Abstract

Direct tests between corporate social responsibility (CSR) and firm performance (FP) have been argued to be spurious. Following this line of argument, the present study tests a mediated model in understanding the CSR–FP relationship. Specifically, we posit that reputation and customer satisfaction mediate fully the CSR–FP relationship. Based on the results from a sample of 280 Australian firms, the findings suggest that CSR is linked with FP. However, the effect is indirect: while CSR is linked to both reputation and customer satisfaction, reputation alone mediates the CSR–FP relationship. The results are interesting, suggesting that to reduce ambiguity surrounding the CSR–FP relationship scholars need to significantly expand studies that address moderating and mediating variables. Discussion is given to these findings along with paths for future research.

Keywords

1. Introduction

Is the relationship between corporate social responsibility (CSR) and firm performance (FP) straightforward? The supporting evidence may potentially be misleading. First, although negative and neutral results have been found, overall, research demonstrates a modest positive relationship (Margolis et al., 2008; Margolis and Walsh, 2003; Orlitzky et al., 2003; van Beurden and Gössling, 2008). However, second, many scholars question the results of much CSR–FP research because most studies omit important intervening variables (Griffin and Mahon, 1997; Margolis et al., 2008; Margolis and Walsh, 2003; Rowley and Berman, 2000; Wood and Jones, 1995). In a test of one such intervening variable, Luo and Bhattacharya (2006) find that customer satisfaction mediates fully the effect of CSR on market value (a measure of FP). This lends some support that the relationship between CSR and FP is likely more complex than most studies reveal, and that tests of moderation and mediation are required (Margolis et al., 2008; Margolis and Walsh, 2003; Rowley and Berman, 2000; Ullmann, 1985).

In an effort to advance research on the CSR–FP relationship, we expand the work of Luo and Bhattacharya (2006) by asking the question, ‘Do customer satisfaction and reputation fully mediate the CSR–FP relationship?’. This is important for two key reasons. First, CSR has a multiplicative effect on business benefits. That is, CSR is argued to offer a number of business benefits, including maintaining the license to operate, risk reduction, efficiency gains, and tax advantages (Weber, 2008). However, with few exceptions (e.g. Greening and Turban, 2000; Turban and Greening, 1997) direct financial benefits remain the interest of CSR research (Lee et al., 2009; Margolis et al., 2008). By exploring additional benefits empirically, we not only offer some verification of the many predicted outcomes of engaging in CSR, but also test a CSR–FP relationship that is argued to be more complex than most studies reveal (Margolis et al., 2008; Margolis and Walsh, 2003; Rowley and Berman, 2000). That is, we offer a test of mediation.

Second, while the evidence suggests that customer satisfaction is linked with FP (Anderson et al., 1994, 1997), other studies find that higher levels of customer satisfaction also increase firm reputation (Walsh et al., 2006, 2009; Wang et al., 2003). At the same time, studies demonstrate that a good reputation positively impacts on FP (e.g. Fombrun and Shanley, 1990; Kotha et al., 2001; Roberts and Dowling, 2002; Shamsie, 2003). Based on the evidence, we argue that in studies of the CSR–FP link, both customer satisfaction and reputation should be included, given both are predicted benefits of CSR (Brammer and Pavelin, 2004; Gassenheimer et al., 1998; Weber, 2008; Wood, 2010) and both have been found to have a positive relationship with FP. While building on the foundation of Luo and Bhattacharya (2006), we argue that the relationship between CSR and FP is more complex than their study reveals, particularly when customer satisfaction and reputation are built into the model. CSR is indirectly linked to FP both through customer satisfaction and reputation, and taking into account these relationships, we posit that reputation is the sole mediating factor.

Our research advances the understanding of the CSR–FP link in three ways. First, we respond to calls from several scholars to study mediating mechanisms between CSR and FP given the relative paucity of currently available research; our study therefore explores those factors that might explain whether and when particular firms may earn positive financial returns from CSR. Second, we include two of the most important predicted benefits of CSR, namely, customer satisfaction and reputation. We do this through expanding previous research by developing and testing a more complex relationship. This is important because researchers are able to ‘draw measureable, testable links from [CSR] to outcomes such as [customer satisfaction and reputation], and from there to FP’ (Wood, 2010: 60). According to Wood (2010), studies of mediation are necessary because they drive research away from a theoretically untenable relationship (i.e. direct links between CSR and FP). Lastly, to test our premise, a sample from Australia is used because such samples are underutilized. For example, a recent study on CSR and FP by Australian researchers omitted the use of a sample of local firms (Lee et al., 2009). Using a context-specific sample is important because evidence suggests that engaging in CSR in Australia appears to receive mixed reviews amongst the business community, and committing resources to socially responsible activities might be seen as a cost rather than an investment. Therefore, an Australian sample is helpful given most studies on the CSR–FP link use European or US data. Addressing posited questions will therefore allow scholars to offer relevant advice on the likely outcomes of demonstrating CSR across international contexts, and helps to more fully explore Matten and Moon’s (2008) proposition that CSR is spreading globally from its US-based roots.

2. Theory and hypotheses

2.1 Conceptualization of CSR

Despite a large and growing body of literature on CSR, the construct remains ‘ambiguous’ (Wood, 2010: 50) and has no precise definition (Scherer and Palazzo, 2007), which has led to considerable difficulty in conducting and comparing empirical research results (Lozano, 2008; Margolis et al., 2008; Orlitzky et al., 2011; van Beurden and Gössling, 2008). Multiple viewpoints and definitions likely exist because CSR is internally complex, having relatively open rules of application (Wood, 2010). Similarly, Van Marrewijk (2003) suggests that CSR means something, but that its meaning is not always the same thing to everybody. Lastly, Carroll (1999) demonstrates that CSR has been a dynamic phenomenon, changing through time. However, a core, common theme does appear to exist.

The core theme with respect to CSR is that firms have responsibilities to society including, but extending beyond, profit maximization (Brown and Dacin, 1997; Davis, 1973; Matten and Moon, 2008; Wood, 1991). Unfortunately, definitions of firms’ obligations to society beyond that of profit maximization generally do little to describe what those specific responsibilities are, other than ‘practices’ of some kind reflecting responsibility for a broader ‘societal good’. On the other hand, Carroll (1979, 1999, 2004) overcomes vague or general descriptions of firms’ societal responsibilities by specifying that four such dimensions of CSR exist: (1) economic; (2) legal; (3) ethical; and (4) discretionary.

First, firms have an institutional role of meeting consumptive needs via resource conversion and to do so efficiently and effectively, which is part of the economic dimension of CSR. Second, firms have a legal role to fulfill their economic mission within a legal framework, while complying with all in-effect laws. Third, with respect to ethics, firms have an obligation to abide by moral rules defining appropriate behaviors in society. Lastly, the discretionary dimension of CSR refers to business activities that are not required by law or are not mandated, but are expected by stakeholders as a demonstration of good citizenship. Examples include investing in local social enterprises or providing training to employees.

According to Lozano (2008), Carroll’s work is the clearest conceptualization of CSR because it identifies, or defines, all obligations of a firm towards society. There is some support for such an argument: Carroll’s (1979, 2004) work continues to be popular and is a widely adopted conceptualization of CSR amongst researchers because it systematically differentiates firms’ responsibilities from merely profit making and from the social responsibilities of governments (Wood, 2010). Further, Carroll’s (1979, 2004) conceptualization is particularly important to researchers, as it has been used as the basis for a variety of empirical studies, many which have been published recently (e.g. Galbreath, 2008; Sheth and Babiak, 2010; Shum and Yam, 2011). Lastly, CSR has been argued to be a multidimensional construct (Jamali, 2008), and Carroll’s (1979, 2004) conceptualization addresses four such dimensions.

In sum, this study adopts interpretations of CSR which consist of demonstrable actions and outcomes reflecting business responsibility for societal good. Actions and outcomes include those that respond to economic, legal, ethical, and discretionary dimensions of CSR. An assumption is made that all firms have roles in meeting the dimensions of CSR as defined by Carroll (1979, 2004), and that they can address these dimensions by doing very little to doing much. Thus, in the operationalization of CSR used in this study, we measure the degree to which a firm is demonstrating actions/outcomes that are directly related to its social responsibilities as defined by Carroll (1979, 2004).

2.2 Hypotheses

Although evidence is mixed, studies do find a link between CSR and FP (Margolis et al., 2008; Orlitzky et al., 2003; van Beurden and Gössling, 2008). For example, in recent meta-analysis research of 167 CSR–FP studies, Margolis et al. (2008) find the effect, while modest, is positive. Orlitzky et al. (2003) find similar results. They conduct a meta-analysis of 52 studies, finding an overall positive relationship between CSR and FP. Lastly, van Beurden and Gössling (2008) examine 34 CSR–FP studies and find that 68 percent demonstrate a positive association. The majority of cited studies use European or US samples. However, in Australia, the setting of this study, we believe there is no reason that similar results will not be found. For example, recent evidence suggests that Australian firms recognize the strategic benefits of, and are embracing the business case for, CSR (Black et al., 2011). Australian firms are also demonstrating strong links between CSR activity and positive organizational benefits (Galbreath, 2008). Hence, we expect that demonstration of CSR will offer financial rewards in the Australian context. However, our argument is based on a theory that CSR’s impact on firm performance is one that is not direct, but rather is indirect.

2.3 The mediating effects of customer satisfaction and reputation

Major reviews of the CSR–FP relationship agree that despite the apparent favorable findings, research has not produced a solution, but rather isolated islands of partial insight about an unseen larger picture. As Rowley and Berman (2000: 405) remark on the state of CSR–FP studies, ‘Researchers have combined various mishmashes of uncorrelated variables, which render correlation and ordinary least squares regression results indiscernible.’ Margolis and Walsh (2003) agree, suggesting that scholars developing ever sophisticated empirics to test a direct CSR–FP relationship have only led to obscuring the big picture. The big picture is that returns to CSR are contingent, not universal (Ullmann, 1985; Wood, 2010), and that to more carefully assess conditions under which CSR influences FP, omitted variables must be empirically examined. We argue that customer satisfaction and reputation are two such variables.

Evidence exists in the literature demonstrating that reputation and customer satisfaction relate positively to FP. In their study, Kotha et al. (2001) find that Internet firms with positive reputations enjoy higher market value and sales growth. Roberts and Dowling (2002) find that firms with higher reputations enjoy higher return on assets (ROA), and that these results are persistent over time. Fombrun and Shanley’s (1990) and Shamsie’s (2003) results also support a positive relationship between reputation and FP. Similarly, customer satisfaction has also been found to positively influence FP. For example, studies find that higher customer satisfaction levels lead to higher cash-flow levels (Gruca and Rego, 2005). In other research, scholars find a positive link between customer satisfaction and market value (Fornell et al., 2006). Factoring in this evidence, results suggest that CSR, reputation, and customer satisfaction all have positive effects on FP. However, in the context of this study, we argue that an underlying reason for the positive association of CSR with FP is due to the effects of reputation and customer satisfaction. There are a few key points to our argument.

First, definitions of CSR show that firms need to demonstrate societal benefits that include, but go beyond, economic outcomes. However, society needs to perceive that these benefits are of value for a firm to be considered socially responsible. One way in which the benefits of socially responsible actions are perceived by society as valuable is through a positive reputation (Brammer and Pavelin, 2004). Signaling theory (Spence, 2002) argues that CSR has a positive impact on reputation. This stems from the fact that as a firm demonstrates socially responsible behavior, stakeholders’ judgments of that firm are positively influenced, which is the foundation of reputation (Fombrun and Shanley, 1990). Given that a firm’s reputation is a representation of public opinion, and such opinions are dependent upon meeting stakeholder expectations, the ability to demonstrate a high level of CSR signals that the firm will behave in accordance with stakeholders’ expectations (Brammer and Pavelin, 2006). When stakeholder expectations are met through demonstration of CSR, a firm’s overall reputation is augmented.

The ability to build a positive reputation ensures the continued participation of stakeholders (Brammer and Pavelin, 2006), which is critical to firm survival and performance (Clarkson, 1995). CSR therefore improves FP by positively influencing stakeholder perceptions. In turn, positive stakeholder perceptions gained through demonstration of CSR lead to a better reputation. Development of a strong reputation creates a socially complex, time-dependent, and inimitable resource. Such a resource leads to superior performance (Barney, 1991). Similarly, Jones (1995) argues that firms who develop strong reputations create a high level of trust with their stakeholders. Trust substitutes for expensive governance mechanisms because fewer protective devices are needed if the firm has trustworthy agents and less time is spent in negotiation if initial claims are truthful (Hosmer, 1995; Williamson, 1985). Thus, the development of a better reputation through demonstration of CSR lowers transaction costs, which offers performance-related advantages (Jones, 1995; Prahalad, 1997).

Second, engagement in CSR is a demonstration of equity or fairness (Aguilera et al., 2007). Stemming from social exchange theory (Adams, 1965), equity theory focuses on fairness, rightness, or deservedness judgments individuals make in reference to what one party or another receives (Oliver, 1997). The theory posits that in exchanges, if a party feels equitably treated, satisfaction is the result (Oliver, 1997). Equity is best demonstrated with customers, as they are one of the most important stakeholders and have significant interactions with firms on a regular basis. Demonstration of equity to customers through CSR increases their satisfaction levels. To increase satisfaction levels through CSR, firms can engage in socially responsible practices such as ethical treatment of customers (Carroll, 2004; Taylor, 2003), employee training (which has downstream implications for equitable treatment of customers) (Maignan et al., 1999), or through improvements in product quality (Carroll, 1979, 2004). CSR therefore positively impacts on customer satisfaction. When customer satisfaction is improved, firms benefit through more repeat business and lower customer defection (Bhote, 1996; Galbreath, 2002). Repeat business and lower customer defection increases FP by reducing costs, increasing returns, and generating more sales (Bhote, 1996; Galbreath, 2002).

Lastly, we cannot ignore the fact that a positive relationship has been found between customer satisfaction and reputation (Walsh et al., 2006, 2009; Wang et al., 2003). There is a key reason for this relationship. Reputation, at its core, is a result of past actions that demonstrate to stakeholders information about how well a company meets its commitments and conforms to their expectations (Brown and Logsdon, 1999). As such, when developed well, reputation becomes one of a firm’s most strategic resources (Flanagan and O’Shaughnessy, 2005). However, a major determinant of a positive reputation comes through customer positive word-of-mouth (Hennig-Thurau et al., 2002). Positive word-of-mouth is a result of customers who are satisfied with their interactions with a firm. Further, Nguyen and Leblanc (2001) argue that a positive reputation is one of the most reliable indicators of whether or not a firm’s customers are satisfied. Therefore, we posit that reputation is impacted by customer satisfaction, and that customer satisfaction’s impact on FP is mediated by reputation. Hence, given the previous discussions:

H1: The CSR–FP relationship is one that is mediated rather than direct.

H2: In this mediated relationship, reputation acts as the sole mediating factor between CSR and customer satisfaction and each of these construct’s relationship with FP.

3. Methods

3.1 Sample and data collection

Kinder, Lyndenberg and Domini (KLD) ratings, Fortune’s Most Admired Companies, and even annual reports have become widely used for both sample selection and measurement of CSR and other constructs such as reputation (Waddock, 2003). However, studies using such datasets – especially KLD and Fortune’s Most Admired Companies – are dominated by US samples. Further, secondary datasets such as KLD or annual reports have their own critics, and are vulnerable to various types of biases (Brown and Perry, 1994; Entine, 2003; Fryxell and Wang, 1994; Huse et al., 2011, Jarvis et al., 2003). In our case, we were interested in an Australian sample. Further, we wanted as large a sample as possible to maximize generalizeability. Unfortunately, readily and publicly available equivalents on large sample sizes such as the KLD database or Fortune’s Most Admired Companies in the US do not exist in Australia, nor are reliable and extensive firm-level data available from the government on the constructs under study.

In the absence of available data on our constructs across a large sample, following accepted practice, tested survey measurement items were used wherever possible and new items were developed from theoretical insights in the literature when necessary. The survey approach was considered appropriate for collecting data, particularly to tap into latent constructs where secondary sources were unavailable. We developed a survey in three stages. First, after an extensive literature review across a number of studies, an initial, theory-based instrument was developed. Second, a pilot study was conducted with 20 executives not included in the final sample to assess content validity. Third, based on feedback, minor changes were made and a final version of the survey was constructed.

As for sample selection, Dunn and Bradstreet, a company database service provider, was contacted to draw a sample of firms operating in Australia. To obtain a heterogeneous mix, 3000 firms falling into manufacturing and services classifications were randomly selected. Other organizations, such as public administration and community service entities, were excluded due to their lack of relevance to this study. Companies were a wide range of sizes, although those with less than 50 employees were not included because we wanted to ensure that adequate resources were available to address social responsibilities.

Managing directors were the targeted respondents for this study as they have breadth of knowledge of firm operations and performance, and probably the best insight about the issues in this study. However, as noted, like secondary data sources, survey studies have the potential to introduce various biases (Huse et al., 2011); namely, common method, social desirability, and order bias. To reduce such biases, some procedural techniques were used. In order to reduce the extent of common method variance, we undertook the following. First, we sought to minimize the effect of such variance in our data by building the following suggestions from Spector and Brannick (1995) into our survey instrument. To do this, we: random-ordered the sequence of scale items; reverse-coded certain items; did not imply any preferred response in our statements; paid close attention to time wording; kept the research instrument as short as possible; and provided succinct instructions for survey completion. Second, a cover letter guaranteed anonymity to moderate respondents’ tendency to make socially desirable responses. Lastly, to reduce order bias, dependent and independent variables were placed far apart from each other in the survey.

After an initial mailing and two follow-up letters, the overall response rate was 10 percent. Although the response rate yielded may prima facie appear low, the rate is similar to other studies on CSR and various studies surveying top managers, which demonstrate response rates as low as six percent (e.g. Maignan and Ferrell, 2001; Simons et al., 1999). Further, direct mail surveys have a typical response rate of 5–10 percent, suggesting our response rate was adequate in a country suffering from severe survey fatigue (Galbreath and Galvin, 2008). After eliminating unusable surveys, 280 firms were included in the analysis.

P<0.001

To test for non-response bias, early versus late respondents were compared on all variables used in the study. The rationale behind such an analysis is that late respondents (i.e. sample firms who respond late) are more similar to the general population than the early respondents (we also note that while non-response may lead to a finding of higher levels of the constructs in Figure 1, there is no prima facie reason why it should lead to a bias in the relationship between them). Independent samples t-tests revealed no significant differences between any of the variables. Thus, non-response bias does not appear to be a problem.

Main effects test

Of the 280 valid responses, the most prominent industries include industrial manufacturing (28.9 percent), business services (17 percent), consumer products manufacturing (10.5 percent), financial services (6.5 percent), and other services (22.7 percent). The majority of firms were clustered into two sales revenue categories, with 41.9 percent of firms generating between AUD$10,000,001 and AUD$50,000,000, and 21.7 percent over AUD$200,000,000. Respondents’ average age was 50 years old, while the majority had an undergraduate degree or higher (72.9 percent). Lastly, the mean number of employees was 630.

3.2 Independent variables

A universally accepted conceptualization or measurement of CSR is neither available nor possible (Montiel, 2008; O’Shaughnessy et al., 2007). However, in the absence of readily available secondary data, a forced-choice instrument, based on Carroll’s (1979) conceptualization, has been frequently used to measure CSR for empirical study (e.g. Aupperle et al., 1985; Pinkston and Carroll, 1994, 1996). The main drawback is that the instrument is largely used to determine firms’ CSR orientation. That is, the instrument assesses the degree to which firms give importance, or rank order, economic, legal, ethical, and discretionary dimensions of CSR; the instrument does not adequately assess CSR activities/outcomes for each of the dimensions. Because this study was interested in assessing CSR activities and outcomes, the use of the forced-choice instrument was considered inappropriate.

After reviewing several studies for an appropriate scale, the measurement of CSR used in the research of Maignan and colleagues was chosen for our study. Maignan and colleagues (Maignan et al., 1999; Maignan and Ferrell, 2000, 2001) identified and developed various socially responsible activities that aligned with Carroll’s (1979) conceptualization of CSR, the conceptualization we use in this study. Thus, the scale does not assess the degree to which a firm believes it has social responsibilities or how they rank order those responsibilities; rather, the scales assesses CSR activity, making it ideal for this study. For measurement, a 29-item CSR scale was used (Appendix). The scale has undergone rigorous development in previous studies and has been tested using multiple industries and countries. Further, in a test of six competing measurement models, Maignan and Ferrell (2000) found that the model that incorporated four correlated factors (economic, legal, ethical, discretionary dimensions of CSR) provided the best overall fit. Hence, following Maignan and colleagues (1999; Maignan and Ferrell, 2001), equal weights were applied to each dimension and a firm’s CSR level was computed as the simple averages of the sums of the scores of the responses across the four dimensions. Respondents were asked to provide their perceptions of each dimension of CSR for their firm, where each scale was measured with a 5-point Likert scale, where ‘1 = strongly disagree’ and ‘5 = strongly agree’.

This study relied on the reputation scale developed by Weiss et al. (1999). Weiss and colleagues developed a scale that assesses a firm’s general perception of their reputation. The scale does not assess reputation for anything specific (e.g. product innovation); rather, the scale asks respondents to measure how customers perceive their company’s overall reputation. This is consistent with theoretical treatments of reputation. The scale contained five items rated on a Likert scale, where ‘1 = strongly disagree’ and ‘5 = strongly agree’. Following Weiss et al. (1999), the scale items include: ‘Our firm is viewed by customers as one that is successful’, ‘We are seen by customers as being a very professional organization’, ‘Customers view our firm as one that is stable’, ‘Our firm’s reputation is highly regarded’, and ‘Our firm is viewed as well-established by customers’.

Customer satisfaction indicators should address an overall evaluation of interactions with a firm; therefore, aligned with Ping’s (1993) proposal that the relationship between customer and firm reflects overall satisfaction, four items were developed relating to customers’ expectations and the relationship between customers and the firm. In addition, three items were adopted that are commonly used in customer satisfaction research as indicators of the construct (e.g. Oliver and Swan, 1989). To gauge customer satisfaction then, the scale contained seven items designed to measure perceptions of satisfaction levels of customers. Scale items include: ‘Compared to competitors, our customers find that our products/services are much better’, ‘Our customers are very satisfied with the products/services we offer’, ‘Our customers are very satisfied with the value for price of our products/services’, ‘Our customers find that the products/services we offer exceed their expectations’, ‘The likelihood that our customers will recommend our products/services to others is high’, ‘Our customers are very satisfied with the quality of our products/services’, and ‘The ability to achieve high levels of customer satisfaction is a major strength of our firm’. Each item was rated on a Likert scale, where ‘1 = strongly disagree’ and ‘5 = strongly agree’.

3.3 Dependent variable

FP was gauged with four items, including return on investment (ROI), ROA, sales growth, and profit growth. Items were drawn from Spanos and Lioukas (2001). For each performance indicator, respondents were asked to rate their performance, relative to competitors in their industry, on a 5-point Likert scale where ‘1 = much worse’ and ‘5 = much better’ (Vorhies and Harker, 2000). Although objective performance data would have been helpful, prior research has shown that survey respondents prefer perceptual performance measures because objective measures are seen as confidential, especially among private companies (Spanos and Lioukas, 2001). Use of perceptual performance items also facilitates comparisons across firms and contexts, such as across industries, time horizons, and economic conditions. Prior research of subjective performance measures has also shown them to be a reasonable substitute for objective measures of performance and to have a significant correlation with objective measures of performance (Dawes, 1999; Spanos and Lioukas, 2001). Thus, following the accepted design of previous research (e.g. Dawes, 2002; Spanos and Lioukas, 2001; Vorhies and Harker, 2000), subjective measures of performance were considered appropriate for this study.

3.4 Control variables

Several variables were accounted for to control for confounding effects. These include firm size, firm age, industry type, and sales revenue. Firm size was measured with a single item, number of full-time employees. Firm age was measured with a single item, number of years in business. Because industry type impacts a firm’s competitiveness, categorical variables measuring eight different industries was used. Lastly, for sales revenue, categorical variables measuring six categories, from less than AU$1,000,000 per year to a category of AU$200,000,000 per year or over, were used.

4. Analysis and results

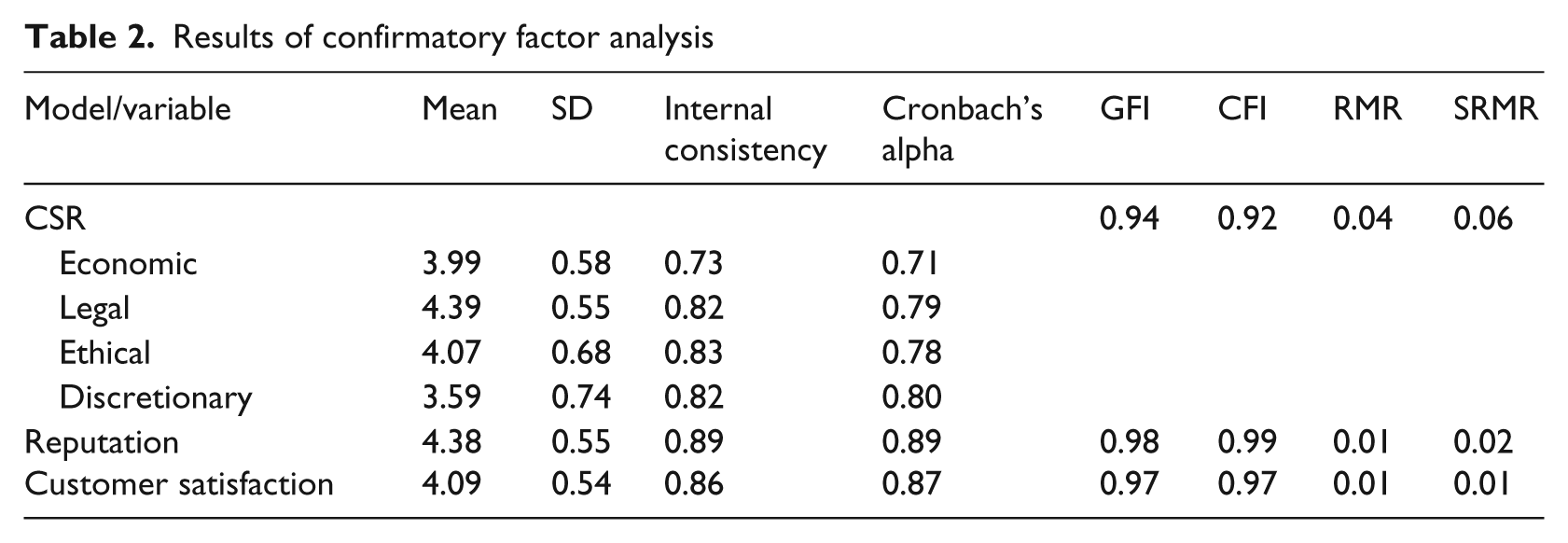

Means, standard deviations, and correlations are presented in Table 1. To assess the psychometric properties of the constructs, this study conducts confirmatory factor analysis (CFA). After scale purification, CSR, reputation, and customer satisfaction met acceptable levels of the major fit indices (Bentler, 1990), exceeding the 0.9 critical level of the comparative fit index (CFI), goodness-of-fit index (GFI), and less than 0.05 value of the root mean square error (RMR) (Table 2). The standardized factor loadings of all the measurement items on their respective constructs were significant (p < 0.05), indicating support for convergent validity. Furthermore, discriminant validity is also supported for CSR, reputation, and customer satisfaction. The square root of the average variance extracted (AVE) exceeds the correlation between factors and the AVE exceeds the 0.5 benchmark (Fornell and Larcker, 1981). Finally, all constructs demonstrated sufficient reliability, exceeding the common benchmark of 0.70.

Descriptive statistics and correlations for continuous variables Correlationsa

Correlation coefficients .12 or greater are significant at p < .05.

Results of confirmatory factor analysis

Regarding FP, CFA suggests the construct is not a first-order model. To explore the psychometric properties further, Principal Components Analysis using SPSS was conducted. A factor analysis test demonstrated that ROA explained nearly 70 percent of the variation. A decision was therefore made to include ROA as the single indicator of FP in the study. We believe this is justified, as ROA is one of the most widely used performance variables in strategy research.

Prior to hypotheses testing, the control variables were assessed to determine their impact on the models. A multi-group method of analysis was used and the results suggest that adding the control variables does little to improve the overall fit of the models, which confirms at least some previous findings on lack of influence of variables such as firm size in studies of CSR (Lee et al., 2009; Orlitzky, 2001; Webb, 2004). Thus, to test the hypotheses and to assess the presence of mediating variables, we followed the procedure outlined by Baron and Kenny (1986). Structural equation modeling (SEM) using AMOS is employed, with the maximum likelihood estimation method as the analysis technique. According to Rowley and Berman (2000), SEM is more appropriate than regression analysis in CSR research as SEM not only simultaneously examines the measurement model – the relationship between each (latent) CSR dimension and each item used to capture it – but the relationships among each latent variable, including dependent variables such as FP.

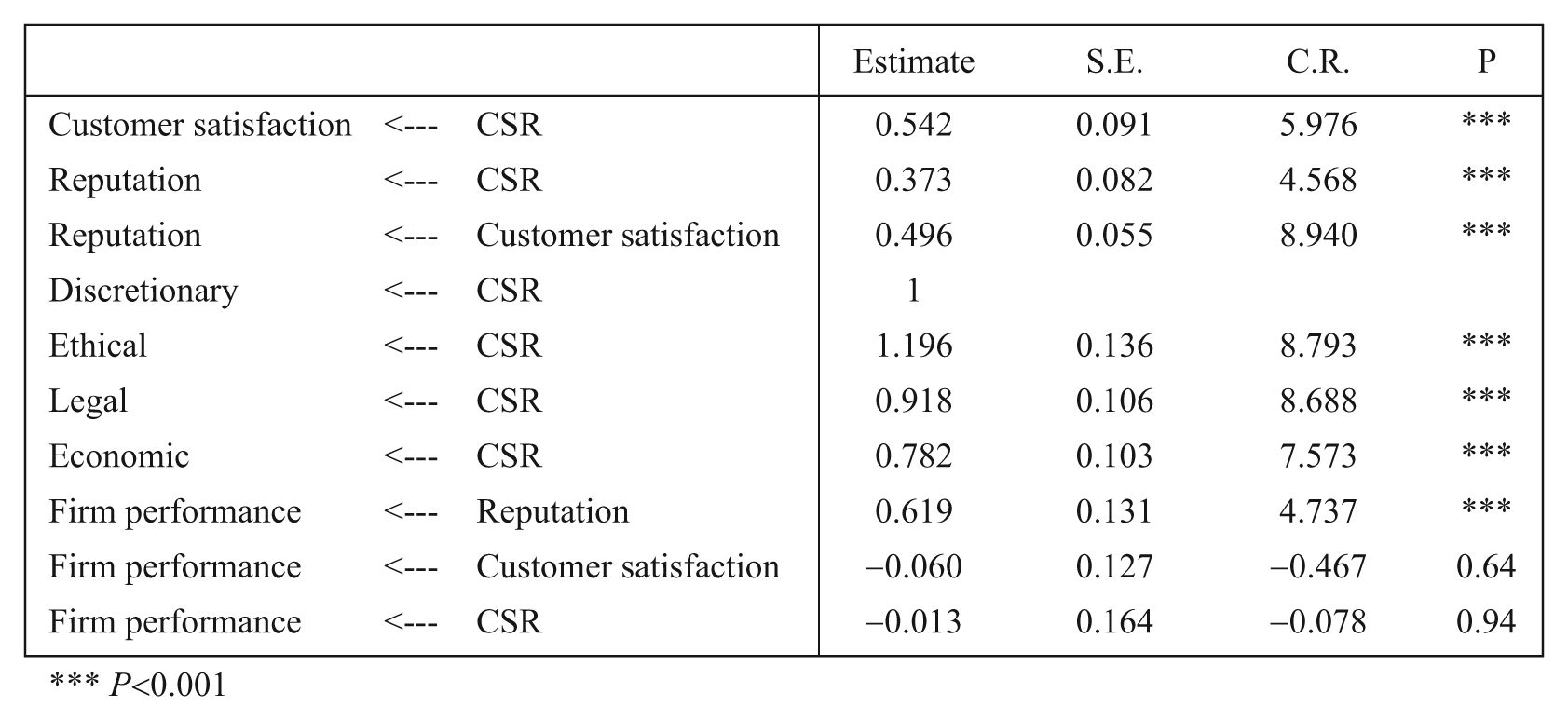

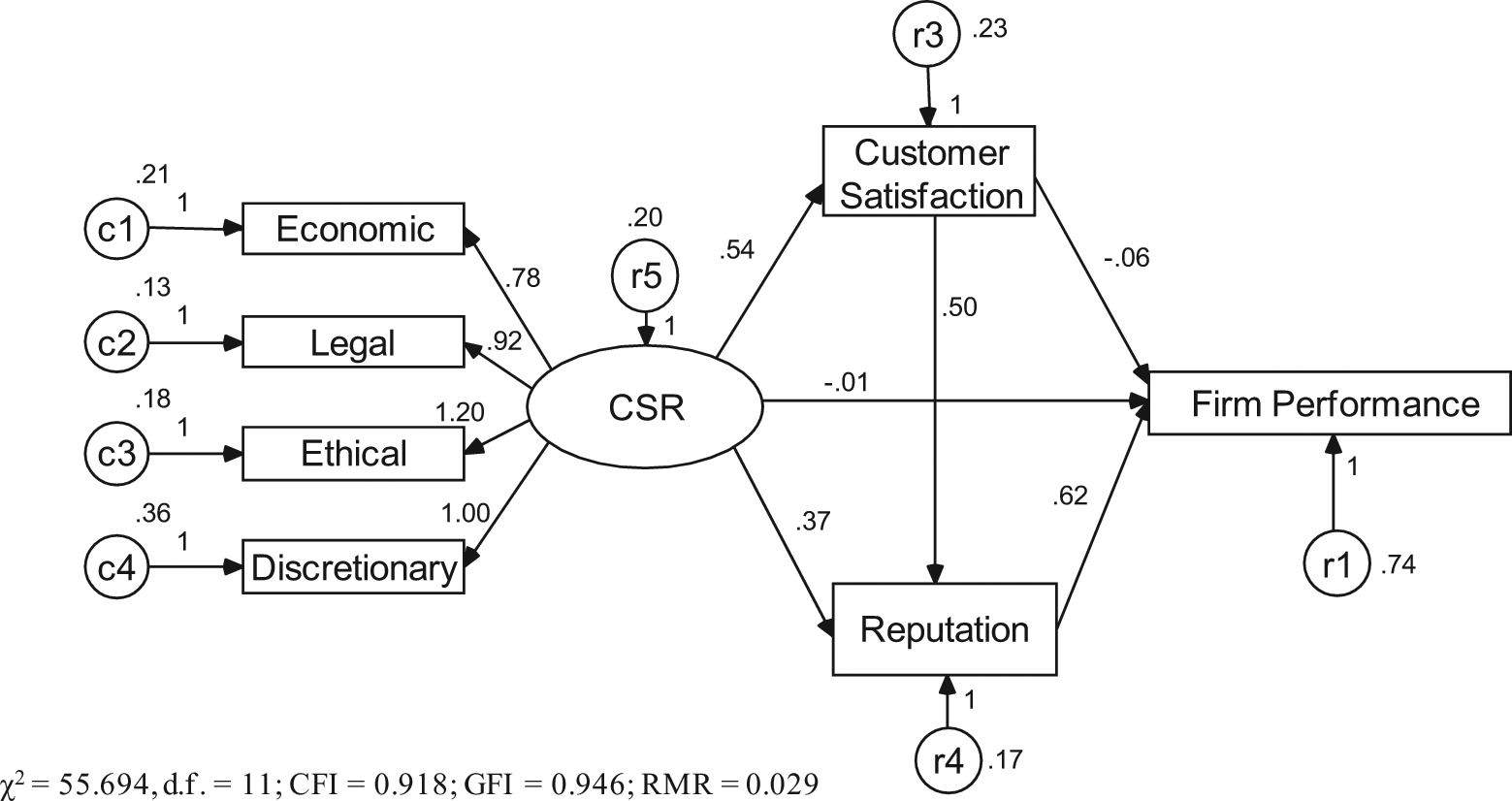

Following Baron and Kenny (1986), initially, only the relationship between CSR and FP is tested. The results of this first model indicate a good fit to the data (χ2 = 27.024, d.f. = 5; CFI = 0.928; GFI = 0.962; RMR = 0.034), demonstrating a significantly positive relationship between CSR and FP. In the second model, we sought to test mediation effects. The model was run with all paths estimated as specified in our hypotheses and for mediation tests. The data demonstrates a good fit to the model (χ2 = 55.694, d.f. = 11; CFI = 0.918; GFI = 0.946; RMR = 0.029). The results of the second model (Figure 1) indicate that the previously significant relationship between CSR and FP becomes insignificant, demonstrating existence of full mediation (Baron and Kenny, 1986). The second model therefore suggests that CSR is associated with higher FP; however, the effect is indirect. This supports hypothesis one. CSR is positively associated with both customer satisfaction and reputation, which fully mediate the FP relationship. As predicted, the association of customer satisfaction with FP is through reputation, rather than through a direct link. This supports hypothesis two. Given the findings, CSR contributes to higher FP, via the resulting better reputation and higher customer satisfaction.

5. Discussion and implications

Both of the hypotheses were confirmed in this study. The findings are significant in that they help to clarify some of the ambiguity surrounding whether or not CSR can be associated with FP and when the association can be positive, rather than neutral or negative. More specially, despite the literature’s assertion for a business case, there is no reason to assume the existence of a direct relationship between CSR and financial performance per se. Hence, rather than look for a universal link between CSR and financial indicators, it is necessary to apply a contingency approach (Rowley and Berman, 2000). In this way, including mediators and/or moderators into analysis can help determine under which conditions CSR could come along with financial benefits, or, on the contrary, with financial losses (Branco and Rodriguez, 2006). In the case of our study, the results suggest that contingencies might determine how and why CSR can positively influence FP. Engagement in CSR appears to forge a better reputation and an increase in customer satisfaction. In turn, reputation and customer satisfaction reduce transaction costs, deliver more repeat business, and lower customer defection (Bhote, 1996; Galbreath, 2002; Jones, 1995; Prahalad, 1997), all of which offer performance-related advantages.

Our study also offers alternative explanations to the Luo and Bhattacharya (2006) study. While they find that the CSR–FP relationship is mediated by customer satisfaction, they omit reputation in the study. This could be problematic. Firms inevitably seek to build (if not maintain) positive reputations, while at the same time interact with and serve customers in such as way to ensure they are satisfied. According to Basdeo et al. (2006), attempts to build a good reputation (or enhance customer satisfaction for that matter) are ‘market actions’ that stakeholders can assess to make inferences about a given company. We argue that engagement in CSR shapes stakeholder inferences of a firm positively, and the subsequent benefit is both a better reputation and improved customer satisfaction. Thus, the benefits of CSR cannot be constrained to a single intangible benefit such as customer satisfaction, but rather can provide potentially many benefits (Weber, 2008, Wood, 2010). Not including reputation in mediation tests in the CSR–FP relationship is likely to skew or overinflate results, particularly where customer satisfaction is used as a variable.

Lastly, some evidence suggests that engagement in CSR in Australia is not universally accepted by the business community (Birch, 2002). Further, the ISO standard for CSR (ISO 26000) was recently ratified by 66 out of 71 countries involved in the voting. Significantly, Australia abstained from voting, casting further concerns as to the importance of CSR as a part of business practice in the country. However, the results of our study suggest that engaging in CSR is not necessarily detrimental to Australian businesses. This finding offers confirmation of the positive effects of CSR found in the bulk of research mainly conducted in Europe and the US. The findings also offer some level of support of Matten and Moon’s (2008) work which posits that CSR, as a practice, is diffusing from its US-based roots around the world.

In sum, this study points to a few key implications. First, recent analysis of the CSR–FP relationship has brought much criticism. Rowley and Berman (2000), for example, have criticized CSR–FP research because it appears to be more of an attempt to legitimate the business case for CSR rather than to engage in serious theoretical development. Similarly, Wood (2010: 59) argues that findings on the CSR–FP link ‘are wishy-washy at best – “doing good” does not seem to hurt companies most of the time, and “causing harm” sometimes does hurt – but these results do not point to a need for more research on the question, but for an abandonment of the…question in favor of more theoretically sound and powerful ones.’ CSR cannot universally produce a favorable impact on FP for all firms all the time, so favorable findings will never be replicable across all datasets. For researchers, an implication of our study therefore suggests far more attention and effort needs to be spent on determining the mechanisms by which CSR increases revenue or reduces costs. Hence, researchers need to carefully select contingent variables, theorize logical connections between CSR and these contingent variables, and then formulate testable links to firm performance. According to Wood (2010), this is the ‘missing link’ in most CSR–FP research to date.

Our results have practical implications as well. Firms throughout the world are challenged to demonstrate responsible corporate behavior. However, demonstrating responsible corporate behavior is not without opportunity costs, and executives remain skeptical of engaging in CSR (McKinsey & Company, 2006). The findings of this study suggest that CSR appears to be a good strategy. Executives should see CSR as a means to build intangible assets such as customer satisfaction and reputation, both of which are critical objectives of most companies. Thus, companies should consider that engaging in CSR activities might represent a robust strategy, particularly in an environment where stakeholders have increased social concerns. In fact, Porter and Kramer (2006) argue that CSR may well be the new battleground for competitive advantage.

6. Limitations, directions for future research, and conclusions

There are limitations to this research. First, secondary sources that adequately capture the key constructs in this study were not readily available for an adequate sample size in Australia. In this absence, following accepted practice, a survey was used for data collection, although this technique is not without limitations. Data that are collected from a single informant using survey techniques may be particularly susceptible to common method variance and social desirability biases.

To check for common method variance, we relied on the post-hoc Harman’s single-factor test (Podsakoff and Organ, 1986). The factor analysis test revealed the absence of a single general factor accounting for most of the observed covariance in the variables. Hence, common method bias did not appear to a problem with this dataset. Following Spector and Brannick (1995), social desirability bias was addressed by using a self-administered survey, ensuring complete anonymity for all respondents, and survey questions addressing dependent and independent variables being placed far apart from each other in the survey. According to Nederhof (1985), self-administered surveys may reduce social desirability bias over other data collection methods because they reduce the salience of social cues by isolating the subject. In fact, studies find that the use of self-administered surveys is generally found to be less influenced by social desirability bias than telephone or face-to-face interviews (Nederhof, 1984; Wiseman, 1972). Hence, while not always eliminating social desirability bias, indications suggest that anonymous self-administration of mail surveys gives rise to less distortion than other methods (Nederhof, 1985).

Second, the sample was drawn from Australian business firms. While we do acknowledge that the results might not generalize to other countries, the findings do extend empirical evidence beyond the US, where much CSR research takes place. Third, conceptualization and measurement of CSR is identified as problematic in the literature (Orlitzky et al., 2011; Van Oosterhout and Heugens, 2008). Thus, we made a choice to leverage a widely recognized and tested CSR construct; namely, Carroll’s (1979) construct. The use of Carroll’s (1979) work could therefore be a limitation; however, given that our interest was in expanding mediation tests of the CSR–FP relationship, we did not seek to break new ground in conceptualizing or measuring CSR but rather relied on a scale previously used in the literature that demonstrated sufficient validity and reliability. Finally, this study is cross-sectional. Clearly, the relationships proposed in this paper need to be studied over time. Addressing this limitation is an opportunity for future research.

Other future research opportunities exist as well. For example, studies could assess if certain conditions impact on firms’ ability to maintain high levels of CSR activity and whether consistently high CSR activity helps or hinders organizational success, financial or otherwise. Lastly, an important focus of recent theoretical treatments expresses interest in the antecedents of CSR (e.g. Aguilera et al., 2007). To advance the field, future research could empirically explore more closely the internal and external drivers of CSR, such as employees’ relational needs or differences in institutional drivers across countries.

In summary, we believe that the associations tested in our model provide one explanation for how CSR might be linked with FP, and why the association might be positive. In so doing, our findings overcome some of the ambiguity surrounding the CSR–FP relationship and provide insights for future research. From a more pragmatic perspective, this study further confirms that actively engaging in CSR is likely to have positive benefits for firms in Australia. The present results suggest that firms proactively engaging in CSR appear to be able to enhance reputation while improving customer satisfaction, with an indirect benefit of improved FP.

Footnotes

Appendix

Funding

This research was supported by funding from Curtin University.