Abstract

On1 23 August 2019, the Finance Minister of India declared and cleared the way for the merger2 of 10 public sector banks into four large public sector banks (PSBs). In pursuance thereof, the Oriental Bank of Commerce (OBC) merged into Punjab National Bank (PNB). OBC held a 23% stake in Canara HSBC OBC Life Insurance Co. Ltd. (CHOIC), whereas PNB itself held a 30% stake in PNB MetLife India Insurance Co. Ltd. (PMLI) (Outlook, 2020). Thus, post-merger, PNB had two insurance businesses. Mr Mallikarjuna Rao, Managing Director & CEO, PNB, was in a fix on whether to continue with a 23% stake in Canara HSBC OBC Life Insurance or discard them. He wondered whether the two competing businesses would augur well for PNB. Should he not get out of Canara HSBC OBC Life Insurance and concentrate on PNB MetLife India Insurance or vice versa? How much cash could he raise through this disposal? Would it be right for him to dispose immediately or wait for a better valuation?3 These questions were circling in his mind. He knew that whatever decision he took, his focus had to be on improving Punjab National Bank’s profitability.

Discussion Questions

Discuss the internal and external business environment of Punjab National Bank (PNB).

Analyse and predict the growth of the life insurance industry in the coming years. Evaluate how it will complement the banking business.

Draw a competitive map of both PNB’s banking and insurance business.

Perform business-wise and integrated SWOT analysis.

Advise Mr Rao on business and corporate strategy.

In the case of PNB, OBC and United Bank merger, while PNB has a 30 per cent stake in PNB MetLife India, OBC has a 23 per cent stake in Canara HSBC Oriental Bank of Commerce Life Insurance. Since both life insurance companies cannot exist under the combined entity post-merger—one of the banks, likely OBC, will have to offload its investment in its insurance company.

—Business Line, 19 September 2019

Journey of the Indian Banking Industry and Punjab National Bank

The Reserve Bank of India, the country’s central banking authority, was established in April 1935, but it was nationalized on 1 January 1949, under the terms of the Reserve Bank of India (Transfer to Public Ownership) Act, 1948 (RBI, n.d.). Post-independence, the government decided to nationalize Indian banks until 1980. However, in 1990 with the liberalization of the economy, new tech-savvy banks were licensed to serve the growing Indian population. Indian banking industry consisted of 27 public sector banks, 21 private sector banks, 49 foreign banks, 56 regional rural banks, 1,562 urban cooperative banks and 94,384 rural cooperative banks. Public sector banks accounted for 61.21% of the total banking assets in FY19. In FY19, the total asset in the public and private banking sector was US$1,422.97 bn and US$741.79 bn, respectively (BFSI, 2020). Investment, apart from loans and advances, generated income for banks. In modern banking, apart from other traditional income sources, third-party product distribution earned substantial income for the banks.

One big player in the Indian banking sector was Punjab National Bank. Punjab National bank began its operations in Lahore on 19 May 1894. The board was created from different parts of India, professing different faiths and varied backgrounds. However, the common objective was to create a national bank for the citizens of the country. The bank started with an authorized capital of US$2,703, and the working capital was US$270. PNB initially had nine employees with a total monthly salary of US$4.33. At the end of 30 June 2020, PNB was India’s second-largest public sector bank. Global business increased by 2.7% year on year to US$243 billion at the end of June 2020 from US$236 billion in June 2019. The bank continued to maintain its forte in the low-cost current account and savings account (CASA) deposits with a share of 43.45%. The bank’s focus had always been on qualitative business growth, recovery and arresting fresh slippages (Punjab National Bank, 2020).

The bank had over 180 million customers, 10,910 branches and 13,000+ ATMs (Automated Teller Machine) post-merger with United Bank of India and Oriental Bank of Commerce, effective from 1 April 2020 (Punjab National Bank, 2020). The bank had created a large customer base with total revenue of US$112.25 billion as on 1 April 2020. The bank had over 100,000 employees and earned revenue through its CASA, lending and cross-selling other financial products like mutual funds, forex, life insurance and non-life insurance. PNB also followed the strategy that most of the private banks adopted, that is, to have insurance and a mutual fund joint venture so that its fee-based income could be increased through the joint ventures and the income made manifold through earning commissions (selling products of joint venture companies) as well as through profit earning as a shareholder.

For PNB, the road post-merger in the banking system was not smooth as it had to look for alternate income through cross-selling, especially insurance. Post second quarter of FY21, due to the government’s decision to grant a moratorium on the loans, its income reduced, thereby widening the bank’s income and expenditure gap. While the bank’s gross NPA ratio fell marginally to 13.4% in September FY21 compared to 14.1% in June FY21, it was mainly due to the asset quality standstill benefit (vide Supreme Court’s order). 4 While asset quality was a concern for all banks, for PNB, there were other concerns. On the one hand, both merged entities PNB and OBC had high NPA load. On the other, the exposure to stressed sectors made the situation more complicated. PNB was exposed to sectors like metal, telecom, agriculture, energy, and so on, which made its operations more prone to NPA creation (Merwin, 2020).

Life Insurance Industry and Global Life Insurance Business

The business of life insurance started in the early eighteenth century when insurance policies were introduced. 5 The first company to offer life insurance was the Amicable Society for a Perpetual Assurance Office, founded in London in 1706 by William Talbot and Sir Thomas Allen (Anzovin, 2000). In the 1750s mathematical models were established to calculate the premium for any insurance policy. In the United States of America, life insurance started in the late 1760s. Between 1787 to 1837, more than two dozen life insurance companies started, but fewer than half a dozen survived. In India, 1818 saw the advent of the life insurance business through Oriental Life Insurance Company Limited (IRDAI, 2020a). Over time, other insurance companies started business in India. The government of India, in 1914, started publishing returns of insurance companies. After independence, on 19 January 1956, an ordinance was passed to nationalize the life insurance business, and thus, the Life Insurance Corporation of India came into existence (IRDAI, 2020a).

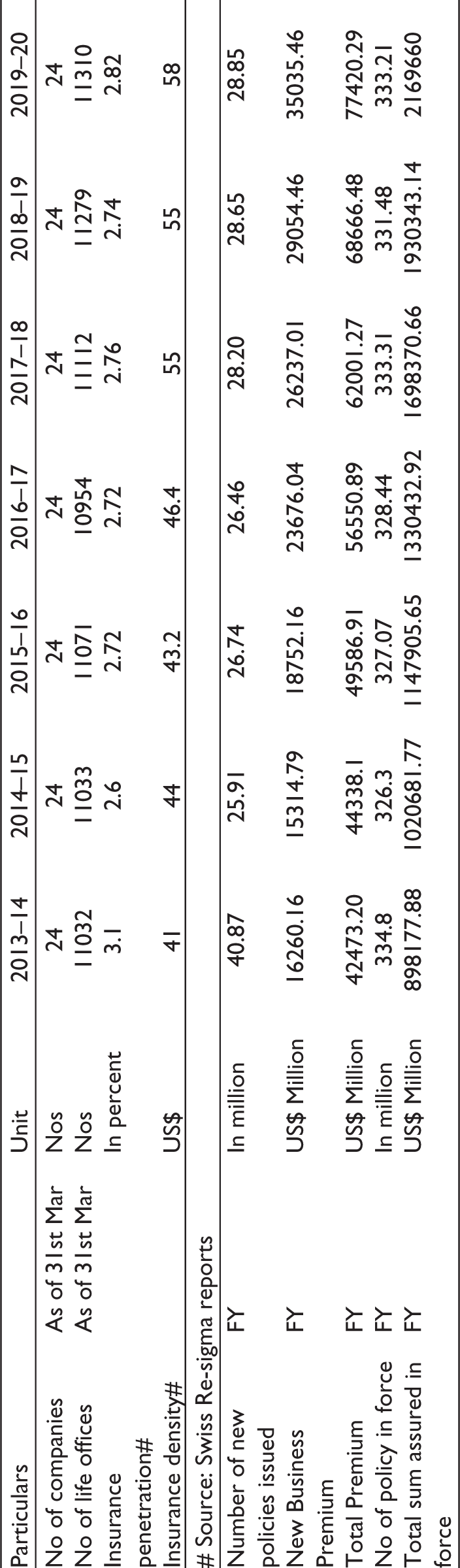

The global life insurance provider market was US$2,951 billion in 2018, expected to grow to US$3,586.96 billion by 2022 at a compounded annual growth rate (CAGR) of 5%. In 2018, the largest region for life insurance providers was North America, followed by Asia Pacific (AP NEWS, 2019). The rise of disposable income in emerging countries like India and China drove the life insurance market. The economic growth in middle-income families translated into high disposable income had increased and drove the investment in life insurance and hence was the main reason for the growth in the life insurance industry (Anand, 2019). The lack of knowledge regarding life insurance worked as a restraint to the growth of the life insurance provider market. Many people across the world still invested in traditional ways. The lack of knowledge on how life insurance worked in creating a huge monetary corpus for an individual which could financially support at the time of financial crunch had been the greatest stumbling block. Life insurance gave benefits not only in the case of death but also maturity benefits (Anand, 2019). Life insurance, across the world, helped individuals by providing post-retirement benefits. Hence globally, it had been slowly accepted as an important investment tool. This acceptance impacted the insurance market in emerging countries. The Swiss Re Institute 6 report mentioned that the world’s largest emerging countries contributed 42% of global life insurance growth while China contributed 27%. The insurance market dashboard is given in Table 1.

Global Insurance Market Dashboard 2020/2021.

Indian Life Insurance Business

The insurance business in India was regulated, the regulator being Insurance Regulatory and Development Authority (IRDA). Malhotra committee recommended regulating the insurance industry through an autonomous body in pursuance of which the IRDA was constituted in 2000. Globally, in 2018, the share of the life insurance business was 54.30% of the total premium collected, whereas, in India, the share of the life insurance premium collected was 73.85%. India ranked 10th in the world in the life insurance market as per the data provided by Swiss Re, its share being 2.62% of the global market. 7 An overview of the Indian insurance business is given in Table 2, while the share of premiums between life and non-life insurance is given in Table 3. The life insurance market grew by 10.75% in FY19 (ETBFSI, 2019). Thus, it could be easily understood that the life insurance industry was not just an emerging business but a sunrise industry in India. The psychology of Indian customers and their understanding of life insurance had improved manifold with the COVID-19 outbreak in 2020 (PTI, 2020a). Life insurance companies sold policies through two major channels in India. The first being the agency model, where the agents licensed by IRDA sold insurance policies of an insurance company and earned a commission. The second channel included Bancassurance (selling insurance to bank customers through banks), where the banks sold the policies to bank customers and earned a commission. Due to the amalgamation of PSU banks, there was an impact on life insurance companies, especially where PSU banks were a shareholder. This would change the business dynamics in the coming years. Banks, as a shareholder of a life insurance company, generated dual income; one as commission by selling policies and the other through dividends distributed by the life insurance company. 8 It was worth noting that IRDA failed to take the policy-level decision due to the merger of banks, making them hold the ownership of two or more insurance companies. Hence, such banks, especially PNB, could hold ownership of more than one life insurance company in the absence of any policy directive from IRDA (PTI, 2019).

Indian life insurance industry update.

Life and Non-life Insurance Market—Total Real Premium Growth Rate 2018.

The Two Competing Life Insurance Companies: PNB MetLife India Insurance Company Limited (PMLI) and Canara HSBC Oriental Bank of Commerce Life Insurance Company Limited (CHOIC)

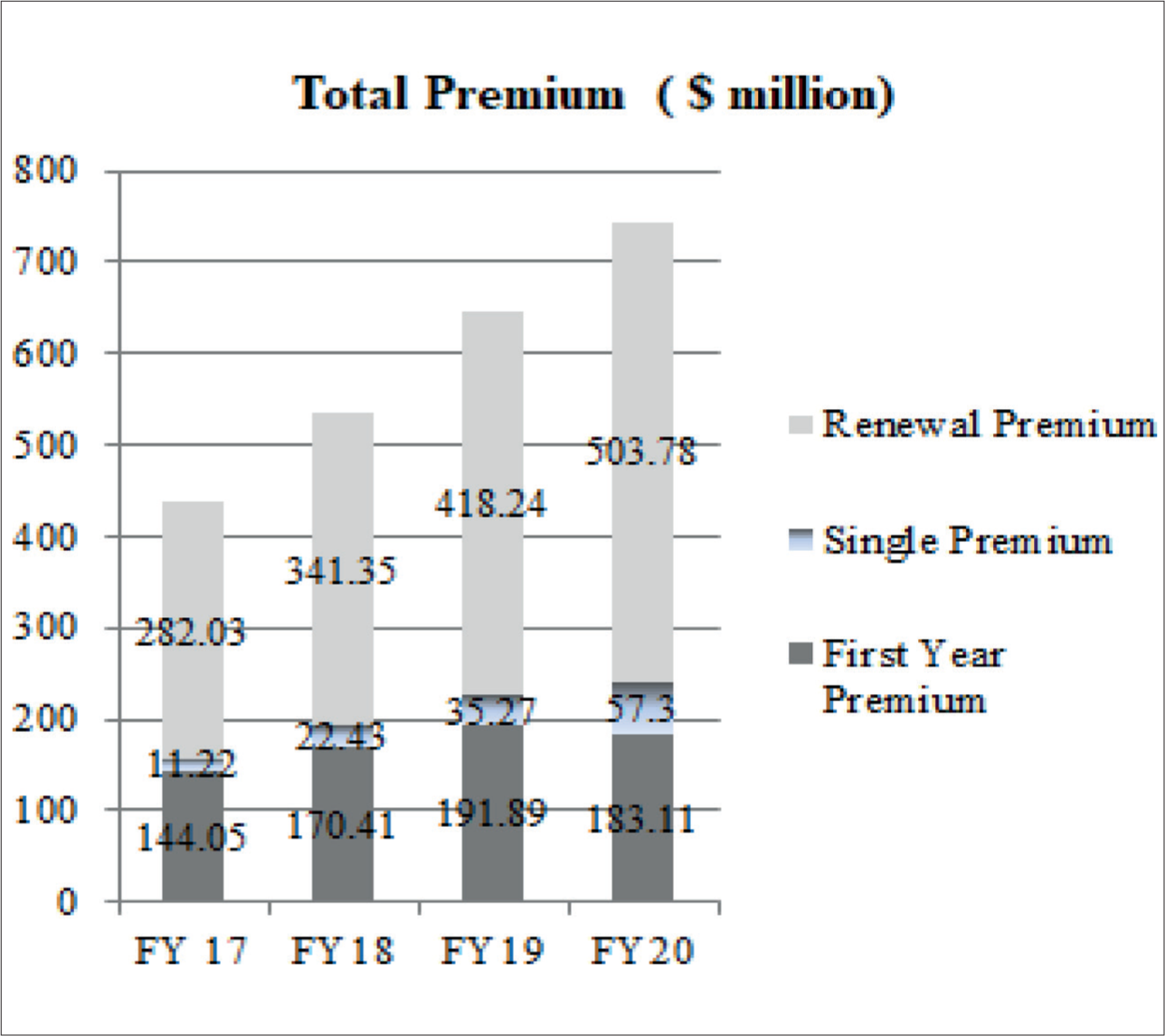

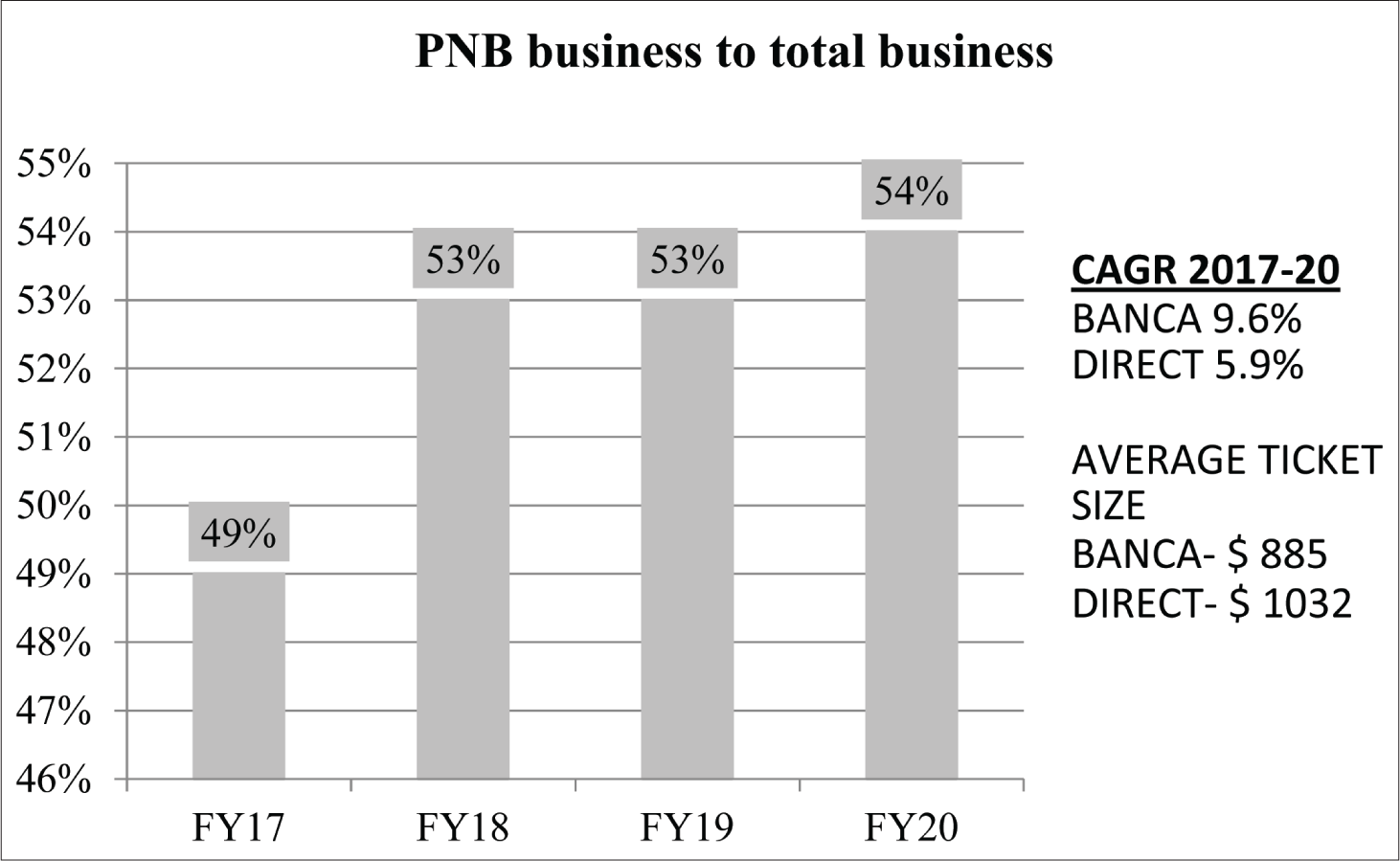

PNB MetLife India Insurance, a joint venture between Punjab National Bank and MetLife International Holding LLC, was India’s leading life insurance company. Apart from these two, J&K bank, M Palonji & Company Private Limited and other private investors were its shareholders. The shareholding pattern is shown in Table 4. PMLI was present in 107 locations across India with access to over 100 million customers and more than 11,000 locations through its strong bank partnership with PNB, J&K bank, Karnataka Bank and other bank partners. 9 The company, which started in 2001, projected a compounded annual growth rate of 11%–13% in the coming few years. Table 5 provides the performance highlights of PMLI for FY19–20. The company introduced innovative products and created new distribution channels for deeper market penetration. The company used Bancassurance (sales through partner bank) and agency models (sales through agents). It focused on new business premium growth for which it used thrust engines like digitization, insurance awareness and customer awareness. The premium had been growing yearly (Figures 1 & 2). The company was present widely in eastern, northern and western India through PNB bank partner. In the south, it had a limited presence through its other channel partners.

PNB MetLife India Insurance Co. Ltd—Shareholding Pattern.

PNB MetLife India Insurance Co. Ltd—Business Statistics.

PMLI, over the last few years, had improved its ranking and was among the country’s top 10 private life insurance companies as per IRDA annual report for the FY20. Though the operating expense had increased, the efficiency, too, had increased; the administration expense came down from 23.5% to 17.1% of the total premium in the last four years from 2017–2020 (PNB MetLife, 2020). The company was able to source business basis customer needs which could be seen in its first-year renewal, which had increased from 72% to 80% in the last four years from 2017–2020. It had emerged as a strong brand in the life insurance industry based on its knowledge acquired from MetLife International and PNB’s large customer reach. The compounded annual growth rate of 16% in new business and 19% in total premium was due to deeper customer penetration (PNB MetLife, 2020). Though the company had increased its business and grown fast, PNB, as a channel partner, could not make the most of it, which was reflected in the low commission income growth. Even the dividend pay-out had not started considering PMLI yet to wipe off all accumulated losses (Part of PNB balance sheet, Table 6).

PNB MetLife India Insurance Company—Profit.

PMLI was looking at the dilution of equity up to 25% through the issue and the IPO that could raise around US$378.38 million, valuing the company at US$1,486.49 million as of March 2019 (Saraswathy, 2019). Initially, it planned to roll out the IPO in the second quarter of FY20, but the plan was deferred due to COVID-19. Meanwhile, PNB and OBC bank merged, and the scenario changed. PNB’s income from commissions from PMLI was approximately US$24.32 million. PNB did not earn a dividend yet from PMLI. PMLI could not completely wipe off all accumulated losses even after FY20 profit of US$12.57 million and still had an accumulated loss of US$94.86 million as per the balance sheet of FY20.

PMLI offered all types of life insurance basis customers’ needs. The company had different term plans that could be sold online or through different channel partners. Term plans provided only death benefits and were available at a low premium. The company launched a few new products, including traditional endowment plans that served the purpose of investment with life coverage. The company gave customers an option to invest in unit-linked investment insurance plans and retirement solutions to its customers. The company not only covered individual life but also had employee benefit schemes for employees of different organizations. As of February 2021, the company website highlighted 16 savings products, 13 protection products, 5 pension products, and 8 optional riders.

While PNB MetLife was doing well, Canara HSBC Life was giving tough competition. Canara HSBC Oriental Bank of Commerce Life Insurance Company Limited (CHOIC) was one of India’s top 12 private life insurance companies. It was established in 2008. CHOIC was a joint venture (JV) between Canara bank and HSBC Insurance (Asia-Pacific) Holdings Limited, and Punjab National Bank, too, had become a JV partner post-merger of Oriental Bank. Table 7 shows the shareholding pattern as per the annual report 2019–2020. Canara bank was the largest shareholder of the insurance company, with 51% ownership. The insurance company operated with 40 branches and additionally sold and serviced customers through more than 20,000+ bank branches within its bank partners. The company thrived on value behaviours like customer centricity, agility, accountability, collaboration, empowerment, and respect. 11 CHOIC had been rapidly growing in the insurance sector with the support of one of the top 5 public sector banks—Canara Bank and Punjab National Bank (Bansal, 2021). The company started its business in 2008 and quickly reached the top tenth position in private life insurance companies in May 2019 (Srivats, 2019). The growth was fast, and the profit generated by the company for the shareholder was nearly US$15 million, which was growing year by year represented in Table 8. It posted a discrete break-even in FY13 and, since then, posted continuous profits. The company wiped off all earlier losses and became a profit centre for its shareholders. The company had a considerable market throughout India as OBC was mainly dominant in northern and eastern India, and Canara bank was dominant in southern and western India.

Canara HSBC OBC Life Insurance Co. Ltd.—Shareholding Pattern.

Canara HSBC OBC Life Insurance Co. Ltd.—Profit Update.

Mr Anuj Mathur, MD & CEO, during an interview with Business Line (Srivats, 2020), said, ‘The company is eyeing 99% claim settlement ratio for individual business in FY20–21’.

He also mentioned that the company’s total premium collection increased steadily and reached US$532.84 million, as shown in Table 9 and would increase steadily with new product addition based on customer requirements. The approximate valuation of the company in November 2018 was US$878.38 million (Mascarenhas, 2018). CHOIC had access to sell insurance in OBC and PNB branches after the merger. It was worth noting that Syndicate bank had merged with Canara bank; hence, the insurance company could sell insurance in the Syndicate bank branches in addition to existing Canara bank branches. As it may, Mathur was confident about CHOIC digitizing its operations to become more competitive and provide better customer service; it had already initiated digital sales for its bank customers. OBC’s income from CHOIC through commission was approximately US$8.65 million in FY19 with 2,300 branches and US$11.35 million in FY20, yet to be disclosed in the annual report. 12 CHOIC wiped off all its accumulated losses in FY19 and could declare a dividend from FY20 profit of US$14.19 million and years going forward.

Canara HSBC OBC Life Insurance Co. Ltd.—Business Statistics.

CHOIC provided a wide range of life insurance plans catering to customers’ financial needs like investment and protection requirements. The plans were tailor-made as per the different life stages of individuals. The plans could be purchased online or from banks or different distributor partners. There were endowment plans which gave guaranteed returns, and some of the plans invested customer money in the financial market and provided returns on market valuation. Some plans were specially created for employees of organizations and affinity groups. The company held 4 term plans, 2 unit linked insurance plans, 4 traditional savings plans, 1 health plan, and 2 retirement plans, as mentioned on the company website in February 2021. Aside from those, the company held 2 group benefit plans also. Available insurance plans for customers per the insurance regulatory and development authority website were more than 30 in February 2021.

PNB and OBC Merger

The intention and objective of the government for the amalgamation of public sector banks were mainly to unlock the banks’ potential and create the NextG (next generation) banking system in the country. Further, the government wanted to build scale to reposition PSBs in the contemplated US$5 trillion economy. This was expected to result in an increased risk appetite of the bank and bring operational efficiency with high lending capacity at low cost. The amalgamation of PNB, OBC, and United bank of India (UBI) created the second largest PSB entity in the country with approximately 11,000 branches, 100,000 employees and a business of US$243.24 billion. 13 For Mr Rao, it would be an income and a strategic decision. There were two important decisions PNB had to make. Considering the amalgamation and the future promise to create a robust bank structure, the first question was whether PNB would like to continue its venture into the life insurance industry. The second was whether to be there as an owner in the life insurance companies or be with one and sell the shares of the second company and generate instant wealth.

Post-merger Scenario

Post-merger, PNB had declared a profit of US$41.62 million even if the provision for bad loans doubled due to the merger. While PNB declared profit, the profit plunged 70% compared to last year’s period. The operating profit of the bank grew 2.5% YOY basis to US$713.51 million. The overall NPA of the bank fell to 14.11% from 16.49% in comparison to the same period last financial year (PTI, 2020b). The bank was focused on amalgamation processes, including system integration of all three banks. While there were challenges, since all three merging banks worked on different geographies, PNB was confident that the integration would be completed fully by March 2020. To smoothen the merger process, RBI selected all three banks basis on their IT compatibilities instead of geographic reach. All three banks used ‘Financle’ software by Infosys; hence, it was easy to integrate IT systems within a year. Harmonizing human resources would be one challenge considering the bank’s working culture and that all three banks had employees with diverse backgrounds (The Economic Time, 2020).

Competition Benchmarking

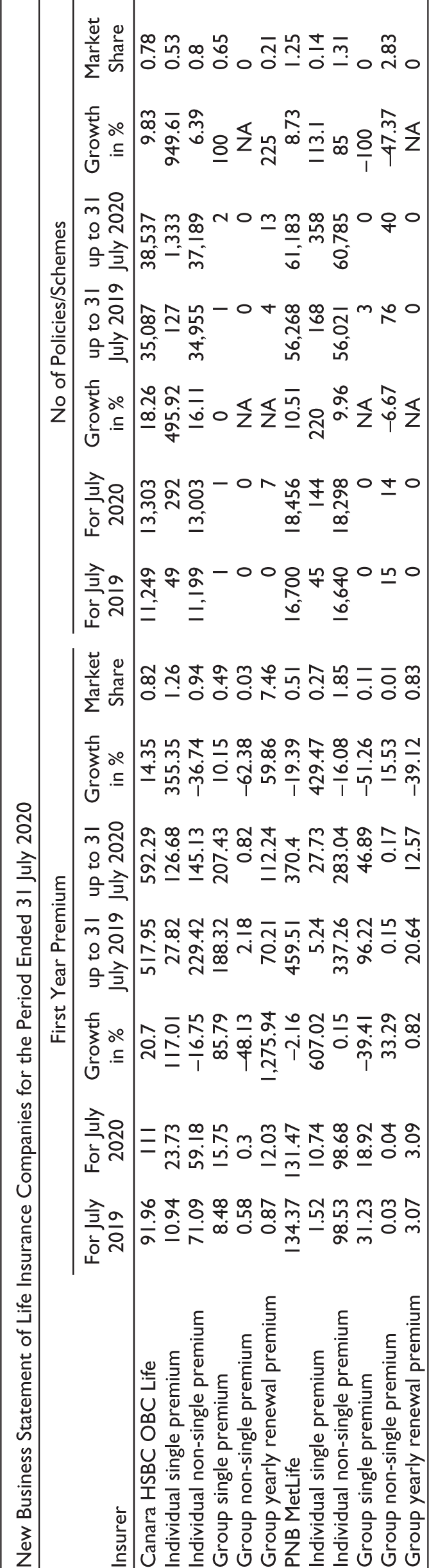

Based on the IRDA business update in July 2020, we could observe the following business update for top life insurance companies, where it was evident that both PMLI and CHOIC were emerging as significant players in the private life insurance space, as shown in Table 10. The choice of option would depend not only on the productivity of the insurance companies but also on the return on investment. For PNB, Canara HSBC OBC Life Insurance Company was profit-generating, while PNB MetLife India Insurance Company was still running at a loss. Here the argument would be on the future delivery of both companies. Also, to evaluate if the post-merger of Punjab National Bank and Canara Bank would shape up its banking business. The quick stability in the banking business could add more business for the life insurance companies and, hence, more profitability.

Life Insurance Business in India: An Overview.

By 2025 Indian banking system would emerge as one of the strongest financial machineries in the world of finance. The emphasis would be on emerging technology supported by new bank models supported by non-traditional alliances, one of which would be a partnership with a non-core business like life insurance. Hence, both these alliances of PNB could be a big profit centre for the bank. However, the real challenge would be to take a quick and thought-through decision to execute this with maximum efficiency and at the right time. Bancassurance was growing fast for the following reasons: it encouraged banks’ customers to purchase insurance policies and further helped build better relationships with the bank. The people who were unaware of and/or were not within reach of insurance policies could benefit through widely distributed banking networks and better marketing channels of banks. An increase in the number of providers meant increased competition; hence, people should expect better premium rates and better services from bank insurance compared to traditional insurance companies. 14 The future looked promising for the life insurance industry with several changes in the regulatory framework, which would lead to further changes in how the industry conducted its business and engaged with its customers. The overall insurance industry was expected to reach US$280 billion by 2020. The life insurance industry in the country was expected to increase by 14%–15% annually in the coming few years. 15

Demographic factors such as the growing middle class, young insurable population and growing awareness of the need for protection and retirement planning would support the growth of Indian life insurance.

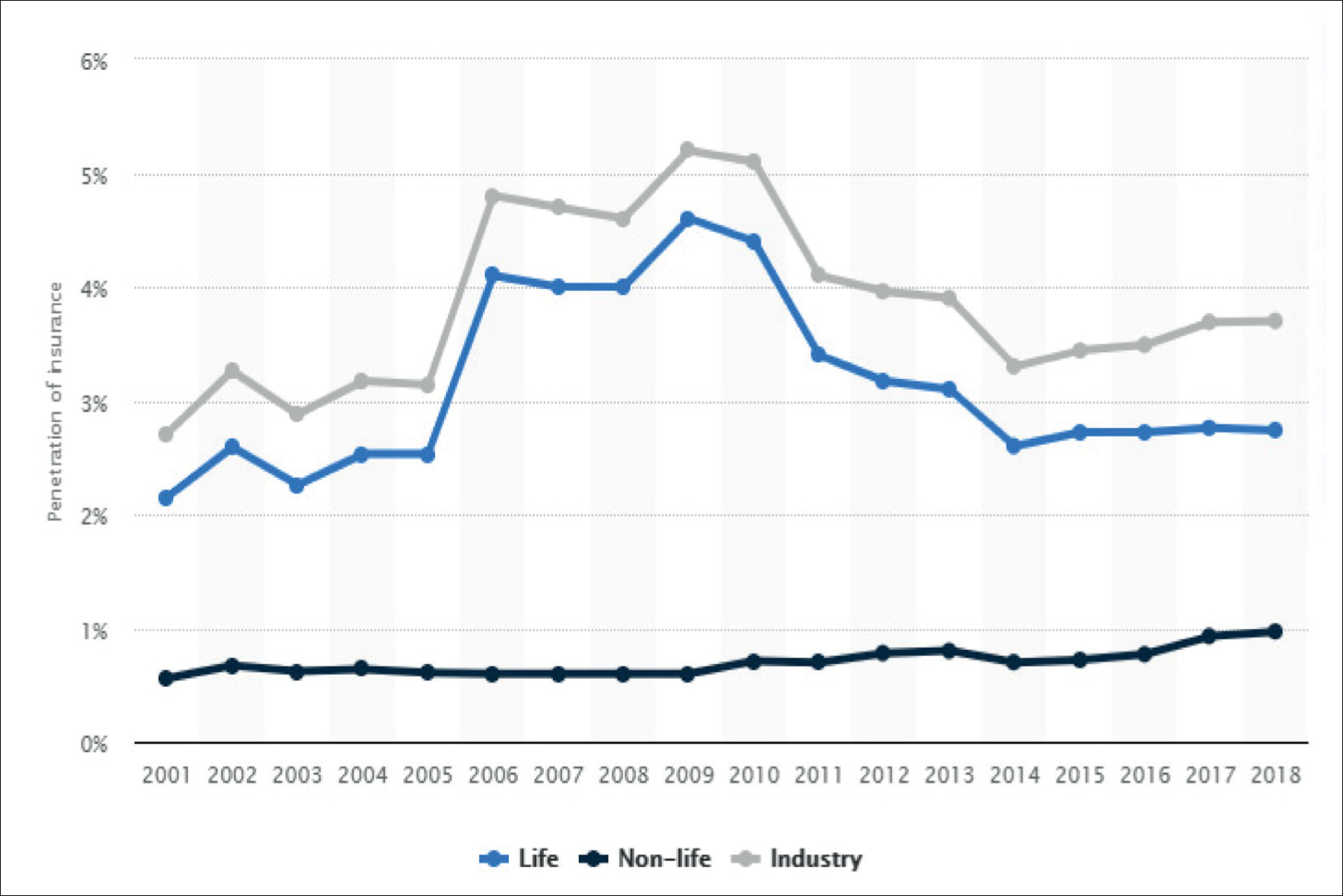

While mainstream revenue was important for an organization and a bank, fee-based income life insurance gave additional corpus to support the company’s financials. This was an important source of earnings for a bank, especially for a PSU bank, considering a higher tendency of NPA for the core business. In such a scenario, Mr Mallikarjuna Rao, MD & CEO of PNB, needed to decide the best possible utilization of investment PNB had done over a period of time in these two life insurance companies. With an insurance penetration of less than 5% in the country, this could become a profitable investment in the future (Statista, 2020). PNB, post amalgamation and consolidation, could concentrate on the insurance business and earn significant revenue adding stability to the balance sheet. The detail of insurance penetration in India is shown in Figure 3.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.