Abstract

This study adds new insights to the academic debate on the effectiveness of both accrual-basis systems and the adoption of harmonised accounting rules at the international level by considering an additional perspective: their effect on corruption. This study investigates a sample of 33 Organisation for Economic Co-operation and Development countries for the period 2010–2014, creating a panel data set that allows the taking of an international comparative approach. The results indicate that corruption is reduced as governments advance in public-sector accounting reforms, adopting International Public Sector Accounting Standards, or implementing accrual-basis systems.

Points for practitioners

Our findings show the relevant role played by public sector accounting reforms in reducing corruption. Concretely, International Public Sector Accounting Standards implementation and accrual-accounting adoption can attenuate the information advantage of politicians towards citizens, reducing the level of corruption. This article contributes to the debate concerning the institutional arrangements that should be implemented to reduce corruption.

Keywords

Introduction

In the last decades, several global corruption scandals (e.g. the Rajoy Government in Spain; the French budget and tax minister, Jerome Cahuzac; the Honduras and Guatemala governments; the former president of the United Nations General Assembly, John Ashe, etc.) have intensified the interest of scholars and practitioners in transparency and accountability. Elected representatives and government officials are considered to be the most likely to be corrupted (Transparency International, 2017).

One way to combat this scourge is transparency. Accordingly, many governments have introduced important reforms with the aim of making public-sector entities more accountable. Transparency is essential to preventing corruption (De Mingo and Cerrillo-i-Martínez, 2018), but just making information available is not enough. Literally, transparency refers to the availability of information, but it does not refer to the quality of such information. To be effective, the content of the available information should become known and understood by readers (Lindstedt and Naurin, 2010), which would imply high information quality.

This idea is particularly relevant in the case of financial and accounting information published by governments. Increasing the quality of such information is a debated issue, frequently related to the use of international accounting standards or accrual-accounting systems. In this regard, International Public Sector Accounting Standards (IPSAS) and the accrual-basis system have been considered as an instrument through which to report reliable, comprehensive, timely and internationally comparable financial information (e.g. Benito et al., 2007; Wang, 2002). Several studies (Ball, 2012; Bergmann, 2012; Caba-Pérez and López-Hernández, 2009; Cohen and Karatzimas, 2015; Navarro-Galera and Rodríguez-Bolívar, 2011) have emphasised that the modernisation of governmental accounting can have several benefits in terms of transparency, but its effect on corruption has not been tested.

Accordingly, this article aims to investigate the effect of both IPSAS implementation and accrual-accounting adoption on the level of corruption. To this end, it uses a sample of 33 Organisation for Economic Co-operation and Development (OECD) countries for the period 2010–2014. The OECD context is highly appropriate as many countries have already adopted accrual accounting, and many standard-setters retain IPSAS as a primary reference for elaborating their national standards, although their implementation is still low (OECD and IFAC, 2017).

The remainder of the article is structured as follows. The second section provides a theoretical background and reviews the literature on IPSAS and accrual-accounting systems adoption, as well as on corruption, developing the research hypotheses. The third section describes the methodology, while the fourth section presents the results of the study. Finally, the fifth section concludes.

Theoretical background

Scholars have investigated factors promoting a better disclosure of financial information (Laswad et al., 2005; Rodríguez Bolívar et al., 2013), frequently using the agency theory perspective, according to which politicians (agents) are expected to act in the interests of citizens (principal). However, a conflict of interest between them can occur (Jensen and Meckling, 1976) as politicians could adopt opportunistic behaviour in the face of information asymmetries (Rogoff and Sibert, 1988).

The public choice theory offers useful insight as it investigates the behaviour of the agents interacting in political markets (Buchanan, 2009). Scholars claim that politicians are expected to remain egoistic, rational, utility maximisers (Mueller, 1989), trying to find how to maximise their own well-being (as individuals could do in economic markets), rather than that of the public (‘self-interest axiom’; see Boyne, 1997). Therefore, the adoption of institutional arrangements is required in order to reduce their ability to engage in opportunistic activities (e.g. rent-seeking, corruption), stimulating them to act in the interest of citizens (‘pressure of competition axiom’).

Indeed, public choice theory provides ad hoc proposals on how to minimise political opportunism, including corruption and rent-seeking (Mbaku, 2008). One of these measures is holding politicians accountable for their actions in order to demonstrate that they have operated according to their responsibilities. Thus, the conflict of interest between politicians and citizens can be solved by reducing the information advantage of the former (Oscarsson, 2008), and allowing citizens to monitoring the actions of politicians (Laswad et al., 2005). More reliable and comparable information could stimulate politicians to act in the interest of citizens, increasing the degree of confidence and public trust in political actors.

Therefore, transparency can be considered as a remedy against corruption, but its effectiveness can depend on the accounting systems in use. Consistently, the adoption of IPSAS or the implementation of accrual-basis systems is expected to play a relevant role in improving accountability, and then improving decision-making processes (Sutcliffe, 2003).

Accrual accounting and accounting harmonisation

Several studies (Barton, 2009; Blöndal, 2002; Christiaens, 2004; Guthrie, 1998; Wynne, 2008) have queried the adoption of accrual-accounting systems in the public sector because such adoption could prevent consideration of the specificities of public administrations (e.g. heritage, non-exchange revenue, etc.). Some scholars even suggest that accrual accounting provides more space for earnings management and the manipulation of accounting numbers (Stalebrink and Sacco, 2007; Pilcher and Van Der Zahn, 2010).

However, other studies have highlighted the advantages of the accrual system. For instance, Pina and Torres (2003) note that it provides complete and accurate information about public entity solvency, the evaluation of assets and liabilities, and the costs of public services. Chan (2003) indicates that the application of accrual accounting can achieve wider accountability in a democratic system and in a free market. Furthermore, accrual-accounting information better supports public management decision-making by allowing for the better planning and management of public resources (Christiaens and Rommel, 2008). This means that accrual-accounting data better satisfy the information needs of markets and investors (Caperchione and Salvatori, 2012; Gomes et al., 2015).

In the same vein, despite the doubts regarding IPSAS implementation, the positive impact of harmonised accounting standards has been extensively supported (Bastida and Benito, 2007; EC, 2013; IFAC, 2003). The last international crisis has strengthened the need for harmonised public-sector reports in order to provide information so as to alert practitioners of financial problems in a timely and reliable manner (Christiaens et al., 2010; Cohen and Karatzimas, 2015; Oulasvirta, 2014). Accordingly, Mussari (2014) has underlined the role of IPSAS implementation in ensuring transparency since international harmonisation facilitates the evaluation of governmental performance (Torres, 2004) and improves the quality of financial reporting (Bergmann, 2012).

Regarding previous arguments, we expect that IPSAS and accrual-accounting adoption reinforces the stakeholders’ power and fosters citizens’ participation (Justice et al., 2006), reducing corruption. Indeed, Guarini (2016) sustains that accounting information plays a key role in contributing to the achievement of politicians’ self-interest.

Corruption and its determinants

Despite the heterogeneity of definitions, corruption generally refers to the discretionary power of public-sector entities that affects how public administration works (Werlin, 1994), that is, the abuse of public power for private benefits (World Bank Group, 1997). To explain the differences in corruption, scholars have examined several determinants, such as political factors, historical conditions, macroeconomic features and population characteristics.

Among political factors, Persson et al. (2003) found that smaller voting districts, larger shares of candidates elected from a party list and proportional elections are associated with higher levels of corruption. Lederman et al. (2005) show that parliamentary systems and political stability are associated with lower corruption.

Historical conditions refer to legal systems: common-law countries have traditionally been characterised by the greater protection of private property, which negatively affects corruption. Indeed, Treisman (2000) found that British-ruled countries tend to be less corrupt, while Treisman (2014) noted that the frequency of bribery is higher in French colonies because of the higher regulation that leads to corruption.

From a macroeconomic perspective, developing or transitional countries tend to show higher corruption levels (Svensson, 2005), and the degree of openness of the economy is negatively associated with corruption (Ades and Di Tella, 1999; Herzfeld and Weiss, 2003). Treisman (2000, 2014) found that more developed, democratic and open economies tend to be less corrupt.

Regarding population characteristics, protestant societies and ethnically/linguistically fragmented societies have been more inclined to monitor abuses by state officials (Treisman, 2000). Education, political rights and civil liberties are also negatively related to corruption (Ades and Di Tella, 1999; Treisman, 2000, 2007; Lederman et al., 2005; Svensson, 2005).

Other studies that investigate mechanisms to reduce and prevent corruption consider transparency as essential (De Mingo and Cerrillo-i-Martínez, 2018). The adoption of open-data initiatives to increase transparency (Janssen et al., 2012; Meijer et al., 2012; Wirtz and Birkmeyer, 2015) is one of the most relevant policies used to control corruption. Additionally, several scholars (Ball, 2012; Bergmann, 2012; Brusca et al., 2015, 2018; Cohen and Karatzimas, 2015) have underlined that the modernisation of governmental accounting, through IPSAS and accrual reforms, can result in several benefits in terms of transparency and accountability, but they did not prove any benefits regarding corruption. Therefore, we presume public-sector accounting and corruption to be associated.

Hypotheses development

High-quality information is essential to solving the agency problem between politicians and citizens by reducing the information advantage of the former. First, public-sector accounting harmonisation, through IPSAS, is considered a useful support for strategic decision-making processes (Sutcliffe, 2003) due to improvements in information quality. Despite previous criticisms, IPSAS implementation leads to more reliable, comprehensive and comparable information (Bastida and Benito, 2007; Kopits and Craig, 1998; Wang, 2002). Therefore, IPSAS can improve the quality of accounting information, which positively impacts on transparency and accountability (Bellanca, 2014; IFAC, 2003; Lapsley et al., 2009). Accordingly, we propose the following hypothesis:

HP1: Public-sector accounting harmonisation reduces perceived corruption.

Second, accrual-basis systems recognise transactions at the time when the economic events occur, regardless of the charges or payments; therefore, financial statements show all economic events and citizens can properly assess the financial position and performance of the government, including both present and future socio-economic implications (Bastida and Benito, 2007). Furthermore, accrual accounting is claimed to satisfy the information needs of markets and investors in a better way compared to other accounting systems (Caperchione and Salvatori, 2012), providing better information on solvency and the costs of public services (Pina and Torres, 2003). Therefore, it is maintained that the use of accrual-accounting systems can improve the quality of information through a specific set of rules, reducing corruption. Accordingly, we propose the following hypothesis:

HP2: Public-sector accrual accounting reduces perceived corruption.

Methodology

Sample

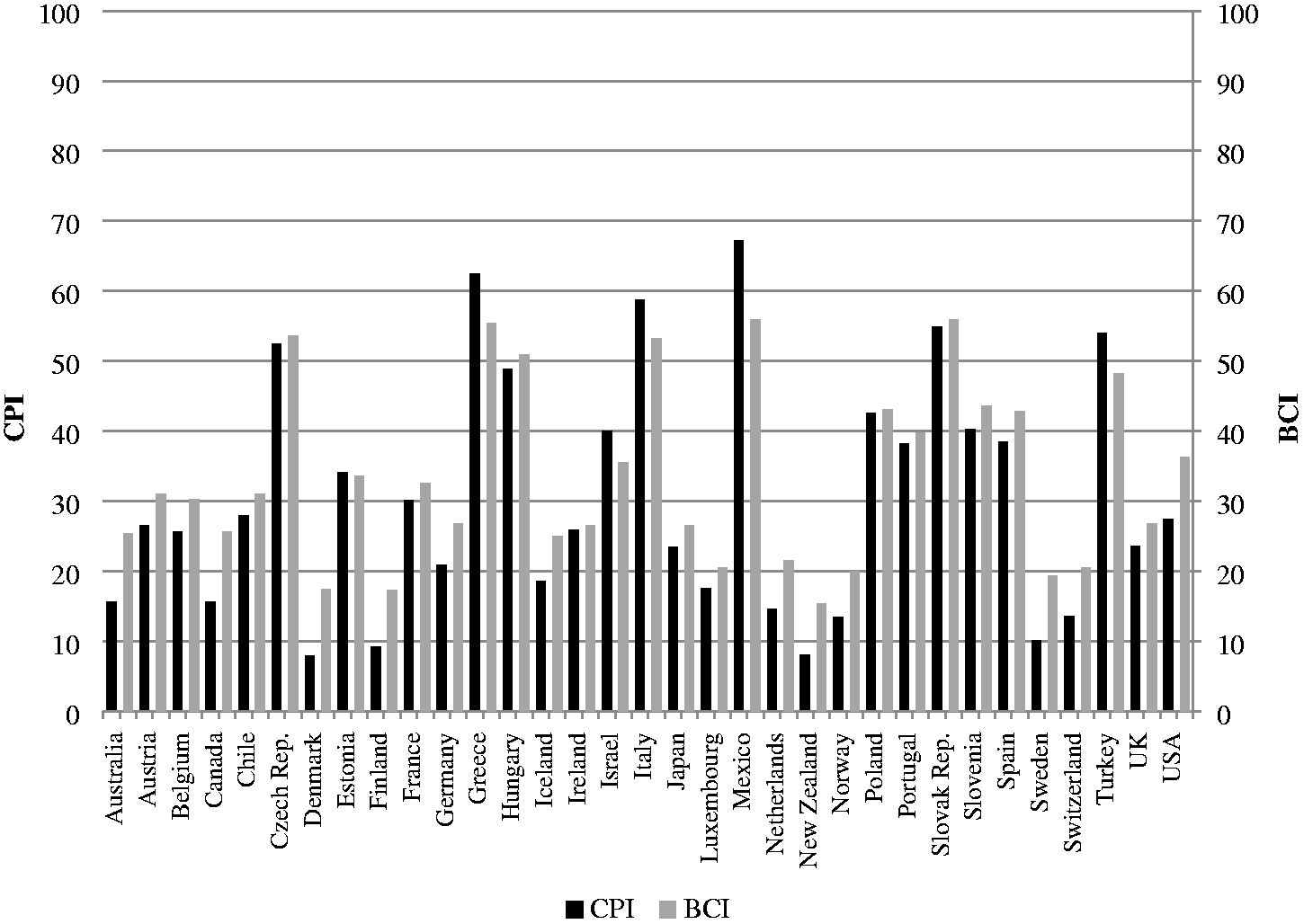

To test the proposed hypotheses, we selected a sample of 33 OECD countries (see Figure 1). 1 The OECD context is highly appropriate because IPSAS are strongly recommended by the OECD, among other multilateral organisations such as the International Monetary Fund (IMF), the World Bank and the United Nations (UN). The majority of OECD countries have adopted accrual accounting, although the direct adoption of IPSAS still remains low (Moretti, 2016).

Distribution of corruption indicators by countries.

The selected period is 2010–2014. Considering the difficulties of obtaining the data, which was hand-collected using the IFAC website and OECD and IFAC (2017), we have selected the largest period over which it was possible to obtain information on public-sector accounting status.

Model and variables

The proposed hypotheses are tested using the following econometric model:

The dependent variable (Corruption) is represented by two indicators: CPI and BCI. The former refers to the Corruption Perception Index published by Transparency International, a politically non-partisan organisation that works with partners in government, business and civil society to put effective measures in place to tackle corruption. CPI represents the perceptions of business people and experts on the level of corruption in the public sector. This index is obtained by using more than 10 different data sources from different institutions, and was standardised to a range of 0–100, with 0 being the highest level and 100 the lowest level of perceived corruption. Here, we use reverse ranging to clarify the representation of ‘corruption’, that is, 0 is the lowest level of perceived corruption and 100 the highest level.

BCI is the Bayesian Corruption Index, which is available from the Quality of Government (QoG) Basic Dataset published by the QoG Institute, an independent research institute at Gothenburg University. BCI is a composite index that combines information from 20 different surveys through more than 80 survey questions that refer to the opinions on the level of corruption from inhabitants, companies, non-governmental organisations (NGOs) and officials working in a country. BCI takes values between 0 and 100, from the lowest to the highest levels of perceived corruption.

The independent variable in model 1 (Accounting) is represented by two indicators: IPSAS and Accruals. Following Bellanca and Vandernoot (2014), the former denotes the status of IPSAS adoption reforms by four levels:

IPSAS = 1: No actions have been undertaken to adopt IPSAS until now. IPSAS = 2: IPSAS adoption is being discussed. IPSAS = 3: IPSAS are being adopted, that is, the legislative process has been undertaken and IPSAS are partially applied. IPSAS = 4: IPSAS are adopted or national standards are broadly consistent with IPSAS.

Following Christiaens et al. (2015), Accruals takes three values regarding the status of accrual-basis reforms in the public sector:

Accruals = 1: Public-sector accounting standards require a cash basis for the preparation of financial statements. Accruals = 2: The country is in transition to accrual accounting or standards require modified systems (modified accrual or modified cash). Accruals = 3: Public-sector accounting standards require an accrual basis for the preparation of financial statements.

Additionally, the results are controlled by various socio-economic and political variables:

Economic development (GDPpc): this is represented by the log per capita purchasing power parity gross domestic product (PPP GDP) at a constant price; data have been obtained from the OECD online databank. It is presumed that more developed economies are less corrupt than others (Donchev and Ujhelyi, 2014; Lederman et al., 2005; Treisman, 2000, 2007, 2014) since the normative separation between public and private property is clearer. Education level (Education): we refer to the number of students enrolled in secondary school, expressed as a percentage of the official school-age population corresponding to that level of education. Data were obtained from the World Bank online databank. It is presumed that education is negatively related to corruption (Ades and Di Tella, 1999; Svensson, 2005) since it enables citizens to monitor politicians and identify corruption activities. Ethno-linguistic fragmentation of the population (Fragmentation): this variable is the sum of two indicators, Ethnic fragmentation and Linguistic fragmentation. Each of them reflects the probability that two randomly selected people from a given country will not share a certain characteristic – ethnicity and language, respectively (Donchev and Ujhelyi, 2014; Lederman et al., 2005; Treisman, 2000, 2014). Fragmentation takes a value of between 0 and 2, and data have been obtained from the QoG OECD Dataset 2017 (Dahlberg et al., 2018). More fragmented societies are supposed to have more political clientelism and, thus, higher corruption levels (Donchev and Ujhelyi, 2014). Trade openness of the economy (Openness): this is represented by the imports of goods and services as a percentage of GDP (Lederman et al., 2005; Svensson, 2005; Treisman, 2007); data have been obtained from the World Bank online databank. The relevance of foreign trade on domestic activities may reduce corruption because it increases competence, which acts as a monitoring mechanism on opportunistic behaviour (Ades and Di Tella, 1999; Herzfeld and Weiss, 2003; Treisman, 2000). Electoral system (System): this is represented by a categorical variable that takes three values: 0 for presidential systems; 1 for assembly-elected president systems; and 2 for parliamentary systems. Data have been obtained from the Database of Political Institutions (DPI), namely, DPI 2015 (Thorsten et al., 2001). In general, parliaments have the power to remove politicians from the executive branch (Lederman et al., 2005; Treisman, 2014), reinforcing the oversight of opportunistic behaviour. Legal origin (Common): this is represented by a dummy variable that takes the value of 1 for common-law countries and 0 otherwise. Common-law countries are usually characterised by the greater protection of property, as well as by greater legal flexibility; such flexibility allows the adaption of laws and moral norms more quickly, which benefits the oversight of opportunistic behaviour (Treisman, 2000).

Although previous studies (e.g. Lederman et al., 2005; Svensson, 2005; Treisman, 2000, 2007, 2014) have used additional variables to explain the level of corruption (e.g. the degree of federalism, the degree of democracy, political competition and stability, the freedom of media and civil liberties, colonial traditions, etc.), most of them are highly correlated with the control variables selected here. Therefore, we do not use all of them in order to avoid multicollinearity problems.

Technique

For panel data, the fixed- or random-effects (FE or RE) estimators could be used to estimate the parameters β of model 1. However, the two estimators require some initial conditions: errors should be homoscedastic and not serial correlated, and independent and control variables should be strictly exogenous.

Therefore, we first test whether errors in model 1 are homoscedastic and serially correlated, using the Breusch–Pagan test and the Wooldridge test, respectively. The p-values obtained for each test are lower than 0.05, meaning that we must reject, for a 95% confidence level, the null hypotheses of: (1) homoscedastic errors; and (2) no serially correlated errors. Therefore, neither FE nor RE estimators are suitable in this case.

Second, independent and control variables should be strictly exogenous; conversely, endogeneity problems arise. Endogeneity appears in model 1 for three reasons (Wooldridge, 2010): (1) the use of proxy variables to represent unobservable or difficult to quantify concepts (e.g. corruption or IPSAS/accruals) leads to measurement errors; (2) results could be additionally controlled by other variables, such as government deficits, economic growth, the rule of law, economic globalisation and so on, but these have been omitted due to multicollinearity problems; and (3) as model 1 is an AR(1) model, reverse causality appears between Corruptiont and Corruptiont – 1. Further, Treisman (2007, 2014) suggested causality problems between corruption indicators and socio-economic and political factors.

Accordingly, endogeneity should be addressed using instrumental variables (IV) methods. However, the conventional IV estimator is inefficient in the presence of heteroscedasticity (Baum et al., 2003). Alternatively, the dynamic panel estimator of Arellano and Bond (1991) overcomes such limitations. Concretely, we used the two-step system estimator (Arellano and Bover, 1995), which improves the efficiency of the traditional difference estimator (Arellano and Bond, 1991) because it has poor finite sample properties (Blundell and Bond, 1998).

The system estimator uses a set of IVs to remove the endogeneity. Concretely, the instruments are the lagged values of the endogenous and predetermined variables. It has been demonstrated that these instruments are uncorrelated with the error term when deriving the estimator (Arellano and Bond, 1991). Nevertheless, researchers must keep in mind that a proliferation of instruments may bias the results. The most adequate instruments are the closest lags since the furthest cannot contain information on the current value of the variables. Therefore, instrument validity is tested using two tests: (i) the Arellano–Bond test for AR2 in first differences, under the null hypothesis of no serial correlation between the error terms; and (ii) the Hansen test of over-identification restrictions, under the null hypothesis that the over-identifying restrictions are valid.

Results

Descriptive analysis

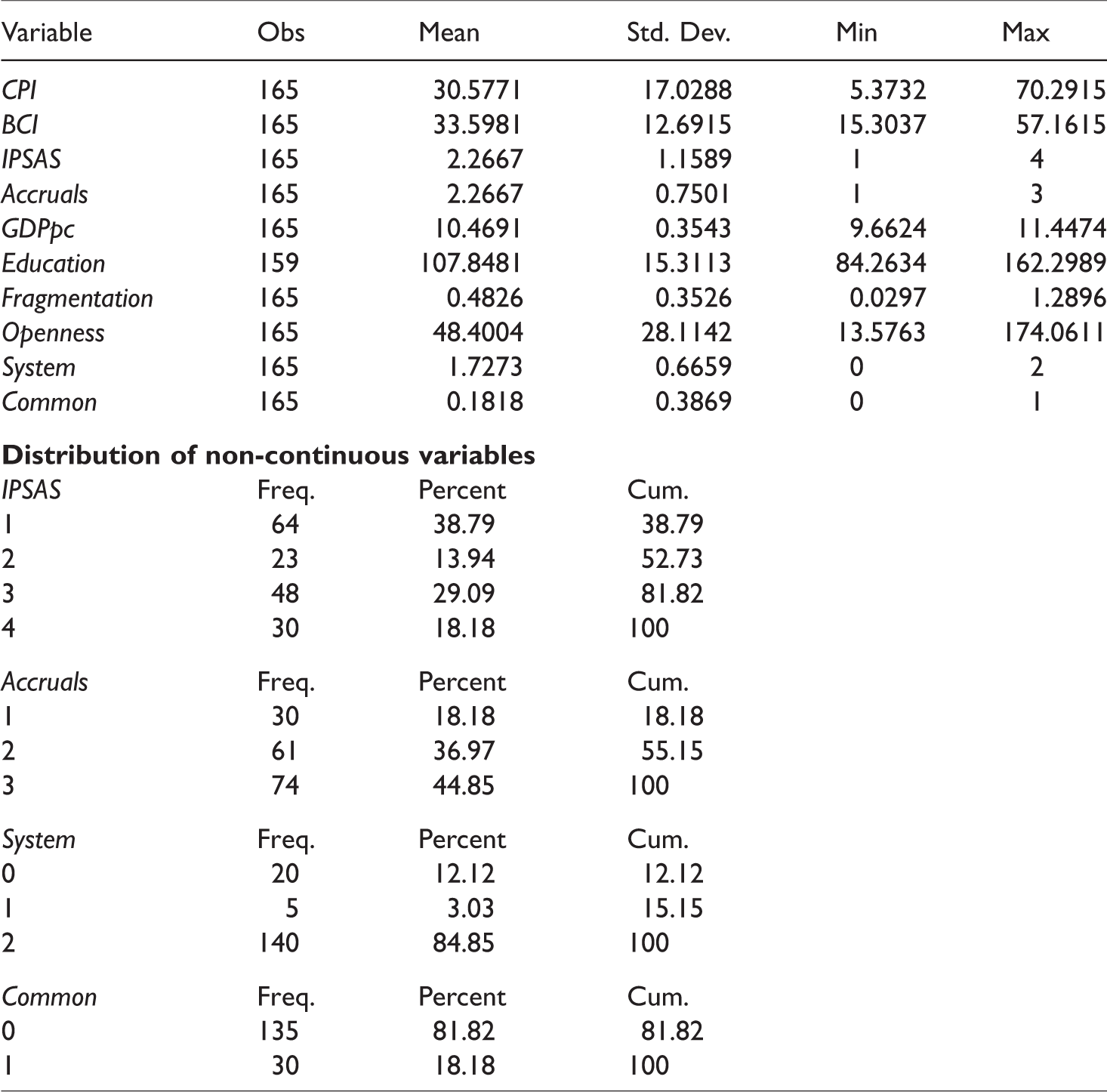

Table 1 shows the descriptive statistics of the variables presented in model 1. Regarding corruption variables (ranging from 0 to 100, from the lowest to the highest level of perceived corruption), the mean values of CPI and BCI indicate low levels of corruption in the OECD context, although there are large differences between countries. Figure 1 shows that Mexico, Greece and Italy scored the highest over the period 2010–2014, while Denmark, New Zealand, Finland and Sweden scored the lowest.

Descriptive statistics.

The mean value of the IPSAS variable is 2.27 in a range between 1 and 4 (from no adoption to full adoption). Therefore, the sample countries are involved in IPSAS adoption reforms but full adoption is uncommon. Only Australia, Canada, New Zealand, Switzerland, the UK and the US achieve a value of 4, suggesting that although the full adoption of IPSAS has not yet been achieved, these countries’ national standards are broadly consistent with IPSAS.

Surprisingly, the mean value of the Accruals variable is also 2.27, although it is measured differently (taking values between 1 and 3). The interesting distribution of IPSAS and Accruals is illustrated at the bottom of the table. Although only 18.18% of observations are broadly consistent with IPSAS (IPSAS = 4), 48.85% use accrual accounting (Accruals = 3), and just 18.18% require cash-basis accounting (Accruals = 1). These results indicate that a large proportion of OECD countries have implemented accrual-basis accounting systems, but full IPSAS implementation is still unusual, and 38.79% have undertaken no actions to adopt IPSAS to date.

As for the other variables, the mean value of GDPpc is 10.47 (in logarithm terms), which refers to USD37,529.01 per capita, while the mean value of the secondary enrolment rate (Education) is 107.84, although there are large differences between countries. Ethno-linguistic diversity (Fragmentation) is very low on average (0.48), with Japan being the least fragmented (0.03) and Canada the most fragmented (1.29). The mean value of Openness indicates that imports of goods and services in the sample is 48.4% of GDP on average, Japan and the US being the countries with a lower level of imports, while Luxembourg shows values higher than 100%. In the case of System, most observations show presidential systems (84.85%) and 12.12% are parliamentary; only Estonia has an assembly-elected president. Finally, the Common variable indicates that 81% of the sample belongs to common-law countries.

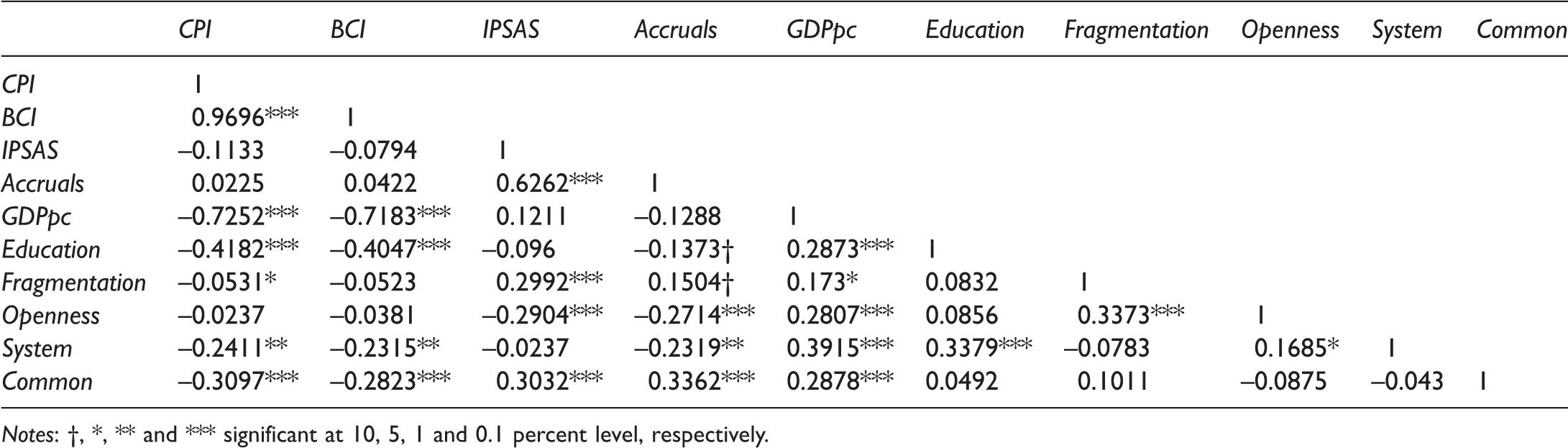

Table 2 illustrates the bivariate correlations. There are high correlations between the corruption variables, namely, CPI and BCI (0.9696), and also between IPSAS and Accruals (0.6262), suggesting that the two pairs of variables exhibit similar features. Therefore, each pair will be inserted in model 1 individually to estimate the β coefficients. The remaining correlations are relatively low, indicating no multicollinearity problems.

Bivariate correlations.

Notes: †, *, ** and *** significant at 10, 5, 1 and 0.1 percent level, respectively.

Empirical analysis

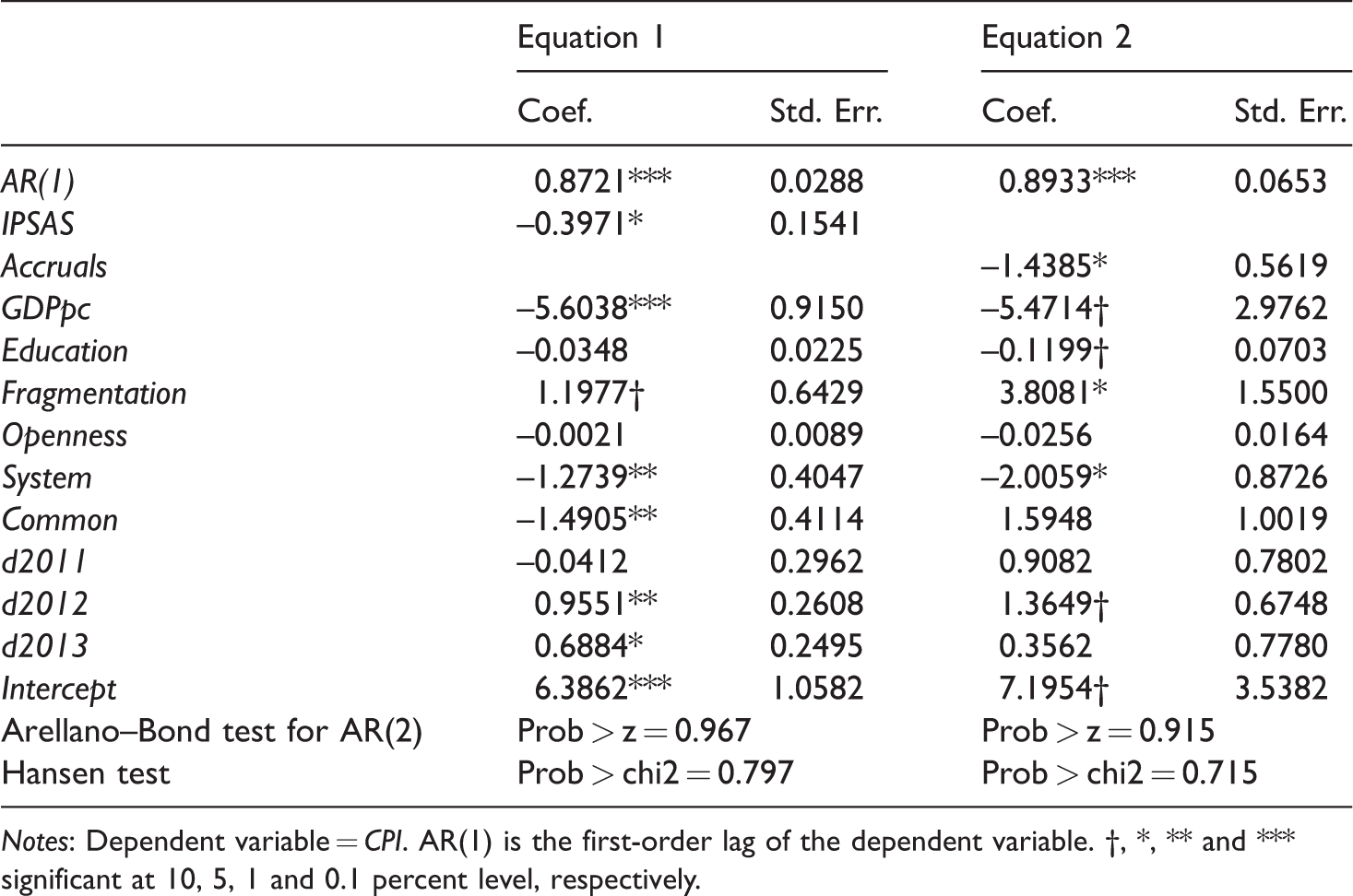

Tables 3 and 4 exhibit the empirical results obtained using the estimations of model 1, demonstrating the effects of the IPSAS (Equation 1) and Accruals (Equation 2) variables on CPI and BCI, respectively. The results of the instrument validity tests are shown at the bottom of each equation. Concretely, the p-value of the Arellano–Bond test for AR(2) suggests that we cannot reject the null hypothesis of ‘inexistence of serial correlation between the error terms’; similarly, the p-value of the Hansen test suggests that we cannot reject the null hypothesis of ‘validity of over-identifying restrictions’. Therefore, these results support the instrument validity.

Effect of public sector accounting on CPI.

Notes: Dependent variable = CPI. AR(1) is the first-order lag of the dependent variable. †, *, ** and *** significant at 10, 5, 1 and 0.1 percent level, respectively.

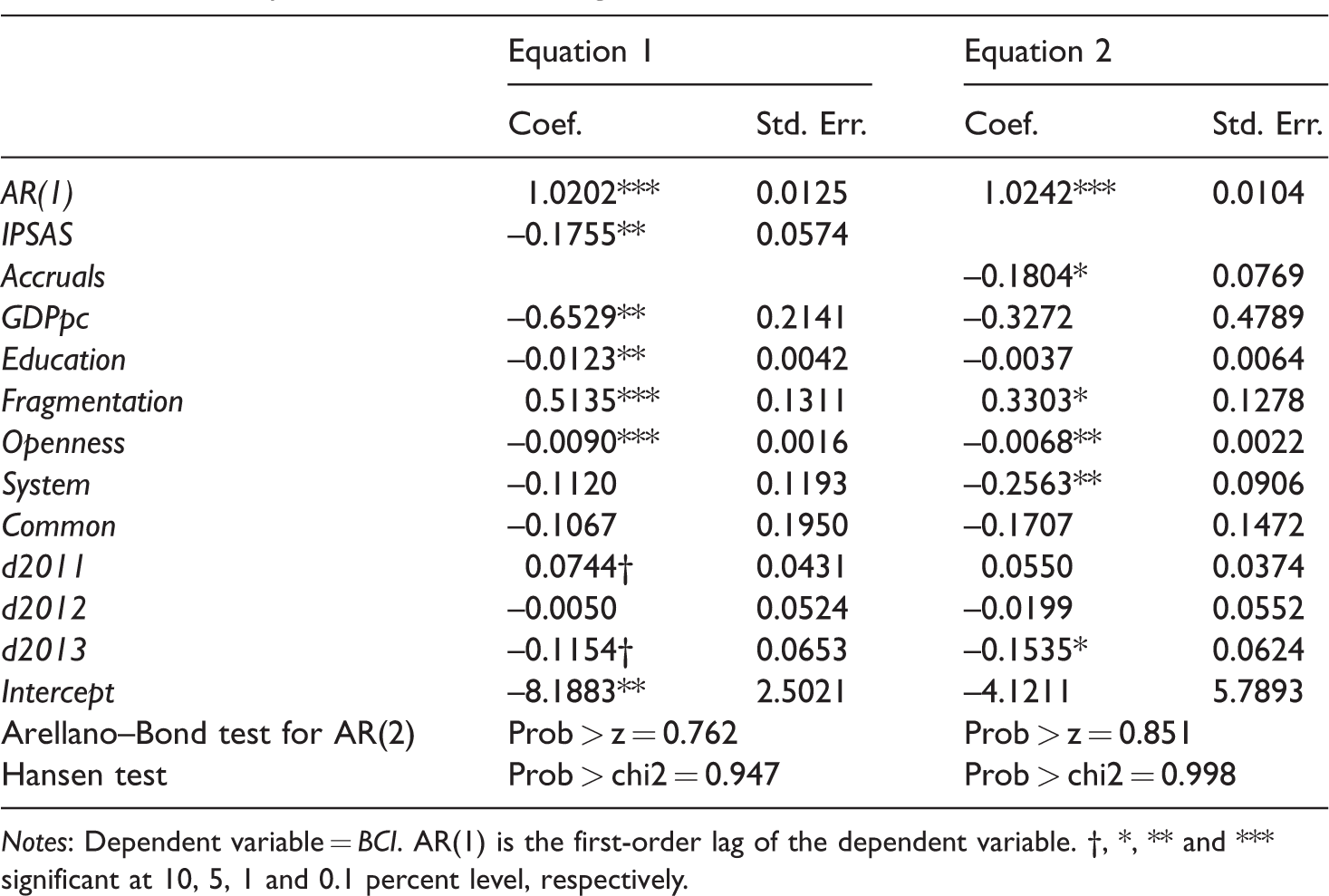

Effect of public sector accounting on BCI.

Notes: Dependent variable = BCI. AR(1) is the first-order lag of the dependent variable. †, *, ** and *** significant at 10, 5, 1 and 0.1 percent level, respectively.

Examining Table 3, both IPSAS and Accruals are statistically relevant and negatively impact on CPI, suggesting that corruption is reduced as governments progress in public-sector accounting harmonisation (variable IPSAS), and implement accrual-accounting systems (variable Accruals), which is in line with our hypotheses H1 and H2.

Regarding control variables, GDPpc and System impact negatively on CPI, while Fragmentation coefficients are positive. Education is statistically relevant only in Equation 2, negatively affecting CPI; Common is statistically relevant only in Equation 1, impacting negatively on the level of corruption; and Openness is not statistically relevant. These results indicate that corruption levels are reduced in more developed countries that have parliamentary political systems, better education rates and more ethno-linguistic homogeneity.

Similarly, Table 4 shows the effect of the same variables on BCI. Again, the IPSAS and Accruals variables negatively impact on the level of corruption, being statistically relevant. These results are in line with those previously obtained for CPI, so we can conclude that public-sector harmonisation, through IPSAS and standardisation by accrual-basis systems, can be a good option for controlling corruption in OECD countries.

Regarding control variables, the results are also similar to those previously obtained for CPI. GDPpc and Education impact negatively on BCI, although they are only relevant in Equation 1, while System is only relevant in Equation 2. The Fragmentation variable is positively associated with BCI, as was the case for CPI. Furthermore, Openness becomes statistically relevant, impacting negatively on the dependent variable in both equations, while Common has lost its relevance. These findings suggest that corruption levels are lower in countries with higher income levels and higher education levels, and that are more culturally homogeneous and more open to international trade; furthermore, parliamentary systems tend to reduce corruption levels.

Discussion and conclusions

Corruption is a significant problem, and many countries have adopted or are adopting incisive measures to reduce and prevent it. As public choice theory scholars claim (Mbaku, 2008), implementing specific institutional arrangements is needed in order to hold politicians accountable for their actions, reducing their opportunistic behaviour and the corruption level. Considering that corruption levels may decrease if the behaviour of politicians and public managers is more transparent (De Mingo and Cerrillo-i-Martínez, 2018), public-sector reforms that increase transparency would have a positive effect on reducing the level of corruption. Our findings corroborate the effect on corruption played by IPSAS and accrual-basis systems as they improve the quality of financial information, strengthening transparency.

Previous studies have largely investigated the effect of socio-economic and political factors on corruption (e.g. De Mingo and Cerrillo-i-Martínez, 2018; Lederman et al., 2005; Persson et al., 2003; Svensson, 2005; Treisman, 2000, 2007, 2014), so this study adds new insights into the role of public-sector accounting reforms. More concretely, it contributes to the academic debate concerning the institutional arrangements that should be implemented to reduce corruption and, more generally, the opportunistic behaviour of politicians. Indeed, IPSAS implementation and accrual-accounting adoption can reduce the information advantage of politicians towards citizens as more reliable and comparable information could stimulate politicians to act in the interest of citizens (Laswad et al., 2005; Oscarsson, 2008), according to the ‘pressure of competition’ axiom, rather than maximising their own well-being (Boyne, 1997).

In addition, this study contributes to the literature on the benefits of the modernisation of governmental accounting (e.g. Ball, 2012; Bergmann, 2012; Caba-Pérez and López-Hernández, 2009; Cohen and Karatzimas, 2015; Navarro-Galera and Rodríguez-Bolívar, 2011) by adding new benefits in terms of corruption. Furthermore, our findings contribute to the debate surrounding the effectiveness of both accrual-basis systems and harmonised accounting rules at an international level. Scholars have carefully examined the advantages and disadvantages of IPSAS and accrual systems, and several doubts have been raised (Oulasvirta, 2014). This study considers an additional perspective, highlighting that the level of corruption can be fought through the standardisation of accounting systems and the adoption of harmonised accounting principles.

However, this article is not free of limitations, which may be addressed in future studies. First, IPSAS and accrual-basis reforms are dynamic processes, so increasing the period of analysis could improve the reliability of the empirical results because it would then be possible to control for the lagged effects of IPSAS/accrual accounting on corruption. Second, we do not consider that international authorities (e.g. the World Bank or IMF) may force some countries to implement IPSAS. In that case, IPSAS implementation may be motivated by other reasons (e.g. providing better-quality information to investors or donors) than fighting corruption.

For future research, besides trying to overcome these limitations, it would be interesting to investigate the specific case of the European Public Sector Accounting Standards (EPSAS), focusing on European Union (EU) member states. The EC (2013: 8) noted that IPSAS implementation is not easy and proposed EPSAS, which are close to IPSAS but adapted to the specific needs of EU member states (Brusca et al., 2018). Furthermore, future studies could try to measure awareness of accrual-accounting and IPSAS implementation by citizens since it is necessary to acquire an effective understanding of increased comparability and standardisation. This issue is not easy to represent, but some advances have been made in the political science literature (e.g. Lindstedt and Naurin, 2010) that may be extrapolated to public-sector accounting.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.