Abstract

This study investigates how information asymmetry influences the equity shares acquired in cross-border acquisitions by Chinese firms. Taking an institution-based perspective, we propose that the extent to which Chinese acquirers react to information asymmetry in the way as predicted by economic perspectives will be influenced by the home institutions of these emerging market multinational enterprises. Based on 547 cross-border acquisitions made by Chinese acquirers from 1987 to 2007, the findings show that Chinese state-owned acquirers were less committed to an economic logic than non-state-owned acquirers. The institutional transition taking place in China in recent years has increased the importance of economic drivers for the Chinese acquirers.

Keywords

Introduction

When a firm decides to expand abroad through foreign direct investment (FDI), it has to determine whether it is going to have a wholly owned foreign subsidiary or to share the ownership with other parties. That ownership decision is of significant strategic importance owing to the inherent benefits and risks of different entry modes (Dikova & van Witteloostuijn, 2007). Economic perspectives regard information asymmetry as an important determinant of ownership decisions of FDI (Anderson & Gatignon, 1986; Beard, 2007; Folta, 1998; Hennart, 1988; Kogut, 1991). Firms are assumed to choose an optimal ownership strategy that maximizes profits so that they will not be outperformed by the competitive environment (Williamson, 1981). Although this assumption is usually treated as implicit, it is crucial for the claim that the most frequently observed strategies should be the ones suggested by these economic perspectives. Empirical studies, however, are limited in examining the boundary conditions for these assumptions, particularly for emerging market multinational enterprises (MNEs).

Taking an institution-based perspective (Peng, Li, Brian, & Chen, 2009), we propose that the home institutions of emerging market MNEs tend to influence acquirers’ responsiveness to information asymmetry as predicted by economic perspectives. We argue that (a) when an MNE is state owned, the assumption about profit maximization may not strictly hold and (b) when home institutions suppress market competition, the assumption about market selection may not strictly hold. In both cases an investing MNE would be less sensitive to information asymmetry, and it may not be possible to predict, using current economic perspectives, the strategies that MNEs from emerging economies choose.

China provides a good context for testing these arguments, for three reasons. First, although the outflow of FDI from China has increased dramatically in recent years, newly emerging MNEs from China are still heavily influenced by institutional factors back home (Peng, 2012; Sun, Peng, Ren, & Yan, 2012). Second, China still has a significant state sector, where state-owned enterprises (SOEs) are expected to assume various obligations such as maintaining payrolls, supporting national development plans, and kowtowing to other politically motivated objectives (Lin, Ma, & Su, 2009; Ralston, Terpstra-Tong, Terpstra, Wang, & Egri, 2006). This means that economic perspectives may not predict Chinese SOEs’ entry strategies as well as they predict those of other Chinese acquirers. Third, China is also being characterized by frequent changes in the regulatory frameworks and interferences from various government authorities in business decisions (Luo, 2002, 2007). Since China joined the World Trade Organization (WTO) in 2001, and with continued economic reforms, Chinese firms have been increasingly facing the market competition and selection forces, adopting an economic logic. Economic perspectives should, therefore, better predict Chinese acquirers’ entry strategies in recent years compared with those in earlier years.

Most of the above arguments were supported by our empirical study on 547 cross-border acquisitions (CBAs) made by Chinese firms from 1987 to 2007. Compared with the state-owned Chinese acquirers, the Chinese acquirers with other ownership structures were generally more responsive to information asymmetry at the firm-, industry- and country-levels in their choice of ownership-based entry mode. As a whole, Chinese acquirers have responded more actively to information asymmetry at different levels in the years after China’s entry into WTO.

The current study aims to contribute to the extant literature in the following three areas. First, we examine the extent to which information asymmetry as predicted by economic perspectives can explain Chinese acquirers’ ownership choices in their CBAs. Second, we examine the interplay of information asymmetry and home institutional factors in determining MNEs’ ownership strategies overseas. We suggest that institutional factors, such as market transition and state ownership, moderate the relationship between information asymmetry and entry strategy. Third, the China context sheds light on the specific pattern of internationalization strategies of emerging economy MNEs.

Theory and Hypotheses

The choice of ownership level in overseas subsidiaries has long been considered an important decision that influences “the control over the venture, the effective transfer of tacit assets, investment requirement, and risk” (Chari & Chang, 2009, p. 1278). Among the extensive literature that has thoroughly investigated various ownership decisions (e.g., acquisitions vs. joint ventures), the determinants of ownership-based entry mode strategy in CBAs for MNEs from emerging economies have not drawn adequate attention in the literature. Building on and extending the main stream economic perspectives largely developed in a Western context, we intended to develop a more contextualized multitheoretic framework to examine the determinants of ownership-based entry mode strategy in CBAs conducted by emerging Chinese MNEs. We focus on information asymmetry (Balakrishnan & Koza, 1993; Chen & Hennart, 2004; Reuer & Koza, 2000) as the key economic conceptual factor that influences firms’ ownership decisions in their CBAs.

Information Asymmetry

Information is asymmetric when one transaction party is better informed than the other, especially when each transaction party withholds private information from each other (Kulkarni, 2000; Varian, 1999). This usually leads to problems such as adverse selection and moral hazards, and yields loss in economic efficiency (Akerlof, 1970; Arrow, 1971; Varian, 1999). CBAs take place in the international market for corporate control, where information asymmetry usually occurs as the seller knows more about the true value of the corporate assets than the buyer (Balakrishnan & Koza, 1993). This gives rise to adverse selection problem and increases the searching cost of the buyers. Acquiring a smaller stake in the target firm can mitigate the hazards of adverse selection (Chen & Hennart, 2004; Reuer & Koza, 2000), because the willingness of the seller to continue to hold substantial equity is a signal of its greater confidence in the quality of the assets for sale. This suggests that the share of ownership purchased in a CBA should be lower in the presence of greater information asymmetry (Beard, 2007).

In addition to adverse selection problem, information asymmetry may also lead to moral hazards, increasing the cost of contract enforcement. After the CBA contracts are signed, the transaction partners may still refuse to comply to their terms, especially when one party cannot accurately evaluate the other’s performance. Anderson and Gatignon (1986) call this “internal uncertainty.” Internal uncertainty is high when acquirers new to a technology, an industry, or a host country are unlikely to fully understand how the partners feel they should behave and how to judge hard-to-quantify results (Anderson & Gatignon, 1986). If they insist on control without knowing how to do it, they may be prone to serious errors that depress the efficiency of the target (Teece, 1976, p. 46). Greater information asymmetry in a CBA transaction thus increases the difficulty in contract enforcement, which encourages an acquirer to buy less equity and delegate some management and control to the original owners.

Information asymmetry may take place at the firm-, industry-, and country-levels. Firm-level information asymmetry was usually operationalized by the technology intensity of the firm. When the target firm operates in a high-technology industry, greater cost is involved in evaluating the target’s assets. This is because the most valuable assets of a high-tech firm usually lie in its knowledge, which is not likely to be fully quantifiable either for the purpose of searching or contract enforcement (Singh & Kogut, 1989). Industry-level information asymmetry usually occurs to diversifying acquirers. When the acquirer and the target firm are from different industries, it is more difficult for the acquirer to be as well informed about the value and performance of the target as the original owners (Balakrishnan & Koza, 1993; Chen & Hennart, 2004; Reuer & Koza, 2000). One frequently used indicator of country-level information asymmetry is cultural distance (Anderson & Gatignon, 1986; Kogut & Singh, 1988). It is believed that cultural distance creates barriers for acquirers in communicating with local employees, suppliers, governments, and other stakeholders, making them rely more on local partners (Barkema & Vermeulen, 1998). To sum up, economic perspectives suggest that in order to mitigate the loss in economic efficiency caused by information asymmetry, the acquirers should take less ownership shares in the target in CBAs in the presence of high-tech target, cross-industry diversification, and large cultural distance.

The Moderating Effect of State Ownership

Institutions set the “rules of the game” for business (North, 1990, p. 3), and can significantly shape firms’ strategies (Chan & Makino, 2007; Peng et al., 2009; Yiu, Lau, & Bruton, 2007). They influence firms’ foreign market entry strategies through their effects on economic factors such as transaction costs (Coase, 1988; Meyer, Esterin, Bhaumik, & Peng, 2009) and also through the social constraints they place on firms’ strategic choices (DiMaggio & Powell, 1983; Scott, 1995). In addition, we suggest a third mechanism: Institutional factors can lessen the importance of economic efficiency in firms’ decision making and further alter their strategic choices.

Williamson (1981) observed that, “the governance implications of transaction cost analysis will be incompletely realized in noncommercial enterprises in which transaction cost economizing entails the sacrifice of other valued objectives” (p. 574). Organizations which are not purely profit-driven may have good reasons not to adopt the optimal governance structure suggested by economic analysis. SOEs are typical examples of these non-economic-driven organizations for two reasons. First, SOEs suffer from serious agency problems. Agency problems occur when cooperating parties have different goals and division of labor (Jensen & Meckling, 1976; Ross, 1973). SOEs are generally considered to suffer more from agency problems than private firms mainly because of the double goal-conflict they face. On one hand, SOEs are actually controlled by bureaucrats who have concentrated control right but not significant cash flow right since the latter is dispersed among the taxpayers of the country (Shleifer & Vishny, 1994). On the other hand, SOE managers are public employees who “cannot personally reap the benefits of increasing revenues yet they will bear many of the costs (i.e., angry workers and disgruntled suppliers) of reducing the firm’s production costs” (Megginson, 2005, p. 39). Agency problems reduce SOEs’ commercial motivation and may prevent them from choosing the optimal ownership strategies in CBAs.

The second reason why SOEs tend to be less profit-driven is that they have various obligations such as maintaining payrolls, supporting national development plans, and kowtowing to other politically motivated objectives (Lin et al., 2009). In almost all countries SOEs enjoy soft budget constraints for them to assume these multiple obligations (Zheng & Chen, 2009). In the case of CBAs, for example, state-owned acquirers may take responsibilities such as securing key strategic natural resources, bridging relationship between two countries, and transferring monetary resources to target governments.

All these make Chinese SOEs less likely to conform to economic perspectives. In particular, state-owned acquirers are less likely to respond to information asymmetry in choosing ownership-based entry mode as predicted by economic perspectives, whether the information asymmetry occurs at the firm-, industry-, or country-levels.

Hypothesis 1a: Ceteris paribus, state ownership moderates the relationship between target technology intensity and equity share purchased in a cross-border acquisition, such that the effect should be more negative for non-state-owned than for state-owned Chinese acquirers.

Hypothesis 1b: Ceteris paribus, state ownership moderates the relationship between diversification and equity share purchased in a cross-border acquisition, such that the effect should be more negative for non-state-owned than for state-owned Chinese acquirers.

Hypothesis 1c: Ceteris paribus, state ownership moderates the relationship between cultural distance and equity share purchased in a cross-border acquisition, such that the effect should be more negative for non-state-owned than for state-owned Chinese acquirers.

The Effect of Institutional Change

Any organization relies to some extent on the external environment for scarce and valuable resources; therefore, organizations will sometimes alter their structure or their pattern of behavior to acquire and retain needed resources (Pfeffer & Salancik, 1978). MNEs from emerging economies are generally in the early stages of internationalization, and their foreign business is initially only marginal, especially for MNEs from nations with a large domestic market (Hedlund, 1986). Although internationalized, these MNEs typically still rely heavily on their home countries for key resources, and react sensitively to the selection forces in the home country by choosing strategies favored by home country selection forces. In competitive markets, the selection forces are generated by market competition and the selection criteria promote long-run economic efficiency (Williamson, 1981). Firms that fail to choose optimal strategies are, by definition, less profitable (Brouthers, Brouthers, & Werner, 2003; Chiles & McMackin, 1996; Hennart, 2007; Li, 1995; Silverman, Nickerson, & Freeman, 1997), and eventually fail in the market if they continue to make suboptimal choices. In emerging economies where market institutions are less developed, however, these market selection forces may not be as sufficient (Anderson, Lee, & Murrell, 2000; Li & Qian, 2012).

Emerging economies are experiencing rapid economic growth driven by economic liberalization (Peng, 2003). In the early stage of liberalization the number of market players is likely to be small due to various entry barriers. When there are a limited number of competitors in a rapidly growing market, the market is not likely to be very selective. Firms low in efficiency can still survive; however, as the level of liberalization increases, and especially as international competitors pour in, the competition intensifies substantially (Salvatore, 2010). This has been the case in China in recent years. China’s WTO membership since late 2001 started to remove entry barriers and stimulate product market competition. Even SOEs were forced to adopt an economic logic to compete (Zheng & Chen, 2009). These changes have intensified the competition faced by Chinese firms who previously were not concerned as much about profit maximization (Jia, 2009; Ralston et al., 2006). This suggests that Chinese acquirers should be more responsive to economic determinants of entry mode choice, such as information asymmetry, after China’s 2001 WTO entry:

Hypothesis 2a: Ceteris paribus, China’s entry into WTO moderates the relationship between target technology intensity and equity share purchased in a cross-border acquisition, such that the effect should be more negative in the years after its entry into WTO.

Hypothesis 2b: Ceteris paribus, China’s entry into WTO moderates the relationship between diversification and equity share purchased in a cross-border acquisition, such that the effect should be more negative in the years after its entry into WTO.

Hypothesis 2c: Ceteris paribus, China’s entry into WTO moderates the relationship between cultural distance and equity share purchased in a cross-border acquisition, such that the effect should be more negative in the years after its entry into WTO.

Method

Sample

Data on 572 CBAs completed by Chinese firms from 1987 to 2007 were identified from the SDC (Securities Data Company) database provided by Thomson Financial. They were used to test the hypotheses. Twenty-four transactions were dropped because of missing data. This left 547 CBAs in the final sample. The final sample was not significantly different from the original sample in terms of the average values of the variables studied. Of the 547, 106 of the transactions involved SOEs whereas the other 441 involved other types of firms. In all, 237 of the transactions were concluded before 2002 and 310 in 2002 or later. In 228 of these CBAs, the Chinese investor acquired less than 50% of the equity in the target; in 15, it acquired exactly 50%; in 78, it acquired majority control; and in 226, the Chinese firm acquired full ownership of the target.

Variables

Dependent variable

The dependent variable of this study was share acquired, denoting the percentage of equity shares acquired by the Chinese firm in a particular CBA, ranging from 0.01 to 100. The variable was coded with information from the SDC database.

Independent and moderating variables

The dummy variable non-state-owned acquirer was coded as “1” if the parent or the ultimate controlling shareholder of the acquirer was not the Chinese government and “0” otherwise. The information on parents and ultimate parents was extracted from the SDC database. The dummy variable post-WTO entry equaled “1” if the transaction happened in or after 2002 and “0” otherwise.

Control variables

There were six groups of control variables. The first group of variables was used to capture the simple main effects of information asymmetries. Firm-level information asymmetry was represented by a high-tech target dummy indicating whether or not the overseas target operated in a high-tech sector. Following the OECD’s classification based on industry-level technology intensity, the following four sectors were coded as high-tech: aerospace, computers/office machinery, electronics/communications, and pharmaceuticals (Hatzichronoglou, 1997). The high-tech target dummy was coded as “1” if the target operated in one of these sectors and “0” otherwise. Industry-level information asymmetry was represented by a product diversification dummy. In each transaction, the main business of the acquiring firm and that of the target were coded according to the North American Industry Classification (NAIC) system. It was developed and adopted by the Office of Management and Budget of the United States in 1997, to replace the Standard Industrial Classification system. If the first two digits of the acquirer’s and the target’s codes were different, the product diversification dummy was coded as “1,” and “0” otherwise. Following Kogut and Singh (1988), cultural distance, that is, country-level information asymmetry, was calculated as a composite index using Hofstede’s (1980) four dimensions of national culture,

where Iij is Hofstede’s index of the ith cultural dimension for the jth country, Vi is the variance of the index of the ith dimension, subscript c indicates China, and CDj is the cultural distance of the jth country from China.

The second group of control variables was designed to capture some firm-level factors which may influence the ownership strategies of acquirers. The CBA experience of an acquirer was measured in terms of the number of CBA transactions the Chinese investor had completed before the focal transaction but after 1987. Prior experience of CBA provides the firm with knowledge about how to collaborate with foreign employees and partners, how to operate in foreign markets, and so on. The increase in CBA experience is likely to increase the ownership stakes they seek in CBAs (Erramilli, 1991). The level of diversification of acquirer was measured by the number of NAIC sectors in which the acquirer operated. High-tech acquirer was a dummy variable defined in the same way as high-tech target. High-tech acquirers might be expected to purchase larger stakes in overseas targets to safeguard their own knowledge assets and/or take advantage of their own absorptive capacity.

Four transaction-level factors comprised the third group of control variables. The level of diversification of target was measured by the number of NAIC sectors in which the target operated. More diversified targets may be more difficult for acquirers to handle, so a negative effect was expected for the level of diversification of target. Publicly held target was a dummy coded as “1” if the target was publicly held and “0” otherwise. Buying a publicly held target usually involved larger amounts of financial resources but less information asymmetry, either a negative or positive relationship between publicly held target, and share acquired would be possible. Unfriendly was a dummy coded as “1” if the transaction partner held an unfriendly attitude toward the Chinese acquirer and “0” otherwise, based on the SDC data. Follow-on investment was a dummy equaling “1” if the focal transaction was not the first investment the acquirer had made in the same target and “0” otherwise. Unfriendly CBAs and follow-on investments were expected to involve only small equity stake acquisition. The data source was the SDC Platinum database.

The fourth group of control variables described the host environment. The country risk index in the International Country Risk Guide published by the Political Risk Service Group is a composite risk measure that estimates the relative political, financial, and economic risk of each country covered. Its estimates range from 1 to 100, with greater figures indicating less risk. Each country’s risk index was subtracted from 100 in the analysis to yield a country risk variable where greater figures indicate greater risk. It has been argued that in the presence of large country risk, firms would have an incentive to wait for new information before increasing their commitment to an investment (Folta, 1998; J. Li & Li, 2010). Preemption risk in the target country was measured by the value of CBA transactions completed there in the three previous years as a percentage of worldwide CBA transactions during that period (Chari & Chang, 2009). The data were obtained from the United Nations Conference on Trade and Development’s Cross-Border M&A database. High preemption risk indicates that there are more rivals competing in an acquisition market, so firms may choose not to wait. In addition, the results of studies of international strategy suggest that it is critical to secure a global market position by investing aggressively in countries that rivals find attractive (Hamel & Prahalad, 1985). Two-year average share was a measure of peers’ influence on Chinese investors. It was the average share acquired by Chinese firms in the same target nation and same industry in the 2 years previous to the focal transaction. According to DiMaggio and Powell (1983), the dominant practice of peers in the past is preferred by followers because it has acquired legitimacy. The gross domestic product (GDP) per capita of the host country as reported by the United Nations or the International Monetary Fund was also included. The institutional freedom index of the target country was that developed by the Fraser Institute, a nonprofit research organization in Canada that collects country-by-country data through 71 partner institutions. The index is designed to consider national regulations, freedom of international trade, access to financing, legal structure, security of property rights, the size and effectiveness of government expenditures, and taxes. Between 1970 and 2000, the index was published on a 5-year basis, then after 2000, yearly. Annual economic freedom indices for the years between 1970 and 2000, were generated by assuming a linear trend within each 5-year range.

The fifth group of control variables comprised industry dummies indicating the acquirers’ and targets’ industries based on Standard Industrial Classification codes. The sixth group consisted of year dummies indicating the year in which the focal transaction took place.

Models

Tobit regression models were evaluated to test the hypotheses, as they allow for censoring of the dependent variable (Greene, 1993) and share acquired had a theoretical range of 0 to 100. Prior empirical research extensively used Tobit regression to investigate the percentage of equity shares acquired in FDI (Chari & Chang, 2009; Cuypers & Martin, 2010).

To test Hypothesis 1, the interactions of the information asymmetry measures and non-state-owned acquirer were calculated. To test Hypothesis 2, the interactions of the information asymmetry measures and post WTO entry were calculated. The variables, except for the dummies, were centered before being modeled.

Results

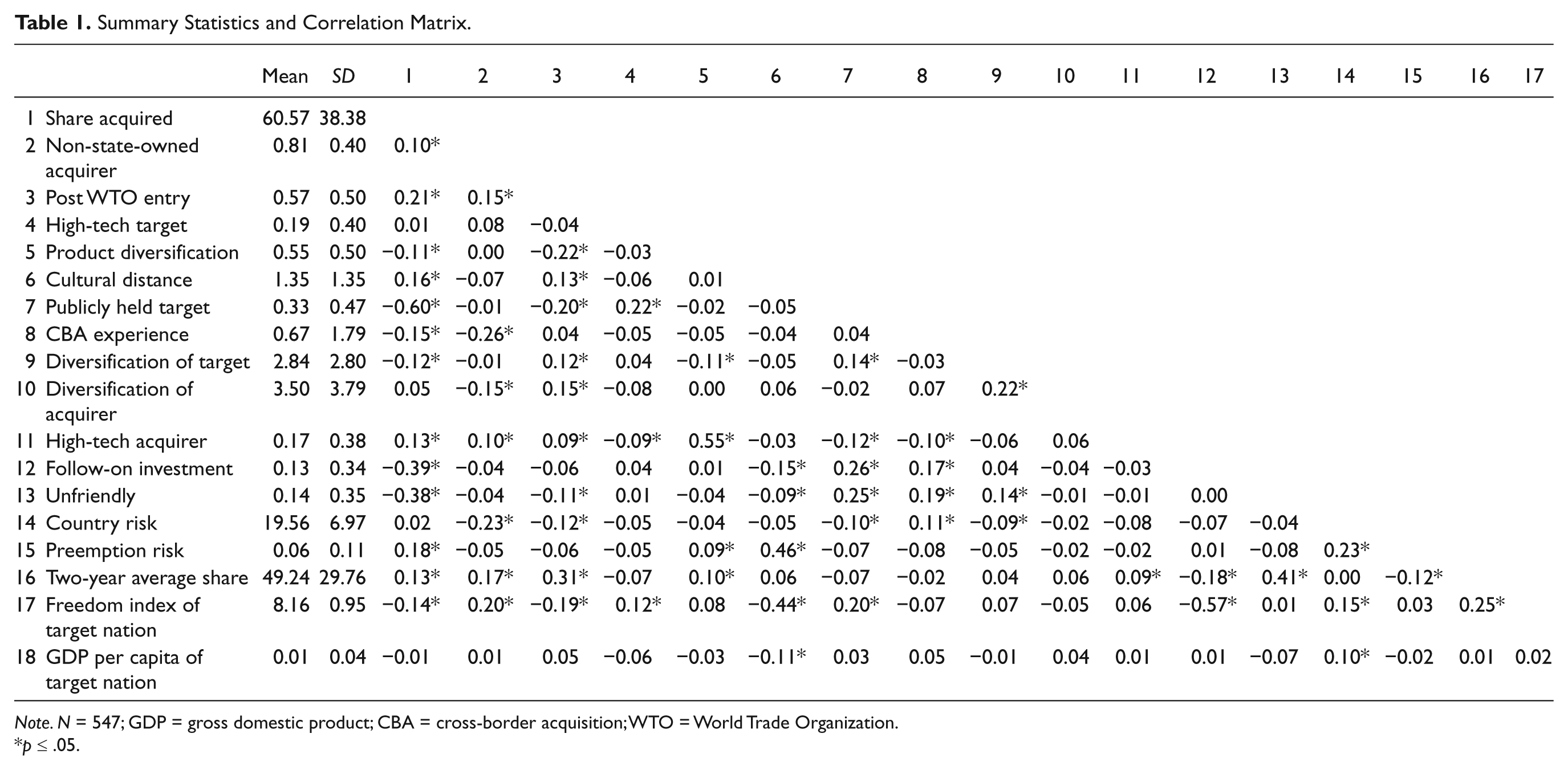

Table 1 shows the summary statistics and the correlation matrix of the variables. No strong intercorrelation is evident among the explanatory variables.

Summary Statistics and Correlation Matrix.

Note. N = 547; GDP = gross domestic product; CBA = cross-border acquisition; WTO = World Trade Organization.

p ≤ .05.

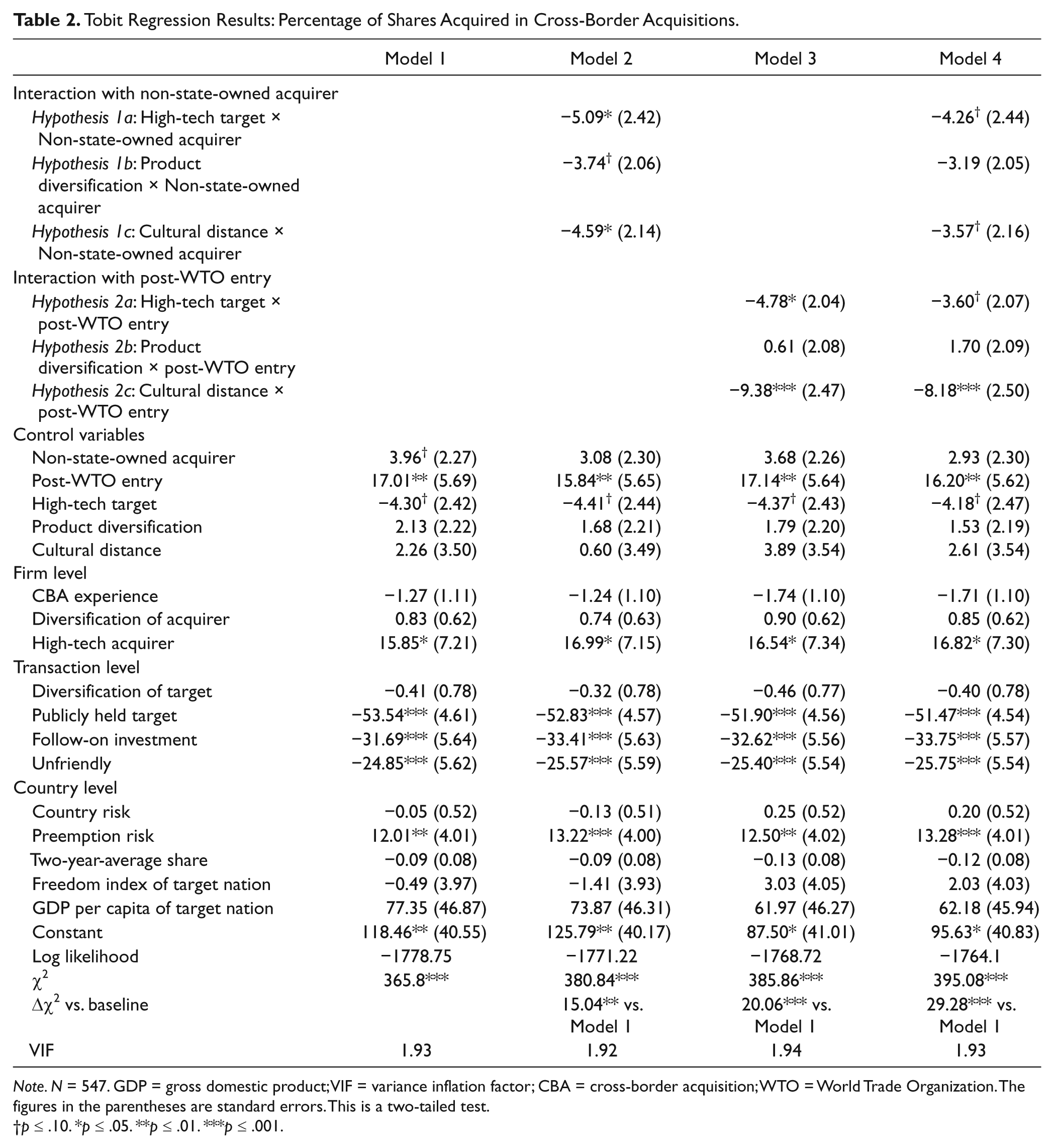

Table 2 reports the Tobit regression results predicting ownership share of CBAs. Model 1 serves as the baseline with control variables. Model 2 is used to test Hypothesis 1. Model 3 is used to test Hypothesis 2. Model 4 is the full model. Interaction items were added into the models subsequently. The Δχ2 values indicate that the predictive power of the models improved significantly as each group of variables was added.

Tobit Regression Results: Percentage of Shares Acquired in Cross-Border Acquisitions.

Note. N = 547. GDP = gross domestic product; VIF = variance inflation factor; CBA = cross-border acquisition; WTO = World Trade Organization. The figures in the parentheses are standard errors. This is a two-tailed test.

p ≤ .10. *p ≤ .05. **p ≤ .01. ***p ≤ .001.

Hypotheses 1a to 1c predict that compared with state-owned acquirers, acquirers with other ownership structures are more likely to respond to the information asymmetries at the firm-, industry-, and country-levels. For this idea to be supported, the coefficients of the interaction items would need to be negative and significant. This is largely what was found in Model 2. The interaction effect of high-tech target and non-state-owned acquirer was negative and significant (p < .05). The interaction effect of product diversification and non-state-owned acquirer was negative and marginally significant (p < .10), and the interaction effect of cultural distance and non-state-owned acquirer was negative and significant (p < .05). Overall, all the three subhypotheses of Hypothesis 1 found some degree of support in the results.

Hypotheses 2a to 2c predict that compared with the period 1987-2001, the Chinese acquirers were more likely to respond to the information asymmetry in the period 2002-2007. For this hypothesis to be supported, the coefficients of the interaction items would need to be negative and significant. This is largely what was found in Model 3. The interaction effect of high-tech target and post WTO entry was negative and significant (p < .05). The interaction effect of cultural distance and post WTO entry was also negative and significant (p < .001). However, the interaction effect of product diversification and post WTO entry was not significant. Overall, two of the three subhypotheses of Hypothesis 2 received support in the results.

Model 4 included all the interaction effects. The interactions increased the explanatory power relative to Model 1 (Δχ2 = 29.28, p < .001), Model 2 (Δχ2 = 14.24, p < .01), and Model 3 (Δχ2 = 9.22, p < .05). Previously reported results more or less continued to hold with some reduced level of significance, which may be attributed to some multicollinearity in the full model.

In addition to the interaction effects with information asymmetries, post WTO entry had a significant and positive direct effect (p < .01) on ownership shares purchased by Chinese acquirers in CBAs. Among the firm-level control variables, high-tech acquirer had a significantly positive effect as expected. Three of the transaction-level control variables were highly significant in all models. The negative effect of publicly held target showed that although the information asymmetry involved with private targets is an important concern of acquirers, the financial resource constraint faced by Chinese acquirers when they tried to purchase publicly held targets has a larger impact on their entry mode choice. The effects of unfriendly and follow-on investment were significant (p < .001) and negative as expected. Among the country-level control variables, preemption risk is the only one with significant effect. As expected, its effect on ownership shares acquired in CBAs was positive.

Finally, to test if ownership increments are more important across certain thresholds, ordered logistic regression (Chari & Chang, 2009) was also applied to the data. Following the methods of Pan (2002), the values of the dependent variable were classified into four categories: below 50%, 50%, greater than 50% but below 100%, and 100%. The results from the Tobit and ordered logistic regressions were largely similar, which showed the robustness of our findings. The ordered logistic regression results are not reported in detail but are available on request from the authors.

Discussion

Contributions of the Study

This study was designed to investigate how different types of new multinational firms from emerging economies such as China respond to information asymmetry in their international acquisition strategies, and how these entry decisions are influenced by home institutions. The results suggest that the institutional framework in emerging economies such as China can challenge some of the basic assumptions underlying the economic perspectives and influences the entry mode strategies of firms from such societies in their international expansion.

The research showed that state-owned acquirers tended to pay less attention to (a) firm-level information asymmetry when acquiring high-tech targets, (b) industry-level information asymmetry occurring in diversifying CBA, and (c) country-level information asymmetry caused by cultural distance between the host country and China. Failure to respond to information asymmetry in the way suggested by the economic perspectives may indicate poor economic efficiency. This tends to confirm that Chinese SOEs are not fully designed or required to pursue commercial profit maximization. WTO entry and other institutional changes in China seem to have increased the market selection forces of competition. This significantly changed the behaviors of Chinese acquirers, who appear to have become more alert to information asymmetry and started to cope with them by adopting the entry modes more aligned with the suggestions of economic perspectives.

The current study contributes to the research on international entry mode strategies from both the economic and institutional perspectives. Extensive empirical research taking economic perspectives showed mixed findings on the effect of economic determinants on entry mode choices (e.g., Cuypers & Martin, 2010; Erramilli, 1991). The national origin of foreign investors was found to play a significant role in explaining the mixed findings (Hennart & Larimo, 2004; Makino & Neupert, 2000; Zhao, Luo, & Suh, 2004). However, the mechanisms through which the national origin of foreign investors influences the effectiveness of economic determinants have not been fully explored (Zhao et al., 2004). Our research suggests that the home institutions, such as state ownership and home institutional changes, can be one of the key mechanisms through which the national origin of foreign investors influences the effectiveness of economic determinants of entry mode choice (Zhao et al., 2004).

This article also extends the research on the effect of institutional logics and institutional change. We show how investors from an emerging economy with multiple institutional logics and substantial institutional change make ownership-based entry mode choices and how these choices change with market transition over time. Institutional logics are “taken-for-granted social prescriptions that guide actors’ behavior in fields of activity” (Battilana & Dorado, 2010, p. 1419). Private sector firms and SOEs tend to hold different institutional logics, leading to their different responsiveness to economic determinants. The effects of institutional change after China’s entry into WTO on their ownership-based entry mode choices in CBAs suggest the importance of considering the evolution of the institutional logics held by Chinese acquirers.

Strengths and Limitations

In addition to industry conditions and firm-specific resources as suggested by economic perspectives, institutions were suggested to be “a third leg for a strategy tripod” (Peng et al., 2009, p. 63). Instead of taking institutional factors as “background,” we found that the institutional conditions and transitions strongly influence firms’ strategic decisions via changing firms’ incentives and challenging some of the basic assumptions underlying the economic perspectives. By considering both the economic and institutional perspectives, this article extended the strategy research on emerging economy firms.

In addition, we have examined two dimensions of institutional factors: one static and the other dynamic. State ownership might describe a static dimension of China’s institutions, but entry into WTO captures a more dynamic aspect of the institutional transition. Both dimensions moderate the relationships between economic determinants and ownership-based entry mode choice of Chinese acquirers. This implies that whether or not Chinese acquirers respond to economic drivers, and how they respond to them, tend to vary across different ownership structures and evolve over time.

Because of data limitations, this study did not incorporate other types of economic determinants apart from information asymmetry. Also because of data limitations, some potentially influential variables could not be included in the models. The size of the Chinese investors and their motivation to get involved in CBAs are prominent examples. In addition, since we relied mainly on the second-hand data, we were not able to examine how institutional factors influence the microdynamics of the decision-making process of CBAs by Chinese firms.

Directions for Future Research

The global financial crisis in the past few years has provided an opportunity for cash-rich Chinese firms to expand to international markets by acquiring overseas firms and assets. This trend has been shown clearly with an increasing number of CBAs by Chinese firms, with supportive government policies encouraging and guiding them to “go global.” Over time, this will provide a good opportunity for further theory development and testing of new hypotheses, particularly, those related to the effects of government policies and political institutions. The generalizability of the key findings of this study for Chinese CBAs also needs to be tested with firms from other emerging economies.

Practical Implications

Our research also provides implications to public policy makers and managers. For public policy makers, it addresses the specificity of SOEs and shows that active integration into the global market increases the importance of economic drivers in firms’ foreign investment decisions. Government policy makers should thus make their policies more market-friendly to promote the economic efficiency and international competitiveness of their firms. For example, following the examples of Japan and South Korea, the Chinese government aimed to bring up groups of large SOEs to form the pillars of the national economy and to enhance their international competitiveness (Zeng & Wang, 2002-2004). The Chinese government launched the “going abroad” policy in 2000 to promote the international expansion of Chinese firms, especially large SOEs. The government has since issued various kinds of policies and incentives for support and guidance in their global expansion (Zeng & Wang, 2002-2004).

Our findings also suggest that managers who deal with investors from emerging markets should keep in mind that state ownership may influence investors’ strategic decisions, which should be tracked over time as home institutions of emerging economies experience significant changes. The state-owned Chinese firms might be less profit-driven than their counterparts in private sectors, but they are becoming more and more alike in recent years.

Conclusion

Rapid economic growth in emerging economies over the past three decades has drawn scholars’ attention to FDI outward from such economies (Buckley et al., 2007; Lau & Bruton, 2008; Li, 2011; Luo & Tung, 2007; Morck, Yeung, & Zhao, 2008; Yiu et al., 2007). This study has been a response to Lau and Bruton’s (2008) call for a micro-level empirical study of outward FDI from emerging economies. By examining the Chinese acquirers’ ownership-based entry mode choices in CBAs, we found that although state ownership tends to reduce Chinese firms’ responsiveness to economic factors (i.e., information asymmetry at the firm-, industry-, and country-levels) as suggested by the economic perspectives, the institutional transition taking place in China in recent years has increased such responsiveness of Chinese acquirers.

Footnotes

Acknowledgements

We would like to thank the coeditors of this special issue, Gregory Dess, Mike Peng, and David Lei for their invitation and guidance in the article development process and thank Haibin Yang and Steve Sauerwald for providing detailed comments and suggestions for improving the article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.