange revenue (Bergmann, 2013).

We can also mention the weight that budgetary systems have in the public sector, in particular, in European continental countries (Jones et al., 2013), with the result that the accounting models focus on the budget. The IPSASB quickly realized the difficulties that this could imply and introduced budget issues: IPSAS 24, ‘Presentation of budget information in financial statements’, dealing with budget reporting, was issued. Another important milestone is the IPSASB conceptual framework for public sector accounting, which contains the concepts, definitions and principles that underpin the development of IPSASs (IPSASB, 2014d).

The IPSASB's active role

The IPSASB is developing an active policy for promoting IPSASs and interesting national governments and international institutions in IPSASs. Examples of this active role are seen in the agenda published continuously by the IPSASB with many presentations and speeches to engage stakeholders, such as participation in European Public Sector Accounting Standards (EPSAS) Task Force meetings and presentations in Korea, Japan, Germany and London, among others.

First, the IPSASB encourages countries to adopt IPSASs. Second, the IPSASB adopted very early on an active policy for the diffusion of IPSASs, translating them into many languages, including Spanish since 2005 (IPSASB, 2013) and French. Third, the IPSASB cooperates to the greatest possible degree with national standard-setters in preparing and issuing standards, with a view to sharing resources.

The IPSASB also encourages debate with users, including: elected and appointed representatives – treasuries, ministries of finance and similar authoritative bodies; and practitioners throughout the world – with the aim of identifying user needs for new standards and guidance.

The international governmental organizations' role

International governmental organizations have played an important role through two different complementary policies: promoting the adoption of IPSASs and setting examples. The adoption of IPSASs has been encouraged by the World Bank (2004), the IMF and the OECD as part of their recommendations to improve the accountability and transparency of public sector entities. The World Bank and IMF cooperate actively through their financial assistance and capacity development programmes (PwC, 2013).

The first starting point for the legitimization of IPSASs has been their adoption by international organizations. For example, the OECD, the European Commission, the North Atlantic Treaty Organization (NATO), the UN, the Council of Europe and the International Criminal Police Organization (INTERPOL) have all adopted IPSASs. The adoption of IPSASs by international financial, economic and political institutions means that they have become a clear and useful reference when requesting faithful financial information from countries and public sector entities.

The sovereign debt crisis and IPSASs: the European Union developments

The global financial crisis and the consequent sovereign debt crisis have also raised several public sector accounting issues. Many governments have important deficits and high debt levels and their control has been fixed as a primary objective for most national governments. Moreover, the financial crisis has created distrust and increased the need for accountability and transparency in the public sector.

In the European Union, the crisis made it even more important to obtain comparable deficit and debt data for all the member states. Eurostat is the Statistical Office of the European Union, responsible for providing the European Union with statistics that enable comparisons between countries and regions, using to this end the European System of Accounts (ESA). ESA provides the macro-level statistical accounting framework for the government and non-government sectors in the European Union and is accruals-based. ESA-based government debt and deficit data for the purposes of the Excessive Deficit Procedure are the result of consolidating the individual accounts of general government entities in the member states (European Commission, 2013b). In this sense, as Jones and Caruana (2014) state, the function of ESA is very different to IPSASs or other financial reporting standards that are directed towards the accountability and transparency of an entity (micro-accounting level).

With the crisis, the European Commission has become aware that the system for fiscal statistics has not sufficiently mitigated the risk of substandard quality data being notified to Eurostat. An improvement in this situation requires the existence and quality of comparable and coherent upstream accruals data at micro-accounting level (European Commission, 2013b; Lüder, 2000).

The introduction of modern and comparable micro-accounting systems has been dealt with by the European Union over the last two years. In 2012, Eurostat issued a public consultation on the suitability of IPSASs for European Union member states, later publishing the report ‘Towards implementing harmonised public sector accounting standards in member states. The suitability of IPSASs for the member states’ (European Commission, 2013b). The European Commission (2013b: 8) considers that IPSASs as they currently stand cannot easily be implemented, and that it is preferable to develop European Union standards based on IPSASs (renaming them EPSAS). EPSAS could initially be based on a set of key IPSASs principles and use IPSASs that were commonly agreed by member states. EPSAS, however, should not regard IPSASs as a constraint for the development of its own standards. At present, this initiative is under debate in the literature (Mussari, 2014).

The global perspective and the awareness of the importance of international accounting harmonization in the public sector

In a world of globalization, different professionals and academics are becoming aware of the importance of accounting harmonization in the public sector (Benito et al., 2007; Christiaens et al., 2010). Even though the harmonization of public sector accounting could be considered less important than that of business sector accounting, the market for government bonds could benefit from comparable financial information. Furthermore, comparable information is required to evaluate compliance with international treaties, such as the Treaty of the European Union, in particular, the Maastricht Treaty.

A path towards the harmonization of financial reporting with national and statistical information

Another stimulus may be the harmonization between micro- and macro-information, currently considered as an objective. In fact, many standard-setters are making efforts in this direction. One example is the IPSASB itself, which published in 2012 the consultation paper IPSASs and Government Finance Statistics Reporting Guidelines, directed at helping to reduce differences between Government Finance Statistics (GFS) reporting guidelines and IPSASs. The aim is to support governments' use of integrated financial information systems that can generate both IPSASs financial statements and GFS reports. In 2014, the IPSASB issued a policy paper titled Process for Considering GFS Reporting Guidelines during Development of IPSASs (IPSASB, 2014e), whose objective is to set out the IPSASB's process for considering statistics reporting guidelines during the development of IPSASs.

Barriers to adopting IPSASs

There are also some barriers that threaten IPSASs adoption, including criticisms received because of their closeness to the business accounting model, the interest of countries in maintaining control and fiscal illusion, the cost and training needs for the adoption of the IPSASs, and concerns about IPSASB governance.

The closeness of IPSASs to the business accounting model

The adoption of the business accounting model by the public sector has been criticized in the literature. This was, in fact, one of the main criticisms in the answers to the public consultation of the European Union (European Commission, 2013a). Some answers highlight the incompleteness of IPSASs with respect to public sector accounting requirements (e.g. with regard to taxation and social benefits). As mentioned earlier, in an attempt to deal with this question, the IPSASB has developed a specific conceptual framework for public sector entities.

Another criticism that has emerged is that IPSASs do not specifically analyse the budgetary particularities of the public administration, and only mention that budgetary information can be included in the financial report. This contrasts with the importance of the budget in some countries and can even be a risk to the adoption of IPSASs in countries where the budget is the cornerstone of the accounting system, as in the case of Finland (Oulasvirta, 2014). Finally, the inclusion of fair value as a measurement criterion for the public sector, which is difficult to calculate, is also being debated (Oulasvirta, 2014).

Maintaining control and fiscal illusion

The interest of countries in maintaining control over the process of standardization with a deep-rooted nationalism, whereby each country considers its accounting system the most adequate, can be another barrier for IPSASs adoption. Furthermore, financial reporting has an important impact on financial sustainability, as debt and deficit can be undervalued (Koen and Van den Noord, 2005), and consolidation and guarantees are two key issues (Bergmann, 2014). Hence, governments can desire to control accounting standards in order to maintain fiscal illusions as accounting devices can give the illusion of change, or make the change appear larger than it actually is (Irwin, 2012).

The cost and training needs for IPSASs adoption

The adoption of new accounting standards requires resources for the project and political support. Investments in information technology (IT) systems and in training for the new systems are necessary (PwC, 2014). This can be a barrier in many countries, especially in a time of budgetary constraints.

Access to supportive expertise and training is variable as there are many countries where civil servants and politicians have not even experimented with accrual accounting. IPSASs adoption will require a process and support for the acquisition of professional expertise and training for the people involved with the new systems.

Concerns about IPSASB governance

The consultation process carried out by Eurostat found that concerns about the governance and oversight of the IPSASB are among the reasons that national authorities mention for not adopting IPSASs (European Commission, 2013a). Trying to respond to these criticisms, in January 2014, an independent review group, chaired by representatives from the IMF, OECD and the World Bank, issued a public consultation on the future governance of the IPSASB in order to resolve the questions related to its governance (IPSASB, 2014c).

Research model

Aims and propositions

The aim of this empirical study is to analyse the stimuli for and barriers to the adoption of IPSASs in American and European Union countries and to consider to what extent these can influence the benefits that countries see in the process in terms of the modernization and harmonization of governmental accounting. To that end, we identify the level of IPSASs adoption in the countries analysed.

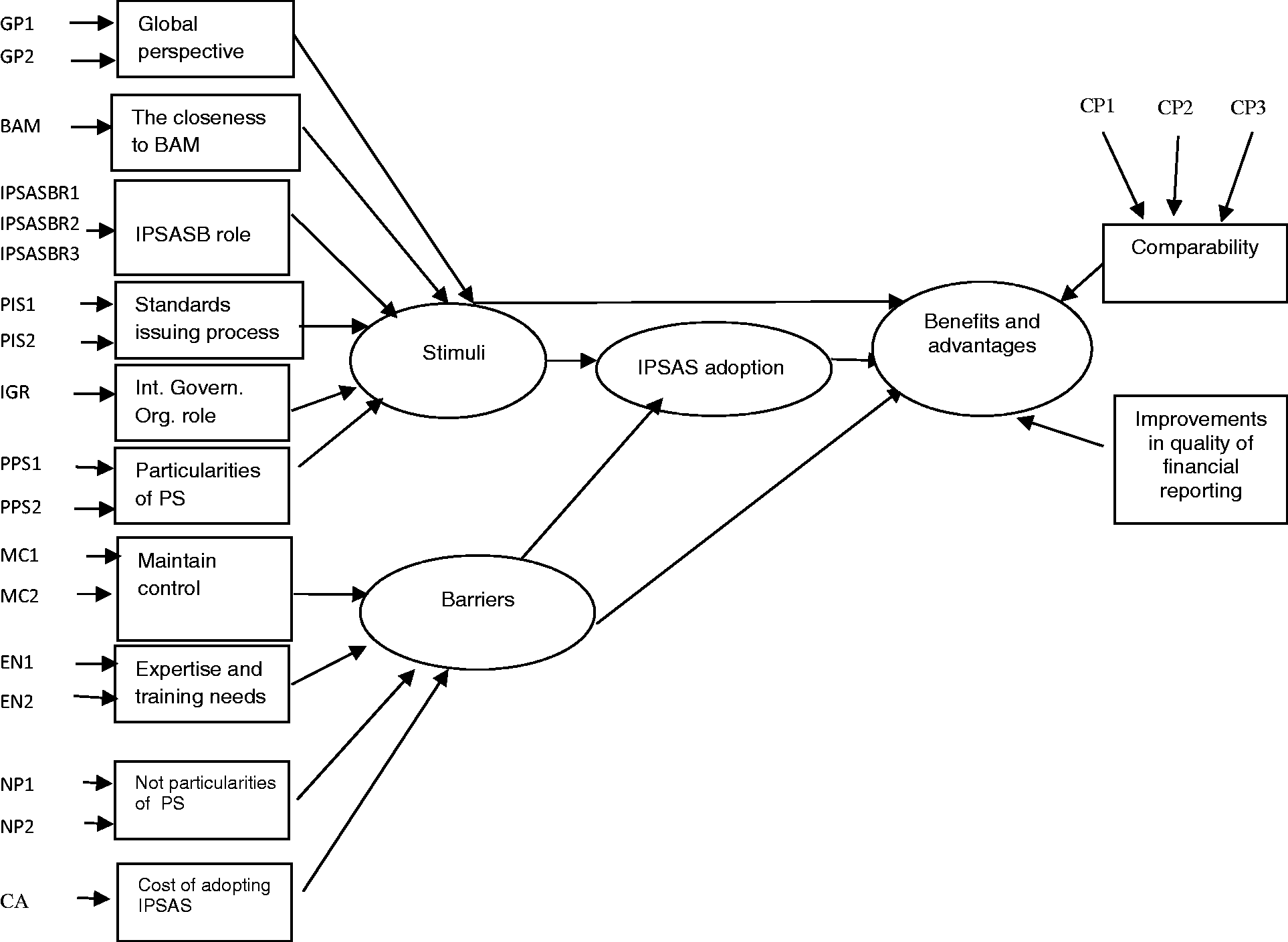

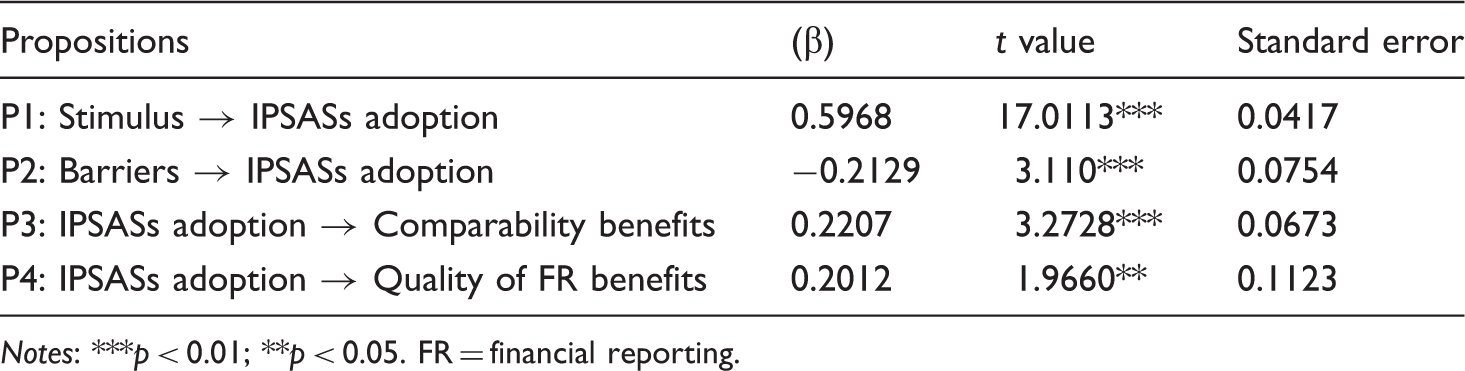

Considering previous literature and the objectives of the article, we have defined the following propositions to be tested empirically: P1: The perceived relevance of the stimulus has a positive effect on the adoption of IPSASs. P2: The perceived relevance of the barriers has a negative effect on the adoption of IPSASs. P3: IPSASs adoption has a positive effect on the perceived benefits of IPSASs in terms of the comparability of information. P4: IPSASs adoption has a positive effect on the perceived benefits of IPSASs in terms of improvements in the quality of financial reporting, increasing transparency and accountability, which allows for the modernization of accounting systems. Variables included in the study. Structure of the research model.

Data and method

We have obtained the data for our study through a research questionnaire sent to accounting officials in charge of central government financial reporting. For countries that did not answer the questionnaire, we sent it to an academic expert in the field in the corresponding country. Between November 2012 and February 2013, the questionnaire was emailed to the 28 European Union countries and to the 23 American continental countries and could be answered online. The questionnaire refers to central government accounting systems.

We received 19 answers from the European Union countries (65% from accounting officials in charge of central government financial reporting and 35% from academics). From the American continental countries, we received 18 replies (83.33% from accounting officials in charge of central government financial reporting and 16.66% from academics).

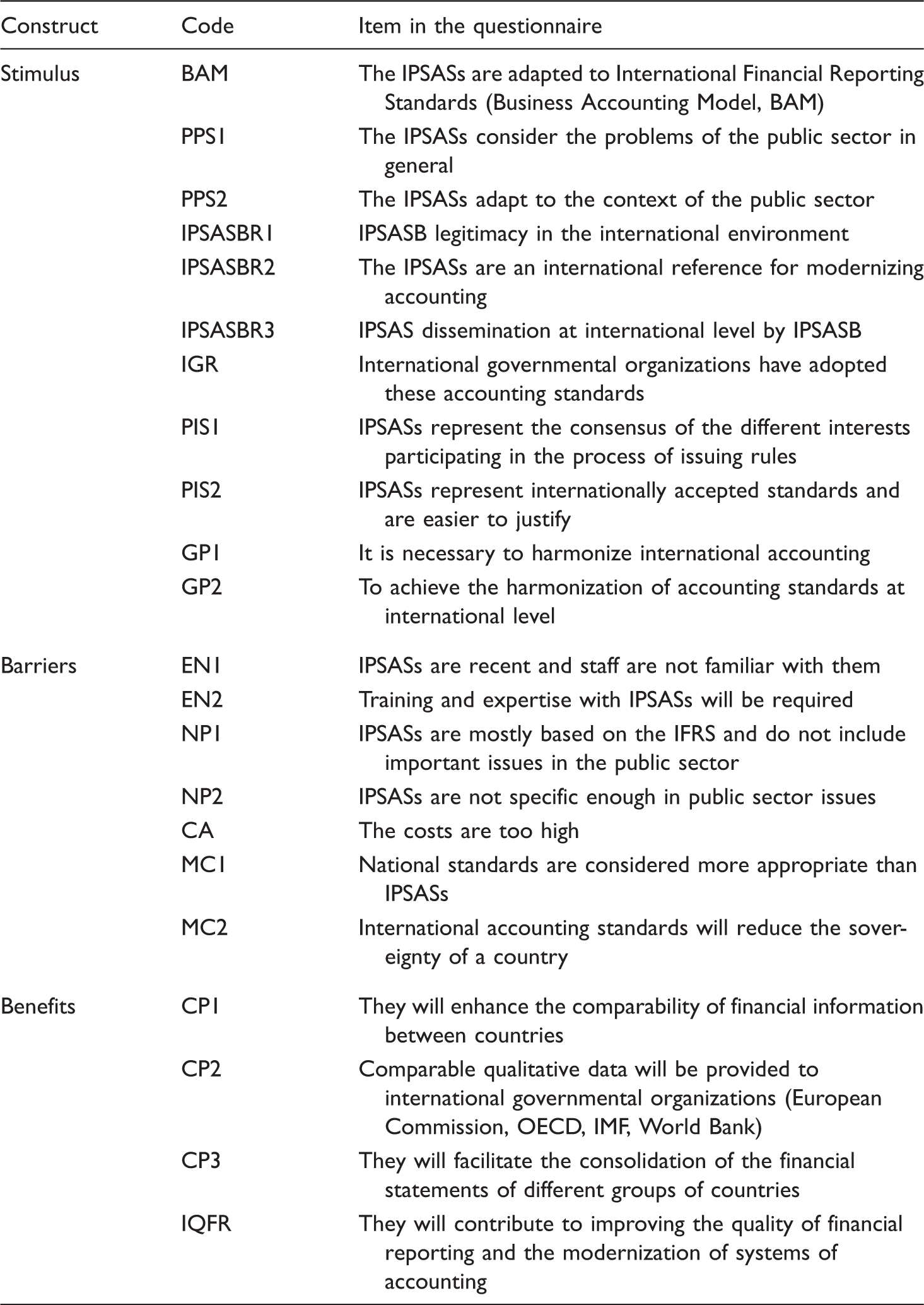

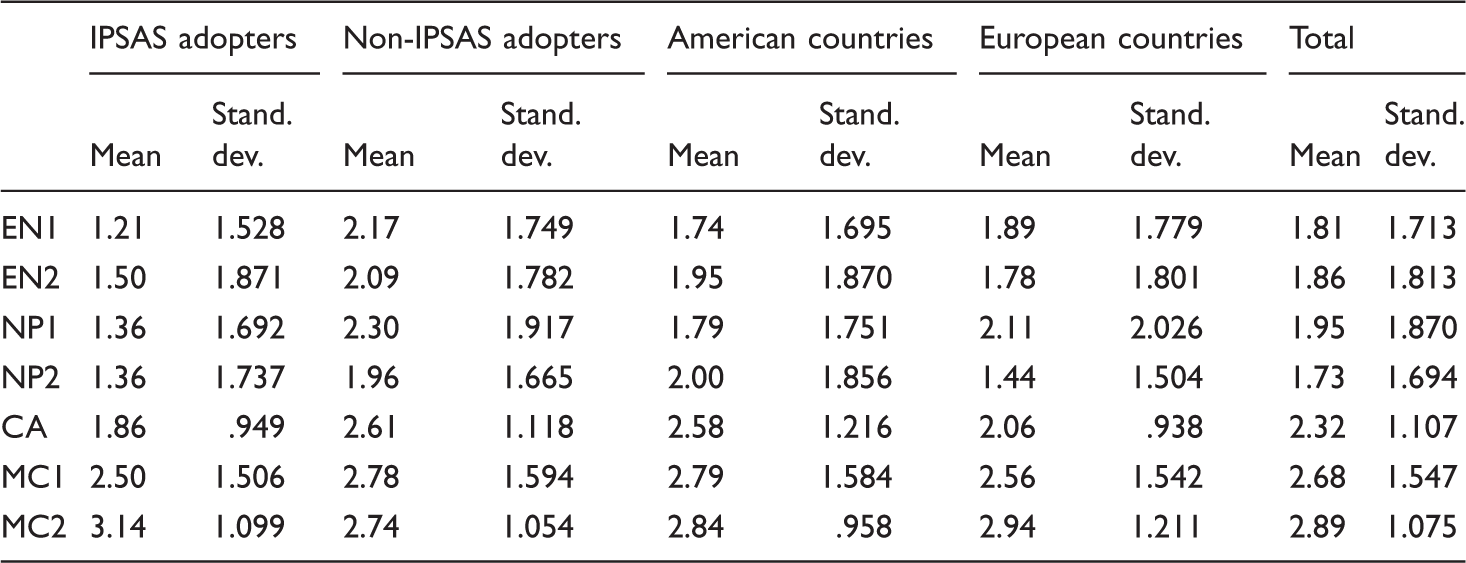

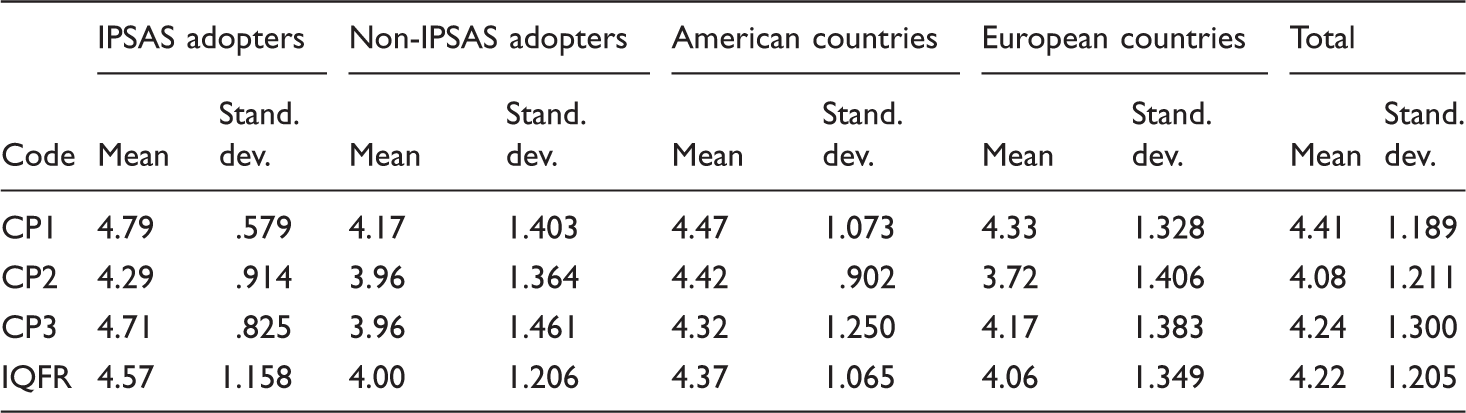

The first step has been to analyse the level of adoption of IPSASs in the countries of the sample, considering that there is no consensus in the literature. To do so, we included a question in the survey. In the case of the European countries, we have also used the studies of PwC (2014) and Ernst and Young (2012) to check that there are no potentially conflicting results. When we had doubts about the answers, we checked them in the literature or with academic experts in the field in the corresponding country. On the basis of the questionnaire, we have defined the variables of stimuli, barriers and benefits included in Table 1, using a Likert-type scale for the responses (1 to 5).

The method used in the article is structural equation modelling (SEM). SEM is a multivariate method of analysis that allows the analysis of causal relationships between variables using multiple regression analyses. One of the strengths of SEM is the ability to construct latent variables or constructs, which are variables that are not directly measurable but can be estimated through measured variables. It allows multiple measures to be associated with a single latent construct. In our case, using the items of the questionnaire contained in Table 1, we constructed three latent variables: stimuli for, barriers to and benefits of IPSASs adoption.

SEM combines the structural model and the measurement model. The first shows whether the observed variables are good indicators of the latent variables, and the second describes the relationships between latent variables only. One important advantage is that within the model, a construct can function as a dependent variable and as an independent variable.

We use the partial least-squares SEM (PLS-SEM) included in the software SmartPLS 2.0. PLS-SEM has the advantage of being able to estimate even small samples correctly and has been considered suitable to reflect formatively measured constructs and to identify successful relationships between constructs (Hair et al., 2012).

Analysis of results

Exploratory analysis

Adoption of IPSASs in European Union and American countries.

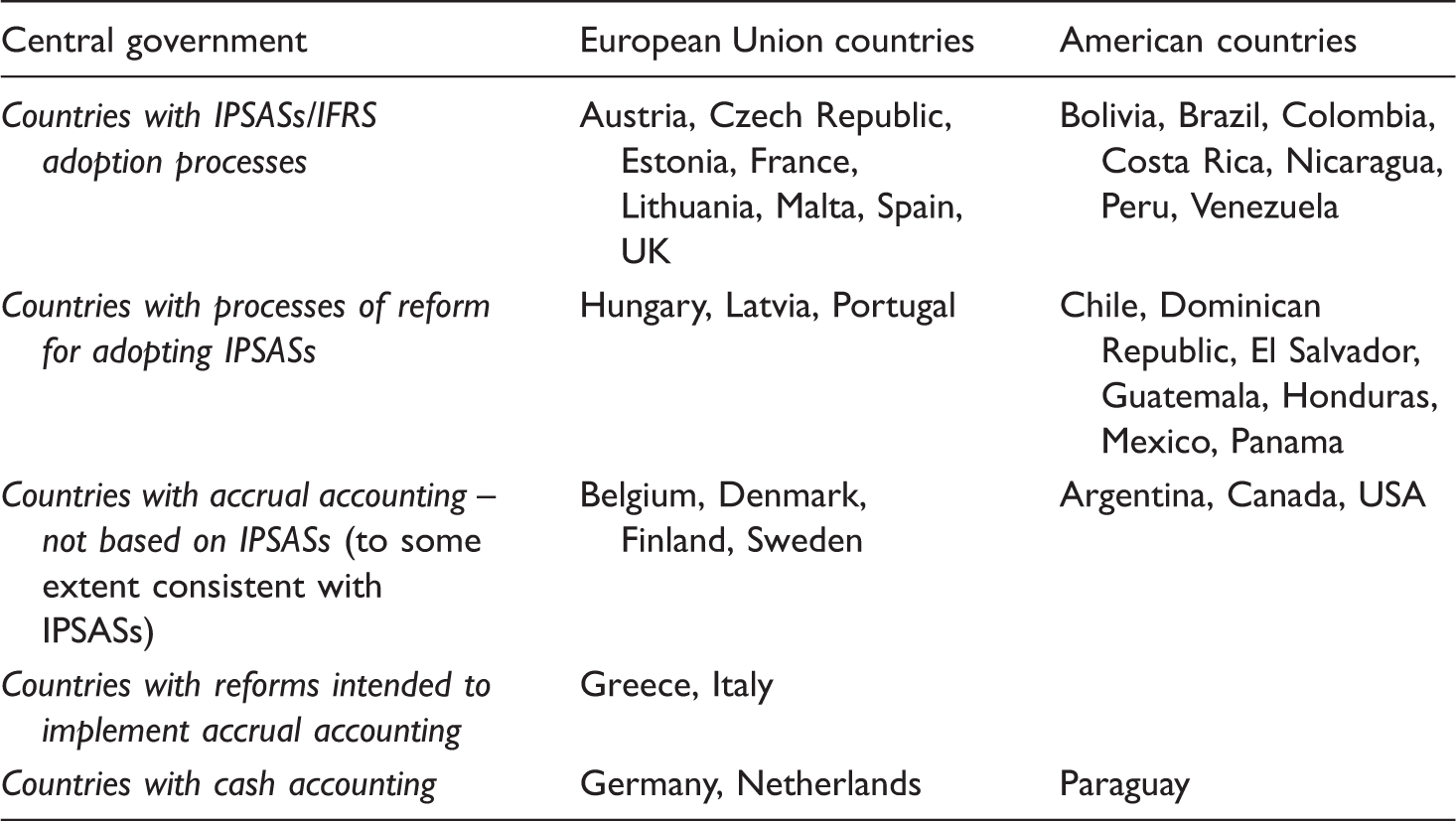

The IPSASs have been adopted in eight European Union countries and there are three more that have started a process of reforming governmental accounting and have considered IPSASs as their reference. There are four countries that maintain an accrual accounting system, sometimes similar to business accounting and with some similarities with IPSASs (PwC, 2014) but that cannot be said to be IPSAS-based. For example, in Sweden, the Swedish Financial Management Authority (ESV, 2012) explains that, to quite a substantial extent, the rules correspond to the IPSASs regarding principles and definitions but that there is room in certain areas for further adjustment of the rules to adapt them to the IPSASs.

There are four countries that, at present, use cash accounting – Germany, the Netherlands, Italy and Greece – although two of them have initiated reforms for using accrual accounting (Italy and Greece). In Germany, the reforms started in 2006, but for the moment, they have been abandoned (Jones and Lüder, 2011).

In a similar way, there are seven American continental countries defined as IPSASs followers and another seven that have initiated a process of reform towards the adoption of IPSASs. Only three American continental countries apply accrual accounting but their accounting standards are not based on IPSASs. In the American continent, only Paraguay uses cash accounting in practice, although legal rules include a modified accrual system.

To sum up, it appears that the recommendations of international governmental organizations and the efforts of the IPSASB to persuade countries to adopt the IPSASs are beginning to bear fruit. These standards have played an important role in the reforms of central governments of the European Union and American continental countries. This is especially true in the case of Latin American countries that see IPSASs as a tool for implementing accrual accounting in the public sector, as in Honduras, which uses cash accounting but plans to introduce accrual through the adoption of IPSASs.

Stimuli for and barriers to adopting IPSASs

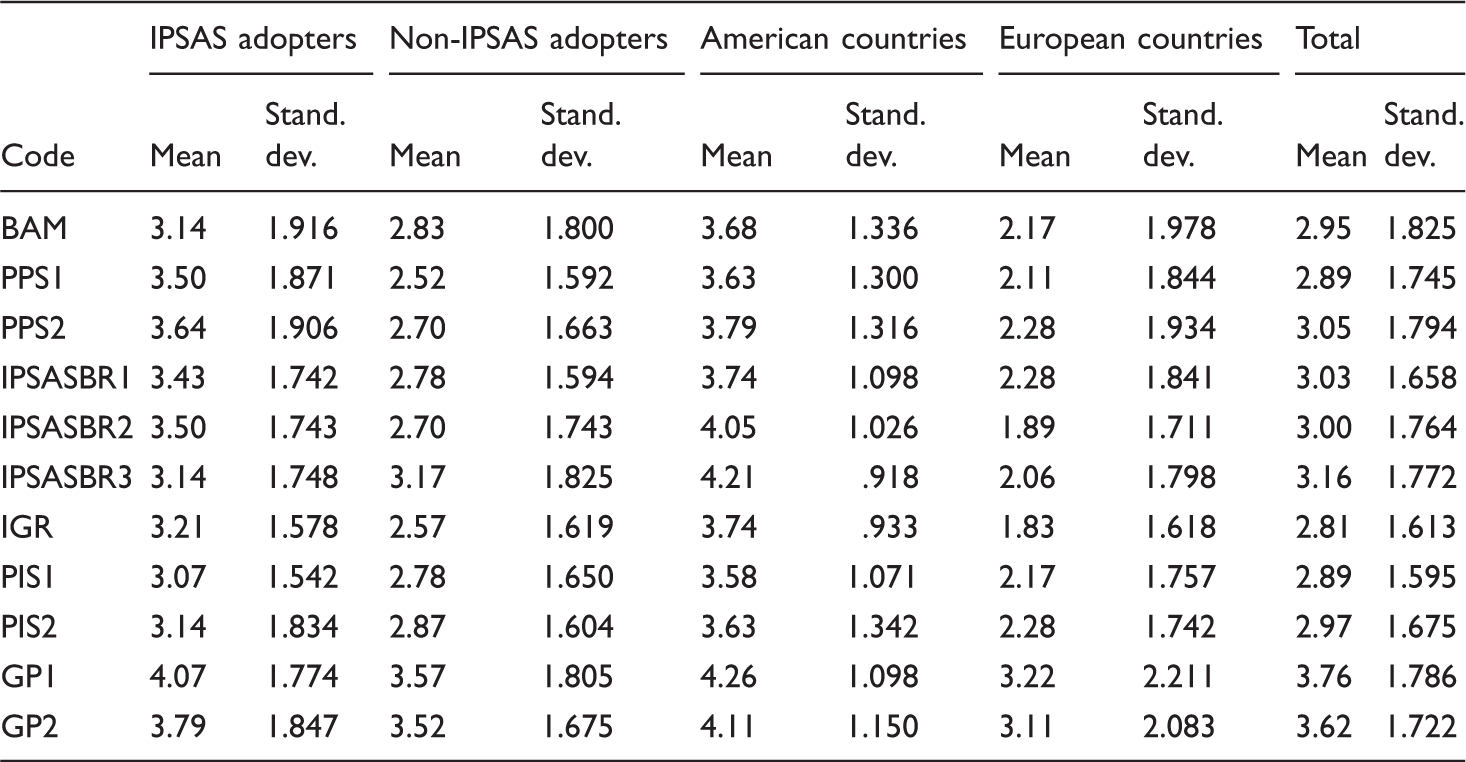

Stimuli for adopting the IPSASs.

Most of the participants agree on the importance of achieving international harmonization and consider that this is an important factor for countries adopting IPSASs (GP1 and GP2 variables). The analysis shows that all the stimuli have a higher value for adopter countries than for non-adopters. The stimuli are perceived as more important by American countries than by European Union countries. In fact, European Union countries value the harmonization of international accounting in the public sector less than the American countries.

IPSASs adopters believe that IPSASs consider the problems and adapt to the public sector context (PPS1 and PPS2), and American countries give higher values than the European countries. Most IPSASs adopters consider them an international reference for modernizing accounting (IPSASBR2), and this is especially true for American countries.

The adoption of IPSASs by international governmental organizations (IGR) has been another stimulus for countries and many consider that IPSASs have gained international legitimacy and that their adoption is easier to justify (IPSASBR1). There are no important differences between adopters and non-adopters with respect to the relevance of IPSASs dissemination by the IPSASB at the international level (IPSASBR3), although this item is more valued by American countries.

The similarities between IPSASs and IFRS is another positive factor for IPSASs adopters (BAM variable), especially in American countries. The IPSASB has taken advantage of IASB legitimacy, although this orientation has been heavily criticized in the literature.

Barriers to adopting IPSASs.

The cost of adopting the IPSASs (CA) is also considered a barrier, mainly in non-adopter countries and in American countries. There are also some respondents who consider that IPSASs are based on IFRS (NP1) and that some public sector particularities are missing (NP2), especially in the group of non-adopters, but the means are only of 1.95 and 1.73 for the total responses. The lack of familiarity with IPSASs because they are recent (EN1) and the need for training and expertise with IPSASs (EN2) are not important barriers to adopting IPSASs given that the mean values of the variables are 1.81 and 1.86, respectively.

Benefits of adopting the IPSASs

The advantages of IPSASs in practice.

SEM

Cronbach's alpha, composite reliability and AVE.

Structural model.

Notes: ***p < 0.01; **p < 0.05. FR = financial reporting.

These results show that the stimuli are positive factors in the adoption of IPSASs (β = 0.5968; p < 0.01). However, the barriers negatively affect their adoption (β = −0.2129; p < 0.01). We also find that the adoption of IPSASs has a positive effect on the perceived benefits of the IPSASs, both in the comparability of financial reporting between different countries and in the improvements of the quality of financial reporting, and hence in transparency and accountability.

Conclusions

Accountability and transparency are considered to be essential for restoring citizen trust in governments, and to achieve them, modern accounting systems are necessary. The idea of modernizing governmental accounting has spread around the world. Both in European Union and in American countries, governments are aware of the importance of modern accounting systems. In spite of the criticisms received (Lapsley et al., 2009; Newberry, 2014), accrual accounting has been gaining ground in public sector accounting systems and currently only a few countries maintain the cash accounting system.

In modernizing their systems, governments may find stimuli to adopt IPSASs, but there are also some barriers that can hinder the process. Of a total of 37 countries, 15 have adopted IPSASs (eight in the European Union and seven in the American continental countries), and there are three European Union and seven American countries with intentions of carrying out IPSASs-like reforms. In the European Union, there are four countries that apply accrual accounting but without plans to adapt their accounting systems to IPSASs, while only three American countries are in the same situation, including Canada and the US. The accounting systems in these countries are, to a certain extent, consistent with IPSASs, as we have mentioned for the case of Sweden.

At the same time, four European Union countries maintain cash or modified cash basis accounting, while only one American country is in this situation. Paraguay has the intention of moving to accrual accounting, as do two countries from the European Union: Greece and Italy.

The stimuli for adopting IPSASs are perceived as more relevant by adopter countries than by non-adopters. The latter do not give so much importance to the need for harmonizing public sector accounting or to the adaptation of IPSASs to public sector particularities. It appears that American countries give more importance to the harmonization of public sector accounting even though there are no efforts for inter-country comparison of organizations similar to the European Union. For example, there is no Mercosul programme of harmonization, although the World Bank's support of IPSASs can act as a push factor towards the harmonization of public sector accounting. The participants in this study consider that IPSASs are an international reference for modernizing accounting. The interest of countries in maintaining control, the consideration that national standards are more appropriate than IPSASs and the cost of adoption are the main barriers.

The structural model confirms that the indicators selected to measure the stimuli and barriers and our propositions are adequate. The stimuli have a positive effect on IPSASs adoption while the barriers have a negative impact on adopting IPSASs.

The most important finding in this study is that both adopters and non-adopters value the benefits of IPSASs for achieving international comparability and for improving the quality of financial reporting systems. Countries in the study consider that the adoption of IPSASs has really allowed an increase in transparency and accountability. The structural model allows us to confirm the effect of IPSASs adoption on the perceived benefits of IPSASs.

The European Union has become aware of the importance of modernizing the accounting systems of its member countries, and of harmonizing them. Another criticism of IPSASs is their flexibility and the different alternatives they offer. These reasons have led the European Commission to develop its own standards, the EPSAS, a European version of IPSASs (European Commission, 2013b). This will be the path for harmonizing the accounting systems of European Union countries. EPSAS will be based on IPSASs, which is another proof of the efficacy and legitimacy of IPSASs for modernizing and harmonizing governmental accounting.

Footnotes

Acknowledgements

This research was carried out with financial support from the European Social Fund and the Regional Government of Aragón-Spain (Research group CEMBE) and from the Regional Government of Andalusia-Spain (Research projects SEJ 6628 and SEJ-7700).