Abstract

What are regulatory intermediaries? What roles do regulatory intermediaries play? What is the basis of their regulatory capacity and authority? This article examines these questions by focusing on the Big-4 international audit firms in the context of harmonizing international financial reporting standards. I argue that regulatory intermediaries perform a variety of regulatory market failure correcting functions for both regulatory makers and takers. Intermediation is far from being secondary to the regulatory process, and intermediaries, particularly those of transnational nature, have a pivotal role. Furthermore, regulatory intermediaries, as exemplified in the case of the Big-4, continuously challenge the primacy of the state, and the division of labor and balance of power between regulatory actors. Regulatory entrepreneurship and activism, coupled with unique organizational model based on global networks of partnerships, have led to the ascension of the Big-4 to unprecedented regulatory and market powers.

Introduction

The scholarly literature on regulatory governance divides the field of regulation between rule-makers (those setting rules and standards) and rule-takers (the targets of regulation). These two groups interact with one another in numerous ways, such as through the issuance and undertaking of legal and nonlegal binding and voluntary restrictions, setting of obligations and standards, monitoring, enforcement, certification, as well as through regulatory capture and lobbying by the rule-takers of the rule-makers (Cortese et al., 2010; Cortese and Irvine, 2010). Yet, this supply and demand dichotomy is challenged by the concept of intermediaries that link and intervene between regulatory makers and takers (Levi-Faur and Starobin, 2014). The many roles ascribed to regulatory intermediaries often overlap with those of actors on the supply or demand sides of regulation. Thus, while intermediation encapsulates the idea of a spatial and functional middle position between regulatory takers and makers, its theoretical and functional underpinnings remain blurred.

This article analyzes regulatory intermediation, the connector between the supply and demand in the regulatory chain (Levi-Faur and Starobin, 2014), focusing on the role played by large international accountancy and audit firms. These firms considered typical regulatory intermediaries (Levi-Faur and Starobin, 2014), are mandated by governments to provide periodical independent examination of corporate financial accounts according to defined accounting and audit standards. This article asks three key questions:

What are regulatory intermediaries and what distinguishes them from other regulatory actors?

What roles do regulatory intermediaries play and what functions do they serve and for whom?

What is the basis of their regulatory capacity and authority?

In answering these questions, this article focuses on the role of big auditors, particularly the “Big-4” international firms (KPMG, Deloitte, PricewaterhouseCoopers, and Ernst & Young), in harmonizing international financial reporting standards (IFRS hereafter) over several decades.

This article argues that regulatory intermediaries perform a variety of regulatory market failure correcting functions for both regulatory makers and takers. Regulatory intermediaries derive and execute intermediary authority in a dynamic and evolving manner. They gain authority from regulatory makers and takers (as a function of their reputation as experts) and other stakeholders (through the perception that they are independent and objective). At the same time, intermediaries continuously challenge the regulatory division of labor, and attempt to seize authority from the bottom-up or by taking part in regulatory-making capacities. Intermediaries’ organizational structure can facilitate this dynamic, as in the case of the Big-4, which gained extraordinary economic and regulatory powers by expanding their intermediary role into the realm of standard-setting.

International accountancy and auditing firms, including the Big-4, provide a typical case study of a profession engaged in performing typical regulatory intermediary roles (Fransen and LeBaron, 2019; Levi-Faur and Starobin, 2014). International accountancy and auditing firms connect governments, firms, and investors by monitoring and enforcing rules and standards and how they are interpreted. The Big-4 firms dominate the accountancy and auditing profession, representing most transnational activities in the sector. Nevertheless, little has been written about the Big-4’s ascension in the global economy (Botzem and Quack, 2009; Strange, 1996). This article focuses on the Big-4’s engagement in developing and harmonizing IFRS as a critical issue that affects regulatory makers, takers, and intermediaries. The development and harmonization of standards is crucial in this case study, revealing the motivations, roles, capacities, and actions across domestic and international levels of the IFRS global governance regime and in relation to other governmental and private actors. The article examines the Big-4 in the period from 1966 to 2014, with reference to previous periods when necessary. The analysis is based on primary sources published by the firms and international organizations. The secondary literature is employed to distill and reconstruct the role of the Big-4, particularly in the earlier parts of the period under examination. The data are complemented with interviews with senior partners in the London and New York partnerships of the Big-4 firms and executive-level officials at the International Accounting Standards Board (IASB). 1

The article is structured as follows. The next section reviews the concept of regulatory intermediaries and then briefly introduces the notion of accountancy and auditing standards as a regulatory good at national and international levels. The following section analyzes the Big-4’s organizational model to explain the emergence of regulatory intermediaries, their motivations and interests, and the basis of their power and authority. Subsequently, the Big-4 are analyzed in the context of IFRS, examining regulatory intermediary roles, the shaping of transnational governance, relations with other regulatory actors, and issues of accountability and change. Based on the empirical analysis, the final sections consider theoretical implications and draws conclusions.

Transnational regulatory governance and regulatory intermediaries

Globalization and the proliferation of international organizations, nonstate actors, international laws, norms, rules, and regimes have all given rise to the advancement of global regulatory governance. Such governance does not imply global order, yet many global activities are regulated by international or transnational formal and informal institutions, such as the International Monetary Fund (IMF) and the World Bank (Abbott and Snidal, 2000; Whitman, 2009). While domestic regulatory governance has expanded to include new areas and actors, regulation is ever more global, as the regulatory process has, in many areas, shifted to the international and transnational (Mattli and Woods, 2009). This transformation reflects the spread of regulatory capitalism (Levi-Faur, 2005), driven by market liberalization and privatization (Levi-Faur, 2011), processes complemented by increased regulation by states, civil society, and market actors in differentiated and hybrid forms (Levi-Faur, 2011). Thus, horizontal (nonhierarchical) and vertical (hierarchical) authority is increasingly fragmented, shaped, and practiced through diverse institutional strategies (Levi-Faur and Starobin, 2014).

The regulatory market perceives regulation as a dynamic political–economic process, rather than a given and imposed outcome. Regulatory interactions take place in “[m]ultistep, iterative, sense-making and reflexive processes rather than solely by one or few formative events” (Levi-Faur and Starobin, 2014: 16). Furthermore, this perspective incorporates a multitude of actors into a single explanatory framework, such as government agencies, nongovernmental organizations (NGOs), firms, interest groups, and society at large. These actors can be rule-makers or rule-takers, with the former supplying regulation demanded by the latter or having regulations allocated to them. Regulatory relations are becoming ever more extensive and complex. On one hand, regulation is practiced on domestic and international levels, which are increasingly dependent on each other; on the other hand, regulatory relations at both these levels have expanded into private spaces, with new and flexible regulatory arrangements that are either binding or voluntary (Hale and Held, 2011).

Levi-Faur and Starobin (2014) shift our attention to the important and largely neglected role of rule-intermediaries in the regulatory process. Referring to the Rana Plaza textile factory fire in Bangladesh (24 April 2013), they demonstrate that regulatory interactions between rule-makers and rule-takers are multifaceted, relating to transnational regulatory interactions, with intermediary actors having significant roles. Rule-intermediaries are defined as [r]egulatory actors with the capacity to affect, control, and monitor relations between rule-makers and rule-takers via their interpretations of standards and their role in the increasingly institutionalized processes of monitoring, verification, testing, auditing, and certification. (Levi-Faur and Starobin, 2014: 21)

Consequently, rule-intermediaries act at the interface of the regulator and the regulated (King et al., 2007). In many cases, rule-makers and rule-takers delegate intermediation to the regulatory agents, thus placing intermediaries with either the supply or demand sides. For example, credit-rating agencies monitor countries and firms according to standards they created independently or in cooperation with other rule-makers (White, 2010). Other examples include labor standards (O’Rourke, 2003), food (Reinecke et al., 2012), and fair trade (Macdonald, 2007). Thus, an important theoretical and empirical challenge is to draw clearer distinctions between regulatory intermediaries and other actors about the identity of regulatory intermediaries, as well as the roles and functions they perform.

Regulatory intermediaries play a regular, institutional role within the regulatory process. They are entrusted with regulatory roles because they possess advantages such as expertise, trust, access to information, and greater proximity to rule-takers and rule-makers. These advantages are important for certain regulatory processes, such as enforcement and monitoring, inspection, and rule-making. These advantages also lower regulatory transaction and social costs, thus incentivizing both rule-makers and rule-takers to delegate authority and responsibility to rule-intermediaries (Kearl, 1983; Levi-Faur and Starobin, 2014). A case in point is when regulatory governance tasks are delegated through “orchestration,” that is, the voluntary enlistment of intermediary actors, by providing them with ideational and material support, to address target actors in pursuit of governance goals (Abbott et al., 2015). International governmental organizations use regulatory intermediaries as a means of indirect governance. Such organizations sometimes delegate responsibilities to rule-intermediaries in order to advance and support their governance goals (Abbott et al., 2015). However, regulatory intermediaries often operate as independent actors, with distinct interests and a unique agenda (White, 2010).

Analysis of regulatory intermediaries raises two broad theoretical and empirical challenges. The first concerns the identity of regulatory intermediaries: Who are they, what roles do they perform, and what functions do they serve? These questions have received little attention so far, which has also been limited to the national level, as noted in the above discussion (Kearl, 1983; King et al., 2007; Levi-Faur and Starobin, 2014; O’Rourke, 2003; Partnoy, 2006; Reinecke et al., 2012). This article furthers the discussion, and analyzes the identity, roles, and operation of intermediaries as part of the global economy. This discussion helps to demarcate clear conceptual boundaries between intermediaries and other actors, and to better understanding the motivations of intermediaries, rather than assuming their intermediary role is delegated. Furthermore, as regulatory intermediation does not stem solely from delegation (Abbott et al., 2015), this article expands the theoretical and empirical examination with respect to the regulatory intermediation life cycle: that is, the emergence of intermediaries, their operation, and how they gain or lose autonomy.

Accounting standards and the IFRS

Accounting standards are rules and guidelines specifying how firms should report assets, liabilities, and events in their financial statements. The standards define the type and degree of information and include elements such as assets, liabilities, profits, costs, and revenues. A fundamental rationale in this is to create a level playing field across firms in reporting their financial status and value to shareholders and the public. While accounting standards may appear to be quite technical, they significantly influence the incentives structure behind firms’ behavior. 2 For this reason, they serve governments in assessing tax liability, corporate malfunction, and anticipating financial instability.

Historically, accounting standards have varied according to country-specific political, legal, cultural, and economic trajectories, with two well-entrenched accountancy schools of thought prevailing that reflect different political economies and regulatory governance regimes. In the Anglo-Saxon tradition, investors and companies are an important driving force behind the demand for regulation, which is largely supplied by professional associations acting as rule-makers. 3 However, in the Continental school, parliaments and governments are rule-makers and suppliers of regulation (Gallhofer and Haslam, 2007). Continental European practice focuses less on information provision and more on safeguarding creditors’ interests. In these countries, standard-setting is an integral part of the legal system, and accountancy standards are altered through legislation rather than case law. 4

National regulators have an incentive to work closely with the accountancy sector in developing and enforcing standards since accountancy and auditing firms serve an important intermediary role in ensuring that rules and standards are applied and enforced appropriately (Mügge and Stellinga, 2015). This relationship reflects a principal–agent problem, whereby the principal (the state) depends on the agent (auditors) to supply adequate information on their clients, necessary for effective regulation and supervision.

Over the past decades, the international harmonization of standards eventually led to the development of an international regulatory regime, whereby a growing number of countries have adhered to IFRS. Far from a linear trajectory, this process of shaping international regulation in accounting and reporting standards involved a multitude of actors engaged at domestic and international levels, including the Organization for European Economic Cooperation (OEEC), United Nations (UN), World Trade Organization (WTO), and the Organization for Economic Cooperation and Development (OECD) (Honeck, 2002; Katsikas, 2006; Kerwer, 2008; Zund, 1983). Yet, even more significant was the transatlantic divide between the European Union (EU) and the United States. While EU member states sought and failed to harmonize their national accounting standards at the regional level, they also disagreed with US attempts to align international harmonization and convergence toward US General Accepted Accounting Practices (US GAAP) (Gallhofer and Haslam, 2007; Haller, 2002; Katstikas, 2011; Mattli and Büthe, 2005b; Posner, 2010).

In 2002, the EU decided that, starting in 2005, all EU companies listed in a regulated market must prepare and publish their statements in accordance with IFRS, thus subordinating over 7,000 companies across the EU to IASB’s international accounting standards. In August 2008, the US Securities and Exchange Commission (SEC) announced that certain companies would be allowed to provide IFRS reporting from 2010, and all companies would be required to do so from 2014 (Epstein, 2008). Although the latter decision was revised in 2010, with US GAAP and IFRS continuing to coexist (White, 2017), IFRS created a level-playing field in terms of a common international language concerning the reporting of companies’ financial statements. While IFRS are accepted in some 150 jurisdictions, 5 they are an outcome of international and private regulatory governance, at the heart of which lies the IASB, a London-based independent and private organization that develops and oversees IFRS. The IASB is the standards-setting body of the IFRS Foundation. Beyond developing new standards, the Board approves interpretations of existing IFRS standards through a continuous interactive process of research, discussion, and proposal of new standards. Following this process, drafts are developed for public review before adoption and publication.

The Big-4 and regulatory intermediation

Enforcement and information problems between rule-makers and rule-takers lead to the emergence of accountants as regulatory intermediaries (Hay et al., 2014). As business operations become more complex, demand for transparency, simplification, accuracy, and authenticity of financial statements increases (Meuwissen, 2014). Investors, creditors, and the public find it difficult to assess corporate financial information, thus constraining their ability to make informed market decisions. From the perspective of the beneficiaries of regulation, financial reporting standards only partially solve the information problem, as proper, professional enforcement of rule-takers compliance is imperative to assess whether regulatory compliance is met. Enforcement and information problems are also acute for governments due to financial stability supervision and tax collection. Governments, often the rule-makers of financial reporting standards, depend on the accuracy and quality of corporate financial reporting, but at the same time have limited enforcement capacity. Constrained by limited expertise and resources and understaffing, they depend on external, independent audits to reliably assess and verify reported information. Deferring auditing to accounting firms reduces the cost of government but imposes financial burdens on regulatory takers who pay the auditors for their intermediation. Yet, auditing is not just an issue of attesting to the reliability of financial reporting for the benefit of rule-makers and regulatory beneficiaries; firms as rule-takers often lack the expertise to provide quality financial reporting and need external professional assistance to evaluate and present the data they provide.

Hence, accountants’ role as regulatory intermediaries emerges from a three-way information problem between rule-makers, rule-takers, and the beneficiaries of regulation. Accountants act as regulatory intermediaries between governments, firms, investors, and the public. They provide independent, periodical examination of corporate financial accounts to the public, and perform auditing services comprising examination, verification, authentication, and assessment of corporate financial disclosure. Auditors’ capacity to act as regulatory intermediaries depends on their reputation (Meuwissen, 2014) for expertise and independence, achieved through regulation that conditions entry into the practice on lengthy studies, exams, apprenticeship and licensing. These preserve accountancy as a highly skilled and technical occupation (Meuwissen, 2014).

Professional independence complements expertise in creating a reputation level that convinces regulatory makers and the beneficiaries of regulation to delegate authority or accept an accountants’ authority as a regulatory intermediary (Meuwissen, 2014). Expertise is thus important only if stakeholders trust accountants are serving the public interest objectively. Accountants are required by law to provide an objective opinion and can be charged with malpractice if they are found to be in misconduct or if they perform their duties below required standards. Nevertheless, in practice the independence of accountants can be questionable and poses a major challenge for regulation. Audit services are performed in the interest of the public but are paid for by the same firms that are the subject of audit. Many cases over the years have demonstrated that accountants tend to favor their clients’ interests over those of the public: cases in point are Enron (2001), Lehman Brothers (2008), Toshiba (2015), and recently, in 2018, Carillion (Church et al., 2018; Davis, 2018; Mitchell and Sikka, 2011; Montagna, 1986; Shapiro, 2004–2005; The Economist, 2003, 2013).

The Big-4

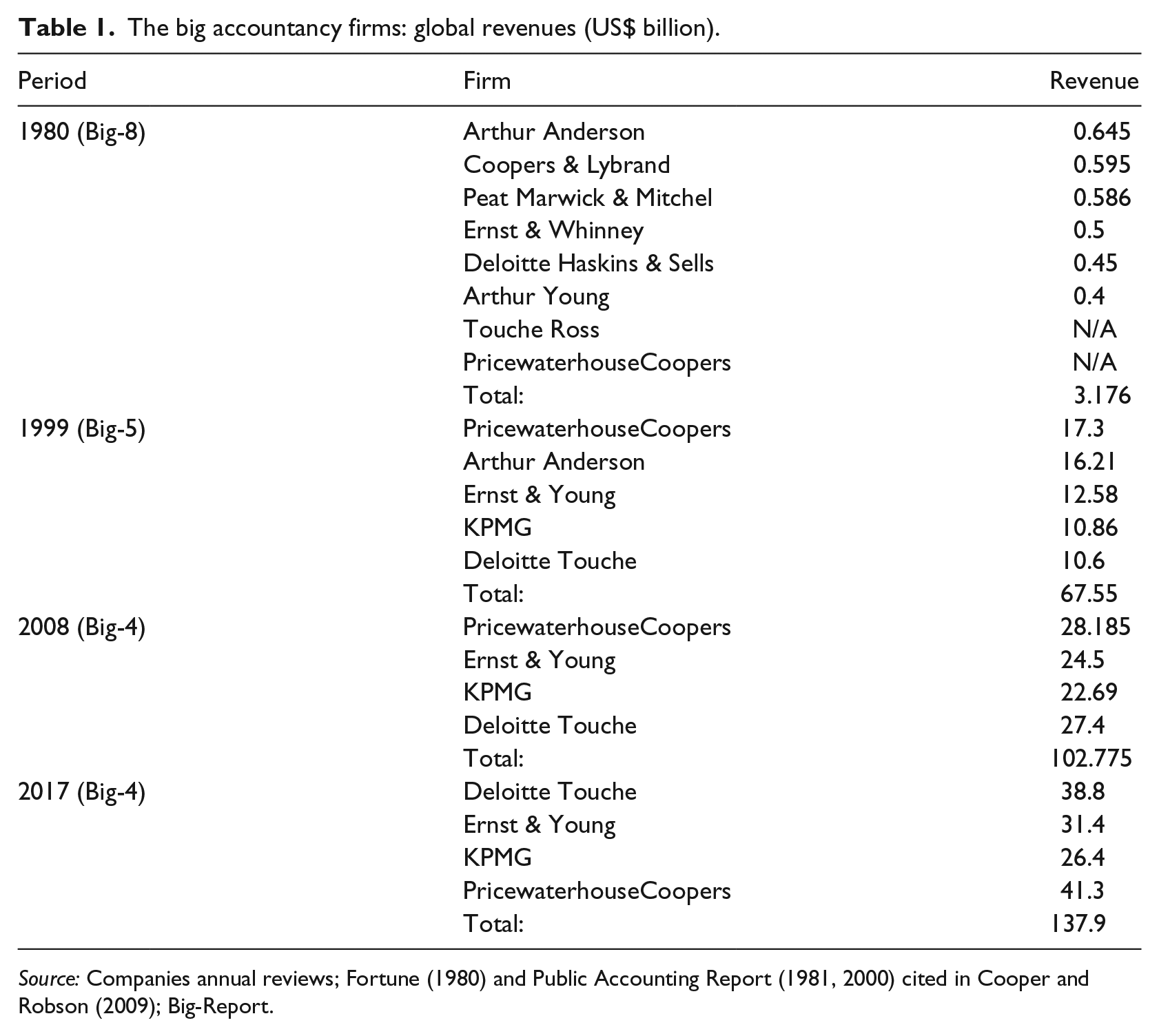

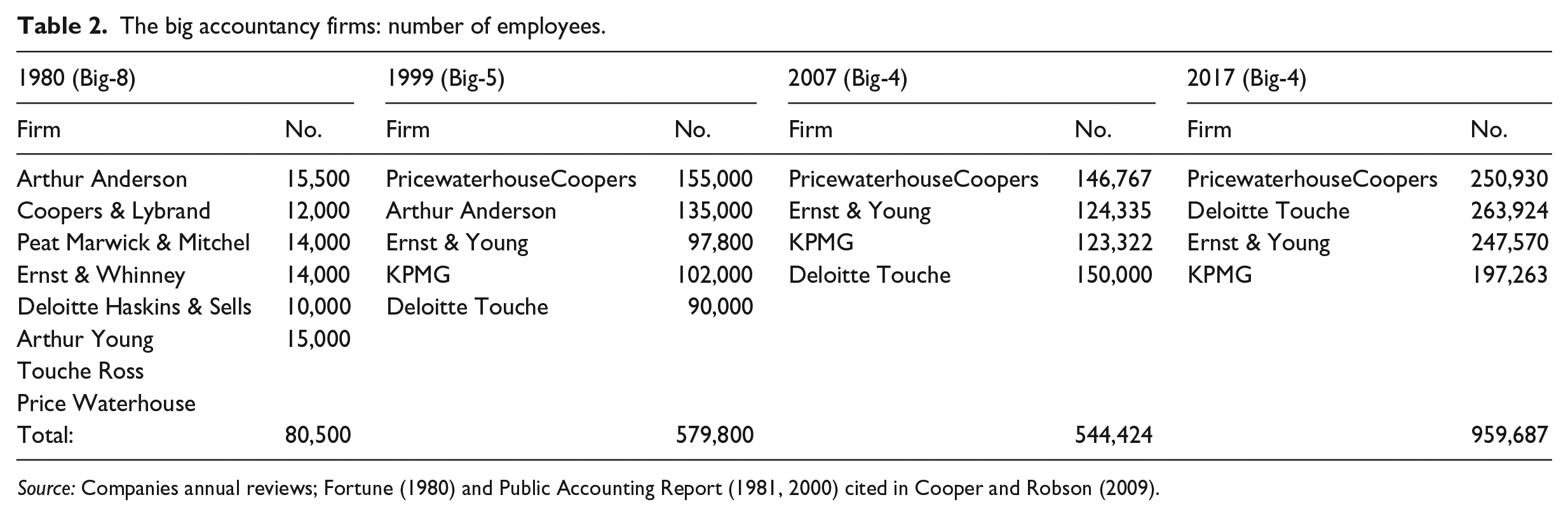

Since the second half of the twentieth century, consolidation led to the global domination of the accountancy profession by eight large accountancy and auditing firms, often termed the Big-8 (Zukin and DiMaggio, 1990). These firms originated in networks of partnerships from the United Kingdom and the United States, which, in the early 1900s, were small firms with several partners and several hundred employees. From the late 1970s to the 1990s, the accountancy sector further consolidated, with the Big-8 merging with smaller firms and expanding partnerships (Boys, 2005). Since 2002, the market has been dominated by an oligopoly of four firms, known as the Big-4 (Allen et al., 2013). Consolidation of the audit market was driven by numerous factors, including the spread of information technologies which reduce the labor-intensive costs; audit firms’ need to expand in order to service the increasing internationalization of their clients and capital flows; clients’ demands for a one-stop audit, tax, and business consultancy shop for global operations (thus achieving economies of scale by following clients’ expansion); increasing provision of government consultancy services; growing competition among big auditors; and the need to withstand losses resulting from audit malpractice litigations (Chandar et al., 2014; Malsch et al., 2018; Shore and Wright, 2018). They dominate global audit markets, and their market shares tend to exceed over 90 per cent of most OECD countries, as well as other important economies (Big-4, 2013, Botzem, 2012; Hanlon, 1999). Tables 1 and 2 show the immense growth of revenues and employees of the big international accountancy firms over a period of 37 years. In the past decade, the combined revenues of the Big-4 have increased by over 34 per cent, reaching a total of US$137.9 billion. Despite the global financial crisis, which affected part of this period, some firms’ revenues grew by more than 50 per cent (PricewaterhouseCoopers). Moreover, the Big-4 employ almost one million people.

The big accountancy firms: global revenues (US$ billion).

Source: Companies annual reviews; Fortune (1980) and Public Accounting Report (1981, 2000) cited in Cooper and Robson (2009); Big-Report.

The big accountancy firms: number of employees.

Source: Companies annual reviews; Fortune (1980) and Public Accounting Report (1981, 2000) cited in Cooper and Robson (2009).

Most international accounting firms are partnerships, some dating from the nineteenth century. Over the years, many became global through mergers and expansion of their partnerships, forming networks of firms owned and managed independently, whether wholly or partly (Boys, 2005). The firms do not each constitute a single entity but form a range of many independent firms in different geographical locations. Firms in the network enter into agreements with one another to share a common brand and quality standards, and each network has a coordinating entity, which directs the network’s activities and concentrates on brand, strategy, quality and risk (Interviews 1 and 3). The coordinating entities do not provide external professional services and do not own the firms in the network, which are separate legal entities (Interview 1). Firms in the networks are limited liability partnerships (LLPs), which limit the personal liability of partners in the case of clients’ litigation in cases of malpractice and audit failure. Hence, partners share profits but are shielded from the adverse consequences of negligence by other partners (Cousins et al., 2004). The partnership and network structures enable firms to develop a global reputation: joining the networks means subscribing to global brands, each of which encompasses over 150 countries and jurisdictions. The partnership structure provides accountancy companies with advantages vis-a-vis their clients. They expand internationally through enlarging their partnerships network while servicing their clients as local companies, thus being able to more meaningfully interact and influence both domestic and international levels (Baskerville and Hay, 2010).

The partnership structure is a hybrid of diffuse and centralized control. Centralization is key to efficiency through sharing of back-office facilities, accumulation of knowledge and reputation, and quality assurance across the network, as well as referral of clients between partners and facilitation of intra-corporate transfers (Interview 4). Diffusion enables effective and proximate delivery of services to clients. It is also a key element in the financial stability of the partnership firm, since each partnership is financially independent (Interviews 1 and 3). The partnership structure positions the firms in a unique regulatory role. Accounting and auditing practices are often developed and become standard practice through accountancy companies. They are also an important human resource for rule-takers, as their alumni take up key positions in corporate accounting and finance across all industries. The partnership network is highly coordinated, particularly regarding its regulatory intermediary roles, such as auditing and translation/interpretation of rules (Interviews 1–8).

Accountancy firms are conscious and sophisticated political actors (Botzem, 2012). The growth of their economic power has strengthened their ability to influence the political–economic environment in which they act. Historically, particularly in Anglo-Saxon countries, senior partners from accountancy firms founded and were involved in running professional associations (Cooper and Robson, 2009). This critical involvement is well illustrated in the establishment and continuing management of organizations such as the Financial Accounting Standards Board (FASB), the American Institute of Certified Public Accountants (AICPA), and the Institute of Chartered Accountants in England and Wales (ICAEW). Partners have also played a central role in founding and developing the SEC and the International Accounting Standards Committee (IASC) (Cooper and Robson, 2009; Mattli and Büthe, 2005a). While the Big-4 have expanded their membership of regulatory boards, in some jurisdictions they notably no longer conduct high-level involvement with professional bodies. Thus, accountancy firms are not only networks in terms of their structure but are also active participants in a complex political-economic web involving the private sector, professional standards-setting institutions, and regulators.

The participation of large auditor firms in the development and running of professional associations and regulatory bodies gives the firms influence over rule-making. First, as members of the organizations they influence through voice and funding. Since in many countries, particularly in the Anglo-Saxon world, accountancy standards-setting is conducted largely by the private sector, accountancy firms are not only reactive, but active in proposing new standards and modifications. Second, the influence of big, international accountancy firms, in almost all cases, extends to decision-making mechanisms. Acting and former partners of the big accountancy firms are highly represented in professional associations, such as in the case of AICPA or ICAEW. In the latter, one of the oldest associations in the world, over 70 per cent of all presidents came from the Big-4 companies, and over 80 per cent from the biggest eight firms. 6 If their number of years in office are considered, their influence is even greater.

IFRS, the Big-4 and regulatory intermediaries

The harmonization of IFRS has received considerable attention in recent years, mainly seen as a transatlantic competition and later convergence between the United States and Europe (Camfferman and Zeff, 2007; Mattli and Büthe, 2005b; Posner, 2010). While the United States has a long tradition of standards-setting, the European integration project sought to combine the diversified trajectories of countries’ accountancy systems. With the establishment of the European Community (EC) in 1957, creation of common accountancy standards was viewed as a necessary component in ensuring freedom of corporate establishment, cross-border trade, and a European capital market (Haller, 2002; Katsikas, 2006). By 2002, the EU had abandoned the aim of converging and harmonizing European financial reporting standards, deciding instead to adopt the International Accountancy Standards (IAS) developed by the IASC, which were later renamed as IFRS. In this period and context, the firms (notably the Big-4 in their configurations prior to market consolidation) were largely demanders of regulation. At that time, their regulatory intermediary role principally focused on the traditional functions of auditing, inspection, and enforcement (Königsgruber, 2009; Mügge, 2008; Quaglia, 2014). Rather than providing a new explanation of IFRS harmonization, this section complements existing narratives, in which the contribution of the Big-4 as regulatory intermediaries is mostly absent (Botzem and Quack, 2009). This focus on the Big-4 does not downplay the pivotal role of the United States, EU, and other actors in the process of harmonization. Nevertheless, it points to the largely neglected significance of the Big-4 in this process.

International harmonization of accounting standards: from the Accountants International Study Group to the IASC

In 1966, accountancy firms and professional associations from the United Kingdom, the United States, and Canada formed the Accountants International Study Group (AISG) with the aim of developing IAS as a counterweight to European attempts to develop pan-European standards (Colasse, 2010; Veron, 2007). The Big-8 firms played a prominent role in the AISG: they possessed a strong knowledge-creation advantage over national accounting standards-setting bodies, because their international network structure provided them with the capacity to produce comparative research and policy recommendations on auditing standards, professional organization, and accounting principles and practices. Indeed, an important study jointly produced by the firms through AICPA used the partnership network to create the first-ever comparative volume by a professional body, recommending greater uniformity in international accounting and professional standards (AICPA, 1964; Camfferman and Zeff, 2007). Over a decade, the AISG produced 20 comparative studies highlighting the problem of financial statements’ non-comparability across jurisdictions (Zeff, 2012).

In 1972, the AISG invited six more professional associations to join its initiative to create the IASC, with the declared ambition to develop internationally accepted standards. Existing member associations were joined by others from Australia, France, West Germany, Japan, Mexico, and the Netherlands. As in the case of the AISG, British accountancy firms were behind the motivation to establish the IASC, feeling they were not successfully securing their interests in lobby efforts during negotiations over the European Fourth Directive. Thus, while they domestically lobbied the British government and acted regionally through European professional associations, they began to diversify their options by creating a new international platform (Hopwood, 2004). From a regulatory perspective, the firms gradually and independently expanded their intermediary regulatory roles into a position situating them to provide alternative rule-making, thus enhancing their status in international rule-setting.

The formation of the AISG and IASC highlights that despite government efforts to develop international standards in international organizations, many of them clearly believed the prospects for success were greater at the regional level (Europe). This was not enough for accountancy firms wanting to enlarge their global networks and market penetration since it did not solve the transatlantic accountancy standards divide. Furthermore, private actors, most notably accountancy and auditing firms, were willing to engage in the frontline of negotiations on international accounting standards-setting. The firms played three regulatory roles. First, as agenda-setters and facilitators they brought together various international actors that were demanding rules, not only rule-makers and rule-intermediaries in their respective countries. This cooperation platform enabled these actors to discuss and later develop international standards with lesser government intervention. Second, accounting and auditing firms produced and disseminated knowledge by preparing policy-oriented comparative studies, serving demanders of harmonization and rule-makers alike. The establishment of the IASC also had a symbolic function, signaling to the rule-takers (such as multinational companies) who are the auditing firms’ clients that the firms are seeking solutions to disparity in global standards, which can remove a hurdle for clients’ internationalization. Hence, auditors were not just intermediating the rules, but seeking to shape them. Furthermore, the creation of the IASC signaled to governments that they were distanced from their constituencies, incentivizing them to reengage in international rule-making harmonization. Thus, the creation of an international private alliance was instrumental in increasing the political and economic powers of accountancy firms, as well as their expertise basis vis-a-vis other regulatory and market actors, such as governments, professional associations, and clients.

Auditing firms’ IASC engagement extended beyond demand for regulation and the performance of agenda-setting, facilitation, and production of knowledge. When intergovernmental negotiations for harmonization proved unsuccessful in Europe, the IASC went on to develop its own 26 IAS. These standards, developed from 1973 to 1988, were adopted at the beginning of the 1990s, as several European countries amended their laws to permit reporting in accordance with IAS following de-facto adoption of the standards by many European companies wanting to exploit the opportunities brought about by the globalization of trade, finance, and capital. Indeed, some European companies chose to adopt dual reporting along with the US GAAP and according to national required standards; however, most European firms embarking on this process chose IAS. Many EU member states either brought their regulation into line with the IAS or permitted it as a second, complementary reporting system (Katsikas, 2006). The growing alternative produced by the IASC, de-facto convergence to the IAS, and persistent political disagreement in Europe spurred the European Commission’s move in 2002 to suggest that European accountancy standards’ harmonization be made to the IAS/IFRS (European Commission, 1995). 7

In developing the IAS and extending their international recognition, big audit firms played a role considerably bigger than that of rule-shaping. The firms (initially the Big-8, eventually reduced to the Big-5) actively participated rule-setting. The firms continued lobbying for the general objective of international harmonization, as well as specific IAS proposals (Larson and Brown, 2001). Concurrently, they became part of the rule-making process, both directly and indirectly (Colasse, 2010). Representatives of the big firms were members of country-specific delegations participating at the IASC meetings, with many delegations including partners from all Big-8 firms (Camfferman and Zeff, 2007; Zeff, 2012). Furthermore, current and past partners from the firms became members and representatives on the IASC bodies drafting IAS. As the work of the IASC expanded in content and geography, the organization became increasingly financially dependent on contributions from the big auditors. In 1990, following a formal IASC request, the Big-6 companies at the time 8 began providing “critical funding” to the organization through annual contributions (Camfferman and Zeff, 2007).

In the 1990s, the IASC succeeded in setting standards that were voluntarily adopted by a growing number of countries worldwide. This can be attributed, at least in part, to its strategy of cooption and coalition-building. From 1976 onwards, the IASC cooperated on various initiatives with the Bank of International Settlements (1976), the OECD (1979), the UN (1980), and new national standard-setting organizations, the SEC (1984), FASB (1985), and the International Organization of Securities Commissions (IOSCO). Membership and observer status were offered to organizations with close affinity to standards-setting, such as the Association of Financial Analysts (1986), the Federation of Swiss Holding Companies (1995), and the Association of Financial Executives (1996). The International Chamber of Commerce (ICC), International Federation of Trade Unions (IFTU), International Banking Association, World Bank, OECD, and UN organs became affiliated, as did the FASB (1988), the EU Commission (1990), IOSCO (1996), and the Republic of China (1997), 9 who joined as observers. The rationale behind the cooptation strategy was to bring in and include the main actors in accounting standards-setting in such a way that these actors would become stakeholders in IASC harmonization efforts, provide it with legitimacy, and eventually voluntarily adopt and endorse the IAS (Veron, 2007). As an organizational strategy of the IASC, it gave the big audit firms, who were already represented in the IASC, a seat and voice in rule-making with these new member organizations and governments.

For the big international auditors, the IASC was a rule-setting platform (Botzem and Quack, 2006), providing an opportunity to draw on regulatory power capacities at both international and domestic levels. Thus, along with taking a leading role at the IASC, the big firms significantly influenced rule-making in some of the key national accounting standards-setting organizations that joined the IASC. A case in point is the FASB. In 1976, the Metcalf inquiry into the accounting profession produced an extensive report on the excessive political powers of the Big-8 firms, finding that they dominated the decision-making process of accounting standards-setting in the United States, enjoyed disproportionate representation, and controlled funding and staffing (Bratton, 2007; Zeff, 2003a). Despite changes made, the big auditors continued to exert much influence over the FASB (Sutton, 1984).

Motives and drivers to reform the IASC

As earlier noted, this focus on the regulatory activism of the big international auditors does not suggest they were the key actors in the process that led to the adoption of IFRS. Much of this took place in context of bridging a transatlantic divide, with governments and their representative organizations at the forefront (Posner, 2010). The big auditing firms were able to influence this process to the extent that their regulatory role went from traditional intermediary functions, such as auditing and verification, to being included in rule-making (Mattli and Büthe, 2005a). The importance of other governmental and intergovernmental actors in international harmonization can be seen in IASC’s efforts to win recognition and acceptance from the SEC, FASB, and IOSCO. The endorsement of these organizations, responsible for the world’s most important capital markets, was critical for the IAS to become globally accepted. Recommendation by IOSCO to accept IAS would have had an important impact on IASC’s attempts, because IOSCO was the standards-setting organization for stock exchanges around the world (Kerwer, 2008). This situation was clear to the SEC, which used IOSCO to influence the IASC to introduce changes that would lead to greater convergence between the IAS and US GAAP (Katsikas, 2006). SEC’s influence is reflected in the 2001 strategic transformation of the IASC into the IASB. This change reflected pressure from the SEC and FASB, due to which the IASC decided to become a not-for-profit, independent foundation and board, whose members are selected according to experience and expertise.

It should be noted, however, that others also considerably influenced the IASC’s transformation into the IASB. From 1992 to 2001, the IASC participated as an observer in a working group known as the G4+1, which included representatives of national accounting standard-setters from Australia, Canada, New Zealand, the United Kingdom, and the United States. This group published 12 discussion papers, enjoyed a world-class reputation for accounting expertise and considerably influenced the IASC to take on projects it might have otherwise ignored. While tensions and turf wars existed between G4 members and the IASC regarding what should constitute the appropriate and desired international standard-setting body, the G4 played an important role in signaling and pushing the IASC to reform and restructure (Street, 2006, 2007). The G4 dissolved as a group following the formation of the IASB. On one hand, bringing on board the IASC indicated that the G4 members recognized the centrality of the IASC in setting standards for international accounting and its role in bridging between the Anglo-Saxon and Continental European worlds of accountancy. On the other hand, it reflects the IASC’s need to attract and recruit the high-quality professional expertise necessary to ensure the acceptance of its international standard-setting position.

The big auditors favored this transition, even if it conflicted at times with their specific views on particular standards. Winning IOSCO’s recommendation to its members to adopt the IAS/IFRS increased their ability to serve international clients and increased their market shares. Yet, the transition of the IASC to the IASB was also warmly welcomed from a regulatory perspective. The transition increased the regulatory capacity and powers of the large auditors by improving their representation in the IASB, giving them over a third of the seats on the Board, and giving greater voice to the FASB in the harmonization process (Botzem and Quack, 2006; Dewing and Russell, 2004).

The transformation of the IASC into the IASB, and its willingness to accommodate US demands, resulted from the SEC decision in 2007 requiring US companies to fully comply with IFRS reporting by 2015. In this process, the Big-4 played the role of rule-demanders and rule-shapers through lobbying and advocacy. All the Big-4 firms submitted letters to the SEC encouraging it to move toward IFRS adoption in the fastest way possible, and also sent top professionals and partners to the United States to influence colleagues and clients to support the move (Solomon, 2008; Zeff, 2008).

To persuade the SEC, in November 2006 the chief executive officers of the six biggest accounting firms (Big-4+2) published a joint White Paper (DiPiazza et al., 2006) prioritizing the issue of global convergence of accountancy standards for capital markets and the accountancy and auditing professions (Albrecht, 2008). For the Big-4, IFRS offered a large advantage since it allowed them to speak and practice a common language throughout the partnership network and enabled easier internal movement of labor and referral of clients. 10 Furthermore, an international standards regime based on principles reduces the liability risks of complying with detailed standards in different locations. Transition to IFRS also had major financial advantages for the Big-4, increasing fee revenues and revenues generated from transforming their clients’ financial reporting and systems. In an attempt to shape public support to influence the SEC, several auditors (KPMG, PricewaterhouseCoopers) and International Federation of Accountants (IFAC) issued industry and business surveys that supported transition to IFRS (Gill, 2007; Mügge, 2008). 11

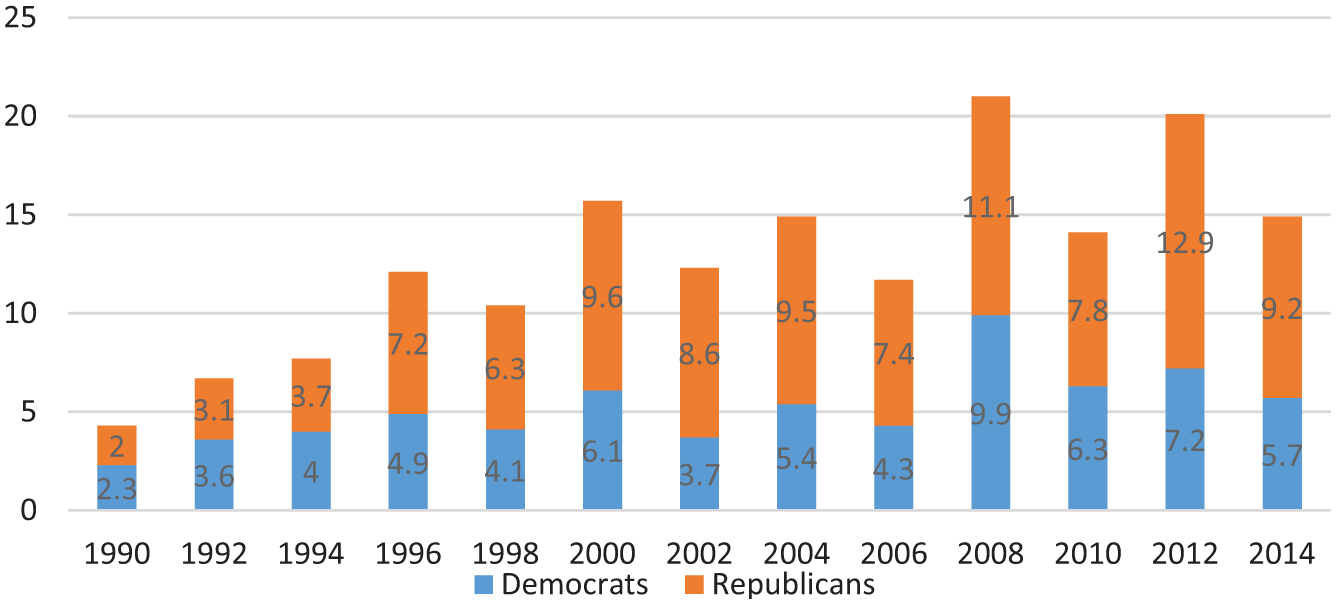

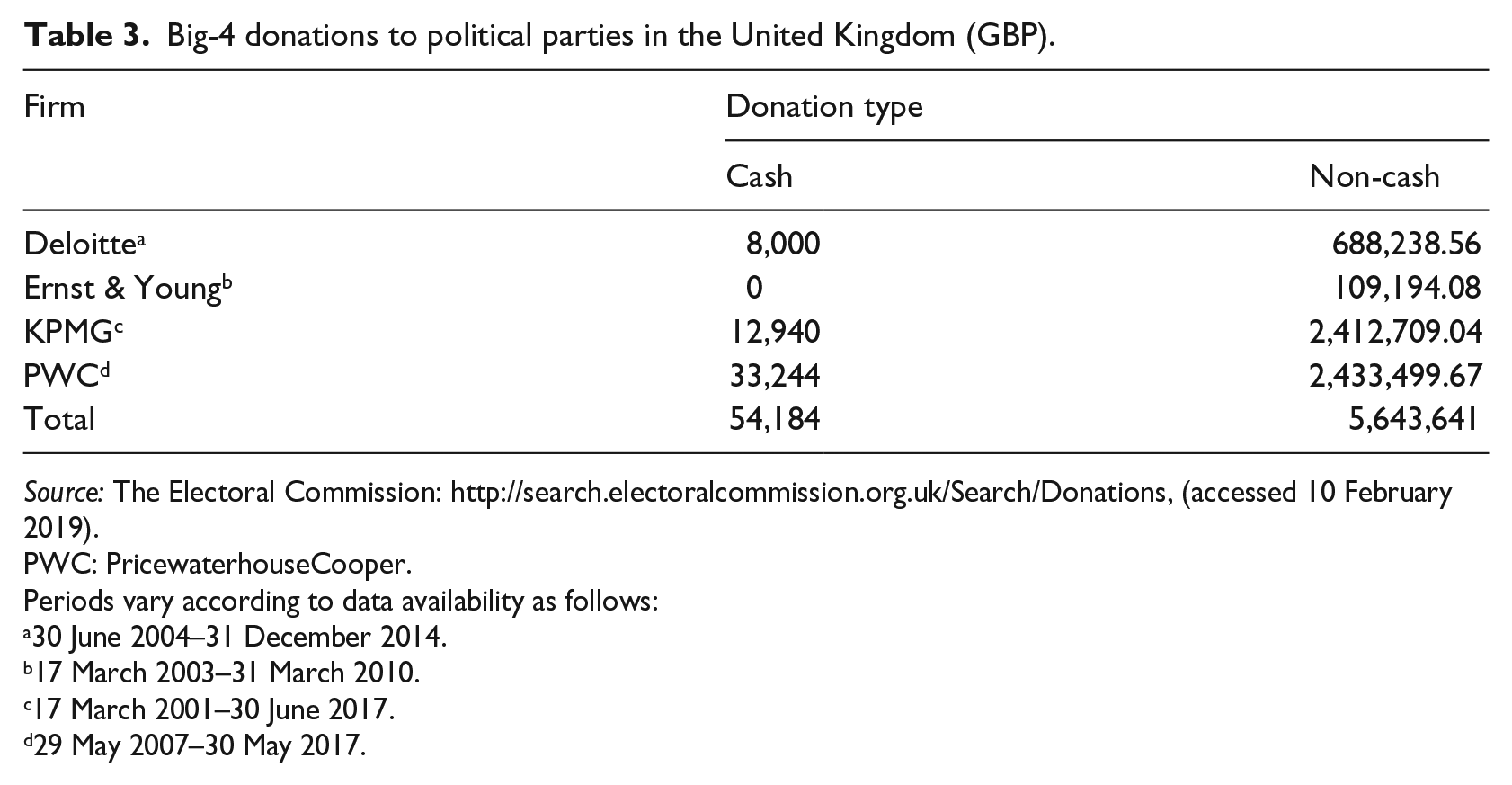

While evidence is circumstantial, and one cannot draw clear causality between lobbying and outcomes, a fundamental asset in the success of Big-4’s influencing the regulatory-setting process is the firms’ political financial connections. Vast economic resources are invested in political contributions made by the Big-4 and their partnership networks in the United States and the United Kingdom, as reported in Figure 1 (Big-4 and AICPA contributions constitute most of these contributions) and Table 3. These contributions should be understood as political investments based on expectations for future returns on matters important to the accountancy and auditing sector. Financial contributions are also accompanied by considerable lobbying (Königsgruber, 2009; Zeff, 2016), including numerous influential persons who are former Congressmen, officials, and Parliament staffers turned as lobbyists or vice versa. Official declarations made by accountancy lobbyists indicate IFRS as one of the key issues advocated (Centre for Responsive Politics, 2016). Table 3 indicates that most Big-4 contributions to political parties in the United Kingdom are made indirectly by funding parties’ staff salaries and the provision of various services. 12

Political contributions to the accountancy sector. Total, 1998–2014, United States (US$ million).

Big-4 donations to political parties in the United Kingdom (GBP).

Source: The Electoral Commission: http://search.electoralcommission.org.uk/Search/Donations, (accessed 10 February 2019).

PWC: PricewaterhouseCooper.

Periods vary according to data availability as follows:

30 June 2004–31 December 2014.

17 March 2003–31 March 2010.

17 March 2001–30 June 2017.

29 May 2007–30 May 2017.

For example, Ernst & Young was among the 10 biggest lobbying firms in the United States between 1998 and 2016. 13 Empirical study of Political Action Committees (PACs) found that accountants made significantly higher contributions to legislators who were members of Congress committees affecting accounting affairs (Königsgruber, 2009). Lobbying Congress was a priority for the Big-4, since the former can veto any standard decided by the SEC (Beresford, 2001; Zeff, 2016). Big-4 contributions have grown considerably since the SEC began reviewing the possible adoption of IFRS in 2001. The Big-4 also make large financial contributions to political parties and candidates in other countries. For example, the Big-4 became a prominent lobby actor, using former senior politicians to influence Australian Parliament (Ferguson and Johnston, 2010).

This emphasis on the Big-4 in analyzing the agency role of regulatory intermediaries in constituting IFRS global governance does not suggest per se that these firms operated a lobbying cartel, although, as noted above, formal interfirm coordination between the big auditors existed in professional associations. While market competition prevailed between the big auditors (Zeff, 2003b), they were interested in promoting closer international convergence of accounting standards, regardless of their specific substance. Convergence became more desirable as ideological rifts minimized toward clear preferences for an international principals-based regime, particularly among the big firms (Solomon, 2008).

As incentives for interfirm coordination have strengthened, indications show cartel behavior among the Big-4 and possibly several smaller firms operating in the context of IFRS. The abovementioned November 2006 joint White Paper (DiPiazza et al., 2006) submitted to the SEC is a case in point. Although two interviewees for this research objected to using the terms cartel or market collusion, senior partners and top managers in all Big-4 firms acknowledged a highly coordinated IFRS interfirm mechanism (Interviews 1 and 2, 4 and 5, and 7). Although it ostensibly deals with technical issues of IFRS interpretation, this mechanism reaches into commercial and political interests and is translated into joint strategies. 14

Interviewees reported that Big-4 senior partners responsible for IFRS meet at national, regional, and global levels regularly and frequently to discuss IFRS issues and share information. These meetings include nontechnical firm professionals, discussing topics on clients and national and global spread of IFRS. As one interviewee stated, “the meetings are informal and officially they do not exist and not documented. We get together for an extended lunch” (Interview 3). Another interviewee noted with respect to interfirm informal coordination meetings that “we discuss technical and nontechnical matters, which concerns us and our clients . . . disagreement over interpretations is usually discussed” (Interview 2). One interviewee at the IASB reported that the firms “interact with each other prior to the meetings. It is noticeable that at the meetings with the IASB, the firms are usually in consensus rather than divided over issues” (Interview 9). Since IFRS is based on principles and their interpretation, these coordination meetings enable the firms to agree upon particular interpretations, which are then published in the firms’ respective IFRS manuals and presented to the IASB for adoption. Many of these meetings are held prior to the firms’ regular meetings with the IASB (Interviews 6 and 8), thus enabling them to present a consistent approach to the IASB and possibly also the FASB’s Emerging Issues Task Force (ETIF) and the former UK Urgent Issues Task Force (UTIF). 15 Moreover, it can be deduced that the meetings serve an important commercial interest of the Big-4 vis-a-vis their audit clients. Armed with common interpretations of particular standards, the firms can prevent clients from audit-shopping for more financially advantageous interpretations. Hence, cartel behavior cuts off market competition by restraining clients’ powers to switch between suppliers, and undermines auditors’ role as regulatory intermediaries by eroding their independence and objectivity. Not least important is the fact that the chief executive officers (CEOs) of the Big-4 meet to discuss not only technical IFRS matters, but also policy and strategy issues. Although informal, these meetings are held regularly and are highly structured (Interview 3). With no inter-state anti-cartel coordination or enforcement to restrict market power abuse, the Big-4 gain an important power asset that states cannot overcome.

Notwithstanding other actors’ interests, the Big-4’s financial, political, and regulatory investments have influenced transformation of the audit field. Their aim was to constitute a regulatory space to enhance their intermediary roles and capacities. Doing so required moving beyond the standard intermediary role at the interface of regulation supply and demand. Having the IFRS as a common set of rules maximized each firm’s internal economy of scale, but a global IFRS governance regime also benefited the Big-4 by enhancing external economies of scale. Three issues, relating to the Big-4’s constitutive role, are noteworthy.

First, the Big-4 firms all founded “global IFRS centers” for training staff and facilitating global intrafirm cross-border movement of employees through a shared and updated common professional language. These IFRS centers also train professional staff of Big-4 client firms, an issue that was more critical before the widespread acceptance of IFRS across the globe. Training clients in the early stages was a building block in creating demand for IFRS (Interviews 2, 4, and 5; Harris, 2008; Whitehouse, 2008), increasing pressure for a global IFRS regime and expanding demand for the services of the Big-4. Yet, not all audit and accountancy intermediaries shared similar interests concerning IFRS. Convergence toward IFRS entailed significant fixed costs, which were not beneficial to smaller auditors, whose clients were less internationally orientated. Furthermore, smaller auditors did not share the advantages of the Big-4, which could spread IFRS adaptation costs over a large number of clients and expected significant returns from future market shares (Wieczynska, 2016).

Second, the Big-4’s constitutive role in creating demand for IFRS extended also to the realm of intermediation. Thus, the Big-4 not only trained and educated staff but provided IFRS education to new generations of intermediators in university studies around the world. The Big-4 support numerous professorships, chairs, and other contributions (De Villiers and Venter, 2010) as well as academic cooperation schemes which combine the Big-4’s professionalized accounting studies with hands-on experience and knowledge. These schemes shaped the field of accountancy and auditing intermediation, orienting future intermediators toward IFRS. While this focus on IFRS education may be justified today given that IFRS has become universal, Big-4 academic cooperation began well before many national regulators adopted IFRS and served, at least partially, to create a supply of IFRS-trained accountants even before IFRS rules were accepted (Hail et al., 2009).

Third, the transition to IFRS also served to increase Big-4 revenues from non-audit services, particularly advisory services (Interviews 7 and 9). The Big-4 increased their income by advising firms concerning new standards (e.g. leasing and financial instruments) and the provision of related strategic advisory and compliance services (De George et al., 2012; Vieru and Schadewitz, 2010).

Finally, we must look at how regulatory intermediation stretches to regulatory making, as well as the blurring of boundaries between regulatory supply and intermediation (Hansen, 2011; Nölke and Perry, 2007; Perry and Nölke, 2005). 16 The regulatory division of labor breakup is reflected in four dimensions regarding the IASB, the IFRS standard-setting body: lobbying, funding, institutional setup, and rule-making (Perry and Nölke, 2005). Lobbying to influence decision-making is not an act of regulatory making. However, it can become so when the lobbyer and subject of lobbying foster privileged relationships. Evidence of formal lobbying at the IASB shows the Big-4 as the most prominent among all actors trying to influence the process of accounting standards-setting (Perry and Nölke, 2005). Professional accounting associations, representing accounting firms as well, were the next most influential group (Hansen, 2011). While these findings by Hansen (2011) and Perry and Nölke (2005) point to the level and intensity of lobbying, they say less about its consequences. Nevertheless, viewed together with funding activity, it is unlikely (even if possible) that stakeholders will continue to fund a regulatory governance regime they are unhappy with. Funding is critical for the IASB, which depends on (largely private) financial contributions. Large accounting firms contribute a major share of the budget, with the Big-4 funding well over a third of it (Botzem, 2012). If any or all the Big-4 were to stop funding, the consequences for the organization would be dramatic. Thus, dependency exists despite an organizational separation between the IASB and the IASC Foundation (IASCF); the latter was established in part to assume responsibility for fundraising and relieve the IASB of such duties (Mattli and Büthe, 2005a). Past evidence of external influence over the FASB shows that, regardless of separation, funders strongly influence decision-making (Mattli and Büthe, 2005a).

The IASB

The IASC instituted reforms that were designed to make the organization more independent and professional as it transformed into the IASB. 17 It was hoped that this would facilitate the emergence of an IASB similar in kind to the FASB, and ease US acceptance of IFRS (Posner, 2010). The replacement of a part-time decision-making structure with a professional, expert, and experience-led organization might have freed the IASB from national political pressures. But emphasis on experience gave preference to those from large audit firms, who had greater IFRS experience, over others such as academics and national regulators. This change in the relative powers over regulatory making in the IASB has been clearly noted in the literature (Bengtsson, 2011; Chiapello and Medjad, 2009). An examination of the IASB and its various committees reveals that members or past members of the Big-4 are significantly over-represented, for example, as board members in the IASB, trustees in the IASCF, members of the IFRS Interpretation Committee, and the senior staff of the organization (Botzem, 2012; International Financial Reporting Standards (IFRS), 2016; Perry and Nölke, 2005). Thus, the Big-4 (and several other second-tier large auditors) formally engage in IFRS rule-making, and Big-4 employees are represented across IASB ranks and decision-making bodies.

The focus on experience and expertise privileges knowledge accumulated within the boundaries of the practicing accountancy profession. This knowledge, largely generated in the major auditing firms (Chandar et al., 2014), is transformed into standards-setting in several ways. The regulatory process is influenced, for example, through the abovementioned global IFRS centers. Each Big-4 company invests considerable resources in accumulating, managing, and disseminating IFRS knowledge and interpretations from its global partnerships network, using these tools within each firm and for its clients. At the same time, these informational products are focal points for frequent liaisons with the professional staff of the IASB. IASB staff use Big-4 IFRS manuals, conduct regular meetings with Big-4 IFRS teams, and are invited to the firms’ IFRS internal consultations. IASB staff also have many informal conversations with Big-4 IFRS partners and rely on knowledge and experience accumulated in the Big-4 (Interviews 9 and 10) (knowledge that is never free from financial and other interests). Finally, the Big-4 also influence regulatory-making and governance through professional secondments within the IASB’s senior staff. Each firm pays for an IASB fellowship position filled by one of its own senior managers, furthering the financial dependency of the IASB on the firms, and at the same time creating possible expertise-bias in favor of the firms. Describing the blurring of professional boundaries and the long-term effect of the secondments, one IASB interviewee for this article referred to this relationship as creating a “network between the IASB and the firms.”

Discussion

This analysis of the Big-4 draws attention to the important role of intermediaries in the regulatory process and unpacks the notion of regulatory intermediation as a spatial and functional middle position between regulatory makers and takers. Three main issues relevant to theory and practice are noteworthy. First, it examines the reasons for intermediation emergence, and defines the nature, characteristics, and functions of intermediation at domestic and global levels. Second, it distinguishes between the role of intermediation and other regulatory functions and addresses the issue of actor’s multiple regulatory roles and their cross-effects. Finally, it turns the spotlight on the importance of the Big-4 in the world economy.

Why and how? Auditors as regulatory intermediaries

Regulatory intermediation by auditors provides a solution to what can be termed at the structural level as a “regulatory market failure.” Such failure leads to the demand for regulatory intermediation by regulatory makers and takers alike. Thus, the supply of rules and standards by rule-makers to rule-takers and beneficiaries of regulation results in suboptimal equilibrium, because information asymmetry between rule-takers and other actors results in financial reports of questionable accuracy, reliability and integrity (Meuwissen, 2014). Auditors provide a regulatory-correcting function through assessing, authenticating, and verifying corporate financial reports. By attesting to corporations’ financial disclosure and being legally responsible for them, auditors provide quality assurance to regulatory beneficiaries and support rules enforcement. Corporations, the rule-takers of financial reporting standards, require and rely on auditors to provide them with expertise, technical know-how, and verification. Corporations depend on their judgment, particularly in the context of the IFRS, where the interpretations of financial reporting principles regarding corporations’ specific circumstances have significant market consequences. Thus, regulatory intermediary functions also include interpretation and translation of rules. It should be noted, however, that while intermediation provides a solution to regulatory market failure, concentrating the practice in the hands of the Big-4 also increases a systemic risk to financial markets in the case of audit failure. Expanding Big-4 activities to tax and business consultancy with their audit clients, and the increased revenues deriving from such services, incentivizes risk-taking and even fraudulent activity. These vulnerabilities have been exposed by numerous cases, including the 2002 collapse of Arthur Andersen following the Enron scandal, after which the Big-5 was reduced to the Big-4 (Peterson, 2017; Shore and Wright, 2018).

Auditors, most notably large and international ones, accumulate and manage knowledge about accountancy and auditing practices and financial reporting standards. Some of this knowledge is objective, as auditors’ have an advantage in concentrating existing knowledge; however, some of this knowledge, in the case of IFRS, is subjective, as it includes interpreting and translating the rules. Thus, auditors as regulatory intermediators are positioned as knowledge hubs and knowledge producers. This knowledge base provides them with the advantage of expertise and serves an important regulatory intermediation function, as auditors disseminate this knowledge to rule-makers, rule-takers, and other beneficiaries through channels such as services provision, consultations, reporting, training, and cooperation with academic institutions. Knowledge creation, management, and dissemination also have a constitutive role in creating further demand for rules and consequently greater market demand for services provided by the intermediaries.

Auditors, particularly the Big-4, derive intermediary capacities and capabilities through reputation. Reputation depends on an auditor’s expertise and the perception that its performance is independent. Transnational and domestic regulatory intermediation is furthered by the Big-4 partnership structure, whose global network creates international reputation, provides efficient global resources management, and at the same time retains and advances proximity between auditors and clients.

Regulatory demarcation? Intermediation and supply and demand of regulation

Regulatory intermediaries are distinct from other regulatory actors in that they perform specific intermediary functions for both rule-takers and rule-makers that the latter cannot perform. Nevertheless, this does not preclude intermediaries from simultaneously acting as rule-demanders and rule-suppliers. Thus, intermediaries are not confined to a specified regulatory role, and when possible, they attempt to gain as much regulatory power as possible. Intermediaries constantly challenge the regulatory equilibrium at domestic and international levels, seeking to further shape the demand for rules and influence rule-making to become rule-makers themselves. Such behavior was also recently documented regarding Big-4 activity in transnational labor governance (Fransen and LeBaron, 2019). The act of delegating intermediary authority to auditors is thus also a product of auditors’ capacity to simultaneously act within the regulatory “delegating side,” which determines the very nature and scope of such authority. While not the focus of this article, in the long-run intermediation capacity is also affected by macroeconomic conditions, and particularly economic crises. Crises, such as the Great Depression (1929), the Black Monday stock market crash (1987), the dot.com bubble burst (2000), and the financial crisis (2008), tilt the regulatory pendulum away from the auditors and result in government intervention in accountancy rule-making. The Securities Act (1933), Sarbanes-Oxley Act (2002) and Dodd–Frank Wall Street Reform (2010) are respective cases in point (Chandar et al., 2014; Shore and Wright, 2018).

Acting as regulatory intermediaries, the Big-4 has over the years sought to shape auditing and accountancy regulation. In some jurisdictions, the big auditors have exerted considerable influence within national professional associations. These are the gatekeepers of the profession, having regulatory-making responsibilities and authority. This influence was the outcome of economic power enabling the firms to lobby regulators and politicians, provide funding, second and volunteer staff, and assume leadership of professional associations. When negotiations on international and regional convergence of financial reporting standards began, the Big-4 firms expanded their efforts from lobbying to rule-making. Thus, they have influenced governments and the European Commission directly and indirectly through domestic and international professional associations. When lobbying failed, they formed specific groupings within international organizations to collectively increase their powers, and eventually formed an alternative forum, the AISG, later the IASC. This enabled the collective of big international auditors to leverage unique expertise advantages and increased their influence on regulatory decision-making through building coalitions and alliances and co-opting key actors. The Big-5 influenced the EU’s decision not to harmonize European auditing standards, which was pivotal on two fronts: first, IASB’s standards were no longer a matter of voluntary adoption by multinational companies and became mandatory for European corporations; and second, the EU adoption of the IAS/IFRS created a critical mass that triggered an international convergence toward IFRS standards, removing a major hurdle for global standards convergence. Regulatory supply became binding and global, with Big-4 participation in rule-setting. The formation of the IASB furthered this role of the Big-4, through formal and informal representation across the organization’s decision-making and professional bodies, critical funding and secondments, and knowledge creation and dissemination. In this regulatory environment, the Big-4 continue to increase demand for regulation through IFRS education and training initiatives with clients and universities.

The Big-4’s success in changing the regulatory division of labor for financial reporting standards is noteworthy. First, the creation of a common language based on principles rather than detailed rules serves an important economic interest of the firms, further cementing their position as a global oligopoly. Second, the Big-4 retained, and perhaps even increased, their global market status as regulatory intermediaries of high reputation. Third, while acting as regulatory intermediaries, the Big-4 are simultaneously important actors in the demand for regulation and, much more so, in the supply and setting of the regulation for which they intermediate. Despite the persistent inherent conflict of interest of playing these three roles at the same time, the view of auditors as regulatory intermediaries has not substantially eroded. A possible explanation for this is the oligopolistic nature of the market and lack of alternatives. Finally, the breakup of the regulatory division of labor in favor of the Big-4 lessens market competition, as auditors can construct favorable rules and suppress competition for their services. Such behavior results in regulatory loss since it undermines the essence of intermediation, which is founded on objectivity and independence. The case of the Big-4 suggests that the further an actor expands its regulatory role beyond intermediation to include demand and supply regulatory capacities, the greater the loss of its intermediation capacity and function. In other words, although regulatory intermediation may solve regulatory market failures, allowing regulatory intermediaries to play a meaningful role in rule-setting only offsets one regulatory failure with another.

Market powers

The organization of the Big-4 into partnerships is integral to their unprecedented international spread. As international networks of financially independent partnerships, the Big-4 were able to exploit ownership, location and internalization advantages, maximizing internal and external economy of scale gains. The partnership model also instrumentally positioned the partnerships in key regulatory junctions through professional entrepreneurship and service, furthering their ability to remove regulatory hurdles to their firms’ growth. Once the Big-4 expanded from regulatory intermediation to regulatory-setting, they gained considerable influence over the set-up and governance of accountancy and auditing rules, the backbone of the world economy. While this influence increased Big-4’s powers in the realm of regulation and politics, it also strengthened their economic powers, increased the oligopoly structure of the global accounting and auditing industry and prompted cartel behavior. Nevertheless, it should be noted that the ascension of the Big-4 in the world economy and the field of regulation stands in stark contrast to their own lack of accountability and transparency. While these firms are entrusted with ensuring their clients’ accountability and transparency, they themselves are accountable only to their partners in these independent partnerships.

Conclusion

Viewed through the prism of supply and demand, analyses of regulatory interactions often treat intermediation as secondary to the regulatory process. This article argues that regulatory intermediation is an integral component, with regulatory intermediaries playing a pivotal role far beyond “neutral” mitigation between rule-makers and rule-takers. Intermediaries not only look upward to the regulator and downward to the subjects of the regulation, they constantly seek to shape and constitute the field.

Regulatory intermediaries assume a range of roles and functions demanded by regulatory makers, takers, and other beneficiaries. Regulatory intermediaries’ capacity to perform intermediation and the degree to which they affect the regulatory process depend on the intermediary actor’s specific assets (i.e. organizational structure) as well as on external factors regarding the balance of power among regulatory actors. Intermediary capacity is also determined and affected by regulatory intermediaries’ ability to assume multiple roles and act in other regulatory capacities (i.e. rule-setting, which in turn has a far-reaching impact on the regulatory process as a whole). Two important issues which require further examination are noteworthy. First, it is necessary to assess the impact of competition among regulatory intermediary actors on the formation and outcome of regulation. Second, as audit and advisory services to governments are increasingly becoming a major source of income for the Big-4 worldwide, 18 so is their desire to influence the regulatory process of setting International Public Sector Accounting Standards (IPSASs) grows. Future research should address this issue and the roles played by the Big-4 on the International Public Sector Accounting Standards Board (IPSASB).

This article also turns the spotlight on the Big-4. The influential role of these accountancy and auditing firms has received limited attention in global governance and international relations studies. Examining the Big-4’s ascension in the world economy and global regulatory governance contributes to the growing body of literature on the role of nonstate actors in the international system, how this system is created, shaped, and managed, and how regulatory authority and legitimacy are achieved. This analysis furthers the understanding of the concept of regulatory intermediation, its distinction from other regulatory roles, and the political economy, which provides intermediation with power and authority.

Footnotes

Acknowledgements

I thank Bob Hanckè, Yoram Haftel, David Levi-Faur, Mark Thatcher, Michael Storper, Piki Ish-Shalom, and Galia Press Bar-Nathan for their insightful and helpful comments. I am also grateful to two anonymous reviewers for their constructive comments and support in the review process.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.