Abstract

Renewable energy plays a pivotal role in achieving the SDGs, particularly SDG 7 and SDG 13, by driving the transition toward a greener, more resilient economy. Thus, the current study explores the drivers of renewable energy consumption in the United States from 1980Q1 to 2022Q4. Utilising the novel multivariate wavelet quantile regression framework, the study explores these dynamics, allowing for a more comprehensive analysis by capturing the impact of the independent variable on the dependent variable while simultaneously accounting for the effects of other covariates. Furthermore, the study employed wavelet quantile co-integration to capture the long-run association across different quantiles and frequency bands. The findings reveal that inflation consistently reduces the use of renewable energy across all quantiles and time scales, with the strongest effects at higher consumption levels in the short run. While technological innovation and financial globalisation exhibit a positive but heterogeneous impact, especially at higher quantiles in the medium to long term, financial development displays mixed effects depending on the distributional characteristics. These findings highlight the importance of tailored policy tools and recommend inflation-indexed subsidies, targeted green finance mechanisms, and regulatory reforms that align international capital flows with clean energy goals. This study not only introduces a robust analytical approach but also contributes actionable insights into designing dynamic, distributionally sensitive renewable energy policies.

Keywords

Introduction

Climate change poses external risks to both natural ecosystems and human well-being. Greenhouse gas emissions reached a record high of more than 36.8 billion metric tons of carbon emission equivalent in 2022. 1 The natural disasters linked to climate change, such as hurricanes, wildfires, and floods, resulted in economic losses of approximately USD 210 billion in 2021 alone, of which only USD 110 billion was covered by insurance, indicating significant financial risks associated with environmental degradation. 2 Simultaneously, although various economic factors significantly shape policy decisions, investment strategies, and regulatory frameworks, economies still grapple with significant macroeconomic uncertainties. For instance, inflation upsurge and financial market volatility complicate achieving sustainability goals. The balance between economic development and environmental sustainability has long been of scholarly interest. As the solution to environmental and economic challenges, pursuing a cleaner environment has become the paramount objective globally. 3 Despite the existing studies having significantly focused on the isolated impact of macroeconomic volatility on environmental sustainability, fewer studies have linked the collective interaction of these variables, such as inflation and financial globalisation, to clean environmental initiatives.4,5 This study fills the gap by investigating the time-varying dynamics and nonlinear joint influence of these variables on the pursuit of a cleaner environment.

As a fundamental macroeconomic indicator, inflation greatly influences economic life, from households to governments. This influence varies with the level of inflation volatility and the country's economic structure. Governments under inflationary pressure prioritise short-term economic stability over a long-term sustainability goal. 6 High inflation often disrupts economic stability, erodes purchasing power, and creates uncertainties, leading to suboptimal investment decisions critical to environmental protection. Most firms incur high operating expenses, thereby adopting cost-cutting measures essential to achieve short-term profitability. According to the International Energy Agency, 7 the cost of green technology and renewable projects increased by 10 to 15% during periods of rising inflation, undermining the economic feasibility of large-scale green projects and making the green transition process more financially challenging.

On the contrary, the moderate level of inflation stimulates environmental investments and accelerates the transition toward a cleaner environment under certain conditions and mechanisms. When an increase in inflation is anticipated, firms hedge against future financial costs by investing in technologies that reduce their dependence on volatile commodities such as oil and gas. 8 For instance, during the COVID-19 pandemic in 2021–2022, global inflation led to a surge in oil prices from 40 USD per barrel to over 100 USD per barrel. 9 This substantial increase in the price of conventional energy has promoted investment in renewable energy. Likewise, spurred by inflation, companies are driven to implement energy efficiency measures to control rising operational costs and energy consumption. The adoption of sustainable manufacturing practices reduces waste and carbon emissions. In 2022, a more than 16% rise in energy efficiency investments was recorded as a preventive measure against financial shocks. 10 Additionally, governments often respond to inflation with fiscal and monetary policies which stimulate green investments. For instance, they increase interest rates in high inflation to curb its pressure and raise borrowing costs, which deters some investment opportunities but creates opportunities for green initiatives through subsidies, tax incentives, and direct government green project spending. 11 However, the extent to which this mechanism is effective depends on other economic factors, such as financial market stability, the availability of green finance, and regulatory support.

Financial globalisation is the means by which international financial markets are linked through cross-border capital flows. It integrates the dual influence of financial institutions on environmental outcomes. For instance, financial globalisation has increased over the past four decades due to international policy liberalisation, technological advancements, and the pursuit of higher returns in markets. Financial globalisation enhances capital mobility, facilitating foreign direct investment in the renewable energy sector. 12 It provides an opportunity to avail low-cost capital for eco-friendly projects and enhance the diffusion of clean technologies across borders. 13 The ‘pollution halo’ hypothesis is consistent with this association channel, suggesting that foreign investments promote the adoption of advanced technologies and environmental management practices to achieve environmental sustainability targets. 14

Financial globalisation is not always favourable, but it has some pitfalls. Such an increase in capital mobility encourages firms in developed economies to relocate their manufacturing activities to developing countries, where environmental regulations are less stringent, thereby exacerbating local environmental degradation. 15 This aligns with the pollution haven hypothesis, which suggests that economic policies with weak regulatory frameworks prioritise industrial growth over environmental safety, thereby enhancing the tendency towards environmental degradation. 16 Moreover, the volatility of speculative capital flows also introduces financial instability risk and complicates the implementation of consistent environmental policies. 17 In addition, in the wake of financial globalisation, companies may adopt greenwashing strategies to exaggerate their sustainability claims and mislead stakeholders in order to attract investments. Likewise, the climate financing gap and debt-driven development undermine sustainability efforts. 18

The study aims to evaluate the influence of inflation and financial globalisation on achieving a cleaner environment in the United States across various time scales and economic conditions. To do this, the study contributes by introducing the novel Multivariate Wavelet Quantile Regression (MWQR) approach. It fills the gap in the existing literature by jointly examining the time-varying quantile-dependent effect of macroeconomic variables on renewable energy and introducing a multivariate wavelet quantile framework. Traditional econometric models used in prior studies have rarely integrated frequency domain analysis with distributional heterogeneity in a multivariate setting, specifically for the US. Those studies often assume a symmetric relationship between economic variables over time, which inadequately reflects the complexities of real-world economic and environmental relationships. 19 The MWQR approach enables the capture of nonlinear and asymmetric time-frequency dynamics for the association between inflation, financial globalisation, and the environment. The wavelet decomposition in the analysis identifies the short-term volatility and long-term trends. Additionally, the MWQR considers the interdependencies between multiple variables, allowing the study to demonstrate a more comprehensive understanding of how inflation, financial globalisation, and other economic indicators interact to shape environmental outcomes. 20 The study also captured the complex feedback mechanism between financial and macroeconomic indicators, which is often overlooked in univariate or bivariate models.

The United States (US) is a highly financialised economy with a substantial global ecological footprint. 21 By focusing on the US as the sample, this study provides context-specific insights into the macroeconomic factors that influence investment decisions. The findings have significant implications for designing strategies that strike a balance between macroeconomic and environmental sustainability. It identifies the time-varying effects and helps to understand whether financial liberalisation policies or inflation-targeted strategies support or hinder the achievement of sustainability goals. Additionally, it guides the timing and intensity of policy interventions. The economic significance of the study lies in addressing the dual challenges of economic and environmental sustainability, providing an understanding of the diverse integrated strategies needed to mitigate the negative environmental spillovers of economic policies. From a research significance perspective, the application of MWQR provides methodological advancements that broaden the scope of economic modelling in environmental research and also open up new avenues for future studies of other complex time- and economic-varying relations.

The rest of the study is structured into the following sections: Section Two covers the theoretical background and a review of related studies, and Section Three provides a comprehensive overview of the methodology, including data, variable summaries, and econometric strategies. Section four presents the results of the analysis and discusses the findings. Section five concludes the study and presents the policy implications based on the examination's outcome.

Literature review

Theoretical foundation

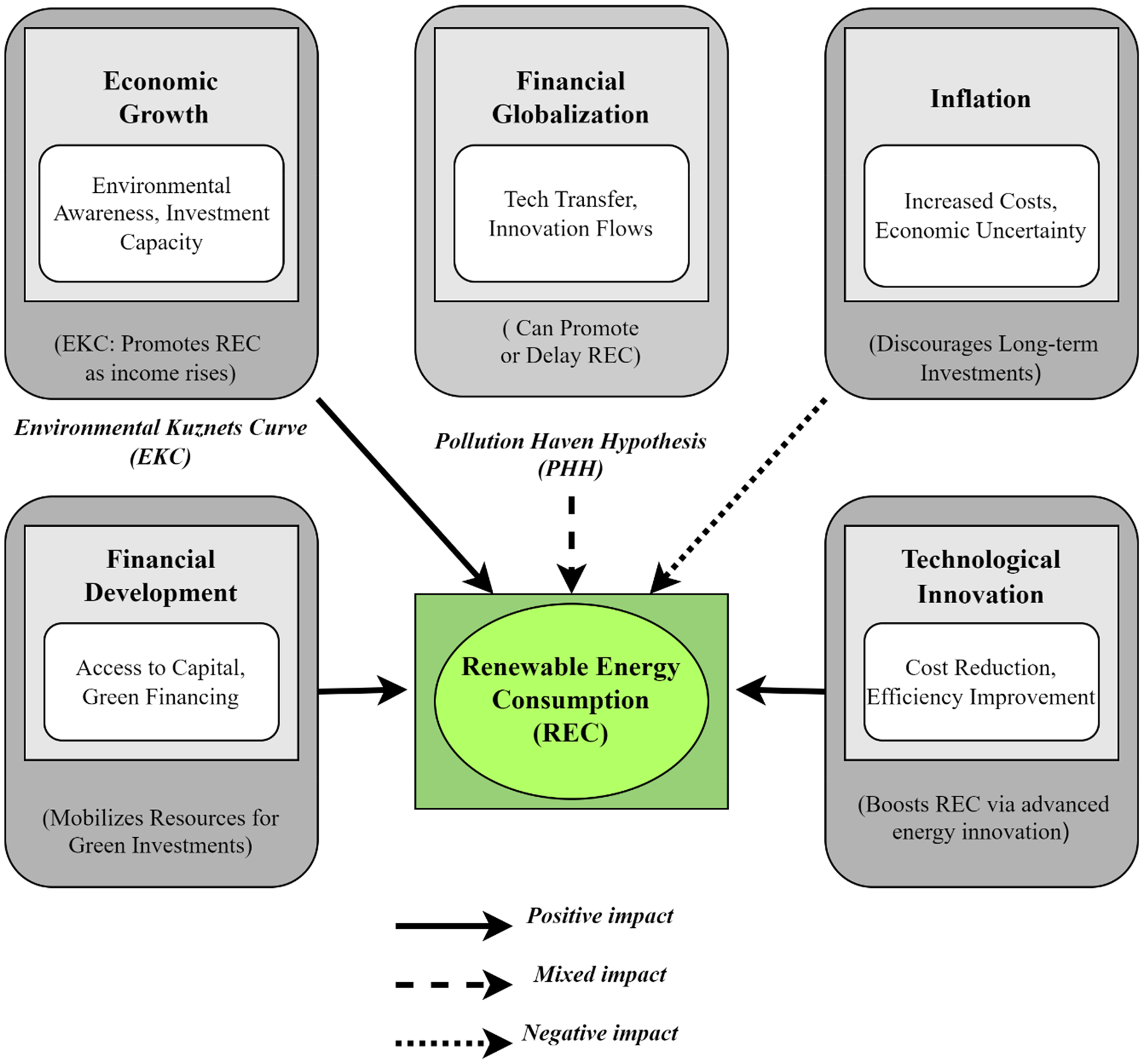

The established financial and economic theories assess the linkage between economic and environmental actors. This study discussed the Pollution Haven Hypothesis (PHH) and Environmental Kuznets Curve (EKC), which provide a foundation for understanding the mechanism of how variables such as economic growth, financial development, financial globalisation, inflation, and technological innovation influence the clean environment pursuit in terms of increased renewable energy consumption in the United States. The EKC was promoted by Grossman and Helpman, 22 who suggested that the relationship between economic growth and environmental degradation has an inverted U-shape in the initial phase of economic growth. The rapid economic growth requires increased energy consumption, resulting in higher pollution levels. However, when economic growth reaches a certain level, excessive income is used to improve environmental quality by creating awareness, improving regulations, and investing in cleaner technologies. 23 The United States is an advanced economy with a high level of economic growth; therefore, it is expected that, due to stringent environmental regulations, policy interventions, and technological advancements, economic growth will promote renewable energy consumption. The country has more available capital for investment in cleaner energy infrastructure. Besides, the government allocates significant subsidies and incentives for the cleaner energy transition based on the higher economic output. Thus, as growth facilitates the embrace of renewables and reduces emissions, the EKC for the US has a downward slope. This theoretical expectation supports the inclusion of economic growth as a key explanatory variable and justifies the exploration of heterogeneous effects across different quantiles and time scales, captured through the MWQR framework (Figure 1).

Theoretical framework.

The PHH by Copeland and Taylor 24 suggests that companies, due to their country's stringent environmental regulations, relocate their production activities to countries with less lenient or weaker environmental controls. The cross-border capital flow in financial globalisation has a dual impact. It facilitates the transfer of cleaner technology; however, it also supports the relocation of factories and increases industrial pollution based on the country's regulatory strength. In the US, the environmental regulations are strict, which indirectly supports the cross-border adjustment mechanism. The US-Mexico-Canada Agreement (USMCA) is an example which replaced the North American Free Trade Agreement (NAFTA) in 2020 to protect the environment. 25 Their primary objective is to ensure that member countries adhere to specific environmental standards and refrain from contributing to cross-border manufacturing or trade, thereby preventing an expansion of their ecological footprint. 26 Although the US has a strong environmental policy, the PHH still informs the dual role of financial globalisation in attracting clean investment flows or exacerbating fossil fuel-intensive energy consumption due to market liberalisation.

These two theories jointly motivate the empirical strategy to account for nonlinear dynamics and distributional effects, expecting that due to the combined effect of the variables, financial globalisation and technology innovation on renewable energy may vary depending upon economic condition and regulatory capacity, which justifies the multivariate and quantile-based approach adopted by the current study. These variables may impact the enhancement or integration of renewable energy by facilitating cross-border technology transfer and capital flows. This financial globalisation accelerates the diffusion of innovations in clean energy. Inflation increases the cost of capital, adversely impacts investments in clean energy projects, and discourages the consumption of renewable energy. According to Akan, 27 investors are less inclined to invest in cost-intensive renewable energy projects, thereby causing the slow growth of the energy sector. Bilal et al. 5 discovered that inflation makes green technology more expensive relative to traditional energy sources, dampening the adoption of renewable energy. The collective effect of inflation mitigates the positive impact of financial globalisation, financial development, and technological innovation. High inflation erodes purchasing power and increases the cost of capital; therefore, policies should aim to stabilise inflation to support clean environmental initiatives.

Review of related studies

Inflation and clean environmental initiatives

The nexus between inflation and renewable energy consumption has been studied in various contexts. Some studies have found inflation to be a potential barrier to clean energy initiatives, while others have focused on how inflation supports the adoption and effectiveness of renewable energy. For instance, high inflation has a determining effect on developing renewable energy channels by accelerating the financing costs related to solar installations, wind farms, and other clean energy projects. High inflation acts as a barrier, making it more challenging for countries to shift toward green energy sources. Akan 28 deciphered the interaction between inflation and renewable energy. From 1990 to 2020, the study collected data from various countries and applied structural equation modelling. The study found that with the rise of inflation, the costs associated with renewable energy projects are exacerbated, increasing the financial burden and slowing the progress of environmental initiatives. Bilal et al. 5 interrogated the relationship between inflation dynamics and alternative energy sources. For the sample of emerging economies from 1995 to 2020, the study elucidated that inflation reduced consumer purchasing power, discouraging investment initiatives in renewable energy. It decreases the feasibility of renewable energy projects, thus significantly weakening the impact of clean environmental initiatives.

High inflation is often associated with economic uncertainties. These uncertainties impose additional risk for long-term investment initiatives due to the unpredictability of profit or returns. Lu et al. 29 examined the linkage between inflation, renewable energy, and trade in the MENA countries from 1990 to 2019. The study applied the augmented production function model, and the outcomes from the panel co-integration tests revealed that inflation-driven economic instability increased the cost and risk of uncertainties affecting environmental improvement. This unstable situation shifts the investors’ focus towards short-term profits through investments in safer and short-term assets, indirectly hindering emission mitigation. Huntington and Liddle 30 uncovered how inflation driven by energy price volatility can slow economic growth and limit the growth of renewable energy adoption in 18 OECD countries. The study spanned from 2016 to 2019. To control for cross-country correlations, the study employed mean-group estimates. The findings showed that financial markets behave differently during periods of high inflation. Due to the perceived instability, they tend to favour conventional investments over riskier and lower-return renewable energy ventures.

Some studies have highlighted the bidirectional feedback between inflation and renewable energy consumption, where a rise in inflation adversely impacts renewable energy initiatives and creates conditions that reinforce energy-related inflation, leading to cyclical challenges. For instance, Liu et al. 4 examined the association between oil price volatility, inflation, and renewable energy consumption from 1990 to 2019 for the top oil-importing and exporting countries. The study employed various diverse panel data assessors. The study's findings demonstrate that inflationary pressure causes a delay in the adoption of renewable energy and perpetuates dependence on fossil fuels, contributing to energy inflation driven by oil price volatility. Kousar et al. 31 examined the feedback effects between inflation and clean energy initiatives of five South Asian economies. The DOLS and FMOLS methods are used as empirical strategies. The study's outcomes suggested that brown growth accelerates in these countries due to the high inflation. The adoption of renewable energy could not be achieved at its full potential when the monetary policies did not take steps to stabilise inflation and break the cycle.

From the existing literature, few studies expand their focus beyond the association between renewable energy and inflation. Instead, they consider how inflation affects the broader environmental policies, including clean technology investments, emission reduction initiatives, and energy efficiency projects. Boufateh and Saadaoui 32 discovered that high inflation restricts access to funding for green technologies; therefore, controlling inflation is crucial for obtaining a supportive financial system for environmental sustainability. Ahmad and Satrovic 32 elucidated the moderating role of green monetary policies for the nexus of inflation and renewable energy consumption in G7 countries from 1995 to 2019. The outcomes of the Method of Moments Quantile Regression (MMQR) indicate that monetary policy can mitigate the adverse effects of inflation on clean environmental initiatives by issuing green bonds and providing subsidies.

Similarly, Sadiq et al. 35 emphasised the importance of proactive government policies in mitigating the negative impact of inflation on renewable energy investments. The data from 1981 to 2019 were used in China. The outcomes of the autoregressive distributed lag (ARDL) model suggest that policies such as tax incentives and subsidies for clean technology adoption and green projects provide financial relief during periods of high inflation. Hence, well-designed monetary and fiscal policies are crucial for achieving stable inflation and meeting environmental sustainability targets.

Financial globalisation and clean environmental initiatives

The impact of financial globalisation on environmental sustainability is complex and multifaceted. Some studies suggest that financial globalisation facilitates renewable energy consumption, while others highlight its detrimental effects. For instance, Miao et al. 33 assessed the impact of financial globalisation on renewable energy consumption in newly industrialised countries (NICs) using annual data from 1990 to 2018. The study applied the MMQR method and found that integrating global financial markets increases global capital accessibility and encourages foreign direct investment in scaling up clean, renewable energy projects. Likewise, Ahmad et al. 34 interrogated the impact of financial globalisation on the environmental quality of G-11 economies. The study used the cross-sectional autoregressive distributed lags (CS-ARDL) from 1995 to 2022. The study's findings revealed that G-11 countries leverage financial globalisation to diversify their energy mix, which helps increase renewable energy consumption and reduce dependency on fossil fuels.

Anton and Afloarei Nucu 35 investigated the interplay between financial globalisation and renewable energy adoption. The study analysed 28 European Union (EU) countries from 1990 to 2015 to assess the impact of financial globalisation. The findings suggested that financial globalisation reduces financial barriers and expands capital accessibility. The well-developed financial system strategically allocates resources for green energy initiatives, enabling the achievement of environmental sustainability. Likewise, Sharif et al. 36 applied the MMQR to the data of top ecologically impacted countries to examine the nexus between renewable energy, green technology, and financial globalisation. The study elucidates that financial globalisation drives the diffusion of green technologies, leading to the reduction of GHGs and the adoption of renewable energy. The cross-border investment integrations are critical to establishing the financial pathway for the green transition.

Conversely, some studies have highlighted the impedimental role of financial development in relation to renewable energy consumption. For instance, Kirikkaleli et al. 37 explored the impact of financial development in Chile using the ARDL, FMOLS, and DOLS approaches. This study demonstrates that global financial integration and development facilitate capital access and amplify investment in fossil fuel projects due to the potentially high returns that attract investors. The diversion of financial resources impedes the pursuit of a clean environment. Similarly, Yang et al. 38 scrutinised the linkage between financial globalisation and energy utilisation in the Gulf Cooperation Council (GCC) countries from 1980 to 2019. The Panel data estimates of the study revealed that financial globalisation opens the door for conventional energy projects, such as oil and gas, in these countries due to their abundant natural resources and high economic dependency. Excessive availability of fossil fuels constrains investment in environmental sustainability initiatives..

Few studies in the existing literature have diagnosed the mixed effects of financial globalisation on environmental sustainability. Ahmad and Wu 39 evaluated the collective impact of green productivity and globalisation on the ecological sustainability of OECD countries. The study's outcomes highlight that financial globalisation provides capital for renewable energy projects. Simultaneously, it creates financial instability and increases the risk of market volatility, which impacts long-term investment decisions. Ramzan et al. 40 determined that financial globalisation has a complex impact on the green transition. According to the Bootstrap Rolling-Window estimates, it has a dual impact on different periods of subsamples in the United Kingdom. Another recent study by Zaidi et al. 41 suggested that financial globalisation is a double-edged sword for the green initiative in the sixteen emerging economies. It enhances energy efficiency and intensifies energy in high-emission industries.

Research gap

Although the existing literature has examined the nexus between macroeconomic factors and environmental sustainability, a significant gap remains in the context of the United States. The US has substantial importance in economic and ecological research due to its stable and steady economic growth, integration with global financial markets, and extensive energy consumption. With the unique economic and regulatory framework, the joint influence of macroeconomic factors on renewable energy is crucial to determine. Most existing studies have focused on the isolated effects of inflation and financial globalisation on environmental sustainability, neglecting the potential interaction between these variables. For instance, the financial globalisation's impact on renewable energy investments may be affected due to high inflation. Likewise, financial globalisation can reduce the adverse impact of inflation on green initiatives.

Additionally, most related studies assume a constant association between the variables over time and employ traditional econometric approaches. The gap raises the question of how the association of variables varies across different periods. The sudden spike due to the short-term macroeconomic shock may have a different impact than the long-run or medium-term association between inflation and clean environmental innovation. Therefore, there is a need to employ an appropriate statistical approach that assesses the time-varying nexus between the study variables. There is also a need to diagnose the nonlinear association between variables over the quantiles. This study fills the gap by applying the more sophisticated approach of Multivariate Wavelet Quantile Regression (MWQR), which allows for a time-varying analysis across different quantiles of renewable energy consumption levels. Through this approach, the study can provide more comprehensive insights and offer a detailed understanding of the changes in the US's short- and long-term structure.

Data and methods

Data

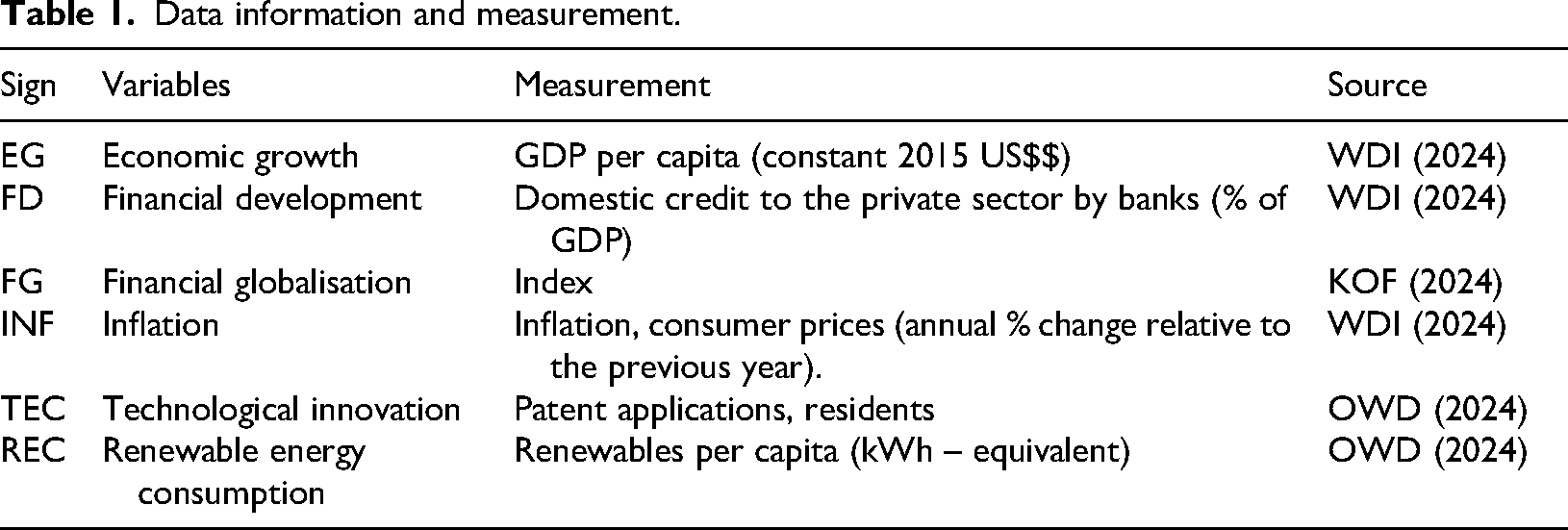

Table 1 provides an overview of the variables, their measurements, and data sources used in the analysis. To measure consistency in scale, reduce heteroscedasticity, and stabilise variance across variables, the natural logarithm transformation has been applied to all variables in the dataset. The independent variables are economic growth (lnEG), Inflation (lnINF), financial globalisation (lnFG), financial development (lnFD), technological innovation (lnTEC), and renewable energy consumption (lnREC). These selected variables reflect established macroeconomic determinants of renewable energy. The dataset spans from 1980 to 2023. However, due to limitations in data availability, transformations were necessary. To address this, we employed the quadratic match sum method to convert annual data into quarterly intervals, which aligns the temporal resolution with the wavelet decomposition requirements and enhances model consistency and granularity.

Data information and measurement.

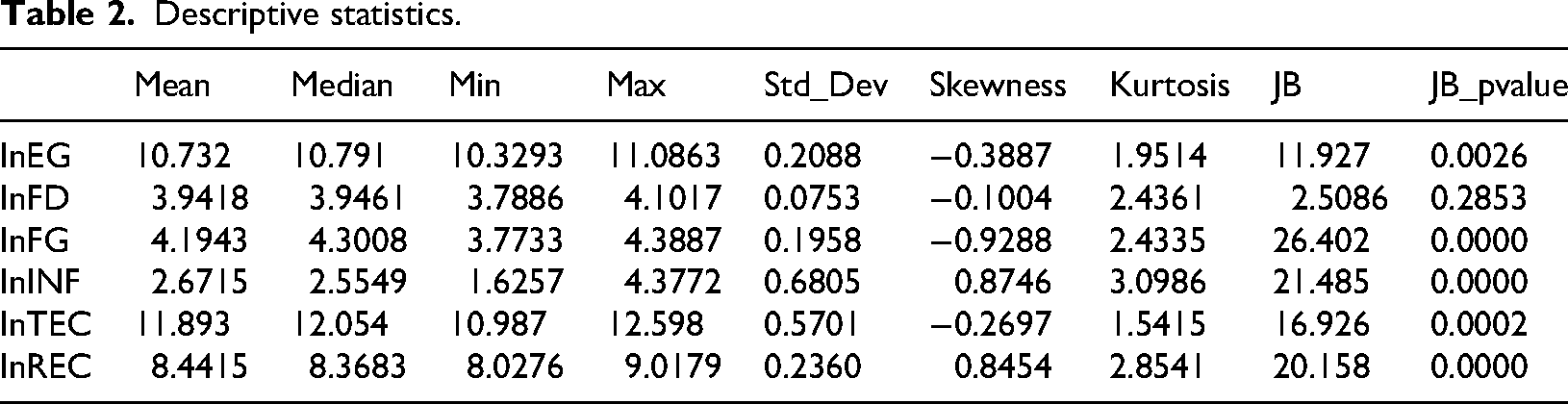

Table 2 presents the descriptive statistics of the variables used in the analysis. The mean and median values indicate central tendencies, while the Minimum and maximum values show the range of each variable. The Standard Deviation (Std_Dev) provides insights into variability, with higher values indicating greater dispersion from the mean. The relatively low standard deviation for most variables suggests moderate variability over the sample period, with lnINF showing the highest dispersion, reflecting notable inflation fluctuations in the US. Skewness reveals the asymmetry of the distribution, where negative values (lnEG and lnFG) suggest a left-skewed distribution, and positive values (lnINF and lnREC) indicate a right-skewed distribution. Kurtosis measures the ‘tailedness’ of the distribution, where values close to 3 are considered normal, while deviations suggest more or fewer outliers, except for lnINF and lnREC, which exhibited heavier tails. The JB test evaluates the normality of each variable's distribution, and its corresponding p-value (JB_pvalue) indicates the statistical significance. Notably, lnEG, lnFG, lnINF, lnTEC, and lnREC reject normality at the 1% significance level, while lnFD does not, suggesting it follows a normal distribution. The non-normality of most variables, reinforces the need for a quantile-based and nonlinear modeling approach.

Descriptive statistics.

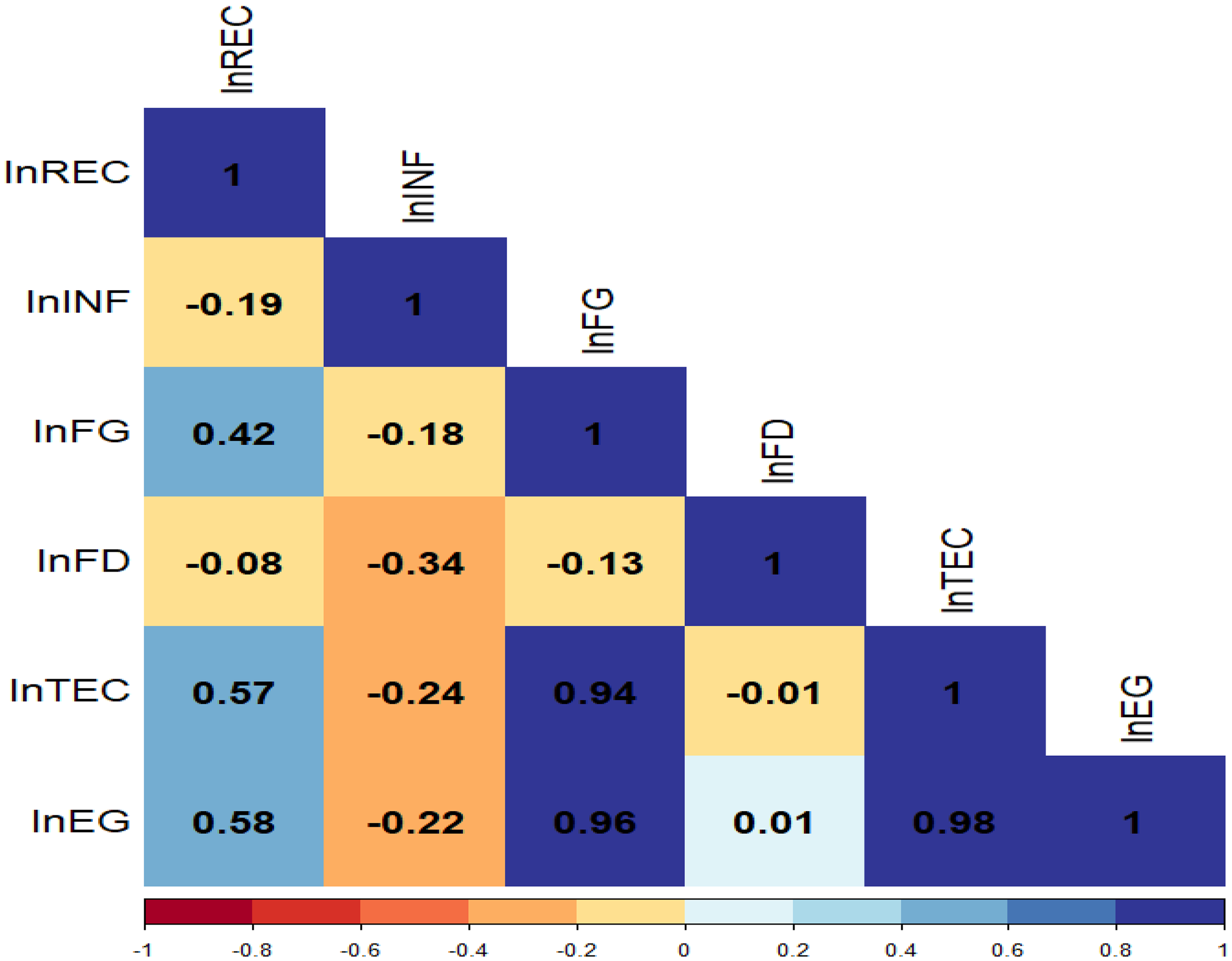

The correlation matrix (Figure 2) reveals that lnREC exhibits moderate positive correlations with lnTEC (0.57) and lnEG (0.58), suggesting that lnTEC and lnEG are key drivers of renewable energy consumption. lnREC also has a weaker positive relationship with lnFG (0.42), suggesting a modest connection between lnFG and lnREC. On the other hand, lnREC shows slight negative correlations with lnINF (−0.19) and lnFD (−0.08), implying that lnINF and lnFD have little to no impact on lnREC in this dataset. The moderate correlation between inflation and renewable energy supports exploring its time-varying inhibitory effects. Similarly, the positive but asymmetric correlation with globalisation and technological innovation suggests potential nonlinearities, justifying the use of MWQR.

Correlation plot.

Proposed methodology

In this study, we introduced the multivariate wavelet quantile regression (MWQR) to explain drivers of renewable energy consumption. The previous empirical analyses rely on linear or mean-based approaches, which assume constant relationships over time and fail to capture nonlinearities. Some standard nonlinear models (NARDL, QQR) are also unable to estimate the time-frequency-specific nature of macroeconomic influences on renewable energy consumption. Besides, the existing wavelet approaches are specifically univariate or bivariate, and therefore, overlook the interdependencies between multiple drivers. In contrast, MWQR allows for the joint modelling of several covariates across both quantiles and time scales, offering a more detailed and policy-relevant insights into how inflation, financial globalisation, technological innovation and financial development shape renewable energy consumption. This approach is not proposed as a new econometric estimator, but rather as a novel and rigorous application of established techniques to fill a methodological gap in the macroeconomics literature. The quantile regression (QR) is defined as follows:

where the conditional quantile of the dependent variable

Previous investigations have shown that the interrelationships between variables can shift across dissimilar time scales. Nevertheless, the QR method does not account for this possibility. To address this limitation, Adebayo and Oktay

13

introduced the Wavelet Quantile Regression (WQR) as a solution. The WQR enables the examination of how the X influences the conditional quantiles of Y across multiple time scales. The Maximal Overlapping Discrete Wavelet Transform (MODWT) suggested by Percival and Walden

43

is used for decomposing the independent variable

where,

While Wavelet Quantile Regression (WQR) offers a robust framework for examining the impact of the independent variable X on the various quantiles of the dependent variable Y across different time scales, it fails to account for the influence of other covariates. This limitation is significant because it restricts the ability to comprehensively understand how various factors interact and affect the response variable across different quantiles. To address this, we extend WQR to Multivariate Wavelet Quantile Regression (MWQR) by adding a vector of control variables Z. At the wavelet scale

where,

Findings and discussions

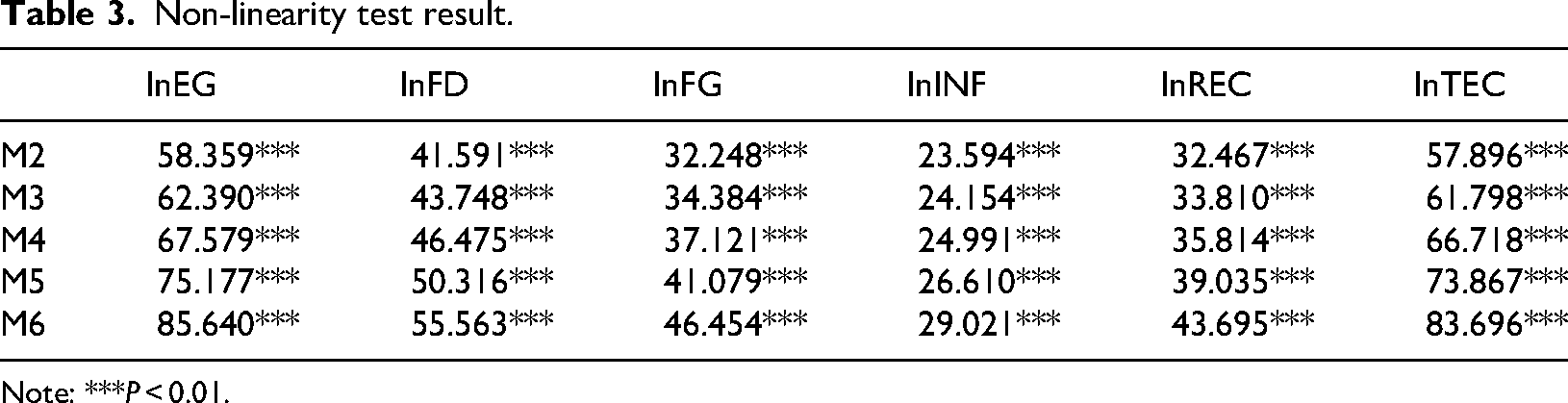

Non-linearity test results

Table 3 presents the results of the non-linearity test for the studied variables. lnEG and lnTEC exhibit the highest levels of non-linearity across all models, peaking in M6 with scores of 85.640 and 83.696, respectively. This suggests that these variables exhibit stronger nonlinear characteristics compared to others, such as lnINF, which shows the lowest non-linearity scores in all models. Therefore, it is crucial to use nonlinear techniques in this investigation.

Non-linearity test result.

Note: ***P < 0.01.

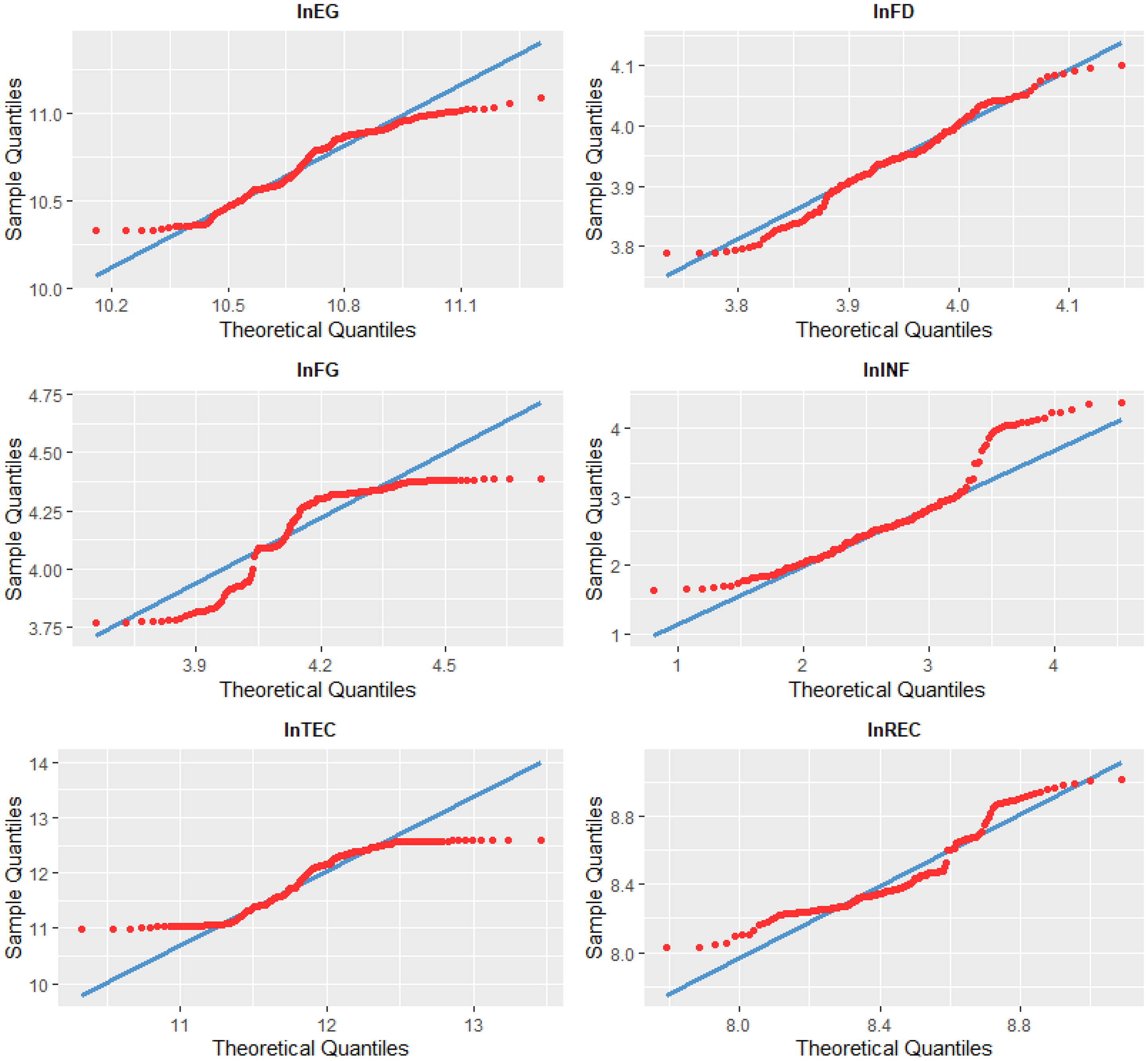

Furthermore, the study used a QQ plot to explore the nonlinear attributes of the variables, with the results shown in Figure 3. The results show that none of the variables align with a normal distribution. These results align with the findings of the BDS test, thereby affirming the non-linearity of the variables.

QQ plot results.

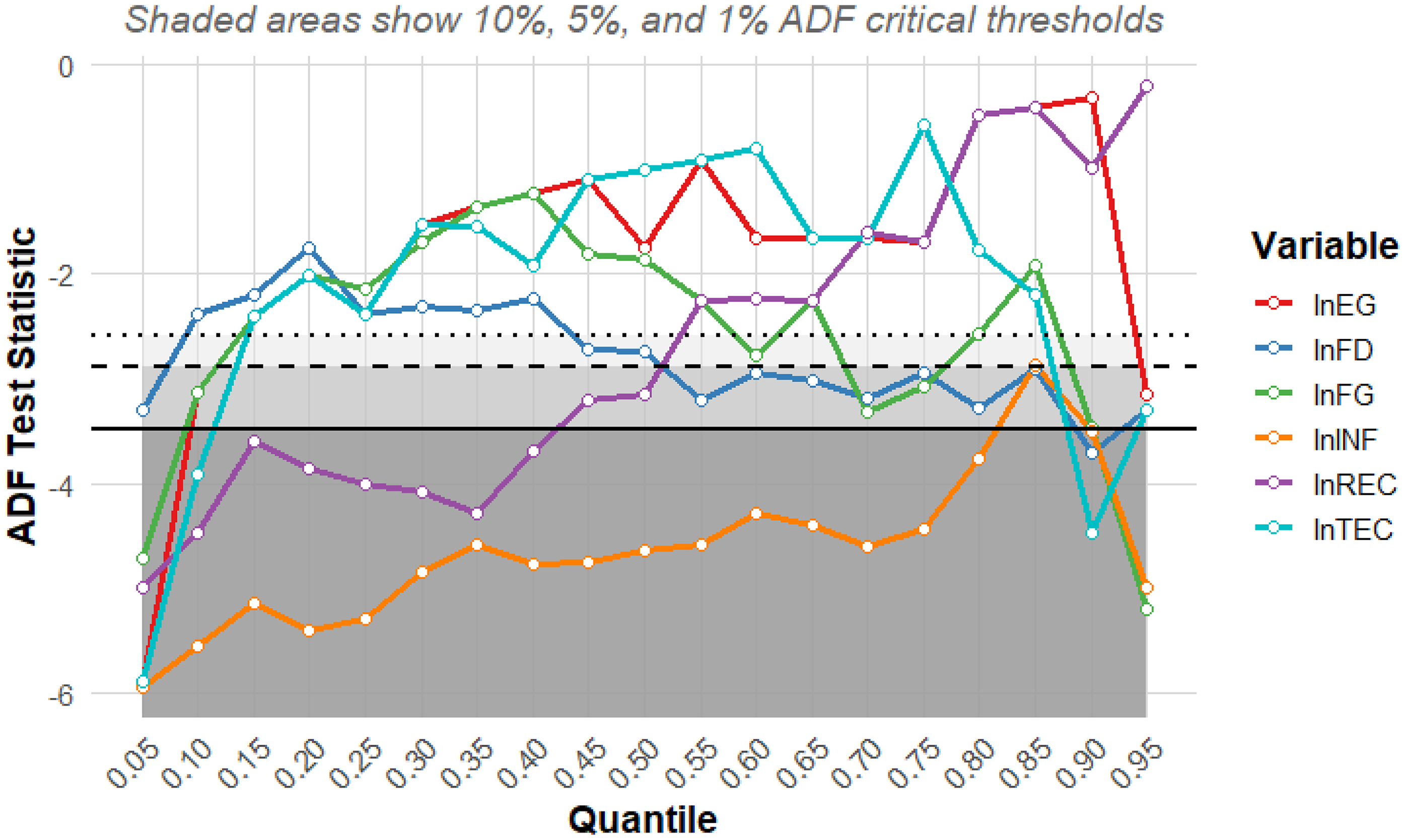

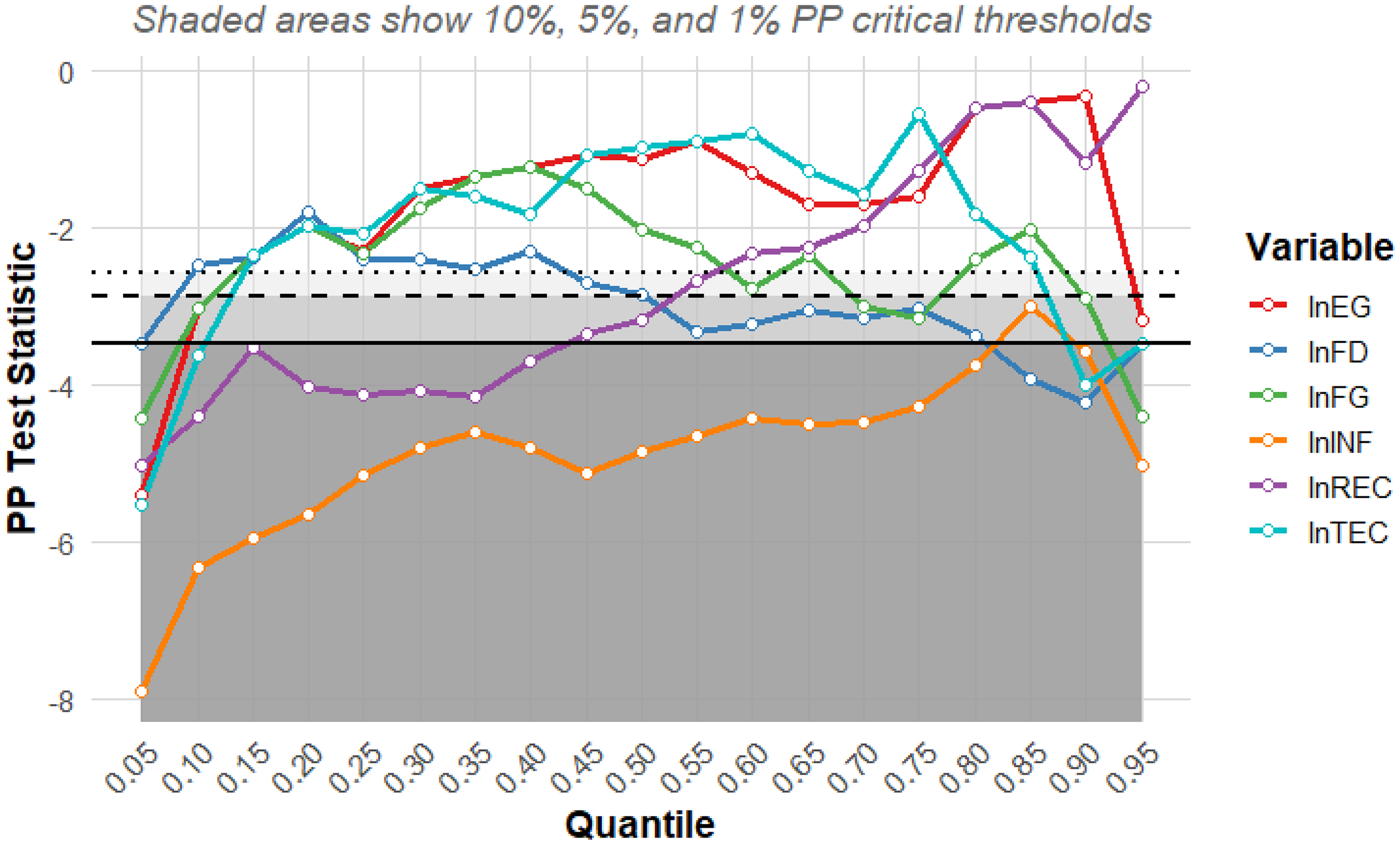

Quantile unit root test results

The Quantile Augmented Dickey-Fuller (QADF) test results are presented in Figure 4. The test statistics vary across quantiles (from 0.1 to 0.9), providing insights into the stationarity of the series at different points in its distribution. The QADF results indicate that most variables exhibit stationarity across all quantiles. Additionally, the Quantile Phillips-Perron (QPP) test (Figure 5) was applied to further assess the stationarity of the series, and its findings are consistent with those of the QADF test. These results confirm that the series are stationary across various quantiles.

QADF test result.

QPP test result.

The QADF and QPP tests are essential in establishing the robustness of the time series properties within the quantile framework given the nonlinear and asymmetric behaviour expected in macro financial variables. These quantile specific tests in Figures 4 and 5 provide a more detailed view than the conventional unit root tests, revealing whether variables like inflation, globalisation and technological innovation exhibited persistence or mean reversion in different parts of the distribution. This is crucial to understanding whether macroeconomic influences operate differently in regimes with low versus high renewable energy consumption. The pattern observed in these figures not only validates the appropriateness of quantile-based modelling but also informs expectations about the long-run relationships explored in subsequent co-integration and regression analysis. For instance, inflation falls below the mean value across quantiles, which indicates its greater volatility and persistence in the lower parts of its distribution, and might be due to its higher sensitivity to financial constraints.

Quantile co-integration

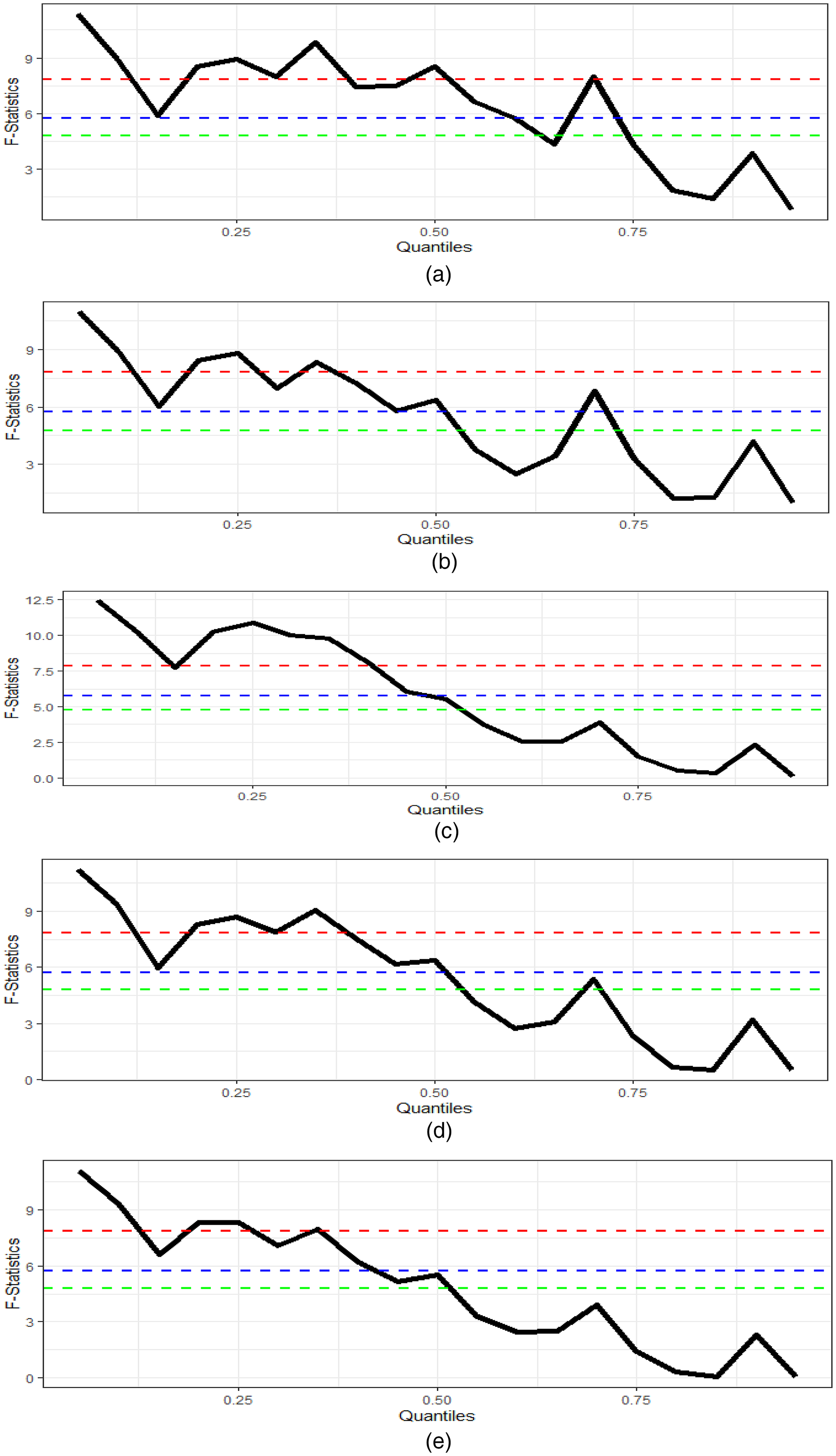

In the next phase, we examined the co-integration between renewable energy consumption and its drivers. In doing so, we used the quantile co-integration, which is superior to the bounds test because it captures the heterogeneous relationship between variables across different quantiles, providing a more comprehensive understanding of the impact of variables at different points in their distribution rather than assuming a uniform relationship throughout, as the bounds test does. Furthermore, quantile co-integration enables more robust analysis in the presence of outliers and non-linearities, which are often prevalent in economic and energy data, providing more accurate and meaningful insights compared to traditional bounds testing methods.

Figure 6 presents the results of the quantile co-integration (QC) analysis. Figure 6(a) illustrates the co-integration relationship between REC and TEC, with evidence of co-integration observed across the lower and middle quantiles. Furthermore, Figure 6(b) shows the co-integration between REC and EG, indicating evidence specifically in the lower and middle quantiles. Similarly, Figure 6(c) highlights the co-integration between REC and INF, with co-integration evident in the lower quantiles. Figure 6(d) also displays the co-integration between REC and FG, showing evidence in the lower and middle quantiles. Finally, Figure 6(e) confirms the co-integration between REC and FD, indicating that both variables move in tandem over time.

Quantile co-integration results. (a) QC between lnREC and lnTEC, (b) QC between lnREC and lnEG, (c) QC between lnREC and lnINF, (d) QC between lnREC and lnFG, (e) QC between lnREC and lnFD.

Multivariate wavelet quantile regression results

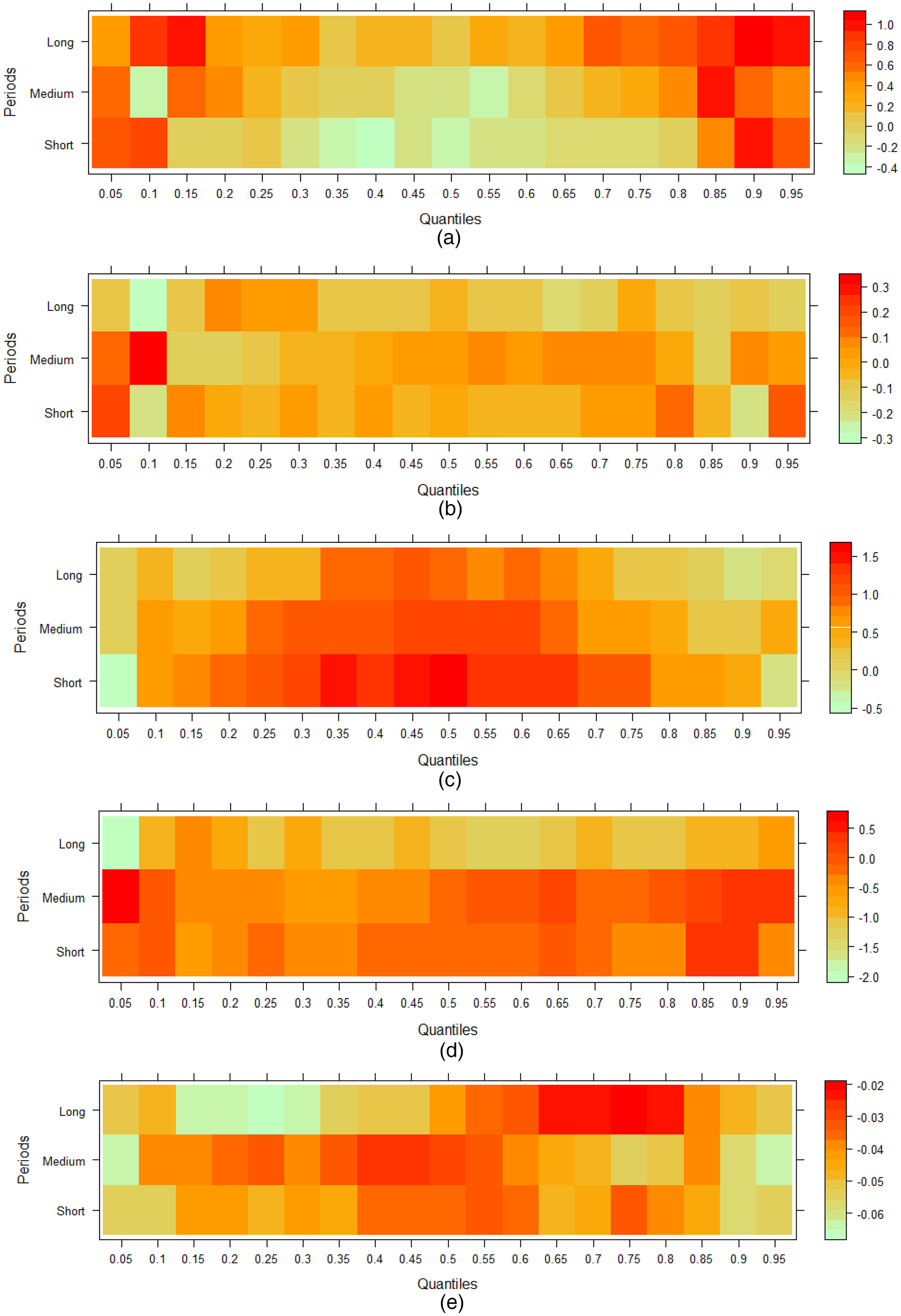

Figure 7(a) illustrates that the influence of EG on REC, while controlling for TEC, INF, FD, and FG in the United States, varies across different quantiles and time horizons. In the short term, the findings suggest a mixed relationship, where an increase in economic growth may lead to a reduction in renewable energy consumption. This could be due to the high dependence on non-renewable energy sources to boost production and meet growing energy demands, as well as the time lag required for renewable energy technologies to expand to scale. 44 Furthermore, financial development –and inflation can indirectly affect REC by altering the cost structures and investments in clean energy. At lower quantiles, the negative impact of economic growth is stronger, potentially indicating a reliance on traditional energy sources at lower growth levels, consistent with the findings by Ahmad et al.. 34 In the medium and long-term, the results show a relatively positive effect of EG on REC, particularly at higher quantiles. This positive relationship can be attributed to increased income levels, which facilitate investments in renewable technologies and infrastructure, as well as financial globalisation promoting capital inflows for sustainable projects. 45 However, studies such as Sharif et al. 36 highlighted that this positive impact is conditional on effective policy measures and a stable macroeconomic environment that encourages renewable energy adoption. In particular, technological innovations are crucial for enhancing the efficiency of renewable energy and making it competitive with fossil fuels. In contrast, some studies, such as Batool et al., 46 argued that without stringent policies, financial development may divert resources to carbon-intensive industries, reducing the relative share of renewables even in the long term.

Multivariate wavelet quantile regression results. (a) Impact of lnEG on lnREC with lnTEC, lnFD, lnINF and lnFG as control variables, (b) impact of lnTEC on lnREC with lnEG, lnFD, lnINF and lnFG as control variables, (c) impact of lnFG on lnREC with lnEG, lnFD, lnINF and lnTEC as control variables, (d) impact of lnFD on lnREC with lnEG, lnFG, lnINF and lnTEC as control variables, (e) impact of lnINF on lnREC with lnEG, lnFG, lnFD and lnTEC as control variables.

Figure 7(b) shows the impact of TEC on REC in the United States while controlling for EG, INF, FD, and FG. In the short term, the results suggest that technological innovations have a mixed effect on REC, as seen by negative correlations at lower quantiles. This outcome may reflect the initial costs associated with the adoption of new technologies, as well as the lag time required for these technologies to achieve efficiency gains that significantly contribute to renewable energy use. 47 Studies like that of Uche et al. 48 supported the notion that, initially, technological advancements might not immediately translate into higher renewable energy consumption due to existing dependencies on traditional energy sources and the challenges of transitioning. In the medium and long-term, technological innovations exhibit a positive relationship with REC, particularly at higher quantiles, suggesting that innovation plays a critical role in facilitating the shift towards sustainable energy. This positive interrelationship is strengthened by financial globalisation, which allows the diffusion of technology and enables countries to adopt state-of-the-art renewable solutions. Studies such as Usman and Hammar 49 highlighted that advancements in technology, coupled with supportive economic conditions, are key to overcoming the barriers to renewable energy adoption in the long run. On the other hand, some scholars argue that technological innovations alone may not suffice if they are not complemented by effective policy frameworks that promote renewable energy.

Figure 7(c) illustrates the impact of FG on REC in the United States, while controlling for EG, INF, FD, and TEC, which reveals variability across different quantiles and periods. In the short term, the findings indicate a mixed relationship, with some negative effects, particularly at lower quantiles. This outcome might be attributed to the initial flow of international capital being diverted to other sectors, especially traditional energy or non-renewable investments, as these often offer quicker returns compared to renewable projects. 36 The complexity of global capital flows, along with regulatory and risk factors, contributes to the varied impact observed in the short term, which aligns with the findings of Anton and Afloarei Nucu. 35 In the medium and long term, financial globalisation has a consistently positive impact on renewable energy consumption, particularly at higher quantiles. This suggests that the integration of the United States into the global financial system facilitates greater access to international funds and investments, which eventually supports the development of renewable energy infrastructure and the deployment of advanced technologies. Studies such as those by Miao et al. 33 argued that capital mobility, driven by financial globalisation, plays a significant role in fostering renewable energy growth, especially when complemented by domestic policies that promote green finance and reduce barriers to renewable investments. However, some researchers like Achuo et al. 50 cautioned that the positive impact of financial globalisation may be contingent on the stability of financial systems and proactive policies that channel these funds toward environmentally friendly projects, emphasising the importance of a supportive policy framework to realise the potential benefits for renewable energy. The temporal divergence suggests that the benefits of financial globalisation materialised gradually, reinforcing the need for complementary policies that can stabilise macroeconomic conditions in the short run and leverage international capital for long-term goals of sustainability.

Figure 7(d) shows how FD impacts REC in the United States while controlling for EG, inflation, FG, and TI across various quantiles and periods. In the short term, financial development appears to have a mixed impact, particularly at lower quantiles where the effect tends to be negative. This suggests that financial resources may initially flow towards well-established sectors, such as fossil fuel industries, which provide more immediate returns compared to the renewable energy sector, as noted by Yang et al. 38 This phenomenon can also be influenced by a lack of incentives or the absence of strong regulatory frameworks to prioritise renewable investments during the early stages of financial development, as noted by Kirikkaleli et al. 37 In the medium and long-term, however, financial development exhibits a positive association with REC, particularly at higher quantiles. As the financial system matures, access to credit and financing for renewable energy projects becomes more readily available, reducing the barriers to entry for new renewable energy investments. This is consistent with the findings of Batool et al., 46 who argue that a well-developed financial system can lower the cost of capital for renewable projects and attract investments in sustainable energy technologies. On the other hand, some scholars, such as Eren et al.,51 contended that the impact of financial development may remain limited if there are insufficient green financial products or if policies do not adequately direct funds toward green energy projects.

Figure 7(e) displays the impact of INF on REC in the United States while controlling for economic growth, financial development, financial globalisation, and technological innovations. In the short term, inflation tends to have a negative impact on renewable energy consumption across most quantiles, with stronger effects observed at higher quantiles. Higher inflation can increase the cost of borrowing and decrease the purchasing power of consumers and investors, making it more challenging for renewable energy projects to secure the necessary funding for implementation and development. The increased cost of capital due to inflation may deter investments in renewable energy projects, particularly in an economic environment where non-renewable energy sources are often perceived as more financially stable in the short term. The negative impact of inflation on renewable energy consumption persists in the medium and long-term but shows some variability across different quantiles. At lower quantiles, the effect is less pronounced, potentially reflecting adaptive measures taken by the market and investors to manage inflationary pressures and maintain investments in the renewable energy sector. 29 Inflationary pressures tend to hinder the adoption of renewable energy by increasing the costs of technologies and raw materials required for renewable infrastructure development. Studies like Huntington and Liddle 30 suggested that without targeted policies that protect renewable energy investments from inflationary risks, such as subsidies or inflation-indexed green bonds, the transition towards renewable energy can be significantly delayed. Conversely, another research by Bilal et al. 5 argued that proactive government policies and inflation-targeting frameworks can mitigate these negative effects, indicating the importance of policy interventions in overcoming the challenges posed by inflation. The temporal divergence suggests that while inflation poses immediate and persistent challenges to renewable energy adoption, the benefits of financial globalisation materialised gradually, reinforcing the need for complementary policies that can stabilised macroeconomic conditions in the short run and leverage international capital for long-term goals of sustainability.

Conclusion and policy pathways

Conclusion

In this pioneering study, we examined the effect of inflation, financial development, financial globalisation, and technological innovation on renewable energy consumption in the United States. The study employed data from 1980Q1 to 2022Q4 to evaluate this nexus. To address the nonlinear nature of the variables, this study introduced multivariate wavelet quantile regression (MWQR), an advancement over wavelet quantile regression (WQR). MWQR allows for a more comprehensive analysis by capturing the impact of the independent variable on the dependent variable while simultaneously accounting for the effects of other covariates. The results of the MWQR show that inflation reduces renewable energy consumption across all quantiles and periods. Furthermore, technological innovations, economic growth, financial globalisation, and financial development impact renewable energy consumption positively or negatively across various quantiles and periods.

Policy recommendations

To enhance renewable energy consumption in the United States, policymakers need to adopt targeted strategies that consider the varying quantiles and time horizons.

First, the findings show that economic growth adversely impacts renewable energy consumption at lower quantiles in the short term, reflecting that during the low lnREN consumption, economic growth supports conventional energy; therefore, short-term policies should prioritise incentives for renewable energy projects to mitigate the adverse effects of economic growth on clean energy consumption. This could include tax incentives for renewable investments, subsidies, and loan guarantees for renewable projects, especially targeting lower-income and high-risk sectors. By doing so, financial resources can be directed towards renewable energy, reducing the dependence on fossil fuel sources that have been observed in lower quantiles during short-term periods. Second, the mixed effect of technology innovation in the short term, with the substantial transformation to a positive driver in the medium to long term, suggests that policymakers should prioritise fostering technological innovations that enhance renewable energy consumption, especially to support medium-term growth. This can be achieved by supporting research and development initiatives and providing grants for pilot projects that integrate new technologies into renewable energy infrastructure. Public-private partnerships could play a decisive role in addressing the initial adoption costs and overcoming barriers to the deployment of renewable technologies. Effective collaboration with global partners can also facilitate the diffusion of advanced technologies, which have been shown to enhance the adoption of renewable energy, particularly in the medium and long term.

Third, as financial globalisation had a delayed but increasingly positive effect, particularly at higher quantities, it offers an opportunity for increased investments in renewable energy, particularly in the long term, as evidenced by the consistently positive relationship at higher quantiles. Policymakers should capitalise on this opportunity by promoting international collaborations and reducing regulatory barriers to foreign investments in the green energy sector. Encouraging the development of green finance mechanisms can also facilitate access to international capital, ensuring that financial globalisation directly supports renewable energy growth while minimising potential risks, such as the diversion of funds to non-renewable industries. Fourth, financial development shows an adverse short-term effect at lower quantiles, due to capital flow biases toward fossil fuel-intensive sectors; therefore, lnFD should also be leveraged to support renewable energy consumption. In the short term, it is essential to direct financial resources toward renewable projects by offering targeted incentives, such as lower interest rates on loans for clean energy projects, and establishing green banking frameworks. In the medium and long term, improving access to finance for renewable energy projects and developing financial products specifically tailored to green investments can help build a more resilient renewable energy market. Establishing green credit guidelines and mandating financial institutions to allocate a portion of their lending portfolio to renewable energy projects could further promote sustainable growth in the energy sector.

Fifth, inflationary pressures need to be addressed to ensure the sustainability of renewable energy investments, as they exert a strong and persistent negative impact across most quantiles. Policymakers should consider implementing inflation-indexed subsidies and financial support programs to protect renewable energy investors from inflation-related risks. By stabilising borrowing costs and ensuring the availability of affordable credit, the negative impact of inflation on renewable energy consumption can be mitigated. Furthermore, proactive monetary policies that target inflation can create a stable macroeconomic environment, fostering the long-term growth of renewable energy projects. Additionally, given the four-year presidential election cycle in the US, changes in administration often result in shifts in policy priorities related to renewable energy. These shifts could influence the timing of funding and regulatory support for clean initiatives, as well as interesting cyclical volatility in renewable energy consumption. Therefore, establishing a bipartisan policy framework, multi-year green investment commitments, and independent regulatory bodies can help ensure policy continuity and investor confidence.

While this study provides valuable insights for the dynamic quantile specific and time varying impact of macroeconomic factors on renewable energy consumption in the US, several limitations need to be acknowledged, For instance the analysis is confined to the single country context, which may limit the generalisability of findings for different economic and financial structure, regulatory environment and level of renewable energy penetration in economic activities. Besides, although the MWQR effectively capture complex interactions across quantiles and frequencies, it does not account for potential structural breaks or regime shifts that can be experienced due to the significant policy changes, technological shocks or global crises. Future research can expand this framework to a panel of countries to compare the cross-sectional heterogeneity in macroeconomic environmental linkage. In addition, integrating structural break tests, nonlinearity and causality models, or machine learning-based forecasting approaches can offer more detailed insights into the stability of the relationships. Moreover, exploring sectoral or state-level dynamics within the US, or incorporating climate risk indicators and a policy stringency index, can also help tailor renewable energy policy recommendations to specific institutional contexts.

Footnotes

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.