Abstract

Rising student debt has sparked concerns about its impact on the transition to adulthood. In this paper, we examine the claim that student debt is leading to a rise in ‘‘boomeranging,’’ or returning home, using data from the National Longitudinal Survey of Youth 1997 Cohort and discrete time-event history models. We have four findings. First, student loan debt is not associated with boomeranging in the complete sample. However, we find that the association differs by race, such that the link between student debt and returning home is stronger for black than for white youth. Third, degree completion is a strong predictor of returning home, whereby those who fail to attain a degree have an increased risk of boomeranging. Fourth, young adult role transitions and socioeconomic well-being are associated with boomeranging. Findings suggest that rising debt has created new risks and may reproduce social inequalities in the transition to adulthood.

Leaving the parental home is a key marker in the transition to adulthood (Furstenberg 2010; Goldscheider and Goldscheider 1999) and a signal for economic independence (Sironi and Furstenberg 2012). But recently, scholars have become concerned with reversibility of the transition to adulthood (Shanahan 2000), and the phenomenon of “boomeranging”—whereby young adults return home after attaining residential independence (Goldscheider and Goldscheider 1999). Dubbed “the boomerang generation” (Parker 2012), the most recent cohort of young adults is returning home at a faster rate than previous cohorts. Although research has begun to interrogate the causes and consequences of boomeranging (Goldscheider and Goldscheider 1999; Sassler, Ciambrone, and Benway 2008; South and Lei 2015; Stone, Berrington, and Falkingham 2014), relatively little is known about this shift in the transition to adulthood, particularly among college-going youth.

Many have argued that the rapid increase in student debt explains the recent rise in boomeranging among young people (Bleemer et al. 2014; Davidson 2014). While these arguments raise important questions, there is little evidence regarding the link between debt and boomeranging. Moreover, despite a growing and diverse college-going population and a large proportion of college goers that leave college without a degree (Buchmann and DiPrete 2006), no research to date has examined how postsecondary educational (PSE) experiences are linked with boomeranging.

In this study, we ask whether student debt is associated with boomeranging among a cohort of college-going young adults. Specifically, we test three distinct claims: first, that student debt hastens boomeranging, because it creates social and economic difficulties for youth; second, that there is heterogeneity in the association between debt and boomeranging by race; third, that failing to complete college, not student debt, creates difficulties in young adulthood and leads youth to boomerang.

Literature Review

The transition to adulthood—the period of life when young people exit adolescent social roles and enter adult social roles, such as full-time employment, marriage, and residential independence—has undergone dramatic changes over the past several decades (see Shanahan 2000 for review). Chief among these changes is that young adults delay entry into traditional adult roles, in part because they spend more time in PSE institutions (Furstenberg 2010). This is reflected in the dramatic expansion of higher education throughout the twentieth and twenty-first centuries, as changes in the structure of the labor market have made it necessary for youth to pursue a college degree to obtain middle-class jobs (Danziger and Ratner 2010). From 1967 to 2012, the percentage of 18- to 24-year-olds enrolled in college increased nearly 61 percent, from 25.5 percent to 41 percent (National Center for Education Statistics 2013b). Simultaneously, the cost of higher education increased and student aid stagnated, leading students and their families to take on historic levels of debt to fund college-going. Student debt has doubled in the past decade, topping $1 trillion in the aggregate, with the average college graduate debtor owing $30,000 (Federal Reserve Bank of New York 2013; Project on Student Debt 2011).

Rising debt levels have fueled scholarly and public concern about the potential impact of student debt on the well-being of young adults, though findings have been mixed (Addo 2014; Dwyer, McCloud and Hodson 2011; Houle and Berger 2015; Nau, Dwyer, and Hodson 2015). Recently, scholars have expressed concern that rising student debt is contributing to the boomerang generation of young adults returning home. Estimates of boomeranging vary, with recent studies reporting that between 20 percent and 50 percent of young adults return home after leaving (Parker 2012; Sandberg-Thoma, Snyder, and Jang 2015; South and Lei 2015; Stone et al. 2014). Indeed, the percentage of young adults who boomerang at least doubled over the course of the twentieth century (Goldscheider et al. 1999; Goldscheider and Goldscheider 1994, 1999). And recent reports suggest that the rise in boomeranging is particularly pronounced among college-going young adults (Stone et al. 2014), who are struggling with student debt and have diminished labor market prospects in the wake of the Great Recession (Dettling and Hsu 2015; Fry 2015). Below, we review existing research and theories centered around three distinct claims regarding the link between student debt and boomeranging: (1) that student debt hastens boomeranging, (2) that this association is stronger for black than for white youth, and (3) that college completion, not debt, is the key predictor of boomeranging. These claims are summarized graphically in Figures 1 through 3.

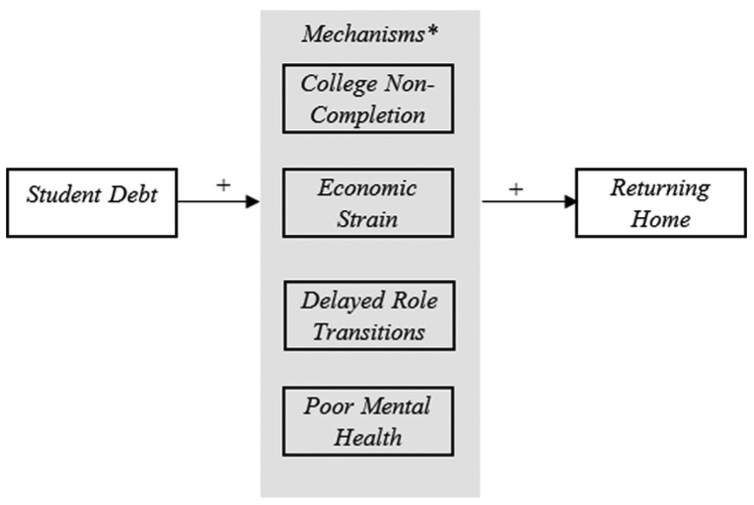

Theoretical associations between student debt, college completion, and boomeranging: Student debt increases the risk of boomeranging.

Theoretical associations between student debt, college completion, and boomeranging: Student loan debt more burdensome for blacks than whites.

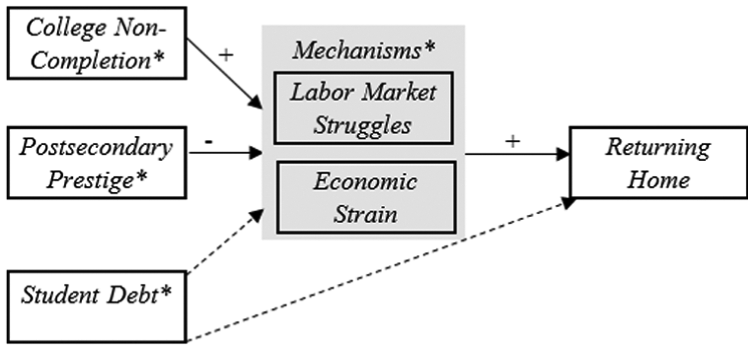

Theoretical associations between student debt, college completion, and boomeranging: College completion and postsecondary characteristics more important for boomeranging than debt.

Student Debt and Boomeranging: Evidence and Mechanisms

That student debt is leading a generation of young people back home is a compelling, plausible hypothesis: when young people leave home, debt payments may become burdensome—particularly given that this type of debt cannot be discharged in bankruptcy—and debt may lead to other pernicious outcomes that hasten a return home. Below, we consider four (nonindependent) pathways through which debt may influence boomeranging: economic strain, college completion, delayed transition to adulthood, and youth well-being.

First, student debt may lead young people to boomerang because it creates economic strain as they struggle with payments. Life course scholars find that economic strain is an important proximate determinant of boomeranging among young adults (Goldscheider and Goldscheider 1999), suggesting that student debt may increase the risk of boomeranging to the extent that debt is tied to economic strain. For example, becoming unemployed and declines in wages increase the risk that young adults boomerang (South and Lei 2015; Stone et al. 2014). Just as wages and unemployment are predictive of boomeranging, high debt loads among college-going youth may be an important contemporary indicator of economic distress, whereby those struggling with debt face a heightened risk of boomeranging.

Relatedly, student debt may lead to boomeranging if it interferes with degree attainment. High debt burdens are associated with an increased risk of dropping out of college (Dwyer et al. 2011). Although there is no evidence of the link between degree attainment and boomeranging, young people who leave college without a degree face higher unemployment rates and lower wages than college graduates (Cellini and Chaudhary 2014; Lang and Weinstein 2013) and thus may be at a higher risk for boomeranging.

Third, student debt may increase the risk of boomeranging because it leads to delays in other adult role transitions. For example, young adults with high student debt are less likely to transition from cohabitation to marriage (Addo 2014), and high debt is also associated with delayed fertility (Nau et al. 2015). Boomeranging research shows that delays in such transitions—as well as union dissolution, leaving college, and nonmarital pregnancy—are associated with an increased risk of returning home (Sandberg-Thoma et al. 2015; South and Lei 2015; Stone et al. 2014).

Finally, the association between debt and boomeranging may operate through youth well-being. Student debt is linked to poor young adult mental health (Walsemann, Gee, and Gentile 2015), and young people with emotional problems are more likely to boomerang (Sandberg-Thoma et al. 2015). To the extent that student debt affects emotional well-being, this may be a mechanism through which student debt affects boomeranging.

In sum, the above arguments, summarized in Figure 1, suggest that we would expect to find a bivariate (positive) association between student debt and boomeranging, and this association should be partially or fully mediated by young adult economic circumstances, college completion, transition to adulthood status, and youth well-being.

Few studies examine the link between student debt and boomeranging, with the exception of two reports produced by the Federal Reserve Board. Dettling and Hsu (2015) use credit-report data to show that student debt is positively associated with boomeranging and that this association is larger for subprime borrowers. While the study provides important evidence of the relationship between student debt and boomeranging, it is limited in several ways. First, the credit-report data omit nondebtors (those without credit reports). Second, the credit-report data lacks information on individual-level socioeconomic and PSE characteristics, which are crucial to fully understand the association between debt and outcomes (Houle 2014). Third, residence with parents is largely inferred using mailing addresses and differences in ages among individuals living in a household rather than directly identifying parent–children pairs or using respondent reports of residence. Another study (Bleemer et al. 2014), using aggregated data from credit reports, finds that state-level debt loads are associated with state-level rates of co-residing with parents. These studies, while illustrative, do not directly measure boomeranging at the individual level, do not include nondebtors with no credit history, and do not consider individual-level mechanisms and confounders of the association between debt and boomeranging. Our study, which utilizes longitudinal individual-level survey data of a nationally representative sample, allows us unique leverage regarding this question.

Student Debt and Boomeranging: Variation by Race

While the above argument implies that student debt may be uniformly negative for young adults, other scholars have argued that debt may be more burdensome for some groups than for others and may have differential consequences across groups, particularly by race. Research in this vein shows student debt may be more burdensome and difficult to repay for black young adults than for white young adults for two key reasons. First, black young adults have significantly higher debt burdens than whites (Cunningham and Santiago 2008; Houle 2014; Jackson and Reynolds 2013), such that blacks are both more likely to borrow, owe $5,000 to $10,000 more than white debtors, and are more likely to default on loans (Houle 2014; Huelsman 2015; Jackson and Reynolds 2013). Second, black young adults experience greater hardship and discrimination, making debt more burdensome to repay and leading debt to have more pernicious consequences.

Discrimination in credit, college, and labor markets is a key mechanism by which debt becomes more burdensome (and difficult to repay) for blacks than for whites. Although student debt is often used by black students to bridge the gap between family resources and the rising costs of college, black youth are more likely to have private loans, which carry high and variable interest rates, have high fees for deferment and forbearance, and offer less protection for borrowers than federal loans (Goldrick-Rab, Kelchen and Houle 2014; Project on Student Debt 2014). In this way, the student loan market is not unlike the mortgage market, in which blacks often lack access to fair credit and instead are more likely to have access to predatory, high-interest loans that are difficult to repay (Williams, Nesiba, and McConnell 2005). Black youth also have more difficulty repaying loans due to discrimination and hardship in the college market. For example, black young adults are often funneled toward predatory for-profit institutions and underfunded schools, which offer fewer labor market benefits and have high dropout rates (Ruch 2001). Finally, even among college graduates, black youth experience discrimination in the labor market. They are less likely to obtain job offers and often receive offers for lower-paying positions with fewer options for career advancements than their white counterparts (Gaddis 2015). More broadly, black–white disparities in earnings, employment, and wealth are observable in young adulthood (Cancio, Evans, and Maume 1996; Zhang 2008), and due to their precarious economic position, black youth may have more difficulty repaying student debt after leaving college.

Additionally, recent evidence suggests that student debt has more negative consequences for black youth than for white youth. For example, 69 percent of blacks who drop out cite student debt as a primary reason for not completing their degree, compared to 43 percent of white students (Johnson, Van Ostern, and White 2012). After leaving college, blacks also report being significantly more concerned about being able to afford student loan payments than whites (Ratcliffe and McKernan 2013) and have more difficulty paying off equivalent amounts of debt than white young adults (Addo, Houle, and Simon 2016), which may be a result of the higher interest rates and lower labor market returns to a college degree they commonly experience. That is, black young adults not only face higher debt burdens than their white counterparts, and are thus exposed to greater risks in their college experience, but they also experience fewer rewards to a college degree (Addo et al. 2016). This suggests that to the extent that student debt creates economic strain that drives young people back to the parental home, the impact of student debt on boomeranging may be stronger for blacks than it is for whites, as summarized in Figure 2. Although one could reasonably hypothesize that the consequences of debt may vary by other characteristics (such as gender or class), we focus on race because (1) black–white differences in debt are substantially larger than gender and socioeconomic background in debt (Addo et al. 2016; Houle 2014), and (2) the burden of student loan debt is uniquely racialized, for the reasons stated above. 1

A Completion Crisis, Not a Debt Crisis: Implications for Boomeranging

A third claim in the literature is that college completion and subsequent labor market attachment better explain the rise in boomeranging than does student debt. While many argue student debt has disastrous consequences, other scholars argue that the student debt crisis is not a debt crisis but a degree completion and for-profit crisis (Dynarski 2015; Dynarski and Kreisman 2013; Looney and Yannelis 2015). That is, those who are struggling with loan repayment are not struggling because they carry high loan balances but because they leave college without a degree and attend institutions with low completion rates and fewer labor market benefits, such as for-profits and two-year institutions (Akers and Chingos 2016). For example, Houle and Berger (2015) challenge recent claims that student debt is dragging down the housing market, finding only a trivial association between student debt and home ownership outcomes. Instead, they find that degree completion is a stronger predictor of home ownership. Indeed, recent estimates suggest that student debt may not be as burdensome as is suggested in popular discourse. For example, the median student debtor pays only 3 to 4 percent of their monthly income on student loan payments, a figure that has remained relatively constant since the early 1990s (Akers and Chingos 2016). As such, degree completion may be a stronger predictor of boomeranging than student debt, ceteris paribus. Unlike the above argument, which suggests that college completion and PSE characteristics may mediate the link between student debt and boomeranging, this argument suggests that PSE characteristics and completion are independent predictors of boomeranging and implies that debt is not a culprit in the rise of boomeranging.

This argument dovetails with sociological research on higher education. While access to PSE in the United States has increased over the twentieth century, these institutions have also become more stratified and diverse in ways that exacerbate inequality (Dwyer, McCloud, and Hodson 2012). Much of the growth in higher education has been in two-year and lower-tier institutions (such as for-profits) that primarily cater to disadvantaged students (Roksa et al. 2007). While attending such institutions may serve as a steppingstone for upward mobility, graduation rates at these institutions are significantly lower than at traditional four-year nonprofit institutions. Indeed, only 31 percent of students at two-year institutions (National Center for Education Statistics 2013c) and 23 percent of students at four-year for-profit institutions graduate within 150 percent of normal time (National Center for Education Statistics 2013a), and those who do not complete their degree do not experience the labor market benefits associated with a college degree (Hout 2012). Moreover, graduates of these institutions tend to have lower-status and lower-wage jobs than four-year nonprofit college graduates, suggesting that degrees from these types of institutions do not confer the same benefits as four-year degrees from public and private nonprofit institutions (Cellini and Chaudhary 2014; Lang and Weinstein 2013). Given that noncompletion and low-status PSE institutions are linked with fewer social and economic rewards, these factors may be important predictors of boomeranging, as summarized in Figure 3.

Recent research provides suggestive, but not conclusive, evidence that college degree completion is associated with returning home, and no research has yet explored how PSE characteristics are linked with boomeranging. South and Lei (2015) find some support for the above argument and show that leaving college is associated with an increased risk of returning home. Similarly, Stone et al. (2014) find that young adults transitioning out of school and into the labor market in England have a higher risk of returning home than young adults who are stably employed. However, these analyses conflate leaving school with degree completion, and thus it is not clear whether there are differences in risk of returning home by completion status. Moreover, both studies include young adults with less than or equal to a high school degree who never attended college in their reference group, thus raising further questions about whether noncompleters are more likely to return home than degree completers. Thus, the link between student debt, college completion, PSE characteristics, and returning to the parental home is unclear.

In sum, in this study we test three claims regarding the impact of student debt on boomeranging; first, that student loan debt is associated with an increased risk of boomeranging; second, that this effect is stronger for black youth, for whom debt is more burdensome; and third, that college completion, rather than debt, is most germane to boomeranging. In doing so, we contribute to two distinct literatures on the consequences of student debt and young adulthood, as well as to research on the changing transition to adulthood, by examining the link between student debt, college completion, and the changing landscape of the transition to adulthood.

Data and Methods

Data

Data for this study are drawn from the National Longitudinal Study of Youth 1997 Cohort (NLSY-97). The NLSY-97 is a nationally representative sample of 8,984 respondents born between 1980 and 1984. Survey respondents have been interviewed yearly since the original round of data collection in 1997 except for a two-year gap between the 2011 and 2013 waves. The NLSY-97 data are particularly well suited for our analyses because the panel follows a recent cohort of youth that hold historically high levels of student loan and consumer debt during their transition into adulthood. We restrict the original sample of 8,984 respondents in several ways. First, we limit our analysis to respondents who ever attended college, and thus were at risk to accumulate student debt (n = 5,615). Second, for the main analysis, we keep only those college-goers who achieve residential independence (n = 5,063), eliminating those respondents who fail to launch. 2 Third, we drop 32 respondents who report living independently or returning to the parental household before the start of the data series. Fourth, we drop six college-goers who report returning to the parental household before they reported living independently (n = 5,025). We then restructure the data into a person-wave format (person-waves = 90,468) and drop all observations following a return to the parental household (n = 5,025; person-waves = 31,731). To account for missing data, we use multiple imputation using the ICE command in Stata 14.0 (Royston 2005). Multiple imputation is a more efficient and less biased strategy for dealing with missing data than listwise deletion (Lee and Carin 2010). The procedure iteratively replaces missing values on all variables with predictions based on random draws from the posterior distributions of parameters observed in the sample, creating multiple complete data sets (Allison 2001). We average results across 15 imputation samples and account for random variation across samples to calculate standard errors (Royston 2005). The multiply imputed results presented here are similar to results seen when using listwise deletion.

Measures

Boomeranging

Prior research has relied on annual household rosters to measure exits from and returns to the parental household (see Sandberg-Thoma et al. 2015; South and Lei 2015). Respondents are considered residentially independent when a parent no longer appears on the household roster, and boomeranging is coded as 1 if a respondent who becomes residentially independent later reports a parent on the household roster. We argue that such a measure is not ideal for a college-going population. First, the NLSY asks only about one’s current household, which may bias estimates for populations whose current or usual residence is ambiguous, such as college-going youth (Martin 1999, 2007). Relatedly, many youth report their parents on the household roster while enrolled in college and living on campus (Thompson 2014), which creates measurement error. Finally, shorter spells of residential independence (especially those lasting less than one year) are not captured by the annual household roster. For these reasons, the Bureau of Labor Statistics has not relied on household roster measures in the NLSY when examining boomeranging (Dey and Pierret 2014).

A measure based on respondents’ own reports of their residential independence is preferable. Starting in 2003, NLSY-97 respondents were asked retrospective questions about the month and year in which they first exited and the month and year they returned to the parental home (if applicable). 3 After 2003, respondents are asked about these transitions at every subsequent wave. As part of this question, respondents are given a direct definition of living on their own and are asked if they have ever established their own household for at least three months. 4 Those who lived independently are then asked if they ever returned to the parental household for a period of at least three months and, if so, the month and year when that occurred. 5 Residentially independent respondents are coded as 1 in the year they report moving back home. This measure is less biased than the household roster measure for several reasons. First, respondents are asked specifically about residential transitions, rather than inferring the transitions from the household roster of one’s implied current residence. Second, the measure avoids bias associated with shorter-term living situations (such as dorms or residential spells in college) because respondents are first prompted with a definition of permanent housing: “Sometimes people live in places temporarily while attending school or working a job or for some other reason, but they consider their permanent residence to be elsewhere. Do you consider the place you are currently living to be your permanent house?” (Bureau of Labor Statistics 2013). Because they are prompted with a clear definition of permanent housing, respondents are less likely to consider short-term or temporary moves when discussing their boomeranging history (Martin, Fay, and Krejsa 2014). Third, because respondents report the month and year of each transition, we can capture exits and returns that last less than one year. This is an important group, as nearly 11 percent of residentially independent respondents who return home do so in the first year. By asking youth specifically about their residential independence that is not temporary, we get a direct, rather than in indirect, measure that is likely less biased than the household roster measure (Dey and Pierret 2014). However, one potential shortcoming of our measure of boomeranging is that respondents are asked if they “move[d] in with their parents or someone else’s household” (Bureau of Labor Statistics 2013). Because that someone else could conceivably be a romantic partner, we include controls for cohabitation and marital status in our analysis. To the extent that this boomeranging measure captures moves with other family members, this likely reflects family structure variation in the United States. Given the variety of family structures in the United States, we contend that moving in with other relatives (rather than parents) is conceptually similar to boomeranging. However, as an additional robustness check, we construct a boomeranging measure based on the household roster and briefly report these findings below.

Student debt

Our focal independent variable is student debt. Respondents are asked questions about types and amounts of debt holdings and assets, including student debt, at approximately ages 20, 25, and 30 as part of the NLSY debts and assets modules (YAST). We then adjust debt for inflation and standardize it to reflect 2010 dollars using the Consumer Price Index Research Series (Bureau of Labor Statistics 2010). While accuracy of self-reported debt data is a concern, evidence shows that borrower self-reports and credit reports are extremely similar for nearly all forms of debt, including student debt (Brown et al. 2011). We use linear interpolation to impute debt between YAST modules and include the natural log of this measure in our empirical models. 6

Covariates

We include an array of time-invariant and time-varying covariates in our models that may confound, suppress, or mediate the link between student debt and boomeranging. Because sociodemographic background is associated with debt accrual (Houle 2014) and boomeranging (South and Lei 2015), time-invariant controls include race (white [referent], black, and other), sex (female [referent], male), region of residence at baseline (Northeast [referent], North Central, South, West), parents’ highest education in 1997 (≤ high school degree [referent], some college, four-year college degree or higher), parental wealth in 1997 (coded in thousands of constant 2010 dollars), number of siblings in household at baseline, and family structure in adolescence (two-parent biological [referent], single parent, stepfamily, other family structure). We also capture parental attachment, which may suppress the association between debt and boomeranging, through questions about a respondent’s relationship with his or her parents. Respondents are asked the extent to which they agree with the following statements regarding their parents (measured on a 5-point Likert agree/disagree scale): (1) I think highly of him/her, (2) He/she is a person I want to be like, and (3) I really enjoy spending time with him/her. We take the average of a respondent’s responses for each question and create a time-stable parental attachment scale by combining the measures into a single summed scale.

We also control for an array of time-varying variables that reflect annual measures of respondents’ PSE experiences and their social and economic characteristics as young adults. This is important, as young adults who consume more PSE (attend longer or attend more expensive schools) accrue more debt than those who consume less PSE, and PSE characteristics may suppress the association between debt and boomeranging (Houle 2014). In addition, degree completion may be a mediator or independently predict boomeranging (noted above). PSE characteristics include degree pursued and attained (graduate school with degree attained [referent], graduate school with no degree, four-year institution with degree attained, four-year institution with no degree, two-year institution with degree attained, two-year institution with no degree attained), current enrollment status (not enrolled [referent], currently enrolled), number of years enrolled in college, percentage of years enrolled full-time, percentage of years enrolled in a private institution, a weighted average of the sticker price of the cost of institutions attended over the respondents’ postsecondary career, and a dummy indicator of whether the respondent ever attended a for-profit institution.

To test whether delays in the transition to adulthood mediate any association between debt and boomeranging, we control for annual measures that reflect a youth’s life stage, including age, marital and relationship status (never married/single [referent], cohabiting, married, divorced or separated), and parental status (childless [referent], has a biological child). In addition, because young adults’ economic resources are likely to reflect their ability to pay down their debt and may mediate the association between debt and boomeranging, we control for full-time employment (1 = yes) and wages (measured in 2010 dollars and transformed using a natural logarithm). To the extent that emotional problems spurred by student debt may drive young adults back home, we also adjust for problem drinking and emotional distress. Problem drinking is an annual dichotomous measure coded 1 if respondents reported binge drinking in the past 30 days (five or more drinks in one sitting) or reported drinking before school or work. Emotional distress is measured biannually (2000, 2002, 2004, 2006, 2008, and 2010) with a composite score of the amount of time respondents reported (1) being nervous, (2) feeling calm and peaceful (reverse coded), (3) feeling downhearted/blue, (4) being a happy person (reverse coded), and (5) feeling so down that nothing could cheer them up. Higher scores indicate greater emotional distress. Survey waves where these indicators are not measured were backfilled from the next available wave.

We also adjust for contemporaneous conditions in young adulthood that are correlated with and may confound the link between debt and boomeranging. To account for the recessionary period— which was associated with a rise in student debt and boomeranging—we include a dummy coded 1 for survey years 2007 to 2010 and 0 for all other years. To ensure our estimates of student debt and boomeranging are not biased by other forms of debt that are correlated with student debt, we control for mortgage debt (1 = yes, 0 = no) and the natural log of reported consumer debt (auto and unsecured) recorded at each YAST module. To the extent that parental support suppresses the association of interest (above and beyond parental attachment), we control for instrumental support with a dichotomous indicator coded 0 if respondents got no support from parents and 1 if respondents received financial support (other than an allowance) in the past year. We also control for urban residence (nonurban [referent], urban).

Analytical Strategy

Over 85 percent of the NLSY-97 sample reported living independently at some point. Those who did not were omitted from the analyses, and among those who did, their observation period starts in the year they first report living independently. The time series for residentially independent respondents end (are censored) when they either return to their parental household or reach the end of the survey period. Because our data are in yearly intervals, we use discrete time proportional hazard models as opposed to Cox regression models. We conducted exploratory analyses to determine the proper functional form of the baseline hazard. Among the various options, including linear time since independence and nonlinear time since independence, a fully nonparametric model (with dummy variables for time) was the best fit for the data. To maintain temporal ordering of the dependent and independent variables, we set up our models such that independent variables at time t predict boomeranging at time t + 1. As such, all independent variables (including interpolated debt) are measured at the same point in time (time t). 7 We use Stata v.14 and standard errors are clustered by respondent to adjust for nonindependence of observations across time.

Results

Descriptive Statistics

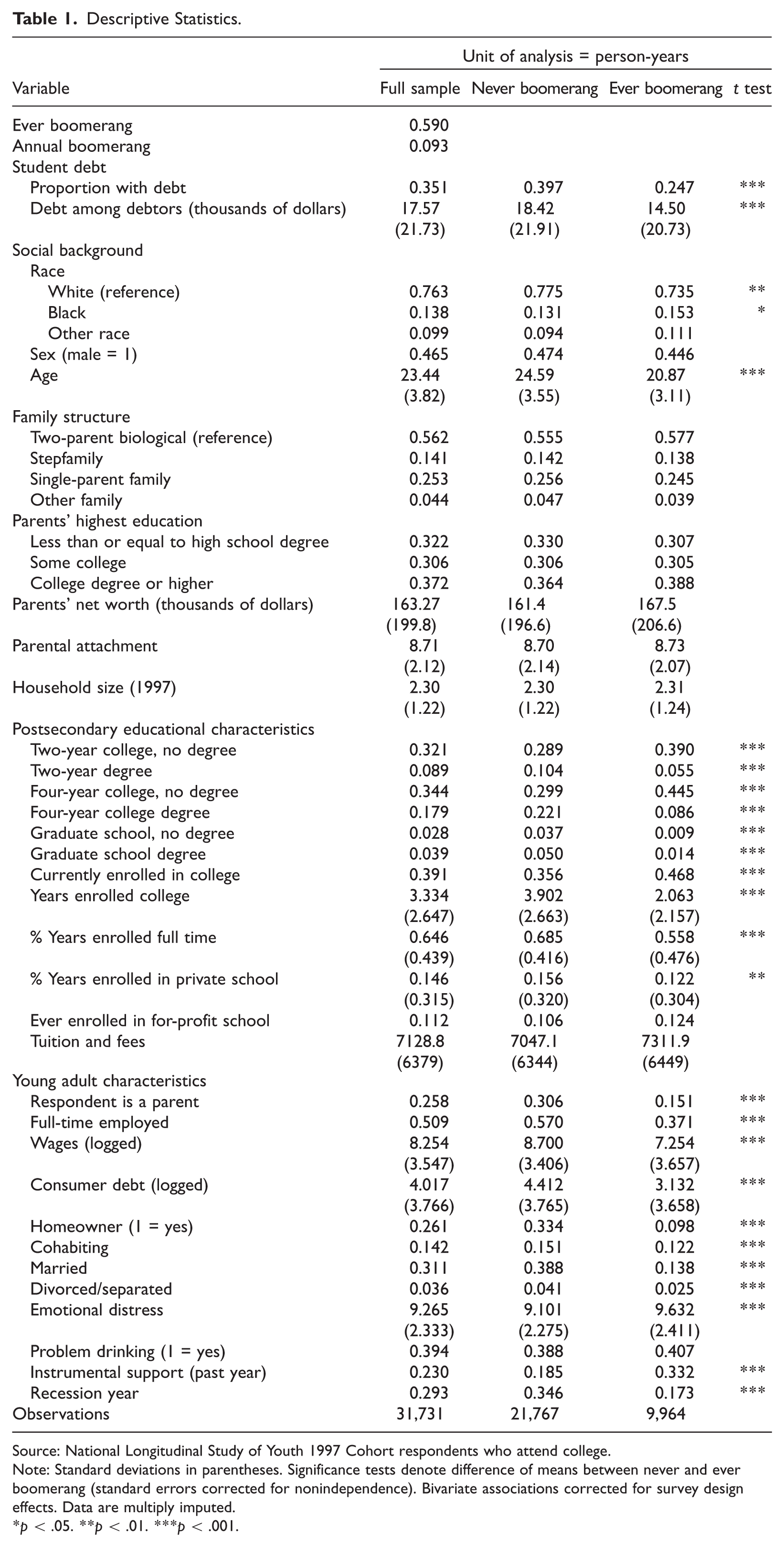

We present descriptive statistics for the full sample and by boomerang status in Table 1. The means and standard deviations in Table 1 are interpreted as averages across all residentially independent person-year observations. Among those who become residentially independent, 59 percent report they boomerang (9.3 percent annually). Notably, if we were to measure boomeranging based on the household roster, only 39 percent of residentially independent respondents would be classified as boomerangers, suggesting that the household roster underestimates boomeranging. This is likely due to household rosters missing short-term moves. Aligning with this, the risk of boomeranging is highest in the first two years of independence (11 percent in the first year and 23 percent in the second year) and then declines precipitously.

Descriptive Statistics.

Source: National Longitudinal Study of Youth 1997 Cohort respondents who attend college.

Note: Standard deviations in parentheses. Significance tests denote difference of means between never and ever boomerang (standard errors corrected for nonindependence). Bivariate associations corrected for survey design effects. Data are multiply imputed.

p < .05. **p < .01. ***p < .001.

Average student debt among debtors in this sample is $17,570. While this figure is lower than the national average, this is because it represents average debt for all person-years since the respondent becomes residentially independent. For comparison, average debt among debtors is $12,777 at YAST-20, $22,358 at YAST-25, and $25,397 at YAST-30, which is consistent with national estimates (Houle 2014).

We find several key differences across respondents by boomerang status. Contrary to our expectations and the dominant narrative, young adults who boomerang report significantly less student debt than those who do not return home. Young adults who boomerang are also more likely to be younger, to be black, and to have lower PSE attainment and are less likely to attain a degree and more likely to attend for-profit institutions. In young adulthood, boomerang respondents are less likely to have transitioned to adult roles (marriage, parenthood), have lower socioeconomic status than their counterparts (lower wages, lower employment), and experience more emotional distress. Overall, the descriptive statistics in Table 1 confirm recent research showing that young adult characteristics are tied to boomeranging but do not support the overall expectation that student debt is driving young adults back to the parental home. Indeed, the bivariate association shows just the opposite—those who boomerang carry less student debt than those who do not. To further interrogate this association, we turn to a series of discrete time event history models predicting boomeranging among college-going young adults.

Discrete Time Event History Models

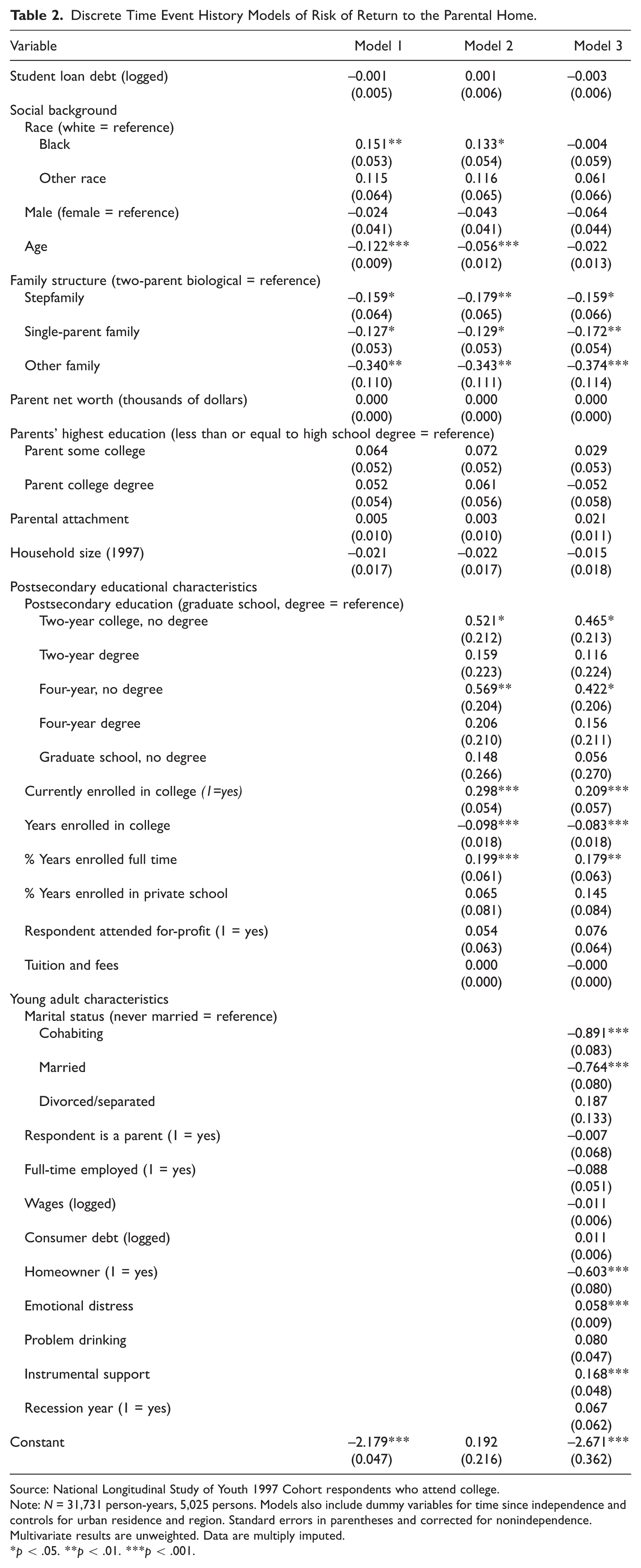

In Table 2, we show results from a series of discrete time event history models. In Model 1 we show the relationship between logged student debt and the hazard of returning home, controlling only for the baseline hazard (captured with dummy variables for each residentially independent observation, but not shown) and sociodemographic background variables. In Model 2 we add PSE characteristics. We then add young adult characteristics in Model 3.

Discrete Time Event History Models of Risk of Return to the Parental Home.

Source: National Longitudinal Study of Youth 1997 Cohort respondents who attend college.

Note: N = 31,731 person-years, 5,025 persons. Models also include dummy variables for time since independence and controls for urban residence and region. Standard errors in parentheses and corrected for nonindependence. Multivariate results are unweighted. Data are multiply imputed.

p < .05. **p < .01. ***p < .001.

Across all models in Table 2, we find no evidence that student debt is associated with an increased risk of returning to the parental home. Indeed, the negative association observed in Table 1 is completely explained by sociodemographic background variables. As such, we find no evidence to support popular claims that student debt is driving young people back home.

In Model 2, we find support for claims that completion, rather than debt, may be driving people home, as postsecondary degree completion is a strong predictor of returning home. Young adults who pursue a two-year or four-year degree but do not complete the degree have the highest risk of returning home. In Model 3, comparing completers to noncompleters in their appropriate reference group, two-and four-year noncompleters have over 40 percent higher risk of returning home than their counterparts in similar institutions who complete their degree (two-year: exp..521-.159 = 1.43; four-year: exp..569-.206 = 1.44; p < .05). Moreover, this association is partially explained by young adult social and economic characteristics in Model 4, suggesting that degree noncompletion increases boomeranging in part because it creates economic and social strain.

Young adult social and economic characteristics are also associated with returning to the parental home, and these patterns are in line with recent research. Young adults who have transitioned into adult roles, such as cohabiting or marital relationships, are significantly less likely to return home, as are homeowners. While wages and employment status are not significant predictors of boomeranging, the coefficients are in the expected direction, and these associations are significant when not controlling for the marital/relationship status variables.

So far we have shown that student loan debt is not associated with boomeranging and instead find that college completion is a strong determinant of returning home. However, student debt may be more burdensome for blacks than for whites and thus have a stronger association with boomeranging for this group. We test this in Table 3 by interacting race with student debt.

Discrete Time Hazard Models Predicting Return to the Parental Home.

Source: National Longitudinal Study of Youth 1997 Cohort respondents who attend college.

Note: N = 31,731 person-years, 5,025 persons. Models also include dummy variables for time since independence and controls for urban residence and region. Standard errors in parentheses and corrected for nonindependence. Multivariate results are unweighted. Data are multiply imputed.

p < .05. **p < .01. ***p < .001.

In Table 3, we find support for the argument that debt is more strongly associated with boomeranging for black youth than it is for white youth. Given the specification of the interactions, the main effect of student debt in Model 1 represents the effect of debt on returning home among white respondents with debt, and the reference category is white respondents with no debt. The race coefficients represent the risk of returning home for black and other-race respondents who have no debt, and the interaction terms represent the effect of debt on returning home among racial-minority respondents. The results in Table 3 suggest that the association between student debt and boomeranging is stronger for black young adults than it is for white young adults. In Model 3, a 10 percent increase in student debt is associated with a 20 percent increase in the risk of boomeranging among blacks, but an equivalent increase in debt has essentially no effect for whites. Interestingly, this interaction is reduced below conventional levels of statistical significance (but is still positive, p < .07) after adjusting for young adult social and economic characteristics. This suggests student loan debt is more burdensome and has greater consequences for black youth than for white youth, and this is in part due to economic and social struggles in young adulthood. Additional models that use categories of debt (no debt, low debt [<$15,000], midlevel debt [$15,000–$30,000], high debt [>$30,000]) reveal that while the magnitude of the interaction effect is large for all debt categories, it is statistically significant for the low-debt group only—suggesting that small amounts of debt are significantly associated with increased risk of boomeranging for black college-goers. This supports recent literature that suggests those who struggle most with loans (and are at high risk of default) have relatively low balances (Dynarski 2015), though we would caution that the effect sizes are large at higher debt levels but may have failed to reach statistical significance due to small sample size.

Additional Analyses

We conducted additional analyses to test the robustness of our findings and to further examine plausible sources of heterogeneity in the association between student debt and boomeranging. One explanation for the null debt findings in the full sample is that debt is preventing youth from becoming residentially independent, which would bias its association with boomeranging toward zero. To test this, we show results from models that predict the risk of residential independence in the appendix. We find that debt is positively associated with leaving home but that this coefficient is reduced to nonsignificance when we adjust for postsecondary educational experience. As such, we find little evidence that student debt is leading to a “failure to launch,” and thus that is unlikely to bias our main findings.

Another concern is that there may be some heterogeneity among young adults who boomerang, such that some young adults are “slowly detaching” and temporarily moving in and out during and after college, while others are returning home for longer periods of time after attaining independence (who we might refer to as “true boomerangers”). 8 To examine this, we use the household roster to construct a residential history that measures the number of times that respondents enter and leave the parental household. Of those who do boomerang, almost 80 percent return to the parental home only once. Furthermore, fewer than 3 percent of those who boomerang leave and return three or more times. This, coupled with our self-report measure that prompts respondents to consider permanent rather than temporary housing, suggests that this is unlikely to bias our findings.

Moreover, our results are consistent across additional measures and operationalizations of debt, such as the annual measures of outstanding student debt reported when respondents are enrolled in college and when limiting our measure of debt to the YAST-25 measure of debt. In addition, given the discrepancy in the estimates of boomeranging when using household rosters versus self-reports, we also test whether our results are robust to the measure of boomeranging used. Our results are substantively equivalent across these measures. Thus, while relying on household roster data appears to underestimate the prevalence of boomeranging, it does capture many important correlates. Finally, to further examine heterogeneity in the association between debt and boomeranging, we test whether the association differs by completion status or for-profit attendance, as recent research suggests that college noncompleters and for-profit attendees may struggle with debt (Looney and Yannelis 2015). We also test whether the association varies by gender, socioeconomic background, or other college characteristics. Further analyses reveal no support for the hypothesis that the link between debt and boomeranging varies across these groups, suggesting that student loan debt is racialized and has greater negative consequences for black youth than for other social groups.

Discussion

Life course scholars have argued that residence with parents in young adulthood is a sign of stunted development and a problematic reversal of one of the core aspects of the transition to adulthood (Sandberg-Thoma et al. 2015; Sassler et al. 2008; South and Lei 2015; Stone et al. 2014). A growing population of young people who attend postsecondary institutions, coupled with rising costs and debt, has raised popular and scholarly concerns about the impact of student debt and college experiences on boomeranging. In this study, we contribute to this small but burgeoning area of research and test three claims regarding the link between student debt and boomeranging: first, that student debt increases the risk of boomeranging because it creates economic strain, increases the risk of college noncompletion, delays adult transitions, and undermines mental health; second, that the association between debt and boomeranging is stronger for blacks than for whites because for blacks, debt is more burdensome due in part to discrimination and hardship in credit, college, and labor markets; third, that college completion, rather than debt, is most consequential for boomeranging. We find support for the second and third arguments and find little evidence that student debt is linked to boomeranging in the total population.

Though our main findings do not align with popular claims about student debt, they are in line with recent literature that has found null or mixed findings regarding the effect of debt on the transition to adulthood (Addo 2014; Houle and Berger 2015). These mixed findings likely reflect that student debt is, as Dwyer and colleagues (2012:1136) note, a “double-edged sword”—on the one hand, a valuable resource to help bridge the gap between their resources and rising costs but, on the other hand, a burden that must be repaid, which may be more challenging for some groups than for others. In other words, rising college costs and debt have made college a riskier proposition for some groups than for others.

To this end, our findings, coupled with recent research on racial disparities in debt, suggest that taking on debt is more consequential for black young adults than for white young adults. Black students are more likely to have trouble paying down debt and may be more likely to drop out of college in response to high debt burdens than are whites (Jackson and Reynolds 2013). Given that blacks experience lower labor market returns to college than whites (Gaddis 2015), while also facing higher debt burdens and dropout risk, black young adults take a great deal more risk in enrolling in college and reap fewer rewards to that risk. This growing body of evidence suggests that rising debt may contribute to growing racial differences in the transition to adulthood (Furstenberg et al. 2004) and may contribute to the fragility of the next generation of the black middle class (Addo et al. 2016). To the extent that student debt may reinforce and reproduce racial inequalities within and across generations, future research should continue to interrogate the causes and consequences of racial disparities in debt and heterogeneity in the consequences of debt by race.

Finally, our findings also demonstrate that college completion—much more so than student debt, in terms of effect size—is a key correlate of returning to the parental home. Young adults who attend either two- or four-year institutions and fail to achieve their degree have a significantly higher risk of returning home than their counterparts, and the coefficient size is among the largest of all model covariates. These findings are consistent with recent scholarly assertions that higher education does not have a debt crisis per se but a completion crisis (Akers and Chingos 2016). In an era of rising college costs, and amid a deteriorating labor market, the economic stakes of college completion are high. In this environment, those who start but do not finish college are in a vulnerable position and, as we show, at an elevated risk of ending up on their parents’ doorstep. Although we do not find an association between for-profit attendance and debt, the coefficient is in the expected direction and may fail to achieve statistical significance because only a very small proportion of respondents attend for-profit institutions. Small sample size may also explain why we do not find evidence for an interaction effect of for-profit attendance by student debt. Moreover, consistent with prior research, we find that young adults’ transition into adult social roles, including marriage, homeownership, and successful employment, are negatively associated with boomerang risk. As such, this suggests that broader demographic changes in the transition to adulthood play a large role in shaping whether college-going youth return home (Fry 2016; Houle and Berger 2015).

While this is the first study to our knowledge to examine the link between student debt, college completion, and boomeranging using longitudinal survey data from a contemporary cohort of young adults that has record levels of student debt, it is not without limitations. First, our student debt measure is limited to three time points, and thus we may miss annual variation in student debt, which could bias our results downward. However, given that our results are robust when using the annual measure of student debt when respondents are in college, and we do not expect student debt to fluctuate dramatically between observations, this is unlikely to severely bias our results. Second, measurement bias in our boomeranging measure (recall and social desirability), is a concern, though our results are consistent with the household roster measure. Third, it is possible that young adults in our sample may not have been residentially independent long enough to observe an association between debt and boomeranging. However, we find this to be unlikely, because most young adults who return home do so very quickly after attaining residential independence, and we find no evidence for an interaction between student debt and time since residential independence. However, future research should continue to follow this cohort as it ages and examine potential long-term effects of student debt on adult outcomes. Finally, we advise caution in causal interpretation of our findings, as student debt is not randomly assigned, and there are likely unobserved differences between students with varying debt loads that may be associated with risk of boomeranging.

Taken together, the findings suggest that college completion, transitioning into adult social roles, and labor market success may better explain rising rates of boomeranging among college-going youth than student debt, but student debt may be exacerbating racial inequalities in transition to adulthood outcomes. Thus, our findings suggest that downstream policies intended to alleviate debt hardship should be targeted toward particular vulnerable groups rather than universally. For example, private lending markets should be better regulated to protect minority students from undue burden. Upstream policies would benefit from greater focus on reducing debt burden through decreasing costs (Goldrick-Rab 2016) as well as policies and programs that promote college completion and labor market success. In sum, the rise of student debt in the United States has created a new form of risk for college-going young adults. For many young adults, that risk may pay off. But for others, taking this risk will create hardship that complicates the transition to adulthood and perhaps will follow young people across the life course, perpetuating social inequalities that have persisted for generations.

Footnotes

Appendix

Discrete Time Event History Models of First Residential Independence.

| Variable | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| Self-report residential independence | |||

| Student loan debt (logged) | 0.016** | −0.004 | 0.003 |

| (0.005) | (0.005) | (0.006) | |

| Constant | −7.397*** | −7.066*** | −5.779*** |

| (0.559) | (0.621) | (0.660) | |

| Model covariates | |||

| Social background characteristics | Yes | Yes | Yes |

| Postsecondary educational characteristics | No | Yes | Yes |

| Young adult characteristics | No | No | Yes |

Source: National Longitudinal Study of Youth 1997 Cohort.

Note: N = 32,886 person-years, 5,266 persons. Models also include dummy variables for time since independence and controls for urban residence and region. Standard errors in parentheses and corrected for nonindependence. Multivariate results are unweighted.

p < .05. **p < .01. ***p < .001.

Acknowledgements

We thank Emily Walton, Janice McCabe, and Joe Digrazia for helpful comments in preparation of this manuscript. We also thank Rob Warren, Linda Renzulli, and the anonymous reviewers whose feedback greatly improved the paper during the revision process.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was generously funded by a grant from the Rockefeller Center at Dartmouth College. This research was also supported by National Institute of General Medical Sciences of the National Institutes of Health (5P20GM104417). The content does not necessarily represent the official views of the National Institutes of Health.