Abstract

Background:

Urban poor face a disproportionate burden of ill health and high out-of-pocket expenditure (OOPE), creating a severe unmet need for affordable and quality health care. This article highlights the impact of health insurance on OOPE and catastrophic healthcare expenditure among the urban poor of India.

Methods:

The study uses randomly collected household data from a baseline survey conducted in the states of Rajasthan and Uttar Pradesh. Separate Insurance impact models have been generated for the analysis.

Results:

Mean out-of-pocket health expenses is higher in the private health facility for the inpatient care but in case of outpatient care, the expenditure was more in public. Expenditure on medicine constitutes the largest part of the total OOPE. Insurance impact model shows that coverage on medicine alone can reduce medical impoverishment by 85% in the case of Outpatient Deparment (OPD) and 71% in the case of Inpatient Department (IPD). The urban poor preferred private facility for treatment in case of illness, albeit when it comes to delivery, they prefer public facility

Conclusions:

Study findings indicate overt reliance on private health care must be regulated, to reduce OOPE among the urban poor. Also, effective universal health insurance can go a long way in reducing the OOPE with availability of free medicines and diagnostics in the public health facilities.

Background

According to census 2011, the urban population is estimated to be 377.1 million which is 31.1% of the total population and had a growth rate of 2.8% per annum during the period 2001–2011 and projects that by 2030, another 250 million people will migrate to Indian cities (The World Bank, 2011). Rapid urbanisation and unplanned growth of cities in India have led to the creation of these large urban poor population or the base of pyramid (BOP) population (spending 3–9 US $/day). As migration to cities increases, the rates of poverty rises in urban and shrinks in rural areas (International Food Policy Research Institute, 2017). According to the Planning Commission, 13.7% of the urban population is estimated to be below the poverty line in the year 2011–2012 (Ministry of Housing and Urban Affairs, 2019). Mostly the urban poor population lives in slums, with no provision of basic civic amenities or social services such as sanitation, adequate diet, education and healthcare utilisation. This continuous growth of the urban population creates alarming problems related to health and wealth in the urban areas of the country (Usmani & Ahmad, 2018).

Health of Urban Poor

Urban poor face a disproportionate burden of ill health and high out-of-pocket expenditure (OOPE), creating a severe unmet need for affordable and quality health care as they face significantly higher social and financial barriers to accessing healthcare (Chowdhury, 2009).

Currently, India is in a stage of epidemiological transition that can be distinguished by high morbidity, low mortality and a dual burden of communicable diseases and non-communicable diseases. Studies have reported a high burden of risk factors and chronic conditions among the urban poor in low and middle-income countries, including India (Bhojani et al., 2013). There is substantial evidence showing health indicators being worse among urban poor than the non-poor. Prevalence of disease like TB and malaria is highest among the low-income group compared to middle and high-income group in the urban areas of states Uttar Pradesh, Bihar, Maharashtra, Andhra Pradesh and Madhya Pradesh (Gupta & Mondal, 2015). Indicators of maternal and child health such as levels of antennal care, safe delivery, child vaccinations and malnutrition in children are also worse among the urban poor than non-poor counterparts (Agarwal, 2011; Prakash & Kumar, 2013). In addition, they are also more likely to seek care from less qualified healthcare professional and incur catastrophic health spending (Seeberg et al., 2014). Bhojani et al. (2013) found that presence of inequities acts as adverse social determinants leaving the urban poor of India with poor health indicators.

Expenditure on Health

In India, around 82% of outpatient care and 56% of inpatient care takes place in the private sector (Garg & Karan, 2009), but this sector is highly fragmented and consists of various types of providers. Some are informal providers and less than qualified (Montagu & Goodman, 2016). Among urban poor households of three cities of India, a large proportion (63% in Bhubaneswar, 61% in Jaipur and 84% in Pune) choose to visit private health facility over Public health facility at the time of sickness of any family member (Singh et al., 2018). This reliance on the private health sector results in a situation where the vast majority of health spending is financed out-of-pocket which puts a financial burden on households, especially poor ones (Bhat et al., 2018).

High OOPE is reported on the outpatient care, inpatient care and childbirth. The NSSO 75th data provide the estimates on OOPE on outpatient care as ₹710, ₹26,475 per hospitalisation and ₹16,092 per childbirth in urban India but that does not always represent the urban poor. The proportion of expenditure in healthcare has increased more for the poorest households of urban India over the years from 1995 to 2004 (Balarajan et al., 2011). Among urban poor, cost of healthcare in Delhi is estimated to be on an average ₹287 for outpatient which is higher for private healthcare as expected. OOPE on hospitalisation was on an average ₹5,112 with expenditure being higher for those who didn’t have any health insurances.

Impact of Health Expenditure

In India, between the year 1995–1996 expenditure survey and 2014 utilisation survey, the proportion of households with catastrophic health expenditure (CHE) has increased 2.24 folds, additionally, it was greater among more developed states than the less developed states (Pandey et al., 2017). OOP health expenditure has been estimated as high as 89.2% in India, (Saksena et al., 2012) which is big barrier in the way of India’s quest to achieve Universal Health Coverage (UHC) (Modugu et al., 2012; van Doorslaer et al., 2006).

The impoverishment impact due to high OOPE on Indian households is also well established in literature. The incidence on financial catastrophe due to healthcare expenditure is highest among the poorest households of Bangalore (Bhojani et al., 2012). Among low-income groups too, the poor lower income group shows higher incidence of CHE compared to poor higher income group in urban poor neighbourhoods of India, Indonesia and Thailand (Seeberg et al., 2014).

In India, 75% of household health OOPE were spent on medicines (Garg & Karan, 2009). Wagner et al. (2007) found that in low- and middle-income countries, health-related OOPE for medicines represent between 26% and 63% of total OOPE. Wagner et al. (2007) and Sangar et al. (2019) also found that in low- and middle-income countries like India, financing of health-care expenditure is predominantly characterised by out-of-pocket (OOP) spending. In India financing drugs and diagnostics is of recent importance because of the reported high OOPE on their purchase especially among the poor (Garg & Karan, 2009).

Results reveal that in urban areas of India, the incidence of OOP health expenditure is concentrated towards poorer consumption groups, whereas in rural areas, it is pro-rich, especially at higher threshold levels (Sangar et al., 2019). Financially protecting households from high OOP payments can be achieved either by funding health services through taxes or risk pooling through an insurance mechanism (Shahrawat & Rao, 2012).

Healthcare Coverage

In India, there is an extensive network of national and state-level publicly financed health insurance schemes such as RSBY, CGHS and Bhamashah Swasthya Bima Yojana, which provide low-cost preventive and curative health services. Yet data from MOPSI, NSS 75th round, show that only 10% of the poorest one-fifth Indians in urban India have any form of government or private health insurance (NSSO, 2019).

However, this system has been ineffective in reducing OOP payments and providing financial protection to the urban poor because these insurance schemes do not provide cover for the outpatient care. But a large segment of the population is the working urban poor, who represent ‘the missing middle’, a large percentage of the population that remains without financial protection, sandwiched between those who are affluent enough to afford health care and those who benefit from government-sponsored health insurance schemes (Bhat et al., 2018).

Impact of Insurance

Many studies have found the potential impact of how health systems are financed on the well-being of households, particularly the poor, has influenced the design of health systems and insurance mechanisms in settings as diverse as the USA, Australia, India and Indonesia (Pradhan & Prescott, 2002; Ranson, 2002; Rice et al., 1990). Doing a multi-country analysis Xu et al. found that prepayments through social insurance, taxation or private insurance are often labelled as mechanisms to achieve financial risk pooling (Xu et al., 2003). Results from their study also reflected that even small costs for common illnesses can be financially disastrous for poor households with no insurance cover. Implementation of universal health insurance leads to significant decreases in the incidence of total potential CHE (World Health Organization, 2006).

Generally, health insurance has been found to increase the utilisation of healthcare and reduce the OOPE; however, it may not be true for all Health insurance programs (Ekman, 2007). Systemic literature review on OOPE after enrolment in National Health insurance scheme in Ghana has demonstrated OOPE by uninsured to be 1.4 to 10 times more and were more likely to incur CHEs than the insured (Okoroh et al., 2018). Evidence from a study in Indonesia showed two health insurance schemes, Askeskin and Askes have reduced OOPE by 34% and 55%, respectively, compared to non-askeskin and non-Askes (Aji et al., 2013). In China too, there is evidence of increase in the probability of accessing healthcare and decrease in the level of OOPE with the availability of health insurance (Jung & Liu Streeter, 2015). However, on a contrary, impact evaluation on RSBY health insurance scheme of India shows that it has failed to reduce OOPE on poor household for both inpatient and outpatient care (Bahuguna et al., 2019; Karan et al., 2017).

From this introductory discussion it is evident that social or individual insurance has an impact on OOPE on health. Research done on potential impact of insurance on OOPE and CHE incurred by the urban poor population especially in Indian context is scanty. So, the present study was undertaken to fulfil the existing gap in evidence, under IPE Global’s Project PAHAL (Partnerships for Affordable Healthcare Access and Longevity) in India, which aims to catalyse the private sector in developing quality and affordable healthcare solutions for the urban poor. Specifically, in this article we report the impact of health insurance on OOPE and CHE due to healthcare expenses among the urban poor or BOP population.

Methods

Data

The data for this article are derived from a baseline cross-sectional survey conducted in two states of Rajasthan and Uttar Pradesh. The intervention districts were Jaipur and Bharatpur in Rajasthan, and Lucknow and Allahabad in Uttar Pradesh. The findings of this article are based on the subsample analysis of the larger data collected for the baseline survey.

Participants and Sampling

The study was conducted among the urban poor population who were earning between 3 and 9 US$/day. In the selected districts, 5 urban wards were selected and in each ward 2 census enumeration block (CEB) were selected. Household selection was done applying systematic random sampling using right-hand rule till the time the desired sample was reached. The survey sample included a total of 3,270 respondents.

The data were collected from head of the household on socio-demographic characteristics, household assets and consumption expenditure with the help of a pre-designed and pre-tested semi-structured questionnaire. The respondent was interviewed for presence of any member with an illness in last 15 days or a hospitalisation during the last 365 days or reporting pregnancy in the last 1 year. Reasons for illness, treatment sought, associated OOPE incurred and mechanisms to cope for the OOPE were subsequently elicited. Quality control was undertaken by field supervisors, who revisited 5% of sampled households to check accuracy of data. Any discordance was resolved through discussion and re-visiting the household. The data collection was done using Computer Assisted Personal Interview (CAPI) using a tablet only after obtaining written informed consent.

Data Analysis

The data were analysed using IBM SPSS ver. 21. Along with OOP expenses on health and prevalence of CHE, impoverishments due to OOPE on delivery, acute illness hospitalisation were computed.

Socio-economic strata for households were determined by division of total sample arranged according to household consumption expenditure. Equivalent household size and equivalised food expenditures were computed using the standard methodology prescribed by WHO as mentioned in study by Xu (World Health Organization, 2005). These were used to generate subsistence expenditure and capacity to pay for each household. Households incurring health care expenses equal to or more than 40% of their capacity to pay were considered as having CHE. If the annual household consumption expenditure was less than subsistence expenditure, the household was characterised as poor, and vice-versa. Households that were above poverty line before incurring healthcare expenses but went below poverty line after healthcare expenditure was characterised as impoverished due to healthcare expenses. Wealth status was assessed using household consumption expenditure.

Ethical clearance for the study was obtained from the Institute Ethics Committee of School of Public Health, Post Graduate Institute of Medical Education and Research, Chandigarh, India. Written informed consent for participation was obtained from the eligible respondents after explaining the purpose of the survey.

Results

Sample Characteristics

Socio-demographic Characteristics of the Study Population.

Household Consumption Expenditure

Average Household Expenditure Pattern.

Outpatient Visits

Illness Rate and Choice of Facility for Treatment.

Out-of-pocket Expenditure on Outpatient Visits

Average Annual Out-of-pocket Expenditure on Outpatient Care.

Potential Impact of Insurance Scheme on Out-of-pocket Expenditure on OPD and Resultant Financial Catastrophe and Impoverishment (scenario 1).

Potential Impact of Insurance Scheme on OPD Expenditure

Table 5 shows the potential impact of an insurance scheme on OOPE on outpatient care among the urban poor households. The present study results showed 10.5% of the household were facing the CHE and 4% of households impoverished because of the high OOPE on outpatient care. It was observed that providing an insurance cover for medicines only will lead to a 77.7% reduction in the OOPE and more than 85% reduction in CHE and impoverishment. Additionally, cover for diagnostic tests in scenario 1 will further reduce OOP expenditure by 84.9% and CHE by 94.3%. Similarly, providing cover for medicines, diagnostic tests as well as consultation charges will result in 98.6% reduction in OOPE while CHE will become zero.

Hospitalisation

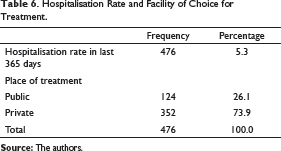

Hospitalisation Rate and Facility of Choice for Treatment.

Out-of-pocket Expenditure on Hospitalisation

Out-of-pocket Expenditure on Hospitaisation Episode.

Potential Impact of Insurance Scheme on Out-of-pocket Expenditure on IPD and Resultant Financial Catastrophe and Impoverishment (scenario 2).

Potential Impact of Insurance Scheme on IPD Expenditure

Table 8 shows the potential impact of an insurance scheme on OOPE on IPD. The present study results showed 13.2% of the household were facing the CHE and 5.2% of households were impoverished because of the high OOPE on inpatient care. It was observed that providing an insurance cover for medicines only will lead to a 53.2% reduction in the OOPE and 68.2% reduction in CHE and 71% reduction in impoverishment rate. Addition of cover for diagnostic tests in scenario 2 will further reduce OOPE by 63.2% and CHE by 76.5%. Similarly, providing cover for medicines, diagnostic tests as well as consultation charges will reduce the catastrophe by 98.5% and impoverishment rate to zero.

Childbirth

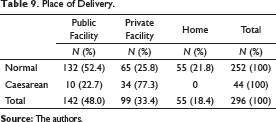

Place of Delivery.

Out-of-pocket Expenditure on Delivery

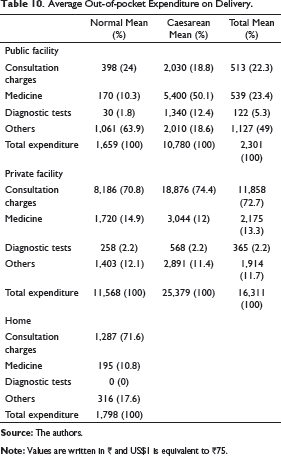

Average Out-of-pocket Expenditure on Delivery.

Potential Impact of Insurance Scheme on Out-of-pocket Expenditure on Delivery and Resultant Financial Catastrophe and Impoverishment (scenario 3).

Potential Impact of Insurance Scheme on Delivery Expenditure

Table 11 shows the potential impact of an insurance scheme on OOPE on delivery. The present study results showed 7.4% of the households were facing the CHE while 4% of the households faced impoverishment due to high OOP expenses on delivery. It was observed that providing an insurance cover for medicines only will lead to a 14.8% reduction in the OOPE (from ₹6,866 to ₹5,851) and 27% reduction in CHE (from 7.4% to 5.4%). Further, there will be 15.4% reduction in the impoverishment (from 4.02% to 3.4%). Addition of cover for diagnostic tests in scenario 1 will further reduce OOPE by 17.4% and will not make any difference to CHE but will reduce the impoverishment by 25.4%. However, under scenario 3, where the insurance scheme potentially provides cover for medicines, diagnostic tests and consultation charges, there will be 81% reduction in OOPE with 100% reduction in CHE. This will also result in the 92.5% reduction in the household impoverishment.

Discussion

The present study population represents the socioeconomically disadvantaged urban poor of the society. In countries like India where the health system is highly privatised and insurance coverage low, it is critical that people, particularly the poor, are protected from high OOP payments for health care. Not surprisingly, the current study shows that nearly 11% of household faced catastrophic health expenses on outpatient care followed by nearly 13% due to inpatient care and more than 7% due to childbirths. More preference for private facilities was seen among the respondents. The study showed that having a health insurance product was critical in bringing down the OOPE, resultant catastrophe and impoverishment among urban poor households.

Our results showed a preference among the urban poor for private sector facilities to utilise outpatient care (74.9%) and inpatient care (73.9%). This finding corroborates with the NSSO 75th round survey report of urban India, which states that 71% of the outpatient care and 61% of the inpatient care are treated in private healthcare. Similarly, in case of child birth, our study reports that public sector (48%) was sought predominantly for childbirths, and NSSO 75th rounds also states that among the poor urban population of India more than 58% of deliveries were taking place in public hospitals (NSSO, 2019). Another study in undeserved urban areas of Mumbai shows that poorer people mostly visited public facility for institutional delivery (More et al., 2009).

The results of the study are in same line with previous studies which shows greater preference for private facility over public facilities, such as a study in the Slum and non-slum urban poor population in three cities of India, which shows that a large proportion of households (40% in Bhubaneswar, 62% in Jaipur and 77% in Pune) choose to visit private health facility (Singh et al., 2018). Similar evidence also persist from urban poor of Mumbai (Arya, 2012; Thandassery & Duggal, 2004). As high as 89% of urban poor with chronic conditions in Bangalore receive care from private facility (Gowda et al., 2015) and also this percentage is high among urban poor in Delhi (Kusuma & Babu, 2019).

Our study found that the overall mean OOPE for outpatient care in a year was ₹20,364 with more utilisation of private facilities for outpatient care. NSSO 71st round shows that in the lowest and second to lowest economic quintile of Urban India, OOPE on healthcare is ₹756 and ₹1,635, respectively, for outpatient care, partial reason of this disparity may be due to the difference in the time period. Study by Ravi et al. (2006) also reveals that average annual OOP spending on health in India have also increased by ₹200 in 1st economic quintile and ₹369 in 2nd economic quintile of urban poor population of India from the year 2004 to 2014. Surprisingly, our study reports higher expenditure in public facility (₹27,928) in OPD than in Private facility (₹18,399) mainly due to the exorbitant expenditure in medicine in Public facility. Contrary to this finding, literature shows average expenditure among outpatient to be much higher in private than public facility among urban poor as per NSSO 71st round report and also among urban poor in Vadodara district of Gujarat (Ranson et al., 2012) and in Delhi (Kusuma & Babu, 2019). However multi country study among low income countries showed more OOPE in public facilities than in private facilities in 12 out of 29 countries, one of them being India (Saksena et al., 2012).

Our study reported higher expenditures in private facilities than public facilities for IPD unlike for OPD. NSSO and other studies have reported the mean OOPE to be more in private facilities than in public sector facilities on both outpatient and hospitalisation (Selvaraj & Karan, 2009). This calls for an action to strengthen the public sector so that more and more people can utilise affordable health care, which in turn will further reduce OOPE. Moreover, there is a need to reduce OOPE in public sector further. Since medicines and diagnostics are two major factors which constitute the OOPE, strengthening the provision of free drugs and diagnostics in the public sector are straightforward interventions to reduce OOPE. A predominantly large proportion of Indian population continues to access outpatient and inpatient care in private sector leading to high OOPE. Hence, there is concurrent need to provide financial risk protection through some form of risk pooling for coping with OOPE in private sector (Fan et al., 2012; Sood et al., 2014).

Our study, similar to other studies (Fan et al., 2012; Garg & Karan, 2009; Mahal et al., 2010; MoHFW, 2005; Prinja et al., 2012; Ranson et al., 2012) found that the major component of OOPE was on drugs for both outpatient and inpatient health care services, which can be as high as 70% of the total expenditure. There is a possibility that the availability of medicines is not always ensured in public health facilities, which in turn forces patients to buy it from private market. Prinja et al. (2015) found that in Punjab and Haryana the overall availability of medicine was 42% and 51%, respectively, in the Public health facilities. Similarly, another study in Delhi have shown overall mean availability of medicine to be 41% and 23% in facilities under state government and municipal corporation of Delhi, respectively (Kotwani, 2013).

In our study the expenditure on delivery in private facilities was almost seven times than that in public facilities. Similar findings were reported by a study on urban slums of Bhubaneswar where 12 times more expenditure in private facilities was found (Sahu & Bharati, 2017). The NSSO 71st round report also stated eight to nine times higher expenditures in private facilities by urban poor of India.

Results suggests that among the study population, nearly 13% of households suffered financial catastrophe, while 5% of the households were impoverished due to OOPEs on hospitalisation. Similar results has been reported in a study by Bhojani et al. (2012) in Bangalore, who found 16% CHE rate among urban poor households due to chronic conditions. Another study in Haryana on general population, reported higher percentage of CHE (25.2%) by households faced due to hospitalisation (Sharma et al., 2017).The catastrophic head count of urban India due to maternal health care has been recorded as high as 79% in the lowest economic quintile and 55% in the second to lowest quintile with 31% impoverishment (Mukherjee, 2012), whereas our study shows CHE in case of nearly 7% household with 4% of the households being impoverished due to OOP expenses on delivery. Another study in urban slums of Odisha had reported 15% CHE due to delivery, and also reported that CHE would had been more than 31% if government schemes such as JSY and Mamata scheme didn’t exist (Sahu & Bharati, 2017).

Findings from this study suggest that OOPE on out patient can be reduced significantly by providing insurance cover for medicines (accounting for 77.7% of total expenditure in OPD) which have the largest impact on catastrophe and impoverishment. Shahrawat and Rao (2012) also found that reducing OOP payments for drugs has remarkable effects on reducing impoverishment due to OOP payments for health care.

In contrast, if we provide insurance on only medicines for inpatient care, it will have less impact compared to outpatient care since expenditure on medicine accounts for only 53% of total expenditure in inpatient care unlike nearly 78% in outpatient care. In light of these findings, other literature also shows evidence of medicine comprising of the major share of OOPE (72%), this share is higher for outpatient care compared to inpatient care among poor Indian population (Garg & Karan, 2009; Shahrawat & Rao, 2012).

Strengths and Limitations

Our study provides information focussing on the urban poor only which is an important dimension and use of Insurance impact models which were generated separately for outpatient, inpatient and childbirths is another strength of this study.

We would also like to acknowledge some limitations of this study in terms of the methodology employed. One of the main concerns is the existence of bias attributable to the fact that the reference period for data collection was 1 year. So, there is a possibility of recall bias creeping in data collection. However, collection of data for hospitalisation using a 1-year recall is a standard practice globally in household surveys (Kjellsson et al., 2014). The current study was conducted on the base of pyramid population belonging to northern Indian states so their characteristics might be different from other parts of the country. Also, the data do not permit analysis at individual level because expenditure is reported at the household level. Finally, as the calculation of out-of-pocket payments did not include indirect costs such as the loss of household income, the proportion of CHE may have underestimated the extent of financial hardship to households. However, the comparability of our results to those from previous surveys and studies validate our findings.

Conclusions

Overall, the findings of our study shows that mean OOPE is higher in private facility for IPD but in case of OPD, expenditure is more in public facility which is mainly due to the substantial amount of expenses on medicine. Expenditure on medicine constitutes the largest part of the total OOPE and insurance impact model shows that coverage on medicine alone can reduce medical impoverishment by 70%–85%. It is worth pointing out that among the urban poor, the preferred choice of facility for treatment in case of illness is private facility, albeit when it comes to delivery, more people preferred to go to public facility. Furthermore, the study sheds light on the fact that number of caesarean deliveries in private was thrice as that of in public facilities. This recommends policy makers and responsible stakeholders or public health workers to work on enabling the public health facilities for better responsiveness and upgraded facilities for caesarean deliveries. Study findings indicate that the overt reliance on private health care must be regulated, to reduce OOPE among the urban poor. Study results highlight the importance of strategies for strengthening the provision of medicines and diagnostics. The Government needs to improve the availability of medicines and diagnostics in public facilities and priorities increasing spending on healthcare as according to study findings, high OOPE are reported even at the public facilities, which is mainly due to medicines and diagnostics. Further, this study can be informative in discerning the right kind of policy for insurance schemes to CHE expenditure and medical impoverishment among urban poor. The advantage of the access of PAHAL programme to private healthcare facilities can be exploited towards development and provision of an essential health package (EHP) that will include essential services at all levels of care for the benefit of this urban poor community and can also accompany policy changes to increase insurance coverage. Policy makers can think of introducing Insurance Impact models that can be helpful in reducing OOPE and achieving the goal of universal health coverage. Also, effective universal health insurance can go a long way in reducing the OOP with availability of free medicines and diagnostics in the public health facilities. Policy makers, researchers, academicians, public health workers, stakeholders may not restrict in applying the results of the insurance impact models only on the urban poor, but also to other urban communities and rural areas too with similar setup. This will ensure protection of households against CHE.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the USAID [grant number AID-386-A-15-00014] under the project PAHAL, IPE Global.