Abstract

Monetary sanctions levied on individuals on probation and parole may dramatically influence their ability to reintegrate into the community and to complete their community supervision. Yet very little work has empirically assessed how agencies respond to these obligations. This is critical, given that individuals under community supervision occupy a liminal space: free in the community yet often at risk of violation, rearrest, additional fines, or re-incarceration. In this article, we introduce an approach to the collection and management of monetary sanctions by an adult probation and parole agency in one Pennsylvania county. This specialized department focuses solely on repayment of fines, fees, and costs for a subset of probationers and parolees who have completed all other supervision requirements. We complement the conceptual overview by presenting administrative data on this caseload (N = 5,811) to describe the population under supervision and assess the factors associated with debt amount, having difficulty with repayment, and being the subject of an enforcement action for non-payment. We conclude with a discussion of the advantages and disadvantages of this model compared with historical and other existing models of debt enforcement during community supervision.

Involvement with the criminal justice system is associated with a range of collateral consequences. An extensive literature documents numerous harmful impacts of being arrested, convicted, and punished (Kirk & Wakefield, 2018), including the imposition of legal financial obligations (LFOs), such as the fines, fees, and costs incurred from contact with the criminal justice system. Much of the relevant scholarship documents the prevalence, amount, and consequences of LFOs assessed against individuals. Legal debts are often substantial in amount, can exacerbate preexisting inequalities, and adversely affect the prison reentry process (Bannon et al., 2010; Harris et al., 2010; Link & Roman, 2017; Pleggenkuhle, 2018). Moreover, the study of LFOs assessed and/or collected by community correctional agencies suggests that leveraging traditional law enforcement tools, such as arrest or incarceration, in the event of nonpayment can result in additional and serious legal and collateral consequences (Link et al., 2020), often disproportionately impacting people of color (Harris, 2016).

However, despite a growing awareness that LFOs cause a serious burden to those under supervision, the exact processes of payment collection and enforcement used by criminal justice agencies remain poorly understood. This gap in understanding exists amid an expansion of financial penalties of criminal justice involvement within the past 10 years and an acknowledgment that LFOs are relied upon as an essential revenue stream for justice system agencies (Menendez et al., 2019). The mechanisms and policies surrounding debt collection are important for two key reasons: (a) they help to contextualize the adverse individual-level consequences reported in the literature, and (b) they clarify how institutions have responded to an increased emphasis on collecting monetary sanctions. These institutional arrangements likely vary across jurisdictions and constitute an important area of research as they potentially set in motion processes that expand or retract the reach of the criminal justice system (Beckett, 2018).

In this article, we document one institutional arrangement used to oversee LFO compliance: the creation of a distinct unit within a community correctional agency specifically tasked with the collection of previously accumulated debt stemming from monetary sanctions. This unit constitutes a departure from a “probation as usual” collection model by monitoring individuals with outstanding LFOs who have otherwise met all terms of supervision and, in turn, allowing them to escape the often onerous restrictions of supervision while paying off old balances. In this structure, individuals may face enforcement actions in response to non-compliance with payment agreements, but punitive measures such as supervision violations or re-incarceration are not used. Importantly, although this model is concerned primarily with the collection of old debts, it is distinct from pay-only, private probation because there are no supervision conditions, potentially punitive direct criminal sanctions (e.g., revocation), or additional fees (see Albin-Lackey, 2014). We describe the structure and policies that govern this unit, highlighting how this model hybridizes criminal and civil systems in the pursuit of legal debt repayment. We supplement this description with an analysis of individuals under this specialized probation caseload, how much debt they owe, and the use of levers to encourage payment. In this way, we begin to illustrate this particular type of collection model and its impact on people under supervision.

Fines, Fees, and their Collection in Probation and Parole

LFOs can include any number of fiscal assessments levied throughout the criminal justice process, such as fines, fees for system operation (e.g., monthly supervision, programming, and drug testing), restitution, and surcharges (Harris, 2016). LFOs frequently attach to an individual’s case while being processed through the courts, but may also be incurred while on community supervision. These sanctions can simultaneously serve punitive and pragmatic (e.g., fiscal) goals. While their imposition may serve as part of a sentence, they have also been used to recover—or even generate—revenue to offset operational costs (Martin et al., 2018).

According to prior research, LFOs are prevalent among individuals involved with the criminal justice system, especially those under community correctional supervision. One study found that 52% of a reentry sample owed some form of criminal justice debt, often including supervision fees, and this debt ranged from US$10.00 to US$13,000.00 (Link, 2019). Another study from Missouri showed an average of US$1,799 in debt (Pleggenkuhle, 2018), while Harris et al. (2010) found that court-related debt grew to an average of nearly US$11,000 in Washington State. There is variation, however, across and within jurisdictions, in the amount that individuals are required to and ultimately pay (Peterson, 2012; Shannon, 2020; Sobol, 2016). Nonetheless, individuals on probation and parole may generally face difficulties in paying legal debts because they disproportionately come from backgrounds marked by low levels of income and educational attainment (Olson et al., 2001; Pleggenkuhle, 2018). As a result, some individuals struggle with adhering to payment schedules, especially because very few jurisdictions use standardized assessments to determine an individual’s ability to pay (Colgan, 2017). This can lead to difficulties under community supervision (Iratzoqui & Metcalfe, 2017) and, ultimately, increase recidivism (Piquero & Jennings, 2017).

Processes of Collecting Fines and Fees in Community Corrections

Despite a growing understanding of debt types, amounts, and consequences, the current processes of tracking, collecting, and enforcing debt payments are not well described in existing research. This omission may reflect the complex and decentralized procedures involved in assessment and repayment. Specifically, multiple criminal justice agencies are involved in levying LFOs, but the agency imposing a particular fine or fee does not always necessarily bear responsibility for its collection. Community corrections agencies typically are responsible for collecting LFOs assessed in other parts of the justice system, and so must enforce payment compliance with all outstanding debts as a condition of supervision (e.g., Shannon, 2020). The lack of knowledge regarding repayment structures may also reflect variation in the degree that departments of probation and parole prioritize LFO enforcement. Some intensively focus on payment collection and enforcement because the agency depends on this revenue for their operating budgets (Ruhland, 2020). Others prioritize collection because LFO payment is considered an obligation or condition of supervision that individuals, by law, must fulfill. In these contexts, payment compliance and collection activities can become a dominant point of emphasis such that probation and parole officers report feeling like bill collectors (Morgan, 1995; Ruhland, 2020). Some agencies may elect to ignore them in light of other supervisory obligations.

Processes and policies surrounding LFO collection and sanctioning for noncompliance are important to understand as a potential mechanism through which individuals can be punished for failing to make payments. Possible consequences for nonpayment can include the loss of a driver’s license, loss of voting rights, or damage to credit (Martin et al., 2018). Moreover, nonpayment may extend the duration of community supervision (Ruhland, 2020) or result in incarceration through supervision revocation (Martin et al., 2018) despite legal prohibitions on debtors’ prisons (Bearden v. Georgia, 1983; Miller et al., 1999).

There are several possible approaches that probation and parole departments can use to track collections and administer sanctions. First, the potential alternative with the greatest benefit to individuals under supervision is the waiving or abolition of fees and costs, especially among those who cannot afford it based on an ability-to-pay assessment or indigency hearing. This approach may require jurisdictions to revisit fundamental funding structures (Link et al., 2020), yet if achieved would eliminate many of the issues with LFOs that are becoming increasingly apparent (Bannon et al., 2010; Brett et al., 2020). On the contrary, some agencies may make minimal adaptations to existing structures to accommodate debt collection, essentially retaining the core functionality of “probation as usual” with supplemental responsibilities relating to debt. For example, collection-related activities may be added to the existing roles of probation and parole officers with a standard caseload. Although this approach may require little innovation or structural change, it may introduce or reinforce practical and ideological challenges for probation officers, a group of system actors already facing role tension in trying to balance control and treatment orientations toward supervision (Clear & Latessa, 1993). Adopting this responsibility likely creates new challenges for officers trying to balance collection tasks within the already complex treatment-control dynamic, as has been observed in some jurisdictions (Hyatt, Powell, & Link, forthcoming; Shannon, 2020).

Other agencies may seek to develop new policies and practices to collect LFOs. Such changes may constitute potential avenues through which the criminal justice system’s authority for control is extended, entrenched, or reduced—an important area of research in the present penal context (Beckett, 2018). For example, agencies may hire dedicated personnel for debt collection in addition to existing staff in traditional supervision roles. This structure calls to mind the bureaucratic processes of extended supervision in the form of “managerial” justice (see Kohler-Hausmann, 2014). However, this arrangement also risks increasing the system’s reach by introducing new mechanisms that may prolong supervision and further entangle people to the system.

Some agencies may choose to ignore the collection of LFO debts altogether, perhaps due to practical or policy limitations. In this case, agencies can outsource this task to external and/or private collection agencies. Such arrangements may avoid some of the immediate collateral and direct consequences associated with LFO collection by probation officers. However, they may create a different and delayed challenge by forging tighter linkages between civil and criminal institutions, approximating the “shadow carceral state” and creating civil pathways to re-incarceration (Beckett & Murakawa, 2012). The involvement of third-party (and often financially driven, private) entities to collect LFOs (see Albin-Lackey, 2014) increases the likelihood that a process, often akin to civil arrears, could be initiated long after the criminal case closes. Although there have been no robust empirical studies in this area, such a process likely increases debt amounts through high-interest rates and late penalties. More importantly, it constitutes a clear but fairly covert expansion of the levers of control available to the justice system. Collectively, these four broad categorizations represent current and potential policy adaptations to oversee LFO collection.

Current Study: The Monetary Compliance Unit (MCU)

We focus our attention on one specific approach to fines and fees collection in the criminal justice system. This particular arrangement demonstrates an adaptation of community corrections to enhanced the emphasis on monetary sanctions imposed by the courts. The example is one of a specialized probation caseload—the MCU—whose explicit purpose is to oversee the repayment of LFO debt. This approach straddles criminal and civil borders through the creation of a unique unit and dedicated staff within a criminal agency to oversee what they treat as a civil matter. We begin with a description of this unit before presenting data on individuals linked with this caseload.

The MCU was created in November 2012 within a county-level adult probation agency in Pennsylvania to collect outstanding LFOs from individuals who have met all other terms of their supervision. Staffed by a supervisor, three probation officers, and an administrative assistant, the purpose of the MCU is to oversee closed criminal cases that still have outstanding monetary balances owed to victims or the county from fines, fees, costs, restitution, or some combination thereof. An additional rationale for the creation of the unit is that it allows regular, non-MCU officers to de-emphasize the collection of monetary sanctions and instead focus on more traditional aims of community supervision, including risk management (Dauphin County Probation Services, 2016).

An individual can be placed on the MCU caseload through three mechanisms: (a) internally, with early discharge from criminal supervision (probation or parole) if the person has completed half of their sentence, all supervision conditions have been satisfied, and payments have been made successfully for about six consecutive months, (b) through a judicial order, or (c) upon the petition of a defense attorney. The vast majority of cases placed on MCU supervision are people who complied with conditions including payments, some are through judicial orders, and very few are the result of actions by a defense attorney. Regardless of the enrollment mechanism, everyone supervised by the MCU is subject to the same policies, procedures, and potential sanctions in the instance of nonpayment.

Before the inception of MCU in 2012, a criminal case with outstanding LFOs could not be closed; the person would remain under probation or parole supervision until all debts were paid, potentially indefinitely. In the county’s new approach, a person’s debt does not preclude their criminal case from being closed. Now, active criminal supervision is discontinued and cases are terminated upon a transfer to MCU. At intake, officers attempt to resolve the entirety of an individual’s outstanding debt by consolidating LFOs from all of their existing dockets (i.e., any open cases, current and old) into one docket. The officers and/or MCU supervisor thereafter have a discussion with the person about what they can reasonably afford to pay each month after accounting for cost-of-living expenses and other responsibilities such as family care. During the process, officers can request financial documents such as bank or credit card statements, bills, and tax returns to gain a sense of income and ability to pay. As a supplemental tool, MCU can access credit databases that contain information on whether people associated with MCU have recently made large purchases. This information can be used by the MCU in the process of negotiating the amount of the monthly payment. According to MCU management, the goal for setting the monthly payment amount is to “aim low” to reduce the chance that the person fails to meet the payment obligation. Once an amount is determined with input from the person and their officer, a formal agreement is signed by all parties, including a judge, and registered on a public court docket. From here, the person will be linked with the MCU until their debt is paid in full; there are no limitations on the amount of time an MCU case can be open.

Payment, Nonpayment, and Civil Consequences

As the MCU caseload comprises people whose criminal cases have expired, MCU is not considered to be punitive or punishment-focused. The nonpayment policies and processes cannot result in a return to traditional criminal supervision, nor can they result in responsive criminal justice action, such as arrest or incarceration. Payments are scheduled monthly and paid to the MCU electronically or in person. Missed payments can result in several responsive actions, all of which provide opportunities to restart payments and cease the enforcement response process. We outline this process in Figure 1. The first responses to missed payments are informal/phone-call reminders from individual officers. If that does not produce a payment and three consecutive payments have been missed, written letters about the missed payments are issued. These letters, sent every 30 days, detail the consequences of continued nonpayment. Letters are sent to all known addresses, including those of the individual, their family members, or any other locations where they were previously known to reside.

Civil graduated sanctions process for nonpayment to MCU.

After three letters have been sent and no valid explanation for the nonpayment has been communicated to the MCU officer within 6 months, the person’s name appears on a “contempt of court” list. Written notification of this status change is hand-delivered to the person under MCU supervision to ensure that they are aware of the actions being taken. If a payment is made at this point, the contempt process ceases. If not, at the contempt hearing, the payment plan is renegotiated between MCU and the judge, and the person can make payments in court. If the person does not appear for their contempt hearing on the date outlined in the notification or fails to contact the MCU officer, a capias warrant—essentially a warrant that compels a person’s presence for a civil proceeding—may then be generated and issued. This responsive lever, however, is not automatic; similar to the revocation of standard probation, this decision to request the issuance of the warrant is made at the discretion of the officer and based on a variety of factors. The capias warrant is used as a civil consequence. Although it coerces people to attend a court hearing, it is not a criminal arrest nor does it have criminal charges attached to it.

Importantly, although the court proceedings concerning nonpayment have begun, individuals have the opportunity to make the missed payments and stop the process. Should the missed payment(s) not be received upon issuance of the capias, the person can be subsequently held in contempt and returned to court where payment agreements can again be renegotiated with MCU staff and the judge. In some cases, Pennsylvania state tax returns can be intercepted should MCU become aware that the person can pay but is not making monthly payments. This tactic is used infrequently, however, according to MCU staff.

While it departs from “probation as usual” collection models, the MCU’s approach of individualization and non-punitiveness can nonetheless incentivize people to pay off their debt burdens. Individuals may wish to avoid contempt hearings, capias violations, and the possibility of recoupment, using alternative coercive measures including tax refund interception. They may also want the removal of the public, internet-accessible docket containing details about the person’s financial payment plan and the associated implication that the person was once on criminal supervision. More broadly, if people linked with MCU perceive the unit as similar to probation-as-usual, they may have the desire to pay off the debts to sever ties with the justice system completely. Although the MCU has been active for some time, there have been no empirical analyses of how and for whom contempt hearings and capias warrants are leveraged.

Data and Method

We use a novel data set created from two sources of administrative records from the MCU and the larger county supervision agency to examine debt and enforcement within this type of monetary unit. 1 First, MCU administrative records tracked and collected within the unit provide information on monetary sanction balances and enforcement from cases under this unit’s supervision from November 2012 (e.g., the unit’s creation) to October 2019. Second, agency-level records containing demographic information about MCU-involved individuals supplement MCU records. Our analysis focuses exclusively on dockets originating in the subject county. 2

Our analytic data set was created by merging these two sources into a single file containing individuals’ legal debt records and demographic information. We were able to successfully match MCU and demographic records for 5,811 of 6,634 cases (88%). The unmatched cases were primarily because of dockets involving codefendants (such that the docket was no longer a unique identifier to a single individual) or administrative recording errors. As these missing data are not systematic, their exclusion is unlikely to introduce bias. 3

Measures and Analytic Strategy

Several variables quantify the amount of money owed by persons under MCU supervision. The beginning balance variable indicates the amount in dollars owed at the time of initial MCU placement. Monthly payment plan amount reflects the agreed-upon sum that an individual will pay monthly toward their beginning balance. A binary variable (1 = yes, 0 = no) indicates whether the person’s presence on the MCU caseload was ordered by the county court. Last amount paid quantifies the amount of the most recent payment and current balance reflects the outstanding balance, both as of November 1, 2019. We counted the number of dockets linked to an individual’s MCU involvement. However, because the MCU consolidates debts from all dockets into one lump sum, our data do not allow for further disaggregation of LFOs by fines, fees, or specific assessed costs.

With respect to enforcement actions, two binary variables (1 = yes, 0 = no) represent certain levers at the agency’s disposal to enforce payment plans and encourage payment agreement compliance. One indicates whether the individual was given a notification of a contempt hearing for not keeping up with the monthly payment. Another tracks whether someone subsequently had a capias warrant issued. In addition, we linked each case to a specific MCU probation officer using two binary indicators for whether the person was supervised by Officer 1 or Officer 2. 4 Finally, basic demographic variables drawn from administrative data indicate an individual’s age in years, sex (male = 1, female = 0), and ethnicity (1 = Hispanic and 0 = non-Hispanic). We coded race using binary variables for White, Black, and other race (which included the small number of people who identified as Asian/Pacific Islander or Native American).

Our descriptive analyses of this MCU probation model, presented in three parts, identify who owes these debts, how much they owe, how well they can pay down the debts, and what consequences they experience for nonpayment. First, we provide univariate statistics on the full sample including debt amounts, payment amounts, and demographics. Second, we assess differences in debt and payment amounts across demographics through a series of t-tests. Finally, we report chi-square findings on sanctions for debt nonpayment. Together, these results allow us to begin to assess the application and advantages and disadvantages of this model of debt management.

Results

Demographics and Legal Debt Among MCU-Associated Individuals

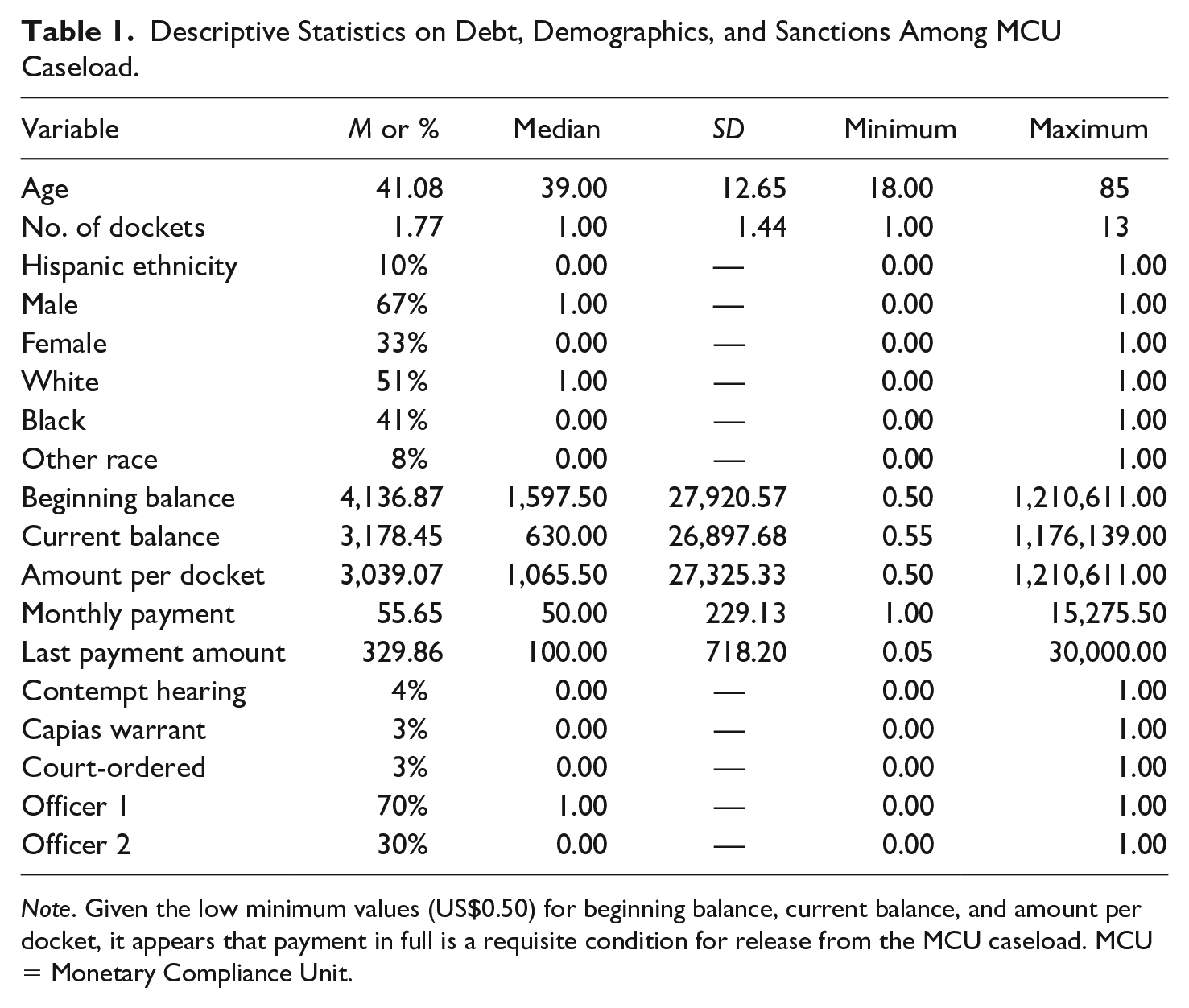

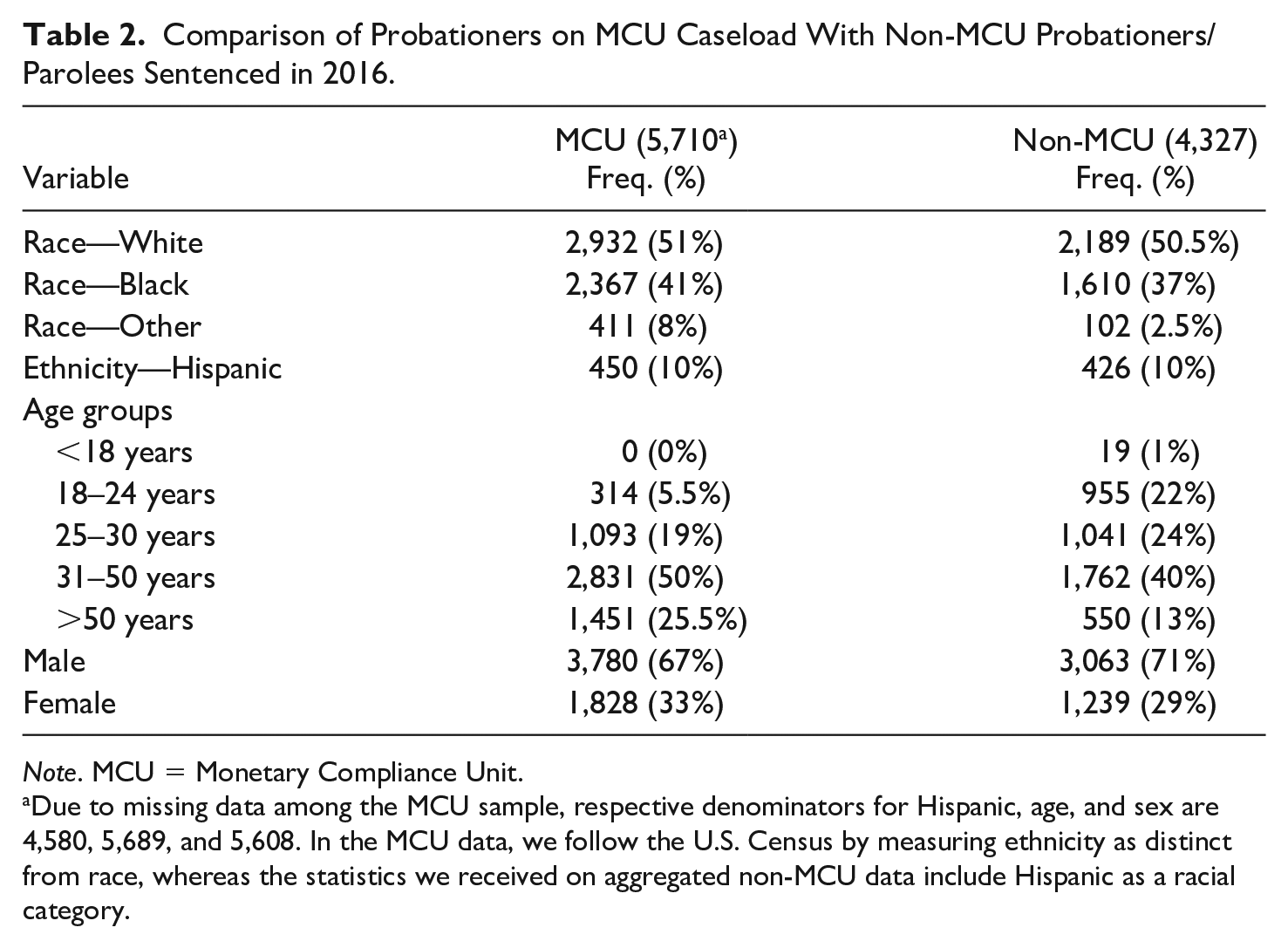

Table 1 displays various univariate statistics. The average age of someone on the MCU caseload is 41 years (median = 39), ranging from 18 to 85 years. Reflecting that the MCU aggregates the debt amounts from multiple court dockets, individuals had an average of 1.77 dockets with a range from 1 to 13. At 51%, a slight majority of people on this caseload are White, while 41% are Black and 8% are Asian or identified as a different race. Although there were more Whites than any other racial group, Blacks were disproportionately represented, given they comprise 18% of this county’s residents (U.S. Census, 2010). Ten percent of the sample identified as Hispanic and a greater number of men were linked to MCU than women (67% vs. 33%). As shown in Table 2, individuals under MCU supervision appear demographically similar to those newly sentenced to supervision under the same county probation agency in 2016, with the exception that MCU participants generally appear slightly older and a larger proportion identify as female. 5

Descriptive Statistics on Debt, Demographics, and Sanctions Among MCU Caseload.

Note. Given the low minimum values (US$0.50) for beginning balance, current balance, and amount per docket, it appears that payment in full is a requisite condition for release from the MCU caseload. MCU = Monetary Compliance Unit.

Comparison of Probationers on MCU Caseload With Non-MCU Probationers/Parolees Sentenced in 2016.

Note. MCU = Monetary Compliance Unit.

Due to missing data among the MCU sample, respective denominators for Hispanic, age, and sex are 4,580, 5,689, and 5,608. In the MCU data, we follow the U.S. Census by measuring ethnicity as distinct from race, whereas the statistics we received on aggregated non-MCU data include Hispanic as a racial category.

In general, there is substantial variation in the amount of overall debt owed. People on this caseload had an average beginning balance of US$4,136.87 (median = US$1,598) in accumulated debt to the county, with a range from US$0.50 to more than US$1.2 million dollars. Given the extremely low values in this sample, it appears that a person with any amount of debt is considered eligible for MCU supervision. Current debt balances were slightly less. The average amount of debt per docket was just more than US$3,000 (median = US$1,066). The median and mean amounts for monthly stipulated payments were US$56 and US$50, respectively. The range of payments varies greatly, reflecting that the MCU agreement is intended to be calibrated to individual circumstances. Despite these agreed-upon amounts, the mean and median amounts of the most recent payment were substantially higher at US$330 and US$100, respectively. While interesting, we note that we cannot determine with the data whether these higher amounts are simply capturing individuals catching up on missed payments from previous months or intentional overpayment. Only 3% of the sample were court-ordered to the MCU, indicating that the probation agency is largely responsible for populating the specialized unit. Finally, a cursory assessment of sanctions for nonpayment (examined in further detail below) indicates that the use of these levers is uncommon. Just more than 4% of the sample had a court hearing scheduled for debt nonpayment and 3% received a capias warrant issued for nonpayment. The agreed-upon monthly payment amounts for the vast majority (99%) of the sample was US$200 or less per month. At 32%, the largest group of people had an agreement set at US$50 per month, followed by 21% at US$25 per month. Seventy-two percent of the sample agreed to pay US$50 or less per month, 35% to pay US$25 or less, and 5% to pay US$15 or less. Two people had agreements in place of US$1 per month.

Differences in Debt

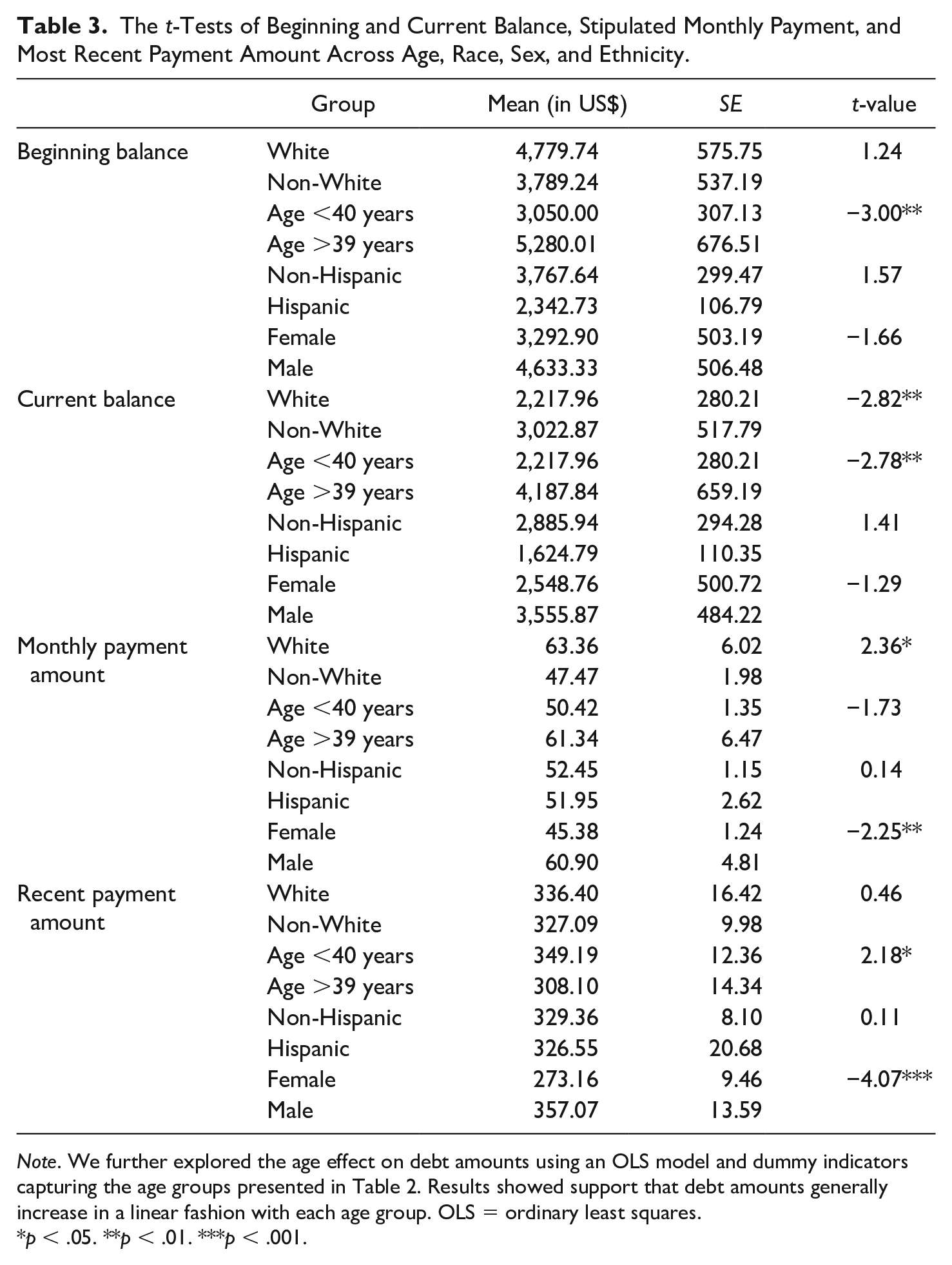

Table 3 presents the findings of t-tests examining mean differences in the beginning and current amounts of debt, stipulated monthly payment amount, and most recent payment amount across key demographic groups. Assessing for differences between older and younger individuals, we split the sample at the median age (39 years) and found that older individuals had significantly higher beginning and current debt obligations than their younger counterparts. 6 Interestingly, individuals identifying as non-White reported significantly more in current debt, but we did not observe a corresponding difference for the beginning balance. It seems that despite similar starting points, non-Whites face more difficulty in paying down their debt. Differences across sex and ethnicity did not meet the thresholds for statistical significance.

The t-Tests of Beginning and Current Balance, Stipulated Monthly Payment, and Most Recent Payment Amount Across Age, Race, Sex, and Ethnicity.

Note. We further explored the age effect on debt amounts using an OLS model and dummy indicators capturing the age groups presented in Table 2. Results showed support that debt amounts generally increase in a linear fashion with each age group. OLS = ordinary least squares.

p < .05. **p < .01. ***p < .001.

Age was significant in a manner different from what was observed for the beginning and current balance as younger people’s recent payment was significantly greater (p < .05). On average, White people agreed to monthly payments of about US$63, whereas non-Whites agreed to about US$47 (p < .05). Unlike before, we now find significant differences across sex regarding monthly and most recent amounts. On average, women had a stipulated monthly agreement of US$45, whereas men averaged US$61 (p < .01). Similarly, the average recent payment for men was significantly higher compared with women (US$357 vs. US$273, p < .001), perhaps capturing differences in their ability to pay due to family circumstances or lower wages among women.

In addition, we used the beginning balance and monthly payment data to calculate how long it would take a person to pay off their balance, assuming strict adherence to non-varying monthly payments (not shown, available upon request). On average, it would take MCU individuals 120 months (median = 46 months) to pay off their complete beginning balance with regular monthly payments in the specified amount. It would take 75 months on average (median = 43 months) for those owing US$10,000 in debt or less to pay their balance. These times may be shorter in reality, however, as data on the most recent payment suggest that some people may pay amounts that exceed their monthly stipulated agreement. 7

Sanctions for Noncompliance

Concerning administrative responses for people who were not paying under their individualized plan, Table 4 reports the results of chi-square tests examining differences in the frequency of contempt hearings and violations across demographic categories. Although there are few statistically significant differences, findings do indicate that non-Whites were significantly more likely to receive a contempt hearing notification for nonpayment and have a capias warrant issued against them (p < .001). More than 5% of non-Whites (5.4%) received a contempt hearing notification compared with 3.4% of Whites. Furthermore, 3.6% of non-Whites and 1.6% of Whites received a capias warrant. The second significant finding was that people aged 40 years and above were more likely to receive a contempt hearing when compared with people aged below 40 years (5.0% vs. 3.6%, p < .01). Although 3.2% of Officer 2’s cases received a capias warrant compared with 2.3% of Officer 1’s cases, the relationship between receiving a capias warrant and officer assignment fell below conventional thresholds for statistical significance (p = .06).

Chi-Square Analyses of Contempt Hearings and Capias Warrants Across Age, Race, Sex, Ethnicity, and Probation Officer.

p < .10. *p < .05. **p < .01. ***p < .001.

Discussion and Conclusion

Given the increasing awareness of the burdens created by LFOs imposed by the criminal justice system, our purposes here were twofold: (a) to describe the MCU and its unique policies regarding the collection of debts among people under community supervision, and (b) to examine the characteristics and experiences of people associated with this caseload. The MCU supervises an administrative caseload and utilizes civil enforcement mechanisms within a criminal justice agency, straddling the civil/criminal divide in its distinct process of LFO collection. Our analysis provides insight into the parameters, population, and impact of this individualized and nonpunitive method of LFO collection and informs conversations about monetary sanction policy reform. Influenced by our two main findings, we conclude by discussing areas for future research, limitations, and tentatively assessing policy advantages and disadvantages of the MCU and alternative models.

Demographic Differences in Debt Amounts

Our analysis revealed two new patterns of demographic variation in individuals’ LFO debt amount. First, we found that non-White persons had a significantly higher average current balance than White persons (see also Harris et al., 2011; Shannon, 2020). Despite both groups starting with similar balances at MCU intake, non-White persons seem to face challenges in repaying debt within a unit purposefully designed to custom-tailor payment plans to attainable amounts. To this point, we note that non-White persons have a lower average monthly payment amount. This finding suggests that even the most realistic approaches to debt collection—like those that customize payment plans to individuals’ economic means—may still fail if the fees themselves impose too much of a financial burden. Although persons facing these difficulties remain tethered to the MCU over a lengthier repayment period, they do not accrue additional fees nor are subject to criminal supervision violations and sanctions during this time, unlike other models of debt collection (e.g., Iratzoqui & Metcalfe, 2017). Even absent these burdens of supervision, however, this protracted connection to the justice system may still impose barriers to social integration while extending time at risk of civil actions for non-compliance.

We also highlight age differences: older persons (age 40 years or above) have significantly higher beginning and remaining balances than their younger counterparts on MCU but are statistically indistinguishable in their payment amount. The MCU’s consolidation policy is agnostic about age on its face but carries a disproportionate impact in practice. Older persons may simply have accrued lengthier criminal careers and associated debts or may be fined at higher amounts if decision-makers perceive them as being more culpable or less suitable for incarceration. Whatever the cause of this difference, age continues to be an important factor for substantially higher debt amounts (see Ruback & Clark, 2011) and potentially greater collateral consequences, especially in a collection structure that collapses debt across criminal histories. The concentration of higher balances among non-White and older individuals—and their consequences, although non-carceral in nature within the MCU—constitutes a subject for future research on the adverse consequences of legal debt.

Demographic Differences in Debt Enforcement Actions

Although infrequently used, we found evidence suggesting racial and socioeconomic disparities in the recipients of the civil sanctions used by the MCU. Non-White persons are more likely to receive a contempt hearing and a capias warrant for nonpayment than White persons. Approaches to LFO nonpayment sanctioning rooted in the punitive criminal justice measures are criticized as racially biased (e.g., Bingham et al., 2016; U.S. Department of Justice, Civil Rights Division, 2015). Findings here also indicate disparities in repayment sanctions within the MCU’s hybrid approach to enforcement—one intended to avoid overly punitive criminal justice–based responses (e.g., revocation and/or incarceration) by individualizing payments to attainable levels and exclusively using civil sanctions. Across collection structures, it appears that some persons will face difficulty in LFO payment regardless of the exact collection mechanism. These financial strains and formal consequences that disproportionately impact non-Whites are concerning. As such, future research should investigate the relative consequences of criminal and civil enforcement actions to adjudicate which approach confers the fewest legal and collateral consequences to individuals and their families and can be implemented equitably across groups (see Martin et al., 2018).

Limitations

These data should be considered in light of their limitations. We cannot examine certain variables that often can affect debt size and whether it is paid down, including employment status, income, education, and the number of dependents. Moreover, we are unable to account for the crime type for which the person was placed under supervision and their criminal history, two relevant variables for contextualizing debt amounts that may be sizable when attached to a specific offense (see, for example, Bannon et al., 2010). Similarly, a lengthy criminal history may generate increasingly large punitive financial sanctions, a factor accounted for by judges, MCU officers, and other decision-makers when making determinations about civil sanctions for nonpayment. We also cannot exclude the possibility that the racial disparities observed in capias warrants may be partially driven by other factors—for example, both criminal history and type of instant offense likely influence the decision to issue a capias. We are also unable to disaggregate fines, fees, and costs from restitution and other LFOs. Finally, because our data do not include a counterfactual group, we cannot draw firm conclusions regarding differences in the debts and consequences of MCU participants compared with those under traditional probation supervision. The policies and procedures regarding MCU suggest that debt burdens accumulate more slowly (because supervision and other fees are no longer assessed) and that levers for nonpayment are less punitive; however, we do not have the data to empirically quantify this difference.

We note that our conclusions here about who struggles with debt and who faces enforcement actions narrowly apply to a probation unit and specific collection process in one county and may not apply to other supervision agencies implementing distinct approaches to monetary sanction collection. For example, our findings regarding age and debt may be specific to the MCU or to this population, given their policy of collapsing all historical outstanding debt for individuals upon intake. More research is needed to comprehensively examine other collection processes within community supervision agencies across the United States as unique policies may similarly generate unique experiences of community supervision and challenges in debt repayment (see Ruhland et al., 2021). Given the observed disparities in this analysis, establishing the prevalence of these units across states, exploring variation in policy and practice, and describing the implications they hold for correctional control and the people subject to these systems should be a future research priority.

Policy Considerations and Conclusion

As the criminal justice landscape has increased its dependency on fines and fees, probation and parole agency practices that respond to nonpayment of LFO debt have specifically been targeted as an area in need of reform (Brett et al., 2020; Link et al., 2020). While we recognize that scaling back or eliminating financial sanctions, especially fees, is a long-term goal for criminal justice reform (see Menendez et al., 2019), we conclude by evaluating whether the specific collection process employed by the MCU represents a scaling back or expansion of correctional control relative to the seemingly dominant collection processes currently employed in community corrections: “supervision as usual” and shifting collection responsibilities to other (external) agencies. Finally, we suggest that the outright abolition or waiver of fees associated with supervision should be given greater consideration as the collateral consequences related to debts are becoming clearer (Brett et al., 2020; Harris, 2016).

In the first approach of “probation as usual,” debt collection is an additional responsibility for the probation officer overseeing a criminal caseload. Officers must figure out a way to incorporate debt collection into an already complex role orientation with both treatment and control responsibilities. When individuals they oversee become delinquent on payments and therefore violate a condition of their supervision, typical punitive levers can be employed. In some jurisdictions, these punishments can be as serious as incarceration. Individuals with outstanding debts at the time their supervision term is set to expire are subject to extensions to the length of their supervision—a process that can continue indefinitely until the debt is paid in full. Under this model, people who cannot pay debt burdens can remain under criminal supervision for lengthy periods, accrue additional debt, and stay at risk of criminal consequences.

In the second approach, community corrections agencies may decide to de-emphasize the importance of monetary sanctions collections by shifting the responsibility to other parties. This arrangement typically features a heavier focus on the traditional aims of community supervision (e.g., deterrence and rehabilitation) and views debt as a civil matter. Agencies taking this approach do not sanction for late or nonpayments and do not allow outstanding debt to prevent the closing of criminal cases. Upon case closure, however, the agency may refer to the person’s debt obligation to an external collection agency, often privately operated. Motivated by their own profits, these agencies may translate their own financial interests into additional fees and high-interest rates for referred individuals, which, in turn, can continue to grow debt faster than it can be paid off and magnify other consequences like further damaged credit and the inability to secure a loan or bank account (Albin-Lackey, 2014; Bannon et al., 2010). Arrests for nonpayment of debt owed to collection agencies can even occur in some cases (Pressner, 2019).

Both of these models differ from the MCU approach in key ways. Unlike the “probation as usual” model, MCU uniquely removes the possibility that criminal justice consequences could result in persons who cannot afford payments by closing criminal cases, effectively shielding them from any further justice system involvement related to nonpayment. Moreover, MCU does not subject individuals to ongoing supervision conditions and the accrual of monthly based fees while outstanding debt is repaid. As such, while MCU is indeed centered on debt collection and can tie someone to a government agency for a lengthy period, its process does step away from some of the punitive aspects of probation-based collection that prevail in much of the country.

The difference between MCU and agencies that choose to ignore debt collection is less clear. Both de-emphasize the resolution of LFOs as a criminal matter, which avoids many of the harshest sanctions for nonpayment. Yet a specialized unit keeps individuals tied to the justice system for reasons framed as a civil matter, whereas the alternative often relinquishes control and surveillance to private collection companies. In this latter case, profit may be a contributing factor to decisions about both debt relief and collections practices. Although there has been far too little research on private debt collectors within criminal justice, MCU may nonetheless have advantages, given the inherent fiscally-informed motivations of collection agencies that likely increase debt amounts and introduce new collateral consequences such as damage to credit ratings.

While the MCU-type model needs more scrutiny and is not without its criticisms, we note that we do not view the MCU as fully consistent with characterizations of the shadow carceral state—that is, arrangements that enhance the reach of correctional control and associated criminal consequences by forging connections between civil matters and criminal justice penalties (see Beckett & Murakawa, 2012). Unlike agencies in the shadow carceral state model, there are no administrative processes or pathways that specifically drive individuals associated with MCU into incarceration. This protection is comparatively advantageous to these two other existing debt collection models as it removes the risk of carceral punishment from supervision violations associated with debt repayment.

Although incarceration is not used, civil contempt proceedings initiated by the MCU for noncompliance may still be impactful. These levers are intended to be less punitive, but the exact immediate and future consequences of these civil actions are not yet clear. Moreover, we do not know to what extent association with MCU may lead people to avoid other critical community and social institutions (Brayne, 2014). Future research should delve into this model (or similar units) to ascertain whether civil enforcement actions provide the intended comparative benefit relative to a traditional violation and punishment model, especially given that the MCU is still associated with disparities in repayment. Despite some comparative advantages of the MCU over existing models, it is likely that abolition of fees and some other financial sanctions altogether proves to be the most advantageous for individuals involved with the justice system who are disproportionately people of color (Harris, 2016) and in disadvantaged socioeconomic backgrounds (Martin et al., 2018). It does not appear that abolition is currently occurring on a large scale; hopefully, future evaluations of jurisdictions that are experimenting with such reforms, such as San Francisco County (see Fines and Fees Justice Center, 2018), can begin to demonstrate the benefits and hurdles involved in this approach.

The various policies surrounding the collection of LFO debt have the potential to dramatically shape the community correctional process, both for the agency and for the individuals under supervision. As demonstrated here, the use of a specialized unit to meet the needs of the individuals under supervision, the agency, and the broader public, warrants further attention and scrutiny as a potential avenue that addresses some of the demonstrated harms associated with traditional court and community corrections policies surrounding debt collection.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by a grant from Arnold Ventures.