Abstract

The purpose of this study is to construct a historical narrative of the development of the standard-setting in Japan, where the main standard-setting bodies were changed from public to private sector entities. This study specifically examines the unique coexistence of four sets of accounting standards through the lens of legality. My findings show that four sets of accounting standards are formalized into the domestic legal system through the endorsement by the Financial Services Agency of Japan, although differences in the standard-setting processes and patterns of public delegation exist. This finding also suggests an interesting example of hybridization between legally incomplete ex ante delegation to private sector standard-setting bodies and ex post endorsement by the public sector.

Introduction

Today, financial reporting standards are developed by private standard-setters in many jurisdictions. Moreover, since the early first decade of the 2000s, many countries have adopted International Financial Reporting Standards (IFRS), 1 defined by the International Accounting Standards Board (IASB), a private sector international standard setter (Camfferman and Zeff, 2007, 2015). As these private sector bodies lack a democratic foundation by nature, the legitimacy of standards and/or standard-setting activity is often subject to debate (e.g. Botzem, 2012; Büthe and Mattli, 2011; Fleckner, 2008; Perry and Nölke, 2005). However, the legalization of accounting standards, one of the fundamental aspects of the legitimacy issue, is rarely discussed.

In traditional comparative and classification studies in international accounting (e.g. Doupnik and Salter, 1995; Gray, 1988; Nobes, 1983), a dichotomy, based on the existence of code-law countries (Franco-German group) and common-law countries (Anglo-Saxon group), has commonly been adopted. While financial reporting rules are part of the formal laws (e.g. commercial code (CC)) and regulate accounting practices in code-law countries, private sector standard-setting bodies set accounting standards in common law countries. Such entities mainly consist of accounting professionals, and play a relatively independent role in the legal system of these countries (Tokuga, 2000). In other words, accounting professionals develop accounting rules with legal backing from company laws and securities laws. Gray (1988) describes the former as “statutory control” and the latter as “professional control.” Some studies suggest that this theoretical framework may have a sufficient explanatory power in the era of IFRS (Nobes, 2006, 2011; Nobes and Stadler, 2013).

These circumstances give rise to the following question motivating this study: what kind of impact does the global harmonization of accounting standards and the institutional change from the public sector to private sector standard-setting bodies bring to the legal backing of accounting standards? This question is particularly relevant to former code-law countries, where public sector standard-setting bodies set the accounting standards, while “statutory control” is performed through written laws. In Japan, which is assumed to be a code-law country in most previous studies, the Accounting Standards Board of Japan (ASBJ), a private sector organization, began issuing accounting standards in 2001. However, many researchers pointed out the unclearness or uncertainty of the formal authority and legal basis of the ASBJ and its standards. Later, the situation changed, and the legal foundation of the ASBJ standards was clarified in 2009, 2 when the decision to permit the voluntary application of IFRS in Japan was taken. In addition, more recently, Japan has authorized the use of four accounting standards: Japanese GAAP, US GAAP, IFRS, and Japan’s Modified International Standards (JMIS) by listed companies in Japan for their consolidated financial statements. Therefore, Japan represents a unique case wherein four sets of accounting standards coexist.

To provide insights into the above motivating question, 3 this study develops the following research questions:

Why has a private sector organization been issuing accounting standards since 2001 in Japan?

Why has the legalization of ASBJ standards changed since 2009?

What kinds of legal backing are provided for the coexisting four sets of consolidated accounting standards in Japan?

To answer these questions, this study constructs a historical narrative of the development of standard-setting in Japan. This study specifically examines the unique experience of the coexistence of four sets of accounting standards through the lens of the legal backing for accounting standard-setting. Thus, the study conducts a thorough and comprehensive review of the setting bodies, purpose, characteristics, circumstances of implementation, number of adopted firms, and legal backing in Japan. Inspired by extant studies, two benchmarks of ex ante delegation and ex post endorsement are used for as a basis for comparison or reference frame to assess the situation in Japan. The first reason why this study focuses on Japan is the uniqueness that four sets of accounting standards are permitted for consolidated financial statements of listed companies. Second, this study examines changes in the legal backing for accounting standards in Japan, once being perceived as a code-law country, to provide insights on countries other than the United States and European countries. I believe that research needs to expand its focus to Asian and African countries and other emerging economies with similar backgrounds.

My findings confirm that, in Japan, four sets of accounting standards are commonly formalized into the domestic legal system through ex post endorsement by the public sector, although differences in the standard-setting processes and public delegations exist. Japan is an interesting example of hybridization between legally incomplete ex ante delegation to the private sector standard-setting bodies and ex post endorsement by the public sector; in other words, the country allows the hybridization between “statutory control” and “professional control.” The historical narratives described in this study suggest that the change in the legalization of ASBJ standards has taken placed in the context of the voluntary adoption of IFRS and this change, paradoxically, suggests the need to strengthen the role of the state.

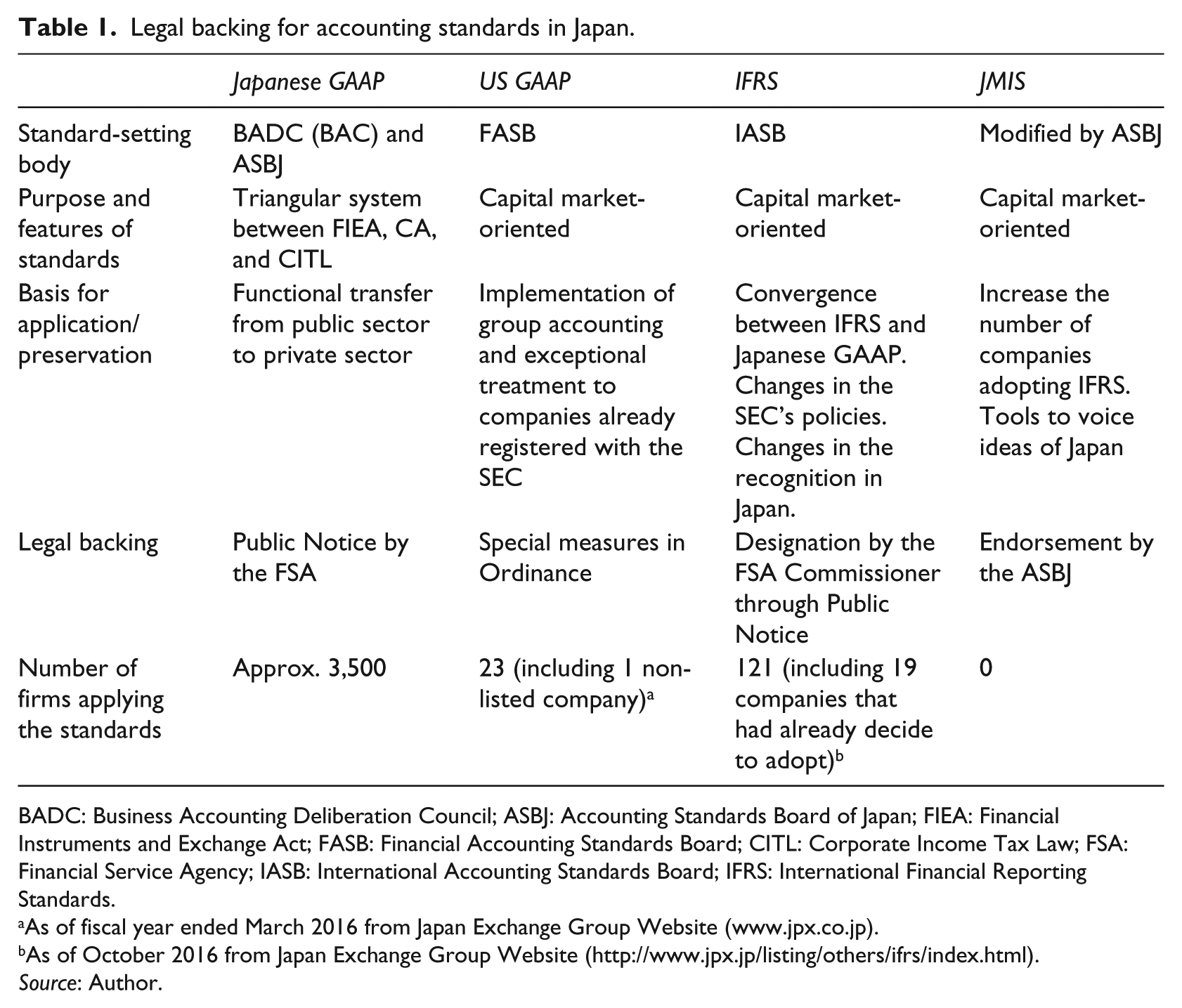

Legal backing for accounting standards in Japan.

BADC: Business Accounting Deliberation Council; ASBJ: Accounting Standards Board of Japan; FIEA: Financial Instruments and Exchange Act; FASB: Financial Accounting Standards Board; CITL: Corporate Income Tax Law; FSA: Financial Service Agency; IASB: International Accounting Standards Board; IFRS: International Financial Reporting Standards.

As of fiscal year ended March 2016 from Japan Exchange Group Website (www.jpx.co.jp).

As of October 2016 from Japan Exchange Group Website (http://www.jpx.jp/listing/others/ifrs/index.html).

Source: Author.

This study contributes to the existing literature in several ways. First, there are limited publications on the accounting history of Japan, especially from the 2000s. Introducing Japan’s unique phenomenon of the coexistence of four sets of accounting standards and demonstrating the legal backing (and the change thereof) of such standards, this study contributes toward creating new knowledge that specifically addresses international readers. Second, the legitimacy studies focusing on the legalization of accounting standards are limited. Demonstrating a country-specific hybridization of the legal basis of accounting standards, this study fills the gap in the existing literature and provides new empirical insights to the legitimacy of accounting standard-setting.

The remainder of this article is organized as follows. The section “Prior studies” reviews prior studies and identifies the research gap in the extent literature. The section “Two benchmark” proposes two benchmarks used as a basis for comparison to assess the situation in Japan, and the section “Methodology” discusses the methodology. In the section “Financial reporting in Japan,” the study reviews the historical development of accounting regulation in Japan and constructs a historical narrative of the unique experience of the coexistence of four sets of accounting standards through the lens of the legal backing for accounting standard-setting. In the last section, I discuss the theoretical implications of this study.

Prior studies

The legitimacy of accounting standards set by private-sector organizations

Both in transnational and domestic levels, the privatization of regulation has become visible and private sector bodies have become principal actors in standard-setting in a variety of areas, especially in accounting (Büthe and Mattli, 2011; Tamm Hallström, 2004). However, these private sector bodies lack democratic legitimacy in nature (Richardson and Eberlein, 2011); therefore, the legitimacy of accounting standards/standard-setting bodies has been assessed by many researchers.

Institutional theorists have made a significant contribution to the discussion on legitimacy (e.g., Scott, 2014; Suchman, 1995). They focus on symbolic systems in society, such as rules, norms, and cultural-cognitive beliefs, and suggest the three most important pillars of institutions: regulative systems, normative systems, and cultural-cognitive systems (Scott, 2014). These three components also provide the bases of legitimacy, as follows: The regulatory emphasis is on conformity to rules: Legitimate organizations are those established by and operating in accordance with relevant legal or quasi-legal requirements. A normative conception stresses a deeper, moral base for internalized than are regulative controls, and the incentives for conformity are hence likely to include intrinsic as well as extrinsic rewards. A cultural-cognitive view points to the legitimacy that comes from conforming to a common definition of the situation, frame of reference, or a recognizable role (for individuals) or structural templates (for organizations). (Scott, 2014: 74)

To define legitimacy, Scott (1995) emphasizes its evaluative dimension and suggests that “legitimacy is not a commodity to be possessed or exchanged but a condition reflecting cultural alignment, normative support, or consonance with relevant rules or laws” (p. 45). On the other hand, Suchman (1995) indicates that “legitimacy is a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions” (p. 574). He emphasizes both the evaluative and cognitive dimensions of legitimacy and the role of the social audience.

Although its importance in the institutional theory, 4 the regulative aspects of legitimacy, how accounting standards and accounting standard-setting bodies are formalized into legal systems, are seldom discussed in previous studies in accounting.

In prior studies before 2000, the common elements of the legitimacy 5 of accounting standards/standard-setting bodies have been identified as, sufficient authority, independence, expertise, and due process. Johnson and Solomons (1984: 172), one of the early studies on the legitimacy of private accounting standard-setters, proposed three conditions essential to the legitimacy of the Financial Accounting Standards Board (FASB): Sufficient authority, substantive due process, and procedural due process. Sufficient authority means that an accounting standard-setting body or process received a clear mandate of authority from the Congress or the Securities and Exchange Commission (SEC), and has the competence to carry out the assigned function. Substantive due process means that an accounting standard-setting body or process meets this criterion if it adequately justifies each exercise of authority and provides an adequate rationale for each decision. Finally, procedural due process means that all interested parties are given a reasonable and timely opportunity to be heard and provided with a reasonable opportunity to influence the rule-making process. Wahlen et al. (1999: 445–446) also suggested a few desirable characteristics of a global financial reporting standard-setter (i.e. requirements for the legitimacy of a global accounting standard-setter): independence, accountability, expertise, representativeness, due process, alignment of authority and responsibility, sufficient resources, and operationality.

Together with sufficient authority, many recent studies suggest an interdependent relationship between public and private sector organizations is a requirement to the legitimacy of accounting standard-setters (e.g. Bratton, 2006; Perry and Nölke, 2005; Richardson, 2009; Zimmerman et al., 2008). 6 Zimmermann et al. (2008) suggest a mixed governance model in which standard setting by the private sector and regulation and enforcements by the public sector co-exist, as it has been adopted in the European Union (EU). The authors introduce two principles to explain the legitimacy of this model: (1) participation and public debate (deliberation) and (2) control and accountability. Perry and Nölke (2005) also argue that public authorities delegating accounting standard setting to the IASB were not consciously choosing fair value accounting; rather, they were adopting an institutional structure that left technical decisions to experts. Their systematic network analysis of the governance structure of the IASB and the European Financial Reporting Advisory Group (EFRAG) reveals that the delegation of authority to experts is characterized by a shift of responsibility from the public to the private sector.

As this discussion shows, for private sector accounting standards to keep their status and their enforcement power, legitimacy, especially their legal backing and relationship with public sector bodies is critical. This study focuses on the legal basis of accounting standards and standard-setting bodies, and investigates the Japanese case in particular.

Two benchmarks

To assess specific features of accounting standards and accounting regulation in a given country, one requires a benchmark to clarify the differences and similarities with other countries (Ramanna, 2015). Traditional comparative studies in international accounting have regarded the United States as a representative example for common-law countries and most EU member states, such as France and Germany, as a benchmark for code-law countries. After 2002, the EU has required their listed companies to use IFRS for their consolidated accounts.

Therefore, this study adopts the accounting system in the United States (US GAAP) and that for consolidated statements in Europe (IFRS) as two benchmarks to analyze the legal backing of Japanese accounting standards. There are three reasons why I refer to these two systems: US GAAP and IFRS are used internationally, both regions have the world’s leading capital markets, and prior studies always compare these two systems as representative examples (Botzem, 2012, 2014; Botzem and Quark, 2009; Dewing and Russell, 2008; Martinez-Diaz, 2005; Mattli and Büthe, 2005; Posner, 2010; Ramanna, 2013). For instance, Büthe and Mattli (2011) suggest as follows: In accounting, the United States has a single, well-established, and uncontested private-sector standard-setting organization, which produces accounting rules for the large U.S. financial market … The institutional structure in Europe, by contrast, is characterized by high levels of fragmentation and contestation at the national and regional levels. (p. 79)

Ex ante delegation: the USA case

In the United States, the Congress delegates its authority to set accounting standards to the SEC, under the Security Act of 1933 and the Security Exchange Act of 1934 (Büthe, 2010; Büthe and Mattli, 2011; Cunningham, 2005; Doron, 2016; Previts and Merino, 1998; Zeff, 2003). In 1938, the SEC issued the Accounting Series Release No. 4 (ASR No. 4) and formally adopted a policy of recognizing accounting principles created by professional accountancy bodies 7 as generally accepted accounting principles (GAAP), for which substantial authoritative support existed. Cunningham (2005) argued, “AICPA bodies were the primary providers of such support through 1973, and continued to provide supplemental authority after that year” (p. 28).

However, as a result of the growing criticism on these bodies, the FASB, a body whose members were selected according to their particular knowledge and interest in financial reporting was established in 1973. 8 At the same time, the SEC issued the ASR No. 150 and recognized that the FASB had substantial authoritative support and its standards were establishing authoritative GAAP. In addition, the SEC reaffirmed the status of the FASB as a designated private sector standard-setter when the Sarbanes-Oxley Act came into force, in July 2002 (US SEC, 2003). The SEC again delegates its authority to the FASB under Section 108 (d) of the Sarbanes-Oxley Act and the ASR No. 150. 9

In sum, FASB standards secure their legal backing through “ex ante delegation of public regulatory authority to private bodies” (Büthe and Mattli, 2011: 204), and “give authority unless the Security and Exchange Commission intervenes” (Fleckner, 2008: 291, Italic original). In that sense, the FASB is the legitimated standard-setting body in the United States and their standards are regarded as legitimated standards. Thus, FASB standards do not need ex post approval from a public office or legislation. Now, US issuers are only permitted to use US GAAP for their consolidated accounts.

Ex post endorsement: the EU case

In July 2002, the EU issued the IAS Regulation, in which required EU-listed companies to apply IAS/IFRS for their consolidated accounts, from 1 January 2005 (Regulation (EC) No. 1606/2002). However, the EU does not automatically accept IASB standards, but decides on their acceptance through an endorsement process to each accounting standard. This endorsement process is conducted by two organizations: EFRAG and the Accounting Regulatory Committee (ARC). First, the private sector EFRAG discusses and advises from a technical perspective. The next steps involve a consulting by the public sector ARC on the results of those initial assessments, from a political standpoint (Bischof and Daske, 2016; Botzem, 2015; Büthe and Mattli, 2011; Walton, 2015).

Therefore, the EU does not entirely delegate its authority to set standards to the IASB, but it introduces an endorsement mechanism to assess whether IFRS meet the EU requirements. In other words, IFRS have “no authority unless the European Commission expressly adopts them” (Fleckner, 2008: 291, Italic original). This endorsement mechanism in the EU has both political and legitimacy implications. Regarding the political impact of the endorsement process, Dewing and Russell (2008) indicate the EU’s concerns on the US hegemony in global accounting standard setting and explain it as follows: … from the EU’s perspective the endorsement of international accounting standards achieved both the explicit objectives of harmonizing accounting in the EU, such that a single set of standards was recognized for cross-border listings and also the implicit objective of negating US hegemony in accounting when the only realistic alternatives to international standards was the adoption of US standards over which the EU has little or no influence. (p. 246)

With regards to the legitimacy of the IASB, Ramanna (2013) points out that, since its foundation, the IASB has been legitimized by the EU to embrace IFRS and the modifications to such standards, after bowing to political pressure from the EU suggesting that “preserving the EU’s reliance on IFRS is an important source of legitimacy for the IASB” (p. 2).

In sum, the IAS Regulation requires EU-listed companies to apply IFRS for their consolidated accounts with legally binding power. In other words, the IAS Regulation provides the source of legitimacy to IFRS. In that sense, the EU delegates the development of standards to the IASB. However, this does not necessarily suggest that the IASB possesses full authority for accounting regulation in the EU. The EU applies a later endorsement procedure for each IFRS standard. In other words, IASB standards secure their legal backing through “ex post endorsement” (Büthe and Mattli, 2011: 204) in the EU. However, in the case of accounting standards for individual financial statements, member states have the option to require or allow the use of IFRS (IFRS Foundation, 2016).

Methodology

Research setting

As investigation of the legal backing for accounting standards/standard-setting, this study focuses on the four sets of accounting standards used by listed companies for their consolidated financial statements in Japan since the 2000s.

Data collection and analysis

To construct a historical narrative of the development of the legal basis of accounting standards in Japan, this study uses official reports, discussion documents and related responses, and a range of additional information available on the ASBJ web page and other resources. 10 It also reviews the extant academic studies.

Financial reporting in Japan

Institutional background: the Japanese legal and financial reporting systems

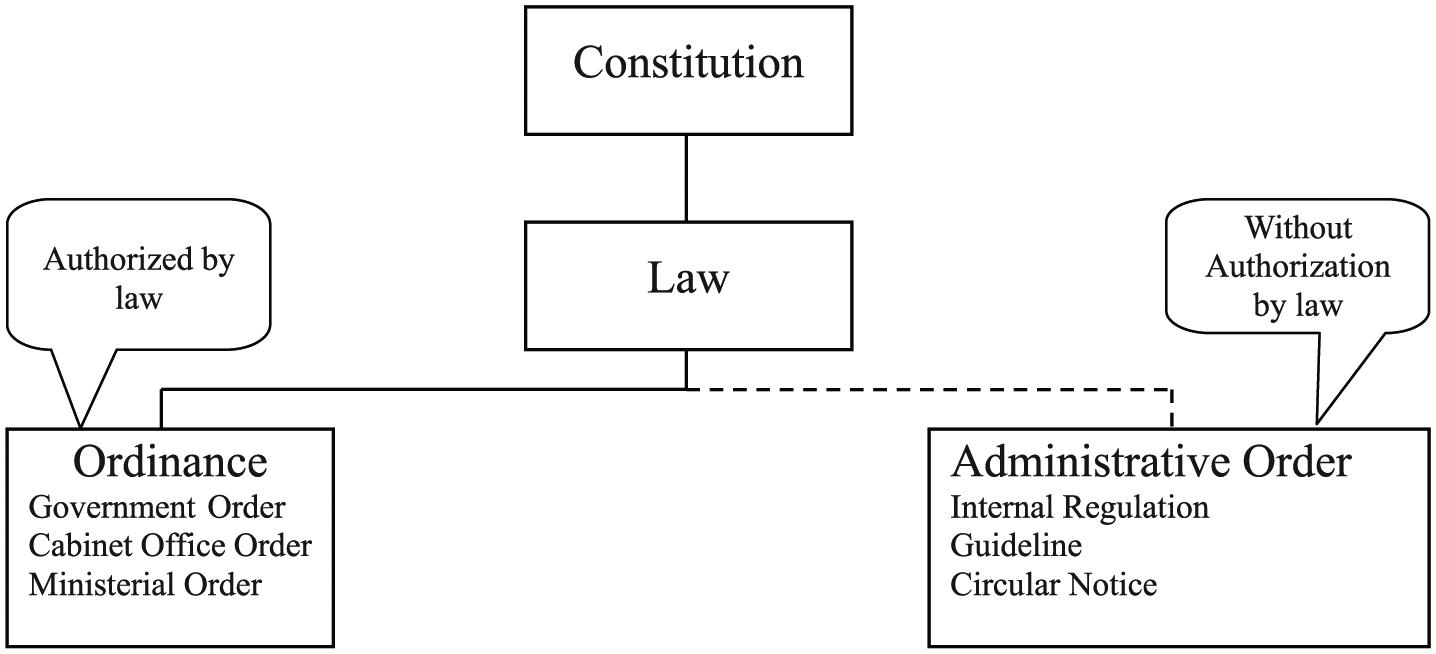

Statute law and codified law, as the written law set down by a legislature body, are distinguished from unwritten law, such as common law and precedents in any countries. The structure of statute law in Japan is arranged in a hierarchical manner as shown in Figure 1, with the Constitution as the fundamental law, laws enacted by the Diet, and ordinances set by administrative agencies of the government (e.g. Government Order, Cabinet Office Order, and Ministerial Order). To secure enforcement power, ordinances require authorization by law. Administrative legislation or administrative law in Japan includes Administrative Orders (e.g. Internal Regulation, Guideline, Circular Notice). However, administrative orders set by administrative bodies, typically, are not regarded as statute law due to their lack of authorization by law. In other words, laws and ordinances are supposed to be enforceable as statutory rules, but administrative orders only set administrative procedures within the bureaucracy and are not binding for the general public.

Classification of administrative legislation in Japan.

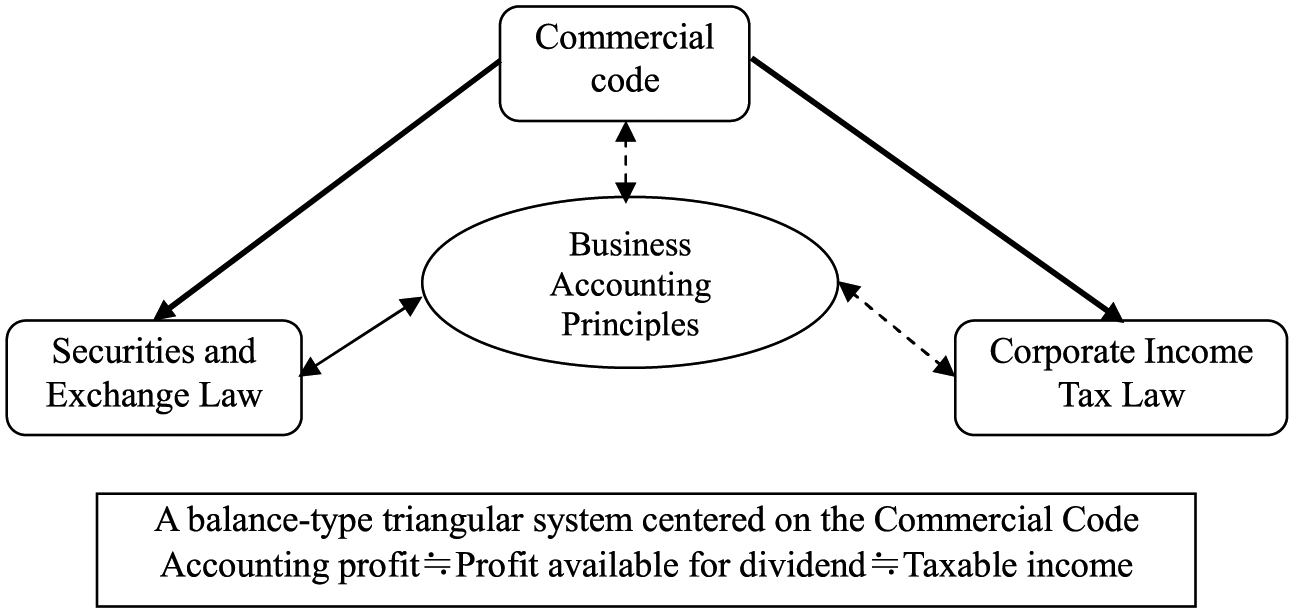

After the Second World War, the so-called triangular, three-code legal system, consisted of the CC, the Securities and Exchange Law (SEL), and the Corporate Income Tax Law (CITL), 11 which constituted “a fairly detailed statutory foundation for disclosure under Japanese generally accepted accounting principles (GAAP)” (Benston et al., 2006: 167). In this triangular system, the accounting profit calculated under SEL, the profit available for dividend calculated under CC, and the taxable income calculated under CITL are nearly equal in Japan, unlike in the United States and the United Kingdom, where these accounting numbers are different in principle (see Figure 2).

The triangular, three-code legal system (before 2006).

The Business Accounting Deliberation Council (BADC), an advisory body of the Ministry of Finance (at that time), deliberated on issues of corporate accounting at the request of the Minister. In that sense, the BADC had been the de facto standard-setter in Japan. 12 Initially, the BADC released their accounting standards in the form of Opinions of the Committee with no legal backing. 13

Under the triangular system, the Japanese GAAP, including basic principles, accounting standards, interpretation, and implementation guidance (issued by the Japanese Institute of Certified Public Accountants, JICPA), must be consistent with the three laws (CC, SEL, and CITL) and cannot override them (Benston et al., 2006: 167). Although the BADC, a quasi-public sector standard-setting body, has been the main pillar of this system, the BADC was not active in producing standards, guidance, and interpretations; however, “it spent much time reconciling various accounting requirements of the Codes” (Benston et al., 2006: 167–168).

The consolidated accounting system introduced in Japan was based on the Opinion on the Establishment of the System of Consolidated Financial Statements, released by the BADC in June 1975, and Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements (Ordinance of the Ministry of Finance No. 28 of 1976), released in October 1976 (Endo et al., 2015: 146–150; Kawamoto, 2001: 335–336). At this time, the 39 Japanese firms, that had already registered with the SEC and prepared their consolidated financial statements under US GAAP, were permitted to use US GAAP also in Japan under Paragraph 2 of the Supplementary Provisions of the Ordinance as an extraordinary measure. 14

The ASBJ

In 1996, the Japanese governments launched the so-called “Financial Big Bang” to deregulate and liberalize the financial sector (Ito and Melvin, 1999). 15 After the burst of the bubble economy in 1991, the country experienced a protracted recession, a substantial amount of non-performing loans held by Japanese banks and their successive collapse, the Asian monetary crisis, and political scandals regarding the Ministry of Japan. This reform aimed to revitalize the Japanese economy by making the Japanese financial market more efficient and internationalized. Moreover, the quality of financial statements of some Asian countries received harsh criticism from the United Nations and the World Bank at the time of the Asian financial crisis. The Big Five accounting firms required that the legend clause 16 had to be included in notes or audit reports of financial statements of some Asian countries, including Japan (Endo et al., 2015: 283; Kimura and Ogawa, 2007: 225). Therefore, together with the financial reform, an accounting reform (the “accounting Big Bang”) to improve the quality of Japanese accounting standards was an urgent matter.

Along with this reformation and responding to the pressure for the accounting harmonization of Japanese GAAP with international accounting standards (i.e. US GAAP and IAS/IFRS), 17 the Financial Accounting Standards Foundation (FASF), the founding body of the ASBJ, was created in July 2001. It promptly established the ASBJ 18 and Japanese accounting standards were considerably revised. These revisions addressed accounting standards for consolidated financial statements, retirement benefits, tax effect accounting, financial instruments, impairment of assets, and business combinations (Koga and Rimmel, 2007: 223). The main features of this reform were a shift in emphasis from individual accounting to consolidated accounting, and the harmonization of international accounting standards and Japanese GAAP.

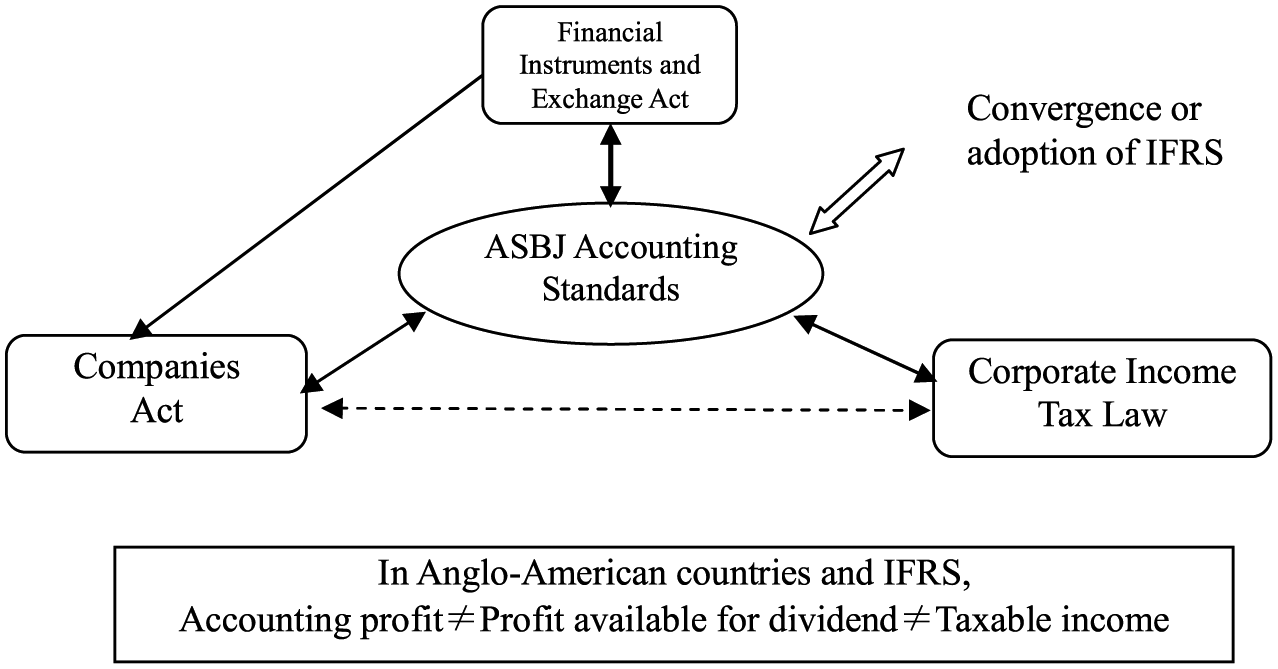

The “accounting Big Bang” also facilitated changes in the legal system: one of which was the legal change from the CC to the Company Act (CA) in 2006, and the other was the shift from the SEL to the Financial Instruments and Exchange Act (FIEA), also in 2006 (see Figure 3). In contrast with the provisions in the CC, the CA delegates the accounting regulations of listed and unlisted public companies to the FIEA except for the calculation of the profit available for dividend. Thus, the calculation of retained earnings is relatively independent of that of accounting profit. Moreover, the relationship between the three laws, insofar as public companies are concerned, has become loosely coupled (Tokuga, 2012: 123).

The current-triangular system (after 2006).

In these circumstances, Article 193 of the FIEA (Terms, Forms, and Preparation Methods of Financial Statements) established the legal basis of accounting standards as follows: The balance sheet, profit and loss statement and other statements of finance and accounting to be submitted under the provisions of this Act shall be prepared in conformity with the terms, forms and preparation methods which the Prime Minister prescribes in a Cabinet Office Ordinance in accordance with the manner generally accepted fair and proper (article 193).

Based on this provision, the Cabinet Office Ordinance No. 49 Ordinance on Terminology, Forms, and Preparation Methods of Financial Statements 19 declared that “terminology, forms, and preparation methods of financial statements … shall be in compliance with business accounting standards that are generally accepted as fair and appropriate” (Article 1 (1)) and “business accounting standards published by the Business Accounting Council … shall be regarded as the business accounting standards that are generally accepted as fair and appropriate” (Article 1 (2)). Similarly, Article 231 of the CA establishes that the accounting for a stock company shall be subject to the business accounting practices generally accepted as fair and appropriate. At the same time, the Ordinance of the Ministry of Justice requires that the interpretation of the terminologies and the implementation of the requirements of this ordinance shall be subject to business accounting standards and practices that are generally accepted as fair and appropriate (Article 3).

According to these provisions, the Financial Service Agency (FSA) originally possessed the accounting standard setting authority in Japan, and this authority was delegated to the BADC (public sector) by the Cabinet Order for Organization of the FSA, not to the ASBJ (private sector). Regarding the legal status of accounting standards, the ASBJ standards become statutory rules only by reference in the “Tsutatsu” (Circular Notice) Guidelines for Ordinance on Terminology, Forms, and Preparation Methods of Financial Statements. This was the status of the legal system of accounting standard setting and regulation in Japan before 2009. Therefore, many researchers underlined the ambiguity and uncertainty of the formal authority and legal basis of the ASBJ (e.g. Benston et al., 2006; Chiba, 2012; Oishi, 2007; Sato, 2004). 20

The Interim Report 2009

In addition to concerns or criticism about the vulnerable legal status of its accounting standards, the ASBJ had been facing the pressure to accelerate convergence with IFRS. Initially, the ASBJ took a “cautious convergence approach” (Tsunogaya and Tokuga, 2015: 299). However, the “Tokyo Agreement” with the IASB and the ASBJ in United States, 2007 had changed the atmosphere, 21 and the situation turned remarkably when the Business Accounting Council (BAC, renamed from BADC, only in English from 2009) approved its Opinion on the Application of International Financial Reporting Standards (IFRS) in Japan (Interim Report) (the Interim Report: BAC, 2009) on 30 June 2009. At the same time, the FSA published 13 related documents including: (1) a proposal for the revision of Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements; 22 (2) a proposal for the revision of Guidelines for Ordinance on Terminology, Forms, and Preparation Methods of Financial Statements; and (3) a “Kinyucho-Kokuji” proposal (Public Notice by the FSA).

The acceleration of the possible application of IFRS in the United States played out in the background of this drastic change. Although the United States had a leading role in the international accounting standard-setting arena from the outset of the International Accounting Standards Committee (IASC), accountants in the United States had been reluctant to implement international accounting standards in their jurisdiction (Camfferman and Zeff, 2007, 2015). However, after the Norwalk Agreement between the FASB and IASB, in 2002, the implementation of IFRS in the United States was positively considered and the US SEC decided to accept financial statements prepared in accordance with IFRS for foreign private issuers (US SEC, 2007). At the same time, the SEC announced that it would determine whether it could enable the use of IFRS for US issuers by 2010 (US SEC, 2008). 23

The essential feature of the Interim Report and related documents is that the Proposed Ordinance added the following clause as General Principles for Application: From among the business accounting standards prepared and published by organizations that, in the course of trade, conduct research and study concerning, and development of, business accounting standards which satisfy all of the following requirements, those which are specified by the Commissioner of the Financial Services Agency as such that are found to have been prepared and published under fair and appropriate procedures and are expected to be generally accepted as fair and appropriate business accounting standards shall be regarded as the business accounting standards that are generally accepted as fair and appropriate … (Article 1 (3))

In particular, the proposed “Kinyucho-Kokuji” (Public Notice by the FSA) postulates that “the business accounting standards that are generally accepted as fair and appropriate” specified by the Commissioner of the FSA include the standards developed by the ASBJ.

In addition, as Special Provision for Application, the Ordinance stipulates that specified companies that meet certain requirements can use the Designated International Accounting Standards in their consolidated financial statements, and the “Kinyucho-Kokuji” specifies that the Designated International Accounting Standards are those developed by the IASB. In other words, the Ordinance allowed individual Japanese companies to start using IFRS voluntarily in their consolidated financial statements from the fiscal year ending on 31 March 2010. 24

The enforcement power of the Public Notice (i.e. “Kinyucho-Kokuji”) is not included in the statutory rules as same as the Circular Notice (i.e. Tsutatsu or Guideline). However, in a special case when the Minister (in this case, the Commissioner of the FSA) establishes a certain provision by the delegation of an Ordinance, the Public Notice may be considered enforceable, as statutory rules. Therefore, unlike in the case of the Circular Notice, the “legal status of accounting standards set by the ASBJ was raised in rank” (Sugimoto, 2009: 84) with this Public Notice. At the same time, although it is limited to the consolidated financial statement of the specified companies, the Designated International Accounting Standards (i.e. IFRS) were approved by the revised Ordinance and Public Notice and IFRS became legitimate in the current Japanese legal system.

The revised Cabinet Office Ordinance No. 73 of 2009, together with the provision of the voluntary adoption of IFRS, maintained the continuous application of US GAAP by firms preparing their consolidated financial statements under US GAAP as a transitional measure with a time limit set by 31 March 2016. However, this time line was later abolished by the Cabinet Office Ordinance No. 44 of 2011 and the Ordinance restored an acceptance provision of US GAAP following the request of Japanese industries.

Discussion paper 2012

On 11 March 2011, the Great East Japan Earthquake and resultant tsunami and nuclear disaster hit north eastern Japan, and had a significant impact on the Japanese economy. In response to this, Shozaburo Jimi, the Minister for Financial Services at that time, released Considering on the Application of IFRS (Jimi, 2011), on 21 June 2011. It specified that the circumstances surrounding the IFRS adoption in Japan had drastically changed since 2009, when the Interim Report was issued, 25 and, as a result, he suggested: (1) to restart the discussions about the IFRS adoption in Japan at the Planning and Coordination Committee in the BAC and (2) to postpone the decision for a mandatory use of IFRS for Japanese issuers. 26

In July 2012, the BAC issued the Discussion Summary for the Consideration on the Application of IFRS in Japan (Discussion Summary: BAC, 2012) on 2 July 2012, as an interim report at the Planning and Coordination Committee of the BAC. The Discussion Summary reviewed the debate into the following seven categories: harmonization of accounting standards, application of IFRS, opinions from Japan, non-consolidated financial statements, accounting standards for small and medium enterprises (SMEs), voluntary adoption, and principles-based accounting. As a whole, the Discussion Summary recommended that consideration should be given to the most suitable way for Japan to respond to IFRS, while pursuing the convergence between the Japanese GAAP and IFRS. The summary also recommended building up examples of the voluntary application of IFRS, as well as paying due attention to the purpose of the application of IFRS and its impact on the Japanese economy and legal system. At the same time, it recommended that Japanese opinions should be reflected in IFRS in an appropriate way, and unlisted SMEs in Japan should not be affected by the influence of IFRS.

For compliance with and legal backing to IFRS, the Discussion Summary repeated that every standard in IFRS, although in the case of voluntary adoption, are incorporated individually into the Japanese legal system with the Public Notice (i.e. “Kinyucho-Kokuji”) as Designated International Accounting Standards. Based on this legal framework, the application of IFRS needed to be discussed; however, as the Discussion Summary suggests, the designation was not to be limited to the pure IFRS, in the future. In this way, the possibility of an endorsement approach (JMIS, as explain later) was introduced.

The present policy 2013

On 20 June 2013, the BAC issued a report on the use of IFRS in Japan (The Present Policy: BAC, 2013). The Present Policy reiterates Japan’s commitment to the goal of a single set of high-quality global accounting standards, and suggests the following steps for the application of IFRS: (1) relaxation of statutory requirements for eligibility for voluntary application of IFRS, (2) a process to incorporate IFRS, and (3) simplification of the disclosure of non-consolidated (single-entity) financial statements. From the viewpoint of legal backing, this study needs to focus on the second step, “a process to incorporate IFRS.” The Present Policy recommends, as a new approach to incorporate IFRS, to create “an endorsement system that examines individual standards from Japan’s viewpoint of “IFRS as they should be” or “IFRS suitable for Japan,” and adopts the standards after deleting or revising some of them, as necessary” (BAC, 2013: 7). It also argues that the ASBJ is an appropriate organization to examine the IFRS standards. In this process, individual standards examined by the ASBJ should be designated by the FSA. In other words, through the endorsement process, it is assumed that individual standards of IFRS are incorporated into Japanese GAAP, in the same manner as the ASBJ standards “specified by the Commissioner of the Financial Services Agency” (COO 73, Article 1 (3)).

As mentioned before, under the current situation, the voluntary application of IFRS by Japanese companies for their consolidated financial statements is accepted. However, IFRS used by Japanese companies should be “designated IFRS,” specified by the Commissioner of the FSA. In the current system, although the Commissioner has an option not to designate some particular pronouncements, in practice, “it has been the application of pure IFRS” (Ito, 2013: 4) because the system does not provide a framework to modify some particular provisions. Therefore, from this change to the endorsement approach, the development of J-IFRS (later called JMIS) secured the Commissioner’s option from the viewpoint of “IFRS suitable for Japan.” In this regard, however, the future development of the application of IFRS in Japan was still unpredictable, as there were heated discussions about costs and benefits of the development of J-IFRS. The coexistence of Japanese GAAP, US GAAP, pure IFRS, and J-IFRS(JMIS) in the Japanese capital markets, and the Japanese strategy for the international financial regulation (how Japan should become further involved in the formulation process of IFRS) are still producing negative consequences.

JMIS

The endorsement of IFRS proposed in the Present Policy is interpreted as an examining process to “IFRS as they should be” or “IFRS suitable for Japan”. In response to the publication of the Present Policy, the ASBJ established the Working Group for the Endorsement of IFRS, composed by preparers, users, auditors, and researchers, which held 17 public meetings. In July 2014, the ASBJ issued the Exposure Draft of Japan’s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications (ASBJ, 2014). The deliberations of the Working Group stipulate the following three criteria for “deletion or modification” or acceptability of IFRS in Japan: (1) fundamental philosophy on accounting standards, (2) difficulties in practice, and (3) relationship to relevant peripheral regulations. Based on these criteria, the Working Group discussed 30 agendas in particular, and eventually focused on four issues: (1) non amortization of goodwill, (2) recycling of items of other comprehensive income and profit or loss, (3) scope of fair value measurement, and (4) capitalization of development costs. The published exposure draft focused on the first two issues. 27

After the comment period, the ASBJ issued Japan’s Modified International Standards (JMIS): Accounting Standards Comprising IFRSs and the ASBJ Modifications (ASBJ, 2015) in June 2015. Although the significance of the endorsement of IFRS in Japan and JMIS is said to be “a tool” (Tsujiyama, 2014: 42) to voice fundamental ideas of Japan on the application of IFRS and/or accounting standards in the international arena, there are various opinions on the real impact on these standards.

For the legal backing of the JMIS, similarly to IFRS and US GAAP, as the FSA proposed the revision of Ordinance on Terminology, Forms, and Preparation Methods of Consolidated Financial Statements, 28 JMIS are incorporated into the Japanese legal system through the Public Notice. However, JMIS are just accounting standards prepared and published by the ASBJ (organizations specified by the Commissioner of the Financial Services Agency); in other words, they are Japanese standards.

The IFRS adoption report of 2015

As described above, based on the Interim Report and the amendment of the relevant cabinet office ordinances, certain Japanese companies have been permitted to voluntarily file their consolidated financial statements prepared in agreement with IFRS. After a temporal cautious stance around 2011 and 2012, the FSA and the BAC returned to a positive attitude towards IFRS for “building up the examples of voluntary applications of IFRS” (BAC, 2013: 1) with the publication of the Present Policy. In addition, in June 2014 the Japanese Cabinet clearly indicated “promotion of an increase in the number of companies voluntarily adopting IFRS” as a target for the first time in a decision by the Japanese Cabinet in its Japan Revitalization Strategy. The Japanese Cabinet also conducted a survey and interviews to establish “how companies that have voluntarily adopted IFRS overcame any challenges they faced during their transition to IFRS, as well as the advantages brought about by their shift to IFRS” (Cabinet Office of Japan, 2014: 106).

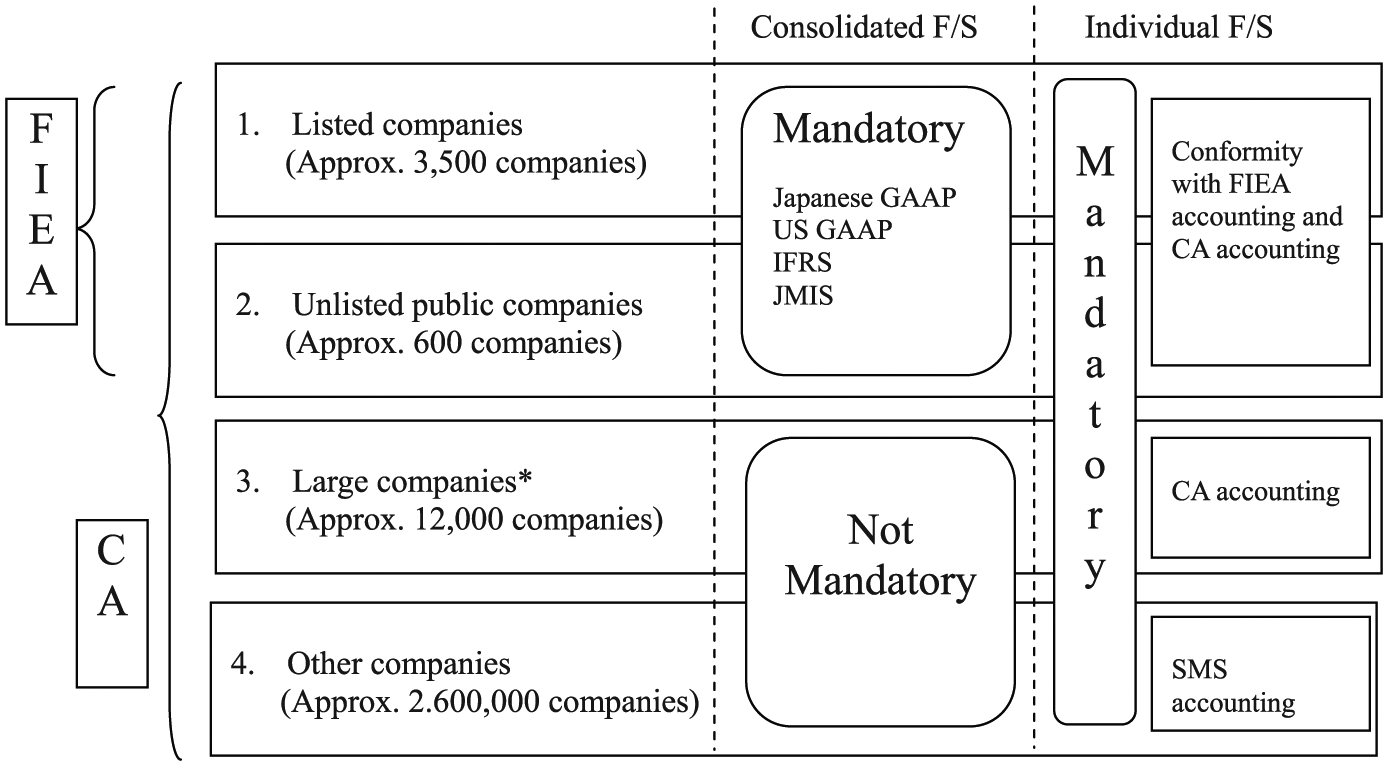

In April 2015, the FSA published the IFRS Adoption Report (The Report: FSA, 2015). This report suggested that the number of companies adopting IFRS had been increasing since 2010, and especially after 2014, when the Japanese Cabinet introduced the Japan Revitalization Strategy. From a survey conducted on Japanese companies which voluntarily adopted IFRS, the report noted that many companies consider “contribution to business management (sophistication of business management)” as the greatest merit of adopting IFRS. The costs for adopting IFRS vary with the company size and primary purpose of adoption. In addition, the report suggested the need to enlarge the number of accounting experts and to make use of connections with other companies and to conduct analyses of other companies’ cases in the transition process to IFRS. Figure 4 indicates the current situation of coexistence of the four standards in financial reporting systems in Japan.

Disclosure requirement under the Companies Act (CA) and the Financial Instruments and Exchange Act (FIEA) in Japan.

Discussion and conclusion

The reason why the ASBJ was established in 2001

The reform of the financial system in Japan began in the late 1990s and aimed to make the Japanese financial market more effective and internationalized. Macroeconomic factors, such as the prolonged recession and the decline in the international status of the Japanese stock market, played out in the background of the reform. Japan conducted extensive accounting improvements, known as the “accounting Big Bang,” and motivated by the need to enhance Japanese GAAP’s quality and to achieve the international harmonization of accounting standards. To address these issues, the ASBJ was established in 2001. Since Japanese policymakers believed that a private sector standard setting body was a condition for a seat in the newly restructured IASB, Japan’s strategy for international accounting standard-setting had a large effect on the establishment of the ASBJ.

The switch from a public sector standard-setting body to a private sector body aimed to take advantage of the existing private expertise. However, such incentives may also have been motivated by “blame avoidance” or “shifting responsibility” (Mattli and Büthe, 2005), especially considering that the Ministry of Finance lost its power after various scandals were revealed in the 1990s.

The establishment of the ASBJ was “an epoch-making social experiment,” as the first ASBJ Chairman, Shizuki Saito, recalls (Saito, 2008: 58), and had a significant impact on the Japanese legal system. In Anglo-American countries, where the calculation of accounting profits is separate from that of distributable earnings and taxable incomes, changes in accounting standards, such as the implementation of IFRS, only relate to accounting disclosure on the financial markets. On the contrary, in Japan, where the accounting system has a close relationship with corporate dividend and taxation systems, a change in the accounting system had a significant influence not only on financial disclosure, but also on other institutional factors. Numerous revisions of the accounting-related laws and regulations have occurred in the 2000s.

The reason why the changes in the legal status of ASBJ standards occurred in 2009

When the FSA decided to allow the voluntary adoption of IFRS, in 2009, Japan faced the need to clarify the legal backing of IFRS and the ASBJ standards, which had received a lot of criticism, in parallel with IFRS. Thus, the change in the legalization of ASBJ standards was operationalized and further enhanced with the introduction of the Public Notice. Paradoxically, by clarifying the delegation of public authority to a private sector body, this change may have strengthened “the role of the state” (Baker and Quéré, 2014; Doron, 2015; Noguchi and Boyns, 2012).

In addition to addressing the cause of the coexistence of four standards in Japan, in this paper, I also focus on the historical momentum for the implementation of the four standards. In 2001, the ASBJ was established with two purposes: to develop Japanese GAAP and to contribute to the development of internationally accepted accounting standards. The ASBJ had to either address the convergence with existing IFRS or the identification of the future direction of IFRS, while improving Japanese GAAP. In 2008, the US SEC issued the roadmap for the voluntary use and mandatory adoption of IFRS in the United States. The change from a cautious to a positive attitude toward IFRS in the United States, together with shifts in the perception of the situation among Japanese industries, had created the conditions for the acceptance of IFRS in Japan. The fact that the United States went back to a cautious attitude in 2010 along with the Great East Japan Earthquake in 2011, triggered the extension of special measures (or acceptation) for US GAAP. JMIS is considered “a tool” to voice the fundamental ideas of Japan regarding standard-setting in the IASB and the expansion of the voluntary application of IFRS as a condition to participate in the discussion in the IASB.

Hybridization of ex ante delegation and ex post endorsement

The previous section suggests that the four sets of accounting standards in Japan have been formalized into the domestic legal system through endorsement or designation by the public sector (e.g. Cabinet Office Ordinance and Public Notice by the FSA of Japan) although differences in the standard-setting processes and public delegations exist.

In the case of Japanese GAAP, the FSA, as a government agency, has the standard-setting authority and delegates it to the BAC, an advisory body of the agency, while the standard-setting function is delegated to the ASBJ, a private sector entity. However, the delegation of the standard-setting authority from the BAC to the ASBJ can be seen as a “functional transfer” (Chiba, 2012: 477), since the BAC has little power compared to that of the US SEC. In the case of US GAAP, the standard-setting authority is temporarily delegated to a foreign private sector entity (FASB) as an extraordinary measure, as established by the Cabinet Office Ordinance. Moreover, in the case of IFRS, the authority is delegated to an international private sector entity (IASB) designated by the FSA Commissioner. Finally, JMIS are translated into law through the endorsement by the ASBJ, and, then, hold the same legal backing as ASBJ standards. The legality of accounting standards and standard-setting bodies in Japan are authorized by the FSA, a public sector entity, through administrative legislation, not laws. In other words, the legitimacy of accounting standards and standard-setting bodies is granted by public endorsement. Therefore, among Scott’s (2014) three pillars of institutional legitimacy, regulatory systems seems to have the most important implications for the legitimacy of accounting standard-setting in Japan.

In the United States, the Congress delegates the authority to set accounting standards to the SEC through the Security Act and Security Exchange Act and to the FASB, a private sector independent standard-setting body consisting of accounting professionals (ex ante delegation or professional control). In that sense, the FASB is the legitimated standard-setting body in the United States, and FASB standards are enforceable unless the SEC’s intervenes against them. Moreover, the SEC requires its domestic issuers to only use US GAAP in preparing their consolidated financial statements. On the contrary, in the EU, the IAS Regulation (European Parliament and the Council of the European Union (EU), 2002) requires EU-listed companies to use IFRS for their consolidated financial statements, and, thus, provides legitimacy to IFRS. However, the EU does not fully delegate the authority to set accounting standards, as it implements a later endorsement mechanism for each standard in IFRS (ex post endorsement). Moreover, member states have the option to require or allow their domestic companies to use IFRS for individual financial statements.

Compared to these two benchmarks, Japan’s situation suggests a unique hybridization between legally incomplete ex ante delegation to the private sector and ex post endorsement by a government agency (public sector). Compared with the United States, the delegation of the standard-setting authority to the ASBJ and other international standard-setting bodies is incomplete because the legal backing of these bodies becomes clear only after specification and designation by the FSA. The Japanese case is quite similar to the EU benchmark. However, major differences exist, such as the coexistence of four sets of standards and the distinction between regional and domestic standards. In addition, even though the EU endorsement process excludes the Conceptual Framework, the designated IFRS in Japan includes the Conceptual Framework approved by the IASB. Moreover, the legalization of accounting standards and standard-setting bodies in the EU is provided by IAS Regulation, a binding legislative act. In contrast, the legalization of accounting standards and standard-setting in Japan is provided by the FSA, through administrative legislation.

Concluding remarks

The purpose of this study is to provide a historical narrative of the standard-setting in Japan and the analysis of the unique experience of the coexistence of four sets of accounting standards through the lens of legality.

First, the narrative shows that the ASBJ was established in 2001 to enhance Japanese GAAP’s quality and to achieve the international harmonization of accounting standards. In addition, Japanese policymakers believed that a private sector standard setting body was a condition for a seat of the newly restructured IASB; Japan’s strategy for international accounting standard-setting had a significant effect on the establishment of the ASBJ. Second, when the FSA decided to permit the voluntary adoption of IFRS, in 2009, Japan needed to clarify the legal backing of IFRS and ASBJ standards, which had received a lot of criticism. Thus, the change in the legalization of ASBJ standards was carried out and enhanced with the release of the Public Notice. Finally, my findings show that the four sets of accounting standards in Japan are formalized into the Japanese legal system through ex post endorsement by the public sector although differences in the standard-setting processes and public delegations exist. This finding also suggests an interesting example of hybridization between legally incomplete ex ante delegation to the private sector and ex post endorsement by the public sector.

Overall, the narrative suggests that the global harmonization of accounting standards and the institutional change from the public sector to private sector standard-setting had a significant impact not only on the legal backing of accounting standards, but also on the Japanese legal system. Nonetheless, this study also suggests that the government still has a major role to play in the legalization and legitimacy of accounting standards.

The findings of this study suggest several future research directions. Given the coexistence of four sets of accounting standards in Japan, this study lacks in-depth consideration of the causal processes that gave rise to such situation. I referred to two benchmarks (the United States and the EU) and the Japanese case; future research would need to conduct a comparative study including other regions and countries, such as other Asian countries and member states of the EU. Finally, as this study takes a historical (or descriptive) approach, it does not consider the costs and benefits, as typical of an economic approach, of the adoption of IFRS and/or the coexistence of several standards in domestic settings.

Footnotes

Acknowledgements

I would like to acknowledge and gratefully thank the guest editors Corinne Cortese and Peter Walton and the two anonymous reviewers for their helpful comments. An earlier version of this article was presented at the European Accounting Association Congress 2014 in Tallinn and the American Accounting Association Annual Meeting 2014 in Atlanta. My particular thanks to valuable comments received from participants, especially Richard Macve, Brigitte Eierle, Martin Emanuel Persson, Muhammad A. Mainoma, Yiming, Yoshihiro Tokuga, and Akinobu Shuto.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.