Abstract

Scholars often explain the rise of tax increment financing (TIF) as a natural progression toward localized revenue sources born of devolution, increased interlocal competition for business investment, and fiscal constraint. Although such factors provide important context, our genealogy of TIF in the state of Illinois reveals that critical actors—private real estate consultants—actively promoted the adoption and subsequent promotion of TIF as an economic development tool. Through interviews and a review of primary documents, we uncover a network of private consultants who had prior experience shepherding federal urban renewal dollars to cities and who later mobilized concerns around the 1970s deindustrialization crisis to steer the use of property tax incentives from job creation/retention to real estate development.

The history of urban policy in Anglo-American countries is traditionally narrated to emphasize a critical transition that occurs during the turbulent 1970s and 1980s. It is during this period that the federal system is restructured; an ascendance of local policies occurs as central support is withdrawn and the initiation of Thatcher/Reagan-style devolution begins. Market-oriented, competitive, and entrepreneurial development strategies supplant Fordist-Keynesian or caretaker ones, such as Title I of the 1949 Housing Act (commonly known as “Urban Renewal”), which was perhaps the last gasp for federal urban policy in the United States.

Recounting these dramatic changes, some scholars assume that steep decreases in federal funding necessitated paradigm shifts (i.e., the move to neoliberal or entrepreneurial local policies) and an increased reliance on locally funded and administered policies (Clarke & Gaile, 1999; Eisinger, 1988; Peterson & Lewis, 1986). Others argue the reverse order of causation: that shifts in ideology were responsible for the subsequent rollback of the federal government and the rollout of neoliberal local policies (Harvey, 1989; Jessop, 1998; Peck & Tickell, 2002). With some exceptions, both perspectives tend to obscure human agency; actors are depicted as faceless and highly scripted in the majority of accounts of state retrenchment and entrepreneurial policy mobilization. Moreover, the narratives that have unfolded from both critical and mainstream interpretations of recent history often have been ones of clean breaks and dramatic, totalizing changes occurring during this period. 1

In contrast, we argue that important changes in urban development policy in the late 20th century were encouraged and embedded in particular locale by a set of strategic “bridging” actors, namely, real estate and economic development consultants. They are bridging actors in several senses. First, the consultants had backgrounds in public service as well as in the allied fields of appraisal, market analysis, public finance, and site location. Mediating between the real estate development field and local government policy making, consultants played a critical role in assisting private sector developers to appropriate property for “public purposes” and receive public subsidies for new construction and redevelopment. Providing advice to both developers and local officials, these market-making actors became the glue that allowed myriad public–private partnerships to flourish from the mid-1970s through the present.

Second, consultants had a vested interest in sustaining the local state’s development trajectory after federal funding for Urban Renewal dried up in the 1970s. Their personal involvement in administering Urban Renewal monies allowed for more continuity between eras than radical breaks, bringing into question the very periodization of these distinct eras in urban policy. These development professionals grafted markers and symbols from the past onto new conditions and enrolled new supporters, making it difficult to distinguish the original practices of Urban Renewal from some of the “new” entrepreneurial policies that followed in their wake.

Specifically, this article examines how private real estate consultants within the state of Illinois influenced the evolution of what has become the most commonly used urban revitalization tool of the last three decades there: tax increment financing or TIF. TIF allows municipalities to designate an area for redevelopment and to monetize the expected increase in property taxes to pay for initial and ongoing expenditures in the area. By 2009, 50 states and the District of Columbia had passed enabling legislation allowing municipalities to use TIF. 2 TIF has been called the most popular economic development strategy in the United States (Briffault, 2010; Krohe, 2007). TIF is in the process of being exported to countries such as the United Kingdom and Australia. 3

Although TIF is considered the quintessential “entrepreneurial” development strategy and is thereby associated with post–federal urban policy, the practice of using TIF actually began in the early 1950s in Minnesota and California as a creative way of matching federal block grants (Dye & Merriman, 2000, 2003). Although many aspects of the contemporary use of TIF have their roots in Urban Renewal–era legislation and development cultures, little is known about the origins of TIF beyond that. Moreover, the story of TIF’s dissemination is told largely through the apolitical lens of formal policy transfers between government actors without mention of the power of the private sector or the informal networks of public sector advisors.

In contrast, our genealogy of TIF in Illinois reveals that private real estate consultants were responsible for the adoption and subsequent promotion of this tool in that state. We argue that this support allowed TIF to not only survive the Urban Renewal period but also to expand into new realms of privatized development assistance that favored real estate development at the expense of investment in other economic sectors (Rast, 2009b). 4 Drawing on the evidence from Illinois, we extend Rast’s (2009a) argument about the postwar role that “the architects of development” involved in Urban Renewal played in reshaping institutions and building regimes in the more recent past. These actors helped establish the norms for public assistance to private development, pushing the limits of acceptable “public purposes.” Consultants translated development for planners and planning for developers. Although such forms of intermediation and expert knowledge are critical for implementing urban policy, they also create conflicts of interest, the potential for self-dealing, and the ability to steer tax revenues toward projects whose public purpose justifications are more dubious.

The Agents of Path Dependency

Following Pierson (2004), we adopt a historical approach to the study of urban development policy, not merely as a strategy to collect evidence but rather “because important aspects of social reality can best be comprehended as temporal processes. It is not the past per se but the unfolding of processes over time that is theoretically central” (p. 264). Pierson and others (see, e.g., Arthur, 1994; David, 1985) use “path dependence” to describe the idea that previous decisions and institutional structures shape the present through positive feedback processes. They assert that the timing of events determines whether certain practices become deeply embedded, widely disseminated, or dissipate into the ether. They also show how changing course tends to become increasingly costly over time. A restricted menu of likely change options exists at different historical junctures.

Although this framework is useful for understanding the stickiness of institutional development, scholars of path dependency tend to privilege structural factors over interested actors in explaining the persistence of institutions. Pierson (2004), for example, emphasizes the role of broader social processes (e.g., changes in demography or technology) in shaping institutions and warns against what he calls “actor-based functionalism,” which “typically rest(s) on the claim that institutions take the form they do because powerful actors engaged in rational, strategic behavior are seeking to produce the outcomes observed” (p. 14). Actors alone, Pierson argues, rarely possess the forethought, capacity for instrumental action, and long-term time horizons to influence institutional design.

Although we agree with Pierson’s critique, we would also point out that structures do not endure automatically (Sayer, 1992) and that the imperatives imposed by structural designs are often ambiguous (Herrigel, 2006). It is possible to focus on key agents or policy entrepreneurs without resorting to the kind of functionalism Pierson identifies. Actors may not intentionally seek the specific changes we observe in retrospect, but by pursuing their own self interests, enacting their beliefs, and enrolling others in their world views, institutional, change can occur. Rast (2011) refers to such processes as “policy feedback” whereby “self-reinforcing processes ensue in which actors benefiting from and empowered by a particular initiative use their enhanced positions to press for its expansion (Mahoney, 2000)” (p. 8). Chwieroth (2010) labels the approach that analyzes agents in this fashion as “strategic agency,” whereas others refer to it as “strategic constructivism,” and to agents as “norm entrepreneurs” (Finnemore & Sikkink, 1998; Jabko, 2006).

Agents tend to act collectively as opposed to independently, and as such, the notion of a profession is a more socialized and less functionalist way of looking at strategic behaviors. Pierson (2004) acknowledges that “ideas are frequently shared with other social actors in ways that create network effects and adaptive expectations . . . (social norms) chronically reproduce themselves” (p. 35). Sayer (1992) too notes that transforming and reproducing social structures is “a skilled accomplishment requiring not only materials but particular kinds of practical knowledge” (p. 96). Professions contain self-interested actors who are socialized through repeated interactions, a homogeneity of background, and dependence on similar sources of remuneration into common world views. Possessing expert knowledge, professionals seek to establish a monopoly on that knowledge and the services derived from it (Macdonald, 1995).

Although professional world views are themselves internalize norms among their members” (Finnemore & Sikkink, 1998, p. 905). Professions are inherently expansionist, pushing the boundaries of expertise into new areas so as not to be trumped by some other professional community doing the same (Abbott, 1998). At the same time, they are slow to change their core beliefs and practices if change will disrupt their traditional sources of funding, legitimacy, and status. They are protective of their power and use institutional change (e.g., altering educational or certification criteria) to move into new territory, shore up their own legitimacy, and fend off challenges. Professions are particularly adept at using discursive tactics to cast “a new set of events as representing a ‘crisis’ for opposing views and frame new initiatives so that they resonate with prevailing organizational beliefs, principles, and practices” (Chwieroth, 2010, p. 14).

In this article, we trace the role played in Illinois by a rather loose-knit profession—real estate consultants—in maintaining the continuity of state market configurations that have come to define the field of local economic development. We selected the state of Illinois for this inquiry because municipalities there have struggled with deindustrialization and have invested a large proportion of their budgets in economic development–related activities. Moreover, because of the state’s association with political corruption (a recent study classified it as the third most corrupt state in the country; see Simpson et al., 2012), the politics of economic development decision making has been better documented there than it has in other states. We follow the methodological guidance of those sociologists, geographers, and political scientists employing a “historical social network analysis” that traces relevant individuals and their cross-border relationships (see, e.g., Mirowski & Plehwe, 2009). First, we defined the core of the network as “self-conscious” advocates for public subsidization of real estate development in the state. We identified these advocates through an archival reading of the legislative debates and expert testimony in support of TIF and reviewing collected reports about the policy from mainstream media sources and trade journals dating back to the early 1970s. Then we conducted lengthy, unstructured interviews with 17 of these bridging actors—partners at consulting firms, legislative and administrative staff, and current and former municipal officials—to follow the channels of communication between consultants, local governments, and the state of Illinois. 5 Interview transcripts are in some cases quoted directly, but we do not identify sources to protect their identities.

The picture that emerges from these sources of data is one of interlocking networks of public and private real-estate actors using the crisis of deindustrialization starting in the 1970s to normalize the public provision of property tax-based subsidies for general-purpose real estate development. Such practices displaced, to some extent, other potential trajectories of economic development (e.g., modernizing manufacturing processes) whose advocates lacked the proximity to sources of capital and expertise that four decades of Urban Renewal helped accrue. They also helped institutionalize a form of privatism and public sector generosity toward the real estate sector that may not have become routine had an alternative development pathway taken hold.

The Historical Antecedents of Tax Increment Financing

Urban renewal is not dead, but alive, and trying to get well. The use of local initiative through the use of tax-increment financing will do much to speed the healing process. (David Hegg, 1973)

The Mechanics of TIF

TIF is a local economic development policy that allows municipalities to designate an area for redevelopment and use the expected increase in property taxes there to pay for initial and ongoing redevelopment expenditures. 6 Despite the state-by-state variation, common features of state-enabling legislation include outlining the designation process (including any required notices and public hearings) and a listing of what public and private expenditures may be lawfully financed by TIF (Weber & Goddeeris, 2007). Legislation must conform to state constitutions, which require that taxing districts spend public money for “public purposes” (Schoettle, 2003). What constitutes a bona fide public purpose is rarely spelled out in detail in the legislation although the doctrine has been defined by case law over the years. To protect against accusations that public purposes are not legitimate, TIF-enabling laws generally require that localities meet two tests: First, they must demonstrate that properties within a specific sublocal area are “blighted,” and second, they must demonstrate that these properties would not be developed “but for” the use of this mechanism.

State-enabling legislation may set out requirements for the physical boundaries of the proposed redevelopment project area. In Illinois, for example, the project area must be at least one and one-half acres in size, contiguous, and contain only properties that will be “substantially benefited” by the proposed TIF plan. The boundaries are often highly irregular and the areas covered varied. After public hearings, the city council passes an ordinance that approves the plan, designates the area as an official redevelopment district, and adopts TIF. TIF districts have life spans that, in most states, are close to 20 years (23 years in Illinois).

The workings of a TIF district are relatively straightforward: All taxpayers in the district pay real estate taxes on the value of their property but, for the life span of the district, the taxes on any new value (i.e., the “incremental” taxes above those collected when the TIF was designated) are used to pay for any eligible public improvements. In this sense, TIF is a textbook example of what public finance economists call “value capture” (Youngman, 2011, p. 321). Overlapping taxing jurisdictions (e.g., school districts) continue to collect revenues on the value of the properties within the district before the TIF was designated.

Once a TIF district is in place, developers and building owners who wish to undertake a project within it apply for funding from the local government or redevelopment agency. States delimit the eligible costs that the TIF increment can subsidize. These typically include those for land acquisition and conveyance, demolition, parcel assembly, land preparation, historic rehabilitation, and other façade improvements. Most TIF legislation also allows municipalities to offer subsidized, below-market rate financing to private developers from the increment. Importantly for this article, TIF funds can be used to cover the cost of planning studies, surveys, and redevelopment plans undertaken by real estate consultants.

If the municipal administration is supportive of the project, it will grant a portion of the project’s development costs as the “TIF allocation,” a commitment of future property taxes from the district. However, developers require the funds immediately, so municipalities “front fund” the project by pledging future property tax revenues as security for borrowing in the present. Municipalities repackage the rights to streams of incremental property tax revenues into fungible bundles and sell these rights as bonds or shorter-term financial instruments. These tax-exempt bonds allow municipalities to avoid constitutional and statutory debt limitations and voter referenda (Sbragia, 1996). 7 In this way, local governments can obtain immediate capital for developers by selling their future property tax revenues in the public debt markets—often without the knowledge of the individual property owners paying their tax bills.

How TIF Became “the Most Popular Tool” 8

Most municipal officials and many scholars explain the meteoric rise of TIF in the last quarter of the 20th century as an example of fiscal ingenuity and revenue chasing in the face of declining federal funds (Clarke & Gaile, 1999; Eisinger, 1988). On average, in 1978 some 15% of city revenues came from the federal government (more than 25% for some major cities), whereas in 1998 less than 3% were derived from federal sources (Kincaid, 1999). At the same time, state property tax revolts and restrictions on tax exempt bonds placed caps on the amount of revenue that could be extracted from local property owners. The dwindling supply of federal grants, coupled with state-imposed restrictions on debt and property tax growth, induced panic and prompted cries of urban fiscal crisis throughout the post-devolution era.

The post–federal era is associated with several different kinds of “entrepreneurial” economic development strategies, of which TIF is considered but one. Eisinger (1988) documents the growth in a number of economic development strategies and their use starting in the late 1970s. Clarke and Gaile (1999) note that the municipal taste for risk, financial complexity, and profit sharing from property development increased after 1980. Both sources classify tools in ways that assume a good fit between the fiscal constraints and the tools selected, arguing that TIF is part of a progression toward more localized revenue sources, such as property taxes and land-based economic development schemes.

Out of the multitude of different abatements, deductions, and public assistance offered by municipalities for private sector projects with an arguable “public purpose,” local governments have some discretion over which strategies they adopt. The available tools at any historical juncture, however, are limited by prevailing ideologies and legal precedent. We contend that policy interventions generally, and economic development strategies specifically, rarely represent a complete break from those of the previous era. Not only do local governments lack the internal capacity to innovate, but they are influenced by what we call “bridging” actors outside of government who have vested interests in maintaining earlier arrangements. Policy feedback further sustains this cycle; drawing from E. E. Schattshneider, Pierson (1993) and Rast (2009b) both note that policies themselves often drive politics. In this way, agents help reinforce path dependencies and particularly in realms of great uncertainty, such as large-scale public investment, the tendency of governments to cautiously stick close to tested paths. Certain tools fall out of favor or are temporarily eclipsed by others that exploit a particular historically contingent opportunity. Indeed, Sbragia (1996) notes that the history of public finance for private development is one of strategic circumvention: as one path is shut down (through legislative fiat, for instance), other ones are hewn. But dependence on entrenched networks of policy actors ensures that these “new” paths are often composites or variations of earlier strategies.

In many ways the history of TIF follows from these ideas. The ideology underpinning it can be traced to the late 19th century with the use of “special assessment districts” (Briffault, 1990, 1997, 2010; Diamond, 1983). The notion that public improvements have localized impacts is the justification for the use of both special assessment districts and TIF districts. Assessment districts were developed to pay for new public improvements whose benefits were primarily restricted to the immediate neighborhood. If property taxes are generated in a specific location, the logic goes, then that these funds should also be used in that same area instead of being channeled to other parts of the municipality. Special assessment districts levy an additional tax to property owners near the new infrastructure, the cumulative value of which covers the cost of the initial expenditure.

Special districts have been a standard feature of the Midwest’s political geography since cities there did not have the history of strong centralized local governments that East Coast cities did (Einhorn, 1991; Fuchs, 1992). These newer cities developed governance over large regions and isolated resources before norms about the reach of the state became institutionalized. In Illinois, for example, Republican legislators preferred to grant Democrat-run cities the right to create special districts rather than liberalize general taxing and revenue policies. Chicago and other Midwestern cities divested the cost of services to these districts, relieving themselves of substantial fiscal pressures that other, particularly Eastern, cities carried themselves (Fuchs, 1992).

Assessment districts, however, are used primarily to finance publicly owned infrastructure such as sewer lines, whereas TIF often channels tax revenues to private, for-profit development projects, the spatial benefits of which are often much more narrowly concentrated. With TIF, the idea of spatially localized taxpayers paying for spatially localized benefits was carried over from earlier assessment districts, but the definition of public benefit and purpose was expanded.

To extend the definition of allowable “public purposes” to which public funds could be directed, TIF drew heavily from state urban renewal statutes. Indeed, TIF arose out of a desire to provide a local match for federal grants during the Urban Renewal period. 9 The Housing Act of 1949 (Title I) and the Amending Act of 1954 authorized the use of federal dollars to purchase inner-city property for urban redevelopment. Massive amounts of federal funds flowed into U.S. cities through the 1970s, subsidizing developers and unionized construction workers with cleared prime land at bargain-basement prices (i.e., “write-downs”). To receive the federal funds for land acquisition, cities were required to draw up plans for development, form renewal agencies emboldened with new legal powers, create mechanisms to quickly appropriate devalued property, and come up with local matching funds (Beauregard, 1993; Rast, 2009a; von Hoffman, 2000). The states of Minnesota (1947) and California (1952) were the first to authorize the use of TIF as an option for providing such a match. These early statutes allowed either municipalities or, in the case of California, counties to pledge future property tax growth to assist with renewal projects.

State urban renewal statutes listed “blighting factors,” which had to be found in the area to justify using public police and expenditure powers to benefit private actors. Blight allowed municipalities to take property through eminent domain and direct public tax dollars to redevelopment projects (Beauregard, 1993; Fogelson, 2001; Page, 1999). Here, as in the later TIF legislation, the definition of blight is vague; it is both a cause of physical deterioration and a state of being in which the built environment is deteriorated or physically impaired beyond normal use. Blighting factors include the age of buildings (their “useful life,” in most cases, was considered 40 to 50 years), density, population gain or loss, overbuilding on lots, lack of ventilation and light, and structural deterioration.

It was believed that property could be better sanitized in its empty state, thus eliminating the possibility of the blight returning; therefore, blighted areas needed to be removed through massive clearance rather than rehabilitated through additional investment (Weber, 2002). Indeed, TIF embodies another critical idea from the Urban Renewal period: the notion that removal of unsightly or obsolete property would improve living conditions. This kind of physical determinism relieves local governments of responsibility for the more intractable socioeconomic problems that may have led to declining real estate values or abandoned property in the first place.

The other requirement of TIF, the “but for” test, is harder to trace, but elements of it appeared in the state urban renewal statutes as well. These statutes required that municipalities attest that the area in question would not develop to its “highest and best use” in the absence of public assistance. In other words, the options of not providing public assistance were stasis or continued decline (“let nature take its course” noted Homer Hoyt and Leonard Smith, 1943; quoted in Fogelson, 2001). This difficult-to-demonstrate but easy-to-argue test harkens back to the notion that every area is a potential slum. The statutes reflect a confidence in the ability of the public sector to manipulate private markets to cause a visible turnaround (Persky, Felsenstein, & Wiewel, 1997).

The federal government formally terminated the Title I program in 1974, channeling some of the financial support for urban redevelopment to the Community Development Block Grant and Section 8 programs. Noting the “federal roots of entrepreneurial activity,” Clarke and Gaile (1999) point out that these new programs not only supported more local development activity but also influenced the types of strategies adopted during the 1970s and 1980s. It is during these transitional years that states beyond Minnesota and California adopted TIF-enabling legislation and the use of TIF accelerated.

To justify the continuation of public revenue transfers to the private sector, municipalities did not jump boldly into new territory but rather adhered to the well-worn strategy of identifying properties with diminished value (“blight”) and potential to be redeemed through public intervention (“but for”). Sticking to this path and adopting similar parameters to the urban renewal statutes allowed municipalities and consultants to subtly shape the grey area that separates public purposes from private ones. As Rast (2009b) notes: Urban renewal legislation created incentives for large-scale redevelopment and encouraged public-private partnerships. Within that framework, multiple outcomes were possible. For one thing, the location of urban renewal projects would have to be determined. . . . In addition, there was the question of which economic sectors should be targeted. Should redevelopment efforts emphasize manufacturing, services, or some combination of both? (p. 401)

During the transition from federal block grants to local property-tax funded redevelopment projects with TIF, the direction that publicly subsidized development could take (i.e., appropriate locations and land uses) was also on the table. In Illinois, as we will show, the active involvement of private real estate consultants in developing the enabling legislation for TIF and marketing TIF to municipalities helped steer this new instrument away from an employment-oriented economic development tool toward its present incarnation as an all-purpose real estate redevelopment one.

The Role of Consultants

Consultants, whether management consultants or other professional providers of advice, are not simply the passive receptors of policies devised by elected officials but rather actively shape the policies and conditions that justify their activities. In addition, consultants’ power is enhanced by the very models of governance they advocate—namely, those that “remove decisions from politics, and thus public scrutiny” (Saint-Martin, 2004, p. 20).

Local economic development consultants take several forms and have complicated histories. Originally economic development consulting emerged from coalitions of civic boosters and promoters who rallied to bring rail depots and industry to their locale (Blakely & Leigh, 2010; Sbragia, 1996). LeRoy (2005) recounts the 1934 birth of Fantus Factory Locating Service, the nation’s first site consultant firm. The site location function would come to define a core activity in the field of economic development over the next 40 years, so that by the 1970s private consultants in this field were skilled in the practices of “business climatology” (LeRoy, 2005, p. 79). Markusen (2007) argues that these consultants helped create the “emergence of an organized U.S. ‘market’ for mobile plants and the jobs and tax base they bring” (p. 5).

Major cities only began to create offices and agencies for economic development in the late 1970s and 1980s. For example, Minneapolis established its Community Development Agency in 1981, whereas Chicago opened its equivalent, the Department of Economic Development, in 1982 (Eisinger, 1988). These governmental bodies were initially focused on industrial attraction as businesses became more mobile and the amount of public funding devoted to pinning them down increased with new appropriations and bond issuances. When the public sector could not afford to hire their own staff to manage their business attraction and retention services, they contracted out to consultants, who had defined their roles as providers of this type of specialized knowledge (Dock, 2009). In this sense, the rise of the economic development consulting firm may track the fiscal fortunes of municipalities and the growth of contracting for services more generally. When revenues are tight, local governments can afford few paid staff of their own (Morning, Hirlinger, & England, 1988). 10

TIF consultants come out of more general purpose economic development consulting and have backgrounds in site location in addition to real estate, regional economics, market analysis, public finance, and site planning. They are represented professionally by national membership organizations such as the Urban Land Institute, the Council of Development Finance Agencies, and the International Economic Development Council, as well as by smaller state-level associations such as the Mid-America Economic Development Council. As the case study of Illinois will make clear, TIF consultants are often former municipal administrators who have walked through the frequently revolving door that separates public from private sectors. Acting as bridging actors between the planning functions of local government and the commission-driven work of consulting, their professional practices provide the mortar that holds together the complex networks governing contemporary urban development.

Mobilizing Tax Increment Financing in Illinois

In Illinois, TIF consultants were instrumental in sustaining the practices of the Urban Renewal era by constructing new institutions in line with older ideas. Consultants not only advocated for the passage of legislation authorizing TIF but also drafted that legislation. They marketed TIF as an indispensable tool to local governments and then situated themselves in the cranny between developers and local governments so that they could facilitate transactions between the two. This position afforded consultants the power to shape post–federal urban redevelopment policy.

The 1970s

The state of Illinois passed enabling legislation for TIF in 1977 (Public Act 79-1525), a good 20 years after Minnesota and California did and about 3 years after the formal demise of Title I. At this time, the state was in a period of prolonged economic free fall as its manufacturing base was decimated by inflation, high gas prices, and the stirrings of an increasingly globalized economy. Although the degree of fiscal instability and deindustrialization were widely recognized as leading to a state of crisis, investment in a real estate model of economic development was not a foregone policy conclusion. In fact, alternative models for local development were propagated during this period by a vigorous industrial retention movement, both in Illinois and across the nation (Clavel, 2010). Local economic development practices ranged from “smokestack chasing” to growing small businesses locally, incorporating new uses of eminent domain and zoning, and developing industry task forces to help firms with internal restructuring and modernization of work processes. In addition, community and labor initiatives included employee buyouts, experiments in worker management, support organizations that provided research and technical advice, and laws requiring advance notice of plant closings (Clavel, 2010; Rast, 1999).

In his study of Chicago, Rast (1999) argues that within the context of global economic change, two coherent economic development alternatives presented themselves, each favoring very different segments of the urban community. On the first model, the chief beneficiaries would be downtown property developers, landowners, and other groups with a stake in the commercial and residential development of Chicago’s downtown area. On the second model, those standing to gain were a select group of manufacturers, workers, and residents from working class communities with an interest in preserving the city’s blue collar jobs base. Both models presented coherent opportunities for economic growth. Neither one could be put into practice without aggressive support from city government. (p. 6)

In the framing of the policy dialogue around TIF in Illinois, a line was successfully drawn between concerns about the loss of manufacturing jobs to a general lack of private investment in real estate. The legislative debate shows that TIF originally was sold as a way to reverse the course of decline in the state’s more depressed urban areas, particularly their retail and industrial districts. Like the Enterprise Zone program that was passed by the General Assembly 5 years later, TIF in 1977 was intended to be a funding source of last resort to attract private investment to difficult-to-develop commercial areas. Senators from Chicago (Howard Carroll) and Rockford (Vivian Hickey), two cities particularly hard hit by deindustrialization, were the bill’s sponsors. Noted Senator Carroll: Very simply put, the idea is that today our urban centers throughout Illinois are not capable of rejuvenating themselves. There is no federal money available. There is no private development money available, and the reason is because we have some blighted or near blighted structures in our urban centers that are decaying, that nobody can afford in today’s market to buy those structures, demolish them, and rebuild those urban centers. What the law does, it provides a municipality with that tool of self-help . . . this (TIF) is a way of local government, by its own bootstraps, cleaning up its own areas, without a real cost to the taxpayer. (Senate Transcript, June 2, 1976, pp. 50-51)

The time may have been ripe to institute programs like TIF, but economic and fiscal conditions in the state are not a sufficient explanation for why Illinois adopted this specific mechanism in 1977. To understand how policy dissemination occurs and how particular programs wend their way through a fragmented system of independent local governments facing similar challenges, it is necessary to identify the specific actors involved in TIF’s early promotion.

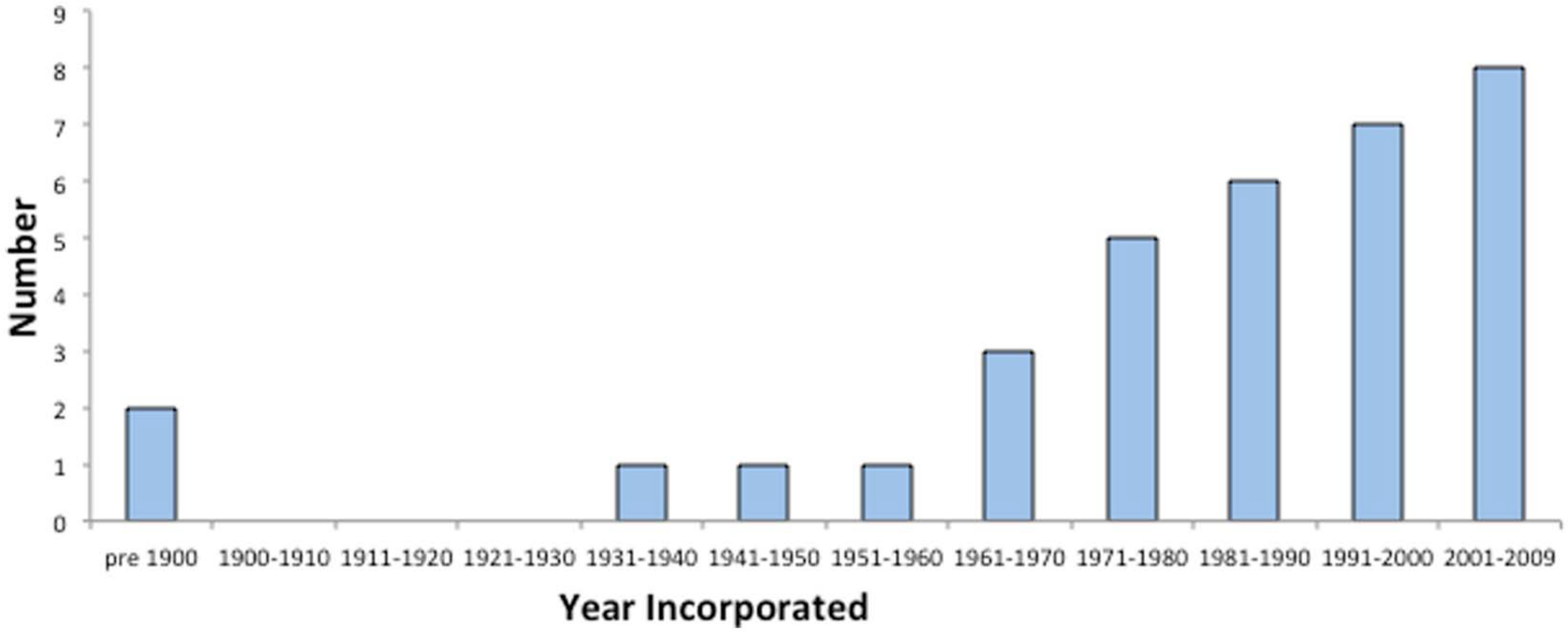

Interviews with legislative staff and private real estate actors active during this period reveal that the impetus to adopt TIF in Illinois came primarily from the private sector, namely, the real estate consulting, public finance, and law firms who counted both developers and local governments as their chief clients (interviews with Legislative Staffer A , personal communication, July 2009, Consultants A and B , personal communication, December 2009). A small group of planning and architectural consulting firms were involved in offering economic development advice to municipal clients and were incorporated during this transitional period (see Figure 1). For example, Peckham Guyton Albers & Viets (PGAV) opened its doors in St. Louis in 1970, Trkla Pettigrew Allen & Payne was founded in Chicago in 1977, and Camiros started in Chicago in 1976.

Consulting firms operating in the Midwest providing TIF services, by year of incorporation in Illinois.

It is important to note that in many cases, the principals of these firms had moved from administering urban renewal funding in the public sector to private consulting work in the early 1970s when public sector employment was shrinking. For example, PGAV’s directors were the former director of the St. Louis Housing Authority and the former director of development for the city of St. Louis. Trkla Pettigrew’s directors previously had worked for the Chicago Housing Authority, and Camiros’ principals had connections at the Illinois Housing Development Authority. In other words, these individuals were critical members of the urban growth coalitions of the 1960s and were instrumental in bringing federal funds to Midwestern cities. They crafted the predecessors of what would later be called public–private partnerships, which would stabilize over the next several decades in the form of TIF.

Consultants at these new firms knew that the loss of Title I and CDBG funding in the late 1970s threatened the growth coalitions that had been put in place during the Urban Renewal era. As one consultant noted: In the 1970s those of us who had cut our teeth on the federal programs were actively trying to find a replacement for Title I. We started looking around to other states. . . . When the money went away, downtown redevelopment projects ground to a screeching halt. Even the school districts recognized that there was a funding void for redevelopment. . . . And if there was no funding, the cities were going to lose out to the suburbs and stagnate. (Interview with Consultant C, personal communication, October 2009)

Consultants saw that TIF offered them a second chance and began actively promoting this policy in Illinois. Several of the key partners from these firms hailed from the state’s core industrial regions and had strong personal convictions about the need for public aid to save both the heavy manufacturing sector and central business districts of cities. They also maintained strong ties to the state general assembly. Legislators used scare tactics to drum up support for the idea of robust local government intervention. Representative Michael Madigan argued: The fact of the matter is that today in the central areas of those metropolitan areas, Chicago, Evanston, Oak Park, Harvey, there is decay, there is deterioration . . . unless there is some governmental mechanism provided, which will act as an incentive toward development, the decay, the deterioration will continue and it will spread block by block by block, and then it will destroy your central business district. (House Transcript, June 10, 1976, p. 175)

Advocates for TIF moved back and forth between public and private sector positions, weaving networks of municipalities, consultants, and developers closer together. Don Eslick, for example, the future director of the Illinois Tax Increment Association, worked for both the lieutenant governor and speaker of the house as well as the financial consulting firm Kane McKenna before he became the primary advocate for TIF in the state. Observers from both public and private sectors note that consultants effectively wrote the original legislation for TIF in Illinois (Interviews with Legislative Staffer A, personal communication, July 2009, Consultants B, personal communication, December 2009, C, and D, personal communication, October 2009). Eslick, as well as PGAV partner Fred Walton and private attorneys Kai Nebel and Jack Teplitz, are attributed with drafting and lobbying for the original TIF legislation (Interviews with Legislative Staffer A, personal communication, July 2009, Consultants B, personal communication, December 2009, C, and D, personal communication, October 2009).

The TIF-enabling legislation was passed in the first year of Republican governor (Big) Jim Thompson’s 14-year reign over a Democrat-controlled legislature. Although critical Republican governor–Democrat mayor alliances were forged through downstate Senate and House legislators that mustered support for urban-favoring programs like TIF and Enterprise Zones, the political culture in Springfield in the late 1970s was not particularly innovative (Interview with Legislative Staffer A, personal communication, July 2009, Consultant C, personal communication, October 2009). The legislature lacked the research staff to develop original programs, and like many state agencies, officials and legislators were open to ideas that were adopted elsewhere but seemed to have a good “fit” with the conditions and fiscal structure of their particular state. Representative Tuerk from Peoria noted in support of TIF: This bill allows cities to make the public investment needed to attract some private development and pay for it with a larger than usual share of the increased property taxes that result. It is an innovative type of plan, despite the fact that it is innovative to Illinois, it is a matter of statute in 14 states. It has been on the books in California for some 20 years; and it has been quite successful on the west coast. (House Transcript, June 10, 1976, p. 163)

Minnesota’s experience with TIF, observed by the planning consultants whose reach included the central states, demonstrated that a West Coast tool could be successfully imported to the Midwest (Interview with Consultant C, personal communication, October 2009). The Illinois Departments of Revenue and of Commerce and Community Affairs were amenable to any program that could encourage local economic development without requiring additional state appropriations (interview with Legislative Staffer A, personal communication, July 2009). This supports much of the research on policy diffusion, which acknowledges that governments often adopt policies because their peers do (see Simons, Dobbin, & Garrett, 2006).

The 1980s

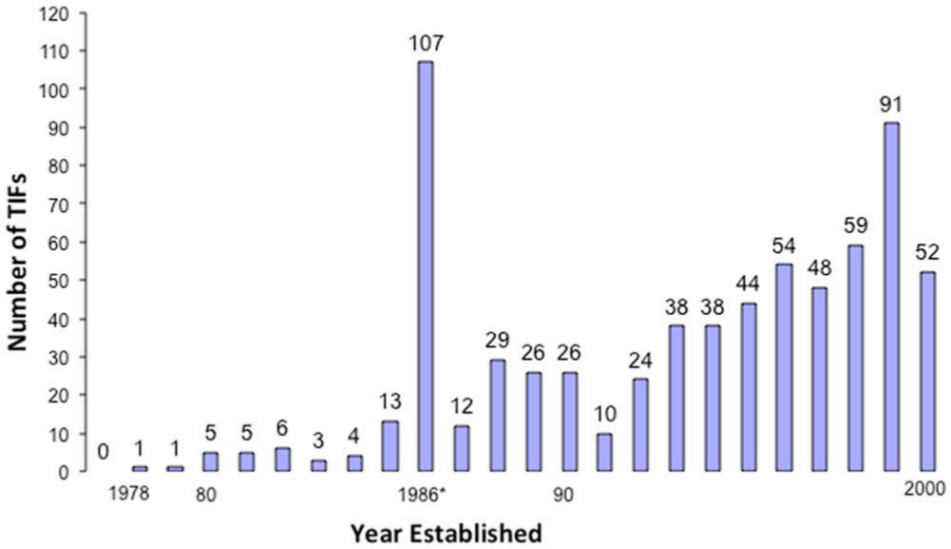

Despite the articulated “need” for economic development interventions to stem industrial job loss, TIF was ignored in Illinois for almost the first decade of its life. Only 26 TIF districts were designated in the state between 1977 and 1984 (see Figure 2). Most of these were in downstate municipalities and Chicago suburbs, such as Homewood and Rosemont. The city of Chicago, for example, was slow to pick up on TIF and ignored the tool throughout much of the building boom of the 1980s. During this time the city was more of a spectator in the “great game” of downtown land trading and development, controlled as it were by a handful of key operators (Miller, 1996). These same local developers dominated the zoning board and planning commissions and were responsible for spurts of building, such as the one between 1979 and 1986 that alone pumped $11 billion into the central business district (Miller, 1996). During the 1980s boom, developers rebuilt the frame around the historic core, adding more than 30 million square feet of Class A office space. Although they fastidiously manipulated the zoning code for maximum floor area and benefited from land write-downs, developers went about their business without much direct financial assistance from the municipal government.

Illinois TIF districts by year established.

The reluctance to adopt TIF after the passage of the 1977 enabling legislation stems in part from the fact that municipalities were slow to move beyond behaviors learned during the Urban Renewal era. City agencies continued to focus on the federal government and the state of Illinois for assistance with urban development, squeezing the waning Urban Development Action Grant, Housing Opportunity Development Action Grant, HUD Section 401 loan guarantees, and Illinois Development Action Grant programs dry (interview with Municipal Attorney A, personal communication, August 2009). In addition, TIF was set to capture new growth in the general fund, which city council members had become adept at draining and steering back to their districts. In other words, TIF promised a reconfiguration of fiscal authority, and elected officials were uncertain about who stood to gain or lose from such a shift. Moreover, local governments were wary of taking control over a property tax base shared by multiple taxing jurisdictions (such as school districts, who received the bulk of local revenues; interview with Legislative Staffer B, personal communication, July 2009).

Additionally, the financial networks and infrastructure necessary to launch TIF were still not in place at this time. TIF was untested and unfamiliar to the local banking community, and municipalities lacked the accounting systems to manage such a program (interview with Municipal Attorney A, personal communication, August 2009). Initial attempts to sell TIF securities met with skepticism. The banking community was hesitant to accept IOUs based on speculative streams of future property tax revenues that were not backed by a municipality’s full faith and credit.

Sensing that the TIF program had stalled out, Fred Walton of the St. Louis consulting firm PGAV proposed in 1984 that municipalities be allowed to capture all subsequent sales tax growth in the TIF districts (instead of sending sales tax “increments” back to the state). 11 This proposal was attractive to municipalities because, in contrast to property taxes, sales taxes could provide a revenue stream early on in the district’s life. Retaining sales tax increments would allow municipalities to avoid expensive trips to the bond market for each project and would enable them to jump-start the retail projects that were gaining steam as the manufacturing sector languished. Walton lobbied those elected representatives whose constituencies were concerned about the decimation of the state’s manufacturing base, framing TIF as a remediation measure for deindustrialization—even though many of the TIF districts would be designated for retail uses only.

Senator Phil Rock, a Democrat from the Chicago suburbs who would go on to spend seven terms as Senate president, sponsored the sales tax amendment to the TIF enabling legislation in 1985. 12 The legislative change passed despite some early administrative opposition to what appeared to be the state’s open-ended contribution to local economic development through its foregone sales taxes. However, there does not appear to have been any floor debate on the amendment, due possibly to the weak committee structure and a lack of understanding of the mechanics and fiscal implications of TIF for the state (interview with Legislative Staffer A, personal communication, July 2009). The amendment allowed all municipalities who designated TIF districts before 1987 to collect any incremental sales tax revenues generated after 1985. Procedures for applying for and distributing this new form of state development aid (which totaled more than $10 million in just 1988) were promulgated in an amendatory act in 1986. Sensing potential liability for municipal overspending, Governor Thompson set a 1-year sunset that phased out new sales tax TIF district designations by 1987. This provided the impetus to designate these districts quickly and without much thought to their specific development needs or goals. 13

After the legislation’s passage, consultants teamed up with the state’s economic development agency and the Illinois Municipal League for an aggressive marketing campaign intended to drum up support for TIF from municipalities (Redfield, 1995). More concretely, consultants offered municipalities assistance with setting up the necessary TIF accounting infrastructure and writing the eligibility studies and redevelopment plans required by law to initiate and designate the districts. In drafting the eligibility study and redevelopment plan for the district, consultants established that the “blight” and “but for” conditions were met. The plans were reviewed at public hearings at which the consultants often represented the city in taking questions from residents and local property owners. The short window provided by the amending legislation and the subsequent road show appears to have worked: In 1986, more than 100 municipalities created 137 “sales tax” TIF districts (these districts could collect property tax increments as well; see Klemens, 1990).

The Illinois Tax Increment Association (ITIA) was formed in 1987 to respond to the rapid growth in TIF districts that occurred after the passage of the sales tax amendment. The founders of the ITIA became the protectors of the state statute and helped to professionalize the disparate consultants who were taking on municipal TIF work. Not only did the organization help cement the norms, identity, and objectives of this emergent consulting profession (see Chwieroth, 2010; Finnemore & Sikkink, 1998), but it also provided a rich source of networks through which to circulate and debate ideas and policy knowledge (Mirowski & Plehwe, 2009). The ITIA became the main lobbying body for TIF-related legislation in Springfield. Comprised of the key TIF consultants 14 and entrepreneurial municipalities, the organization provided resources and encouragement so that even the most hesitant local officials would adopt TIF. They gave legal advice to municipalities where community organizations challenged TIF designations and sought to protect the rights of municipalities to engage in eminent domain and control their revenue structures.

During this time, consultants expanded into new realms. They were hired by developers to make a public benefits case for TIF assistance to municipalities and negotiate an amount of public subsidy. In other words, consultants helped transform the private project into something worthy of municipal assistance by framing it in terms of a public purpose (e.g., additional tax revenues for the public sector, the removal of an eyesore, job creation). Their involvement in this area gave them the power to shape the public purpose doctrine described above. They found themselves advocating for fewer industrial job creation and retention projects and for more mixed-use, residential, and downtown redevelopment projects (interview with Consultant A, personal communication, October 2009). Consultants argued that the market was forcing this change as few industrial tenants and developers were moving to the state or expanding their facilities (interview with Consultant A, personal communication, October 2009, and B, personal communication, December 2009; interview with Municipal Official A, personal communication, September 2009).

Consultants were also hired by municipalities to help them review prospective developers and deals. Because city planners often lacked the requisite knowledge of development finance, private consultants scrutinized developer requests for assistance, offering advice on how much subsidy to provide and what form it should take (i.e., “deal review”). They helped decide the terms of the redevelopment agreement that governed the provision of public assistance (i.e., land, financing) in exchange for the developer’s agreement to specific public benefit covenants.

Given how easy it is to generate conflicts of interest by playing both sides, these different roles were intended to be filled by different consulting firms. In other words, the same firms were not supposed to advise both the municipality and the developer for fear that they would convince the municipality to succumb to the developer’s wishes or vice versa. However, in keeping with Durkheim’s (1933/1977) notion that professions are expected to police themselves, TIF consultants had only their moral contempt to discourage such questionable behavior, and this was often insufficient. 15 “Of course, there are some charlatans in our profession,” noted one Illinois consultant, “but for the most part we follow an unstated code of good behavior.” The ITIA also saw itself as offering advice to consultants on how they could better follow the letter of the law and providing the peer pressure necessary to “weed out the bad seeds” (interview with Consultant A, personal communication, October 2009).

The 1990s

Between 1987 and 2002, 635 new TIF districts were designated in Illinois, at an average of 45 per year. 16 This decade also represents the maturation of the TIF program in Illinois as its reach was extended to include almost every kind of real estate development project and every kind of municipality. Municipalities and developers stretched the tool to fit most circumstances, for example, building new institutional buildings, market-rate residential construction, and even golf courses. Although the passage of the original enabling legislation was based on the promise of job creation and industrial development, TIF was gradually turned into an all-purpose property development tool. The legislation was written so loosely that actors could exploit its flexibility and the gray areas where the law did not reach. Noted Chicago’s commissioner for community development, “All projects have gap financing needs, and TIF completes the deal.” 17 The original focus on depressed urban areas and industrial job retention and attraction was often ignored to focus more on property redevelopment generally.

Consultants and municipalities occasionally pushed the boundaries of TIF use to the limits of what was legally acceptable. The ITIA did not sanction or disbar members who, for example, took an annual cut of municipal increment as an advising fee or who used TIF to pay for fireworks on the Fourth of July (interview with Consultant B, personal communication, December 2009). There was little public pressure to stop either municipalities or consultants from using or proposing TIF for questionable projects. In fact, until the mid-1990s, there was very little media attention to TIF; no major Illinois newspaper ran a story about the passage of the enabling legislation or even the sales tax amendment. As such, public scrutiny of the deals and of the professional networks supporting them did not surface until the program was well established.

In some municipalities, particular consultants were embedded in governance regimes that lasted for decades. For example, the city of Chicago provided “master contracts” for its TIF work to three consultants who would remain active on the TIF front for the next two decades: PGAV, Stephen B. Friedman and Associate, and Teska Associates. The city seemed to have a particular relationship with these consultants. Unlike in other municipalities in Illinois, so many public actors were fighting to control the same monies and take credit for development projects (e.g., the 50 city aldermen) that consultants found themselves with less influence (interview with Consultant A, personal communication, October 2009). Chicago TIF consultants complained that their policy wisdom was often ignored and that they were restricted to the mundane details of the deals. They were able to exert more power over TIF decisions in smaller communities where the shortage of knowledgeable municipal staff allowed them more control. And in still other municipalities, consultants acted more like “guns for hire,” lending their expertise to projects on a short-term basis.

The need for success in financial intermediation, particularly the sale of TIF-backed bonds and notes, tied municipalities to a handful of financial consulting firms that provided these services. Some were strictly financial advisors (i.e., Certified Independent Public Finance Advisors) such as Kane McKenna or Ehlers and Associates, while others played multiple roles as advisors, underwriters, and brokers, such as William Blair & Company, LaSalle Bank, and A.G. Edwards. As the TIF notes and bonds were initially very hard to sell, these specialized underwriting boutiques became important agents in the networks of fiscal governance assuring dispersed investors of the security and appreciation potential of local property (Weber, 2010). They made the uncertainties associated with using yet ungenerated property tax revenues more legible to investors by turning abstract risk relationships into feasibility reports, forecasts, coverage ratios, and cash flow projections (Weber, 2010). Their ability to “manage” risk is key to understanding the professionalization of the field of economic development.

In 1999, amending legislation to the original TIF-enabling act relaxed the requirements for designating new TIF districts. 18 This legislation harkened back to urban renewal statutes that viewed all properties as tottering on the precipice of decline. No longer did parcels have to be “blighted.” If 50% of the improved parcels in the proposed districts were more than 35 years old and could potentially become blighted in the future, they were eligible for a TIF overlay.

The real estate bubble of the late 1990s and early 2000s helped create the feedback effects that locked in TIF. So many TIF districts were in place before the upturn that when the boom came, it allowed Illinois municipalities to amass millions of property tax dollars in their TIF accounts. During the latter half of the decade, the greatest number of new TIF districts came on line to date and importantly, the number of development projects financed by TIF skyrocketed. In 2000, TIF districts generated approximately $5 billion in incremental equalized assessed value or 2.5% of the state’s total property value (Illinois Department of Revenue, 2000). The rapid appreciation of property in TIF districts made it more difficult for municipalities to reverse course because TIF provided them with so much discretionary funding. In this case, the policy of TIF itself became an important cause of the politics surrounding it (Pierson, 1993). Redevelopment and TIF became mutually reinforcing processes that helped shore up the legitimacy and power of the consultants and local officials who promoted them (Rast, 2009b).

Consultants were inundated with TIF-related work, making it difficult to diversify into new areas. Those with finance capacities helped mainstream an instrument that had been on the fringe of the municipal bond market, and the volume of TIF debt grew substantially (Johnson, 1999; Weber, 2010). Some firms purchased the notes themselves (at an amount lower than their face value), others sold them to consortia of local banks, and still others had access to larger institutional investors seeking more standardized assets. These intermediaries profited from the transaction fees and interest rate spreads, (i.e., the difference between what the municipality pays and what it has promised its investors), as well as various underwriting fees. They collected significant fees every time an issuance changed hands, charged for monitoring the project over the instrument’s term, and demanded higher spreads for TIF debt because of the risks involved and the expertise required. Observers have commented on the explosion in soft costs in the TIF budgets over time, all if not most of which went to the legal and consultant sectors (interview with Consultant E and Municipal Official A, personal communication, September 2009).

These heady times came to an end as the real estate markets began to flag and municipalities began to feel the political backlash against eminent domain and corporate welfare, both of which were represented starkly by the municipal use of TIF. By 2008, the property bubble had burst. Falling assessed values and tighter credit for development decreased new starts and reduced the increment available to pay back existing bond and note holders. Kelo v. City of New London (2005), the first eminent domain case to be heard before the Supreme Court since 1984, eventually was decided in the favor of the municipality, but it nonetheless scared entrepreneurial cities and their consultants enough to start considering less confiscatory options.

Conclusion

Scholarship in urban politics and geography tends to focus only on the marquee names, the mayors and the developers that together comprise the public–private partnerships and growth coalitions that reshape the city. In doing so, they ignore the catalysts that bring these two sets of actors into each other’s orbits and shape their mutual interests. In an era where public–private partnerships and contracting out the delivery of urban services are the norm, consultants are strategic agents who shape the ever-permeable organizational boundaries between public and private sectors.

In this article, we investigated how, in the case of Illinois, networked planning and real estate consultants were able to move fluidly between government and the private sector to shore up support for a policy that would benefit both: tax increment financing. Even the most powerful tool can languish without widespread institutionalization, and consultants were responsible for embedding the policies and practices surrounding TIF in this state. This group of professionals both shaped the policy tools available to government and shepherded the dissemination of these tools across states and communities.

Both the tool and the tool’s advocates had their roots in an earlier era of federal assistance to municipalities. TIF built on and expanded the authority given to municipalities to intervene in private real estate markets to stave off decline. Individual consultants had cut their teeth on urban renewal programs that emphasized blight, land write-downs, slum clearance, and generous public assistance for redevelopment schemes that enhanced property values. The 1970s were a critical juncture in the field of economic development when a distinct model of industrial job retention and labor-community activism presented a possible alternative to the more real estate–oriented growth coalitions that formed to channel federal dollars to downtowns. During this transitional period, these coalitions and the consultants that emerged from them held tight to the property development model, appropriating the language and capitalizing on concerns about manufacturing job loss to advocate for a tool that could just as easily be used to subsidize retail, entertainment, hotel, office, and residential uses—in other words, the same kinds of downtown projects that received federal funding during the immediate postwar period. As such, consultants represent a bridge linking what are often considered distinct eras in urban development regimes.

Practitioners can draw on this history of TIF consultants in Illinois for lessons regarding the governance of contemporary economic development. As state and local budgets continue to decline, the future of the economic development profession is once again uncertain. Faced with questions about the value and effectiveness of economic development activities and, at the same time dealing with intensified pressure to bring in tax and job-generating uses, municipalities need to better understand other transitional periods where professionals capitalized on uncertainty for their own benefit. The history of postwar public assistance to private development has remained relatively consistent despite the crises wrought by globalization, deindustrialization, and administrative devolution. Radical shifts have been known to occur—the state of California, for example, passed legislation in 2011 that eliminated all of its redevelopment agencies and transferred bond debt obligations to new entities. But institutional stickiness and professional mobilization makes these events a rarity.

Although the use of consultants is necessary to access expert knowledge, an increasing reliance on them can raise conflicts of interest—particularly when they play both sides of public–private deals. Their time horizons tend to be even shorter than those of elected officials, as they need to show results to get follow-on contracts. This can lead them to favor real estate developments that can be erected quickly over other kinds of projects, such as infrastructure, whose benefits may be less visible and may take longer to materialize. Public sector agencies should ideally develop more of the financial analysis and deal-making expertise in-house (or may consider capping the amount of soft costs that can be covered by TIF), but realistically, consultants are likely to play an increasing role as the number of salaried public employees continues to decrease and demand for economic development grow.

Footnotes

Acknowledgements

The authors wish to thank Ben Teresa for research assistance and Maggie Cowell for her insightful comments on earlier drafts. They are particularly indebted to the practitioners who agreed to be interviewed for this project and to the anonymous reviewers who provided excellent feedback and suggestions.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.