Abstract

Comparing Italy and Sweden, which are countries with different cultural and accounting traditions, this article focuses on the characteristics of their standard-setting processes for the public sector in order to evaluate their prerequisites for international harmonization. The recent attempt by European bodies to stimulate an international public sector accounting harmonization process, the European Public Sector Accounting Standards programme, requires that each country involved in the process assumes its position, taking into account a number of national factors and conditions. To this end, the research identifies the potential positive factors of a national public sector accounting standard-setting context that are favourable to international harmonization. While both countries differ in some respects, the study discusses how the ideal prerequisites can constitute a positive environment in which to implement international harmonization in the European context.

This comparative study identifies conditions to enhance an efficient and reliable national standard-setting process, summarizing the potential positive factors investigated in both countries. It argues that institutional arrangements and specific governance factors (a flexible legal system, efficient auditing, vertical harmonization, an inclusive and participative standard-setting process, and the maturity of accrual accounting) can support key actors in the public sector to react positively to international harmonization, with some emerging scepticism regarding the European Public Sector Accounting Standards programme.

Keywords

Introduction

Over the last three decades, the topic of international public sector accounting (PSA) harmonization has attracted increasing attention in the literature, while European countries have substantially maintained heterogeneous PSA systems (Brusca et al., 2018, Caruana et al., 2019; Christiaens et al., 2015). In addition, the diffusion of International Public Sector Accounting Standards (IPSAS) and the latest European Public Sector Accounting Standards (EPSAS) programme have become a topic of interest because of their potential impact among national networks (Brusca and Martínez, 2016; Jorge et al., 2019a, 2019b; Manes Rossi et al., 2016; Mussari, 2014).

With the aim of harmonizing member states’ PSA systems, the EPSAS programme has been stimulating governments, professionals, academic networks and international organizations of different fields in a debate that involves a number of technical, organizational and governance aspects (Caruana et al., 2019; Jorge et al., 2019a). The discussion is mainly focused on the advantages and disadvantages of the process from an international perspective. The potential convergence of government accounting, budgetary accounting and national accounts systems under accrual principles for the macroeconomic surveillance of and better comparability among accounting numbers across countries in order to generally improve the governance of European Union (EU) bodies are the main controversial areas where the discussion is centred (Caruana et al., 2019). Also, national governments continue to reform their PSA systems at all levels in the search for innovations and reliable data, even if technical difficulties, the accounting environment, the legal system and traditions affect the output and the effective success of these reforms (Christiaens et al., 2015; Jorge et al., 2019b; Manes Rossi et al., 2016).

The fact that EU member states can come to an agreement is not taken for granted because the EPSAS programme could require a reshaping of national standard-setting processes (Brusca et al., 2018). Indeed, the uncertainty around the final output has stimulated a debate on how countries have been approaching the EPSAS programme during the process, which, according to Manes Rossi et al. (2016: 720), deserves ‘further attention and possibly empirical studies to test their actual pros and cons’.

Therefore, this article aims to contribute to the debate on accounting harmonization by focusing on national PSA standard-setting contexts. By investigating two national cases to evaluate their prerequisites for change and attitudes to harmonization, the article focuses on the following research question: what are the potential positive factors of a national PSA standard-setting context that are favourable to international harmonization?

The question follows the need for more research on the systematic analysis of national settings, targeting the technical, organizational and governance issues of their PSA standard-setting contexts (Carnegie and Napier, 2017; Manes Rossi et al., 2016). The national cases concern Italy and Sweden, which were chosen because of their different cultural backgrounds, models of regulation and PSA systems (EC, 2018; Manes Rossi, 2015; Tagesson and Grossi, 2015) in order to answer the growing demand for comparative studies of PSA, covering countries at different levels of socio-economic and political development (Benito et al., 2007).

The remainder of this article comprises the following parts. The second section presents the analytical model that is developed to analyse the two country cases. The third section explains the research design. After the definition of the international stimuli of accounting harmonization in the fourth section, the comparative case study is developed in the fifth, sixth and seventh sections to point out country-specific factors. The article is concluded in the eighth section, which discusses the results, contributions and limitations of the research.

Theoretical background: an analytical model of national PSA standard-setting contexts

National accounting standard-setting processes are embedded (i.e. institutionalized) within national borders as a result of the interplay of national traditions and specific social-cultural factors (Dacin and Dacin, 2008; Lüder, 2002). The so-called process of the institutionalization of PSA is very slow, which is a result of decades of the sedimentation of administrative, legal and accounting traditions. Generally, the literature has remarked that national actors and organizations have a stake in preserving the status quo, manifesting a potential negative reaction to a proposed international reform (Dacin and Dacin, 2008).

Based on these considerations, an analytical model has been derived from conclusions drawn from previous studies of accounting systems and organizational change (e.g. Lüder, 2002; Palthe, 2014) to answer to the research question. The model takes into account technical, organizational and governance aspects that can determine the attitude of a country towards international harmonization.

Nowadays, the international scenario, that is, the EU, the United Nations (UN), the Organisation for Economic Co-operation and Development (OECD), multinational accounting firms (e.g. the Big Four) and financial operators, with their various roles and networks, stimulates the implementation of harmonization programmes for the advantages of reducing transaction costs and creating potential improvements in the comparability of information (Oulasvirta, 2014). These stimuli can interact to encourage national systems to implement a proposed change of international PSA harmonization.

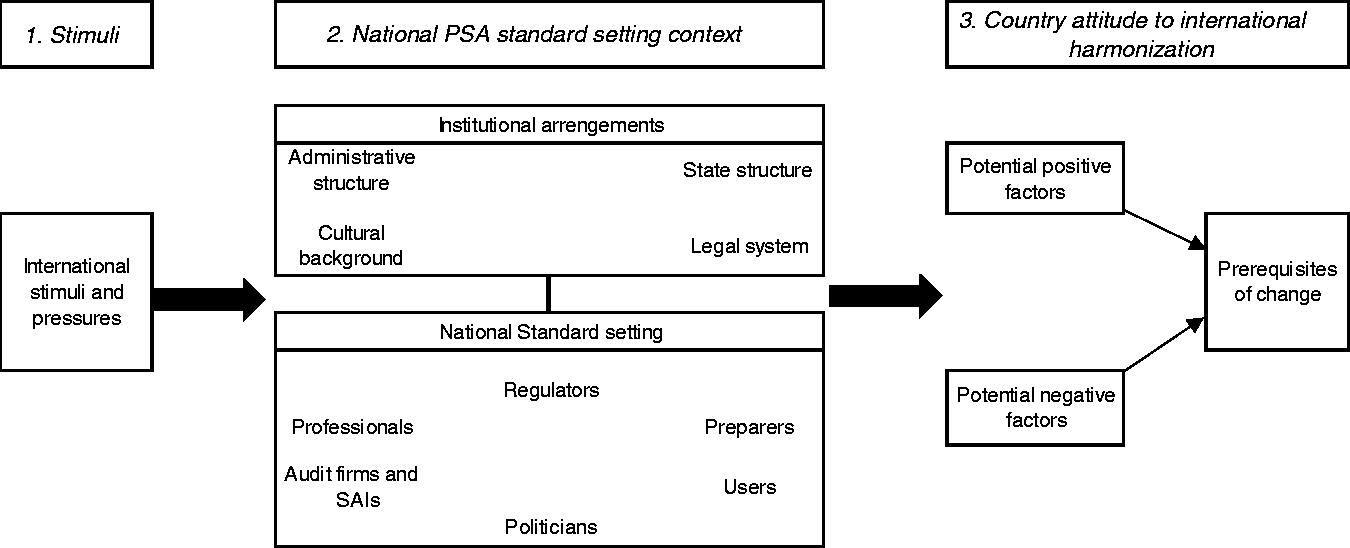

According to Vela and Fuertes (2000) and Lüder (2002), the national PSA standard-setting context is composed of institutional arrangements and a network of actors. Institutional arrangements concern the administrative structure, cultural background, legal system and structure of the state. The second element consists of the various actors in PSA acting in the national setting. In this regard, Kwok and Sharp (2005) defined four main groups of stakeholders: national regulators of accounting standards; independent public accountants; financial statement users; and preparers.

It can be argued that national regulators and standard setters are connected with other actors who can influence the success or failure of a change process. Christensen (2002) distinguishes three types of relevant change actors, namely, those who promote the change process (consultants, commentators, academics and organizations representing professional interests), those who use accounting information (ministers, political advisors, opposition members, auditors, public accounts committees and parliamentary committees) and those who produce the accounting information (central agencies, managers of agencies and public sector accountants). Oulasvirta (2014) explains that preparers generally assume negative behaviours in an accounting change process because this also entails a change in their habits and requires reinventing day-to-day work. In recent decades, this fact has particularly been demonstrated in the adoption of accrual accounting (Jones and Caruana, 2016; Marty et al., 2006).

Figure 1 represents the interplay of the factors described in a process of proposed international PSA harmonization. Key national actors of the national standard-setting context are summarized into six categories: (1) professionals; (2) Supreme Audit Institutions (SAIs); (3) preparers; (4) users; (5) politicians; and (6) regulators.

Analytical model of national PSA standard-setting contexts.

The interplay among networks and institutional arrangements determines the emergence of factors that foster (i.e. potential positive factors) or hinder (i.e. potential negative factors) change. On the one hand, potential positive factors are elements of the national context that are expected to allow or support the internationally proposed change. On the other hand, potential negative factors are country-specific characteristics that represent a barrier to the proposed change. In a broader view, the range of factors can be defined as prerequisites of change, intended as the main preliminary conditions required to facilitate the implementation of the change (see Figure 1). The prerequisites of change could suggest the country’s general attitude to reform. This framework is adopted to carry out a comparative analysis of two countries.

Research design

This study focuses on the European context. The prior literature has stimulated comparative research, covering countries with different socio-economic levels and political traditions (Benito et al., 2007). Considering that countries within close proximity to each other and with similar contexts could lead to the result of the research being seen as irrelevant, Italy and Sweden have been selected.

The two countries may be considered as distant states not just from a geographical, cultural and economic point of view. The recent publication ‘A comparative overview of public administration characteristics and performance in EU28’ (EC, 2018) remarks that the two countries diverge in their public sector, focusing on the following tools: the size of government and civil service system; the structure of government; the political-administrative system; administrative capacity; and performance. In addition, from an accounting perspective, Italy represents the Continental tradition while Sweden represents the Scandinavian matrix (Christiaens et al., 2015). After the selection of countries, a list of crucial factors to execute the analysis was derived from the key elements reviewed in the analytical model (see Table 2).

The empirical part was mainly conducted by examining a wealth of scientific publications and publicly available archived materials of the Italian and Swedish public administrations. Data were categorized into the factors in Table 2 and categorized as potential positive factors (+), potential negative factors (–) and neutral factors (=) with respect to the proposed international harmonization.

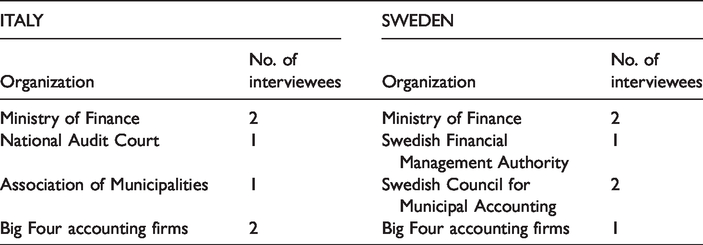

The analysis of official documents has been supplemented with 12 interviews, detailed in Table 1, selecting key actors with the following criteria: (1) the total covering of examined networks; and (2) the representativeness of other categories of key actors. For instance, the Italian member of the Association of Municipalities (ANCI) was one of the heads of that organization and, at the same time, involved in training activities for practitioners in the whole country. Again, the member of the Swedish Ministry of Finance followed EPSAS activities and had positions in municipality and health systems.

Interviews from the national contexts.

Comparative analysis.

Interviews had a dual purpose: they allowed the collection of additional data; and they allowed the triangulation and corroboration of the factors as positive, neutral or negative. Despite the research being unable to generalize the results coming from two countries, the potential positive factors of both countries have been summarized and discussed to suggest further development of the study.

The international scenario: stimuli of international harmonization

Since 2009, European bodies have had to deal with economic shocks and the adoption of anti-crisis measures (Jones and Caruana, 2016; Mussari, 2014). Some states, such as Ireland, Portugal, Spain, Italy and Greece, with high debt to gross domestic product (GDP) ratios, have experienced sovereign debt crises. In 2011, Italy registered a 120% debt/GDP ratio and experienced a speculative attack (35% of its sovereign debt is owned by foreign funders), and a government of experts was appointed to adopt national anti-crisis measures. The stress on Sweden was totally different: in the same year, it registered a 38% debt/GDP ratio and a stable economic situation.

The turbulent economic scenario, as well as the quest for better comparability and transparency of accounting numbers within EU countries (Brusca et al., 2018; EC, 2013; OECD, 2017), encouraged the adoption of the ‘six pack’ and ‘two pack’. These were a number of directives and regulations mainly oriented at coordinating the budgetary cycles and economic planning of member states, though they also defined a more rigid supervision by EU bodies of the fiscal and budgetary matters of countries, thus increasing transparency, accountability and macroeconomic surveillance (EC, 2013).

Directive No. 85/2011 of the six pack ‘on requirements for budgetary frameworks of the Member States’ did not mention mandatory requirements for member states, but the process to implement European accounting harmonization (i.e. the EPSAS programme) commenced from that moment. The EPSAS programme was set up to define a European standard-setting process with the participation of observers from member states and international stakeholders involved in PSA. Those observers include the International Monetary Fund (IMF), the UN, the OECD, the World Bank, the multinational accounting firms (i.e. the Big Four), the IPSAS Board and Accountancy Europe. The main activities of Task Force EPSAS (TFE) consist of periodic meetings with the representatives of international organizations and countries. The task of the TFE is to mobilize European governments (Brusca et al., 2018) to renovate their financial reporting accounting systems with a full accrual approach; the programme does not address budgetary systems. As already mentioned by prior works (Brusca et al., 2018; Caruana et al., 2019), the fundamental role that budgetary systems, mainly in cash accounting, play in policymaking, spending decisions and administrative procedures in national contexts is a critical juncture of the process. Generally, it could be argued that those countries that encountered sovereign debt crises and with little use of accrual-based systems could be more exposed than others to adopting a proposed international reform (Oulasvirta and Bailey, 2016).

The Italian context

Italy is one of the founders of the EU, signing the Treaty of Rome that established the European Economic Community in 1957. The state is a civil law country that was greatly influenced by Napoleonic reforms during its unification. The model of public administration was built with a French influence based on a strong centralized model (Manes Rossi, 2015). The National Audit Court and the General State Accounting Office, a department inside the Ministry of Finance, maintain significant influence on PSA matters. Nowadays, the structure of the state is composed of three levels:

the central government, with ministries and private and public agencies; regions (20); and provinces and municipalities (about 8,100).

Italy does not have a model of regulation with an independent standard-setting agency. The Ministry of Finance has total power over standard-setting activities, which it exercises by using decrees, bills and circulars. The national approach is ‘rule by law’ and standards are adopted with laws or decrees. Cornerstones of the system can be noticed in some articles of the constitution and a number of laws and decrees that frame the entire system, from its principles to detailed treatments.

From a PSA reform that started in 2009, commissions were set up with the aim of running a process of national harmonization. One such commission is focused on the sub-national entities (regions, provinces and municipalities). The so-called ARCONET commission, from the same Ministry of Finance, has a role that is comparable to a standard setter. It is composed of representatives from the Ministry of Finance, the Department of Regional Affairs, the National Audit Court, the National Statistical Office (ISTAT), the Association of Regions, the Union of Provinces (UPI), ANCI, the Italian Institute of Accountancy (OIC), the Italian Association of Certified Public Accountants, the Association of Banks and Assosoftware (an association of information and communication technology (ICT) and software producers). More or less, the same modality of work has been adopted for the other areas of the public sector: working groups and commissions are running sectorial PSA reforms, from universities to the central state (Ministry of Economy and Finance [MEF], 2018).

The controls on accounting numbers are exercised by two main subjects. The National Audit Court exercises deep control over the annual reports of public entities, thanks to its territorial organization. The court also provides recommendations on accounting principles in its year-end report about the government annual report. Additionally, the audit function in each public administration is executed by external professional auditors (single or a board).

The actual accounting system, from central government to lower tiers of government, utilizes a cash and commitment basis of accounting for budgeting and financial reporting. In order to correspond with the European semester, the budgetary cycle begins in April with the adoption of the Economic and Financial Document, detailing mid-term economic projections and fiscal policies without expenditure forecasts. Following this is a top-down process that is managed by the Ministry of Finance to aggregate the baseline forecasts of each ministry, with ongoing meetings (Blöndal et al., 2016). Also, the Budget Bill, issued in the autumn and voted on by 31 December, is composed of 34 missions of expenditures, each is declined in a number of programmes. The resources of each programme are managed by an administrative unit inside the ministries. In 2012, Italy introduced the principle of the ‘balanced balance’ in its Constitution, with annual targets and indicators defined by the Ministry of Finance; the rule is applied in the different tiers of government. A Parliamentary Budget Office has been established as an independent body to verify and endorse the policies applied in the budget, while a number of private and public bodies, such as the Italian Central Bank, analyses and give their own opinions about fiscal and budgetary policies.

Budgetary reporting remains the main system and the main source of data (reconciled by ISTAT) used to calculate the macroeconomic aggregates under the 2010 European System of Accounts (ESA). Accrual accounting was first introduced by the National Health Service with a full approach in 1992, followed by state-owned enterprises and universities in 2012. In the last reform, especially for municipalities, accrual accounting has been progressively introduced as stable practice, though it plays a secondary, informative role in financial reporting, where cash and commitment accounting constitutes the fundamental system (OECD, 2017). The central state, with its ministries, still uses a cash and commitment basis of accounting. The systems are not fully harmonized among the different levels.

The standard-setting process is characterized by a deep bureaucratic approach, determining rigidity in the day-to-day work of users and preparers: The main difficulty is that our system is very complex; the legal system of civil law bases its action on control and authorization of processes … . Everything comes from laws; tasks and procedures are derived from the law. … If you look at an Italian accounting standard, you state that it is too long, complex, and the logic contains most of juridical profiles with enormous difficulties to be applied especially in local contexts with low professional skills and scarcity of human resources. It is very different from the IPSAS logics. (Member of the National Audit Court, Italy)

The Swedish context

Sweden joined the EU in 1995. The country is a constitutional monarchy based on civil law, with Germanic and common law influences. This tradition characterized the system with the independence and autonomy of practices, as also reflected in public administration and accounting practices. The Swedish public sector is organized in three levels:

the central government, with ministries and agencies; counties (21); and municipalities (290).

Until the end of the 1990s, municipal accounting especially had no formal standard setter, and the system was praxis-oriented (Tagesson and Grossi, 2015). Accountability, intended as a control on public finances and the application of accounting standards, historically registered a low intensity.

The definition of accounting standards is divided between two standard setters acting for the central government and the local level. The central government is ruled by the Swedish Financial Management Authority (Ekonomistyrningsverket (ESV)). The ESV defines accounting standards and controls their application in the central government, ministries and agencies.

It consists of two main councils for accounting issues. The first is the Accounting Council that promotes the development of accounting rules and standards, which is composed of representatives from accounting professionals, including the Big Four, experts and the National Audit Office. The second is the Internal Audit Council that develops the internal audit function within the state, which is composed of internal auditors from different areas of the public sector.

The second subject is the Swedish Council for Municipal Accounting (SCMA). The non-profit agency was established in 1997 by the government, the Swedish Association of Local Authorities and county councils. There is a ‘board’ composed of experts in the municipal sector that are representatives of the Ministry of Finance and county council members, and an ‘experts group’ that helps to define the standards and makes recommendations. 2 The members of the ‘experts group’ are representatives of the Big Four, the Ministry of Finance, the Association of Local Authorities and Regions (SALAR) and the local level.

The law outlines the main principles and contents of accounts, whereas the two standard setters publish each standard and recommendation. Controls on accounting data are exercised by the Supreme Audit Institution (SAI), which is responsible for controlling the central government annual report. Additionally, Sweden adopts a questionable model of auditing at the local level: auditors are chosen among municipal politicians that may have little professional competence and a potential lack of independence (Donatella et al., 2018; Tagesson and Grossi, 2015).

The Swedish PSA systems have been profoundly reformed since the end of the 1980s.

3

Adoption of accrual accounting began in 1990 as a package to fight a national economic crisis. Horizontal accounting harmonization across Swedish economic sectors guarantees a good comparability of data and tangible benefits: It is very useful to have the same principles between the public sector and private companies; politicians have knowledge of the private sector accounting systems. It is easier [to] get them involved, for example, in the analysis of the economy or a municipality. There is better comparability, and it is easier to compare and understand for people. … If you go to the education system, if we have people who received education in accounting, they do not need additional training to understand PSA systems. It is easier to recruit. (Member of the ESV, Sweden) The substantial difference between the Swedish central government accounting rules and IPSAS is the kind of supplementary disclosures required. ESV’s point of view is that the requirements of supplementary disclosures in IPSAS are very far-reaching and comprehensive, while the requirements for central government agencies are based on the user’s need of information. (Member of the ESV, Sweden)

The Swedish government appointed three delegates to the EPSAS programme from the central government: one from the ESV and two from the Ministry of Finance, one of whom is also a member of the experts group from municipal accounting to cover the different areas. The issues treated in international meetings are deeply involved in national consultations with representatives of agencies and administrations to get a better understanding of the matter. Sweden has not revealed an official position on EPSAS, even if they support a process of international harmonization.

The comparative analysis

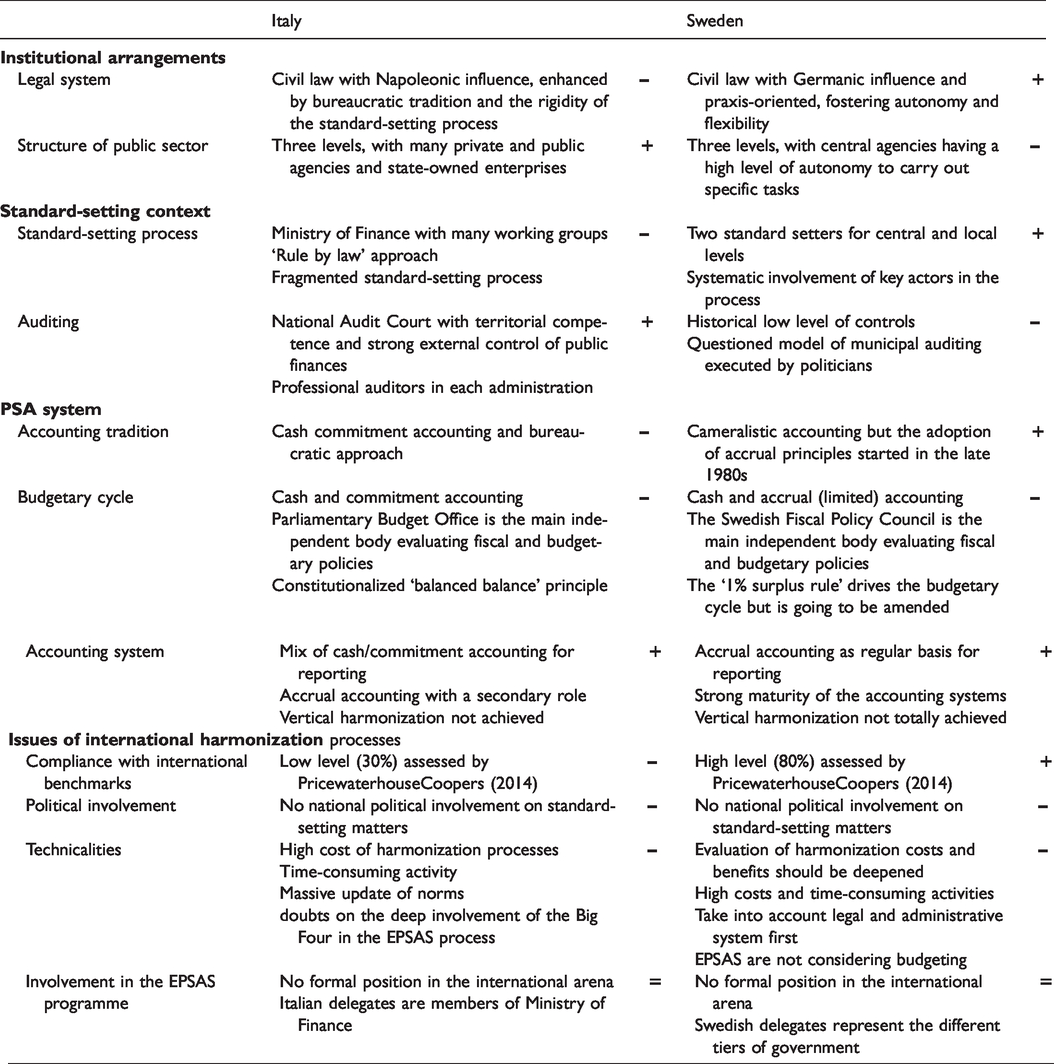

The two countries and their characteristics have been compared. In the following, the factors reported in Table 2 are discussed with respect to their categorization.

The Italian situation shows that the legal system can increase the rigidity of the standard-setting process. On the contrary, Swedish standard setters have a reasonable level of flexibility. At the same time, the structure of the state in Sweden is characterized by the pronounced autonomy of agencies and municipalities. This historical autonomy of lower tiers of government should be balanced by a strong system of controls exercised by the National Audit Court and by the auditors avoiding the tendency to deviate from central practices. Italy seems to have a more centralized structure. The activities of the National Audit Court, especially its sanctions, constitute a tangible tool to guarantee the application of accounting standards and strict control over public finance, while Swedish auditing at the local level is debatable (Donatella et al., 2018). Additionally, the two public sectors also differ in terms of size: Italy has about 8,100 municipalities while Sweden has a more limited number of entities.

Over time, the two countries have developed particularly divergent models of PSA. First, Italy still lacks an independent standard-setting agency, intended as an organization involved in the full-time definition of standards, as in most European countries (Brusca et al., 2018). This has contributed to variations within the Ministry of Finance and a fragmentation of the standard-setting process among many working groups. Differences also emerged in the management of the process. Sweden guarantees a systematic involvement of private and public key actors in the boards, whereas Italian commissions adopt a diverse modality of participation of key actors. Regulators from both countries remarked that a clear and stable standard-setting process can limit the reluctance of practitioners, contributing to a fast embedding of reforms.

Second, the countries adopt different PSA systems. The budgetary cycle, focused on the financial monitoring of expenditures and incomes, and the subsequent use of cash and commitment accounting, still represents the basic architecture of the entire economic and fiscal policy of governments with respect to financial reporting. This fact, including technical procedures, the strong legal dimension of the budget and the governance of the process of both countries, represents a resistance factor for international harmonization. Regarding financial reporting, the latest reform in Italy brought tangible progress in the use of accrual accounting but compliance with international best practices is still lower compared to Sweden, which has been using established accrual-based PSA systems since the 1990s. The research revealed that neither country has reached full vertical harmonization.

Interesting insights emerged from interviews regarding international accounting harmonization. Neither Italy nor Sweden has assumed a formal position on the EPSAS process yet. In addition, concerns emerged with respect to the perspective of international harmonization. A potential EPSAS implementation can require a massive update of norms and institutional arrangements, and the labelled ‘all package’ (i.e. a package of legal, economic, public governance and accounting issues) of harmonization has been questioned. Accounting harmonization is inserted into the wider process of European integration: How can we just say that we have the same accounting regulation when other related things are regulated in different ways? All the packages should be connected. … There are many experts at the meetings and many issues concerning the legal dimension, the concept of subsidiarity, legality. (Member of the Ministry of Finance, Sweden) We think that the works [i.e. the TFE] are not adopting the correct methodology because the standards [i.e. the EPSAS] are substantially prepared by the Big Four. In my prior experience in International Federation of Accountants (IFAC), we noted cases of governmental reporting … completely prepared by auditing multinationals. There is a great debate in our network around these approaches, they are too simple. … In addition, states that adopted a full accrual approach registered problems: an accrual-based system is characterized by a high level of discretion about the valuation of assets, and of the profit/losses. (Member of the National Audit Court, Italy)

Discussion and conclusions

This article aimed to contribute to the debate on accounting harmonization by focusing on national PSA standard-setting contexts. The research, inspired by prior studies on the theme (Christiaens et al., 2015; Lüder, 2002; Palthe, 2014), investigates two national cases to explain how national PSA standard-setting contexts could react to international harmonization processes. The study identifies prerequisites of change that could provide a better understanding of the national levels involved in the EPSAS programme.

The contribution of this article is twofold. First, the study developed an analytical model in an attempt at simultaneously dealing with national settings targeting technical, organizational and governance aspects, which are usually encountered separately in the literature. The research does not reframe ground theories, but the analytical model contributes to the PSA reform and innovation literature by defining a scheme of analysis under an interdisciplinary approach, where international harmonization processes are seen as not solely technical processes, but rather inserted in a complex environmental and sociological national setting (Jorge et al., 2019b; Lüder, 2002).

Second, the study aimed at identifying the governance and practical implications for policymakers in the complex field of PSA. With respect to the research question, Sweden seems to provide a more favourable context for change, with a higher number of potential positive factors than Italy. The findings are in line with prior contributions by Hood (1995) and Vela and Fuertes (2000), who verified attitudes towards implementing New Public Management (NPM) and accounting reforms among a sample of European countries.

Although the research does not permit the generalization of its results to all EU member states, the potential positive factors coming from both countries have been listed and discussed, as follows:

Flexibility of legal system and standards: to quickly adopt accounting reforms, the legal framework of the standard-setting process should allow the standard setter to modify rules without laws. Indeed, Italy, with a contrary situation, is perceived by actors as overly bureaucratic and hard to change. Reliable and professional systems of controls on public finances: high-quality controls and auditing can enhance the correct application of standards, especially when the public sector is vast and fragmented. Maturity of PSA system in the use of international best practices: an established accrual-based accounting system and compliance with international benchmarks can enhance the credibility and reliability of the state in the international arena. At the same time, this condition can reduce costs and activities in the implementation of international harmonization (Jones and Caruana, 2016). High level of vertical harmonization: this condition can facilitate the implementation of an international PSA change, resulting in the high quality and easy comparability of accounting data, as well as the easier planning and implementation of reforms for the whole public sector. High level of integration among budgeting practices and accrual financial reporting: budgeting logic is at the heart of economic and fiscal policy as a whole, and the better alignment of rules, especially for the reporting phase, can enhance the comparability, transparency and usefulness of both systems, as well as better compliance with the legal framework. Aggregation and integration among standard setters: an independent standard-setting agency seems to be more efficient. Fragmentation in standard setting, with the proliferation of subjects, rules and regulations, increases the perception of accounting differences and confusion among different areas of the public sector. Inclusive and participative governance of the standard-setting process: the systematic participation of key actors on the board of the standard setters, including representatives of users, preparers and software houses, can facilitate the acceptance and implementation of ‘functioning’ reforms. An inclusive process could imply more time to define a reform but this condition determines the higher legitimacy of the standard setter. A fragmented network and a lack of participation of key actors may increase resistance to change and problems in aggregating national voices to deal with international harmonization. Political support for the standard-setting process: if the independence of accounting regulation from the political level is considered a positive principle by scholars to protect the reliability and neutrality of accounting data, the role of politics assumes a fundamental role in a time of reform (Marty et al., 2006). Political involvement, from national and international levels, constitutes a tangible aid to boost an accounting reform. Interviewees from both countries hope for a political mobilization to enhance the discussion of the EPSAS programme within their respective national networks.

The aforementioned factors emerged as optimal prerequisites of change, while both countries differ in some respects. The main idea of the study is that a country with a higher number of potential positive factors can positively react to international accounting harmonization, with a process that is easier to manage and lower costs. The factors could be seen as complementary to the governance implications outlined by Caruana et al. (2019), who focused on the international context.

The forthcoming ‘EPSAS package’ should take into account national specificities, limiting contrasts among national systems and the international proposal in both technical and governance aspects. In this regard, the findings of this study confirm that the harmonization of budgeting and fiscal praxis under the ‘six pack’, ‘two pack’ and 2010 ESA may not be integrated with the harmonization of financial reporting accounting promoted by the EPSAS programme. In addition, the literature has already remarked on the deep heterogeneity of practices in EU countries and the debatable role of IPSAS and the Big Four in the EPSAS programme (Christiaens et al., 2015; Manes Rossi et al., 2016).

These conditions could undermine the possibility of reaching an agreement: the more the involved countries diverge in their prerequisites for change, the more difficult it will be for the success of the harmonization process. In this perspective, national contexts could promote more multidisciplinary activities aimed at verifying whether, in their respective networks, ‘the benefits of the adoption of EPSAS become apparent, and outweigh the costs involved’ (Jorge et al., 2019a: 144).

The study presents some limitations. The comparison included just two single countries in a potential sample of 28 member states. Second, the analytical model could consider other international factors that can affect national context, as well as targeting international interviewees. Further research, selecting other European states and privileging the diversity of tradition and cultural background, can enhance the generalization of results and reveal the governance implications for both national and international policymakers.

Footnotes

Acknowledgements

The author wishes to thank the people who participated in the study, the two anonymous reviewers for their constructive and valuable comments, and the academics and professionals, especially members of the EGPA Permanent Study Group XII, who dedicated suggestions. The author is grateful to his mentors, Luca Bartocci, University of Perugia, Italy, and Daniela Argento, Kristianstad University, Sweden.

Declaration of conflicting interests

The author declares no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.