Abstract

Retirement self-efficacy includes perceptions of the extent to which one will be capable of dealing with the tasks involved in the new retiree situation. This study analyzed the psychometric properties of the Brief Retirement Self-Efficacy-11 Scale (BRSE-11) with Spanish workers aged below 62 (N = 694) and tested these properties with Spanish workers aged over 62 (N = 593). Method: We conducted descriptive analysis for the items and exploratory factor analysis with Sample 1 and confirmatory factor analysis (CFA) with Sample 2. Cronbach’s α and CFA were used to assess the internal consistency in both samples, and convergent, discriminant, and nomological validity of the RSE-11 were tested through relationships with general self-efficacy and life satisfaction. Results: Reliability values were adequate, and criterion and discriminant validity for the three factors of the BRSE-11 were supported. BRSE had a significant correlation with general self-efficacy. The three BRSE-11 factors increased the explained variance in life satisfaction after the introduction of general self-efficacy in the hierarchical regression analyses.

Retirement is a very important phenomenon in individuals’ lives, involving psychological and financial facets as well as health and social relations, among others. In view of the extended life expectancy in countries with higher rates of development, adequate preparation for retirement and retirees’ subsequent well-being is currently a concern for people and societies (Wang & Shultz, 2010). Likewise, in Europe, populational aging has led governments and policy makers to debate on the need to increase individual preparation for retirement. If people adequately prepared, they can clarify their expectations about retirement. In addition, other behaviors associated with planning, such as setting financial or leisure goals, would increase, facilitating transition to retirement (Taylor & Schaffer, 2013).

Preparation for retirement is conceptually and empirically related to one’s confidence in the capacity to deal with retirement effectively or retirement self-efficacy (hereafter RSE; Taylor, Cook, & Weinberg, 1997). RSE includes self-perceptions of the extent to which one will be capable of dealing with the specific challenges and tasks involved in the new retiree situation. Researchers in self-efficacy have shown that people will engage in a task to the extent to which they trust their skills to complete it efficiently (Bandura, 1997). Thus, expectations of self-efficacy become one of the most powerful determinants of behavior because they affect the initial decision to perform the behavior, the effort put out, the associated emotions, persistence in the face of adversity, and finally, the amount of success experienced (Bandura, 1997). Moreover, self-efficacy seems to affect task-related stress and life satisfaction in general (Dorfman, Holmes, & Berlin, 1996).

Specific research on RSE is limited. Some studies have indicated that findings concerning self-efficacy in other contexts can be applied to retirement (Fretz, Kluge, Ossana, Jones, & Merikangas, 1989; Taylor & Shore, 1995). Workers with higher RSE tend to plan their retirement in advance and they feel less anxiety concerning retirement. Most of the investigations that include RSE have used single-item measures or much reduced scales without adequate psychometric analysis. Among these studies, one of them simply asked the participants to rate their skill to adapt to retirement and to indicate the effective adjustment opportunities they thought were available to them (Fretz et al., 1989). Another study used only 4 items related to people’s confidence in an easy adjustment, expectations of adjustment problems, feelings about the transition, and their expected enjoyment when they retired (Taylor & Shore, 1995). In these investigations, the level of RSE correlated positively with health, attitudes toward retirement, and planning, and negatively with anxiety and depression (Fretz et al., 1989). Taylor and Shore (1995) also found that RSE correlated positively with the early retirement intention and general satisfaction with retirement or anticipated financial satisfaction (Taylor et al., 1997). Studies carried out with a more extensive RSE scale have found positive correlations with life satisfaction and negative relations with anxiety about retirement (Neuhs, 1990, 1991). In spite of these promising findings, these studies had a limited generalizability because the samples were collected from only two universities. Finally, Harper (2005) developed an RSE scale, called the Retirement Questionnaire, modifying and updating Neuhs’ original version, which has shown adequate psychometric properties. In Harper’s research with 208 workers (university employees), significant correlations between RSE and life satisfaction (r = .54) and between RSE and perceived retirement success (r = .35) have been found.

Finally, some authors have suggested that part of the variability of life satisfaction in people approaching retirement could be due to self-efficacy (Reis & Pushkar, 1993; van Solinge & Henkens, 2005). Thus, the authors maintain that measures of life satisfaction are indicators of the difficulties people undergo when making the transition to retirement and, in this sense, these indicators are affected by their beliefs of general self-efficacy and RSE. In this sense, in this study, we used a measure of life satisfaction that includes several items evaluating satisfaction with specific life areas in retirement (Floyd et al., 1992).

Summing up, considering the specific evidence of RSE and the evidence of general self-efficacy, it is necessary to provide a reliable and valid instrument to appraise the RSE perceptions of people approaching retirement. Therefore, this study has the following two goals: (a) to analyze the psychometric properties of the BRSE-11 in a sample of workers under the age of 62, with regard to its reliability and convergent, discriminant, and nomological validity; and (b) to test these properties on a sample of workers over the age of 62.

Method

Participants

This study consisted of two samples. The first one (Sample 1) comprised Spanish workers below 62 years (N = 694), and the second one (Sample 2) included Spanish workers above 62 and below 66 years (N = 593). For Sample 1, mean age was 58.8 (SD = 2.38), 55% were male, and mean job tenure was 35.8 years (SD = 7.5). In Sample 2, mean age was 63 (SD = .9), 56.3% were male, and mean job tenure was 37.8 years (SD = 8). Regarding retirement preferences, in Sample 1, 41% preferred total retirement as soon as possible, 3.5% partial retirement, and 17.5% had no plans. In Sample 2, 40.5% agreed with total retirement, 5.7% with partial retirement, and only 13.3% had no plans.

Procedure

In order to develop the BRSE-11, we followed two steps. First, we translated the original Retirement Questionnaire (Harper, 2005) to the Spanish context. Various experts on retirement translated the items from the original English scale. A back-translation was then carried out by a native English speaker and compared with the original questionnaire. Afterward, the full questionnaire was administered to a pilot sample of aged workers (N = 326). Psychometric analyses of these data allowed us to retain only 11 items with higher loadings in the exploratory factor analysis (EFA). Second, we administered the BRSE-11 to the two samples (workers below 62 and workers above 62 years of age). This step of the study was carried out by means of questionnaires distributed in different organizations by collaborators of the research team, who performed the task after having received precise instructions to homogenize the administration procedure. Participants were informed of the goal of the study, the anonymity of the data collected, and they expressed their consent verbally, after which they completed a booklet containing the diverse scales of the study.

Instruments

BRSE-11

The scale was based on the Retirement Questionnaire (Harper, 2005), the original form of which included 44 items, with six subscales: physical health, mental health, financial, activities, government and pensions, and retirement itself. This brief measure included 11 items, with only three subscales. The questionnaire required participants to appraise their specific RSE on a 5-point scale ranging between 1 (totally disagree) and 5 (totally agree).

General self-efficacy

We used the Spanish adaptation of the General Self-Efficacy Scale (Baessler & Schwarzer, 1996) with 10 items. Previous studies reported adequate reliability measures for this version, ranging from α = .81 (Schwarzer, Baessler, Kwiatek, Schroder, & Zhang, 1997) to .83 (Juárez & Contreras, 2008). In our study, the scale reached higher reliability values: α = .92 for Sample 1 and α = .91 for Sample 2.

Life satisfaction

As a sensitive measure of specific facets of life near retirement, we used the Satisfaction with Life subscale of the Retirement Satisfaction Inventory (Floyd et al., 1992), which included 11 items. Many aspects included are common to other life satisfaction scales (financial resources or interpersonal relations), whereas other aspects are particularly relevant for future retirees, such as access to social services or transportation. Cronbach’s α reliability for the original subscale was α = .81. In our study, the scale reached acceptable reliability values: α = .81 for Sample 1 and α = .82 for Sample 2.

Data Analysis

We conducted descriptive analysis for the items and EFA with Sample 1, using SPSS 20, and confirmatory factor analysis (CFA) with Sample 2, using Amos 19. Cronbach’s α and CFA were used to assess the internal consistency of the RSE-11 in both samples. Finally, we tested the convergent, discriminant, and nomological validity of the RSE-11 through its relationships with general self-efficacy and life satisfaction.

Results

Exploratory and Confirmatory Factor Analyses

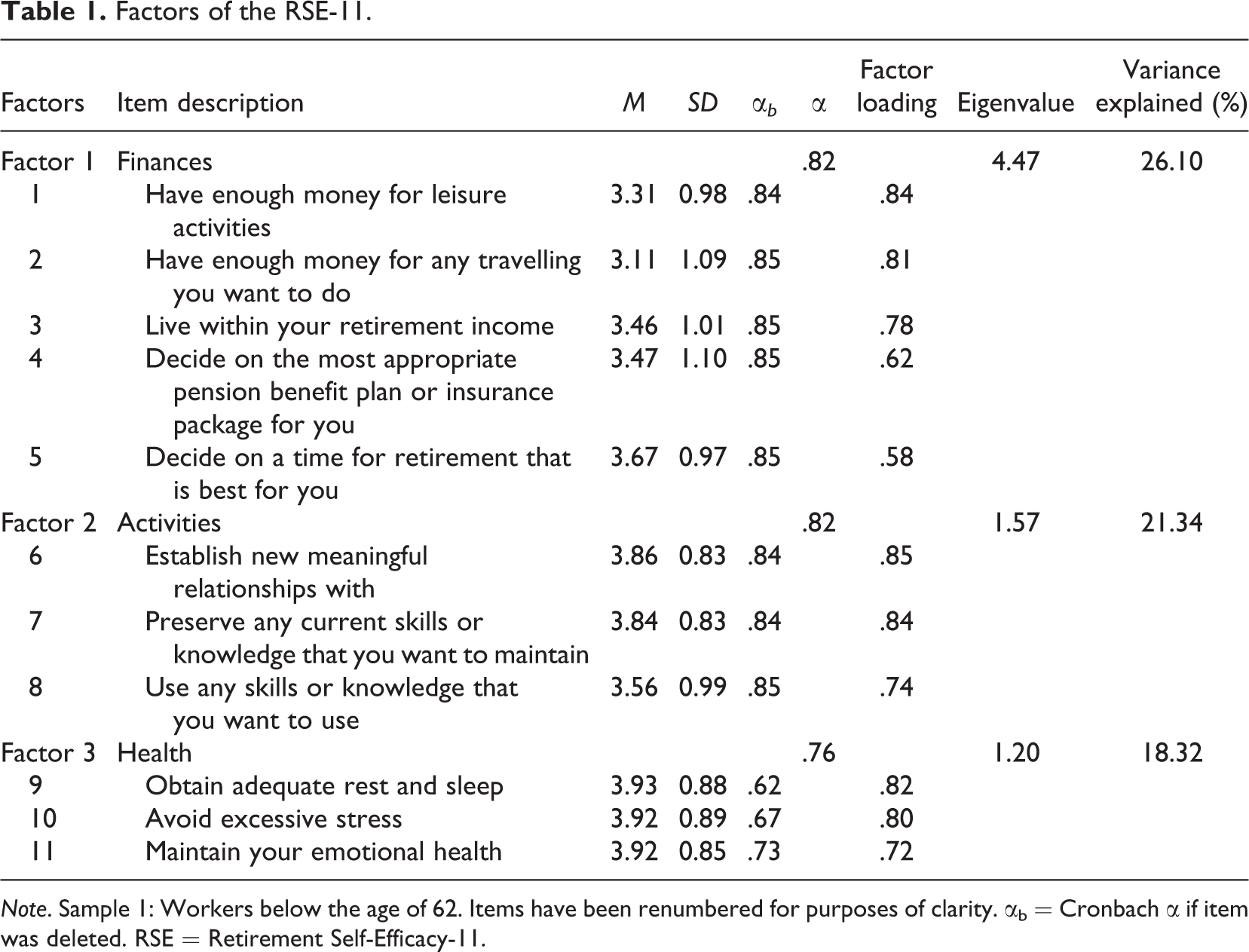

First, we analyzed the psychometric properties of the overall BRSE-11. All items showed an item–total correlation ranging from .62 to .41, and according to Nunnally and Bernstein’s (1994) criteria, all 11 items were retained. EFA was conducted with principal component analysis and varimax rotation. The Kaiser–Meyer–Olkin (KMO) index (.82) and Bartlett’s sphericity test, χ2(55, N = 694) = 3,251.2, p < .000, supported the use of EFA. The KMO criterion supported the three-dimension solution, with Eigenvalues >1. The 5 items loading on Factor 1 (Finances) reflected financial features of retirement and economic decision making. The 3 items included in Factor 2 (Activities) referred to the acquisition and maintenance of valuable relationships, skills, and knowledge. The 3 items loading on Factor 3 (Health) included physical and mental health aspects. We also determined that each item loaded above .40 on its factor and below .30 on the other factors. Psychometric properties of the items in Sample 1 are displayed in Table 1.

Factors of the RSE-11.

Note. Sample 1: Workers below the age of 62. Items have been renumbered for purposes of clarity. αb = Cronbach α if item was deleted. RSE = Retirement Self-Efficacy-11.

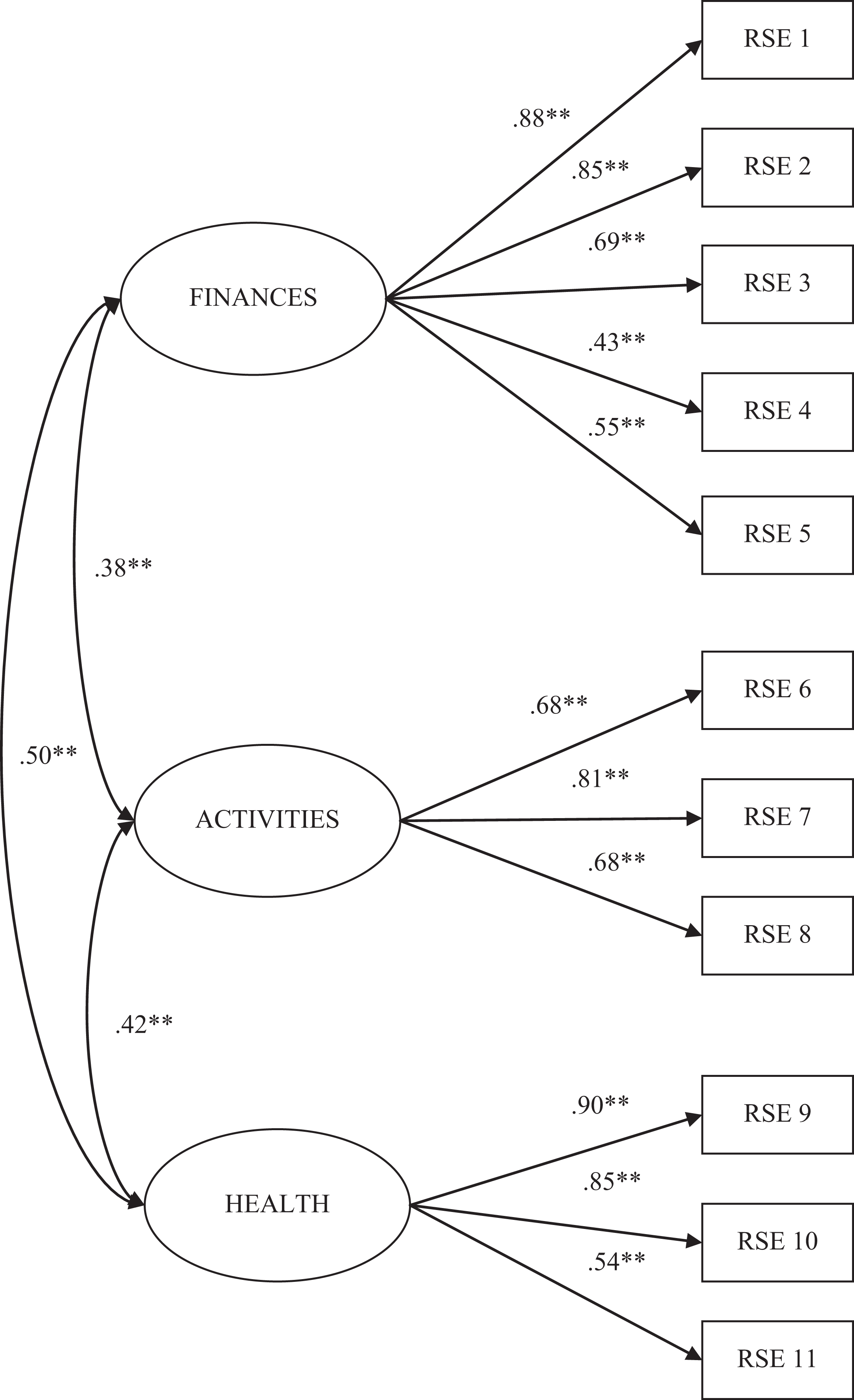

In order to test the fit of the three-factor solution obtained by EFA, we ran CFA with Sample 2, with the maximum likelihood procedure. The goodness-of-fit index (GFI), the adjusted GFI (AGFI), the comparative fit index (CFI), the incremental fit index (IFI), and the Tucker–Lewis index (TLI) must all be over .90. Additionally, the standardized root mean square residual, and the root mean square error of approximation must be below .80, and the χ2/df value must be lower than 3.0. Our results met all the requirements to conclude that the three-dimensional theoretical model exhibits a good fit: χ2(40, N = 593) = 104.06, χ2/df = 2.6, GFI = .97, AGFI = .95, CFI = .98, IFI = .98, TLI = .97. Figure 1 shows the standardized estimates for the model.

Confirmatory factor analysis with BRSE-11 in sample 2 (N = 593). BRSE-11 = Brief Retirement Self-Efficacy-11 Scale.

Considering competitive hypotheses is an important phase of gathering evidence to support the internal structure of the scale (Rios & Wells, 2014). For this purpose, we compared the fit of the three-factor model with that of a single-factor model for the same data. Differences between models were significant (Δχ2 = 909.5, p < .001); therefore, we rejected the most parsimonious model and supported the three-factor solution.

Reliability

Cronbach’s α reliability coefficients of the global BRSE-11 (α = .85) and the three subscales were adequate (ranging from .76 to .82, see Table 1), despite their reduced number of items. These values were confirmed with Sample 2 (global BRSE α = .84, subscales ranging from .76 to .83). Composite reliability (CR) obtained from CFA will be referred to subsequently.

Interrelation of the RSE Scales

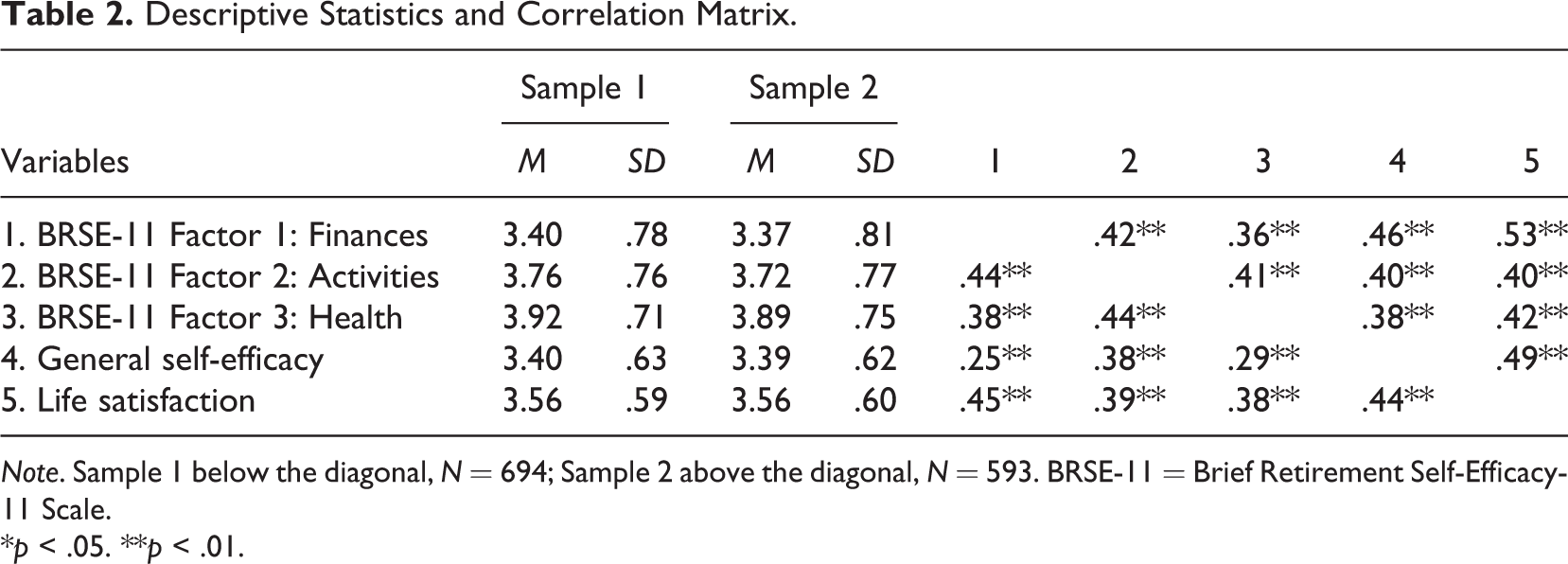

The correlation between the subscales of BRSE-11 was moderate, indicating that the constructs are only slightly related to each other. The subscales with a higher correlation were Health and Activities (r = .44) and Activities and Finances (r = .43), whereas the correlation between Finances and Health was lower (r = .38).

Validity

In order to show that the three factors did not converge sufficiently to be considered redundant, we tested convergent and divergent validity with CFA (Sample 2) following Fornell and Larcker’s (1981) recommendation. The analysis of average variance extracted (AVE) reflects the total quantity of variance of the indicators tapped by the latent construct, and recommended values should be higher than .50. In this study, the AVE of Factor 1 (Finances) was .53, of Factor 2 (Activities) was .50, and of Factor 3 (Health) was .51.

Moreover, in order to address the limitations of Cronbach’s α coefficient, CFA factor loadings can be used to provide a more accurate estimation of reliability through CR, developed by Werts, Linn, and Jöreskog (1974) and recommended by Rios and Wells (2014). Scores should be higher than .70. In this study, the CR value was .83, .72, and .74 for Factors 1, 2, and 3, respectively.

To assess discriminant validity between the constructs, the square root of the mean extracted variance should be higher than the correlation between constructs (Fornell & Larcker, 1981). The results showed that the square root of the mean extracted variance was .73, .71, and .71 for Factors 1, 2, and 3, respectively. In view of these data, the constructs assessed in the model have discriminant validity, although they are all closely related.

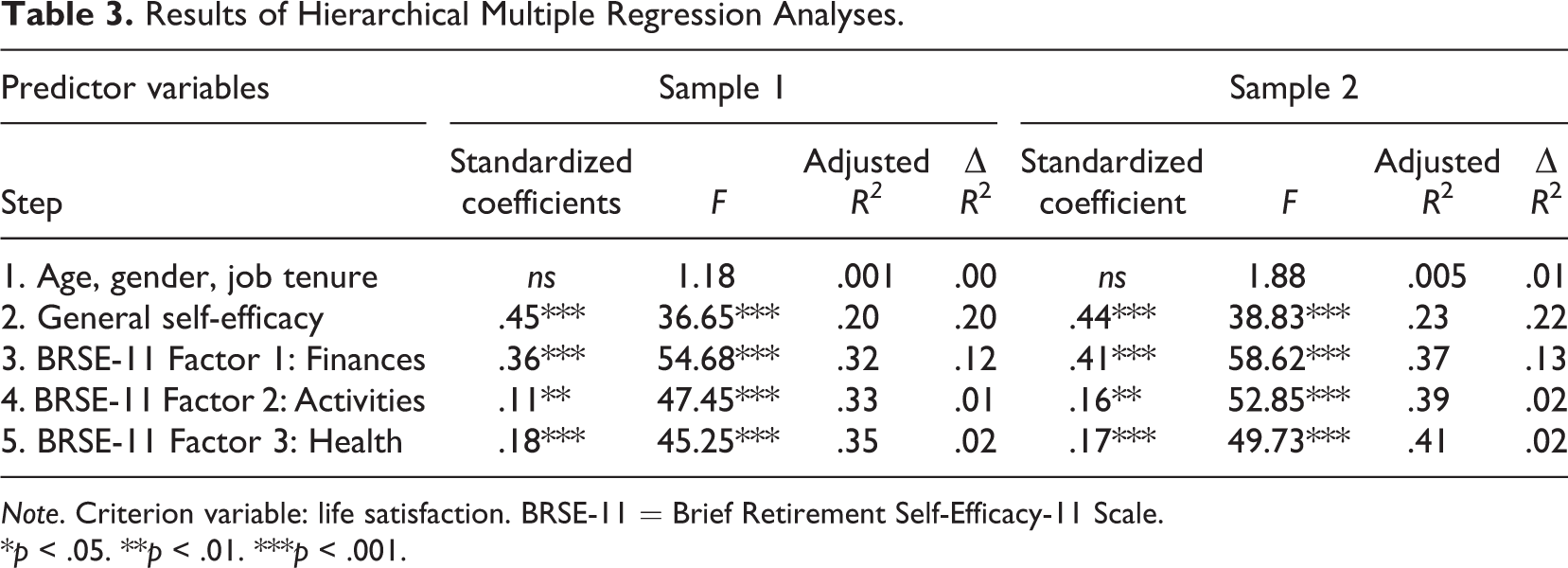

Finally, we explored the nomological network of the BRSE-11 with correlational and regression weight analyses. We found that the three factors of the BRSE-11 (Finances, Activities, and Health) were significantly associated with both global self-efficacy and life satisfaction in both samples of workers (below and above 62 years, see Table 2). Next, using hierarchical multiple regression analysis, we found that the three BRSE-11 factors significantly predicted life satisfaction for aged persons. Each factor was entered in a separate step, and all of them reached statistical significance. Results showed that the percentage of explained variance in life satisfaction significantly increased when retirement self-efficacy was entered in the regression analysis with Sample 1 and Sample 2 (see Table 3).

Descriptive Statistics and Correlation Matrix.

Note. Sample 1 below the diagonal, N = 694; Sample 2 above the diagonal, N = 593. BRSE-11 = Brief Retirement Self-Efficacy-11 Scale.

*p < .05. **p < .01.

Results of Hierarchical Multiple Regression Analyses.

Note. Criterion variable: life satisfaction. BRSE-11 = Brief Retirement Self-Efficacy-11 Scale.

*p < .05. **p < .01. ***p < .001.

Discussion

The aim of this study was to examine the psychometric properties and validity of the BRSE-11. The results showed that the scale has satisfactory psychometric properties. The loadings of the items are stable across the samples, and the factor structure is adequate for both groups of workers (below and above 62 years of age). Reliability values are adequate, despite the reduced number of items. Moreover, the results support the validity and discriminant criteria for the three factors of the BRSE-11. Finally, the nomological network showed that the BRSE-11 has a significant correlation with general self-efficacy. Furthermore, the BRSE-11 predicts life satisfaction both for participants under and over 62 years, and the three factors increased the explained variance in life satisfaction after the introduction of general self-efficacy in the hierarchical regression analysis. Despite the fact that the first factor, Finances, had greater influence on R 2 than the others, all the steps of the regression analysis reached statistical significance.

Only a limited number of studies have utilized instruments to evaluate RSE, and the most comprehensive was the Retirement Questionnaire (Harper, 2005) on which the items for the BRSE-11 were based. Compared with the original, which contains 44 items, the BRSE-11 showed adequate psychometric properties with only 11 items. Moreover, previous studies have had limited generalizability, due to the fact that the employees belonged to only one firm or one University. Our study obtained data from a broad sample of workers under 62 years in the first step, and we subsequently conducted the second step with workers aged between 62 and 65 years, obtaining results that allow us to validate our findings with older workers.

This study has several weaknesses and limitations that should be mentioned. Concerning the size and representativeness of the samples, the limitations of this study are that the sample is nonrandom, it is not representative and the results cannot be generalized to other populations. Moreover, all the data proceed from self-reports, which can include a source of uncontrolled error from the common variance. Validation using independent criteria, such as health records or responses from relatives and friends will be explored in future studies with this measure. However, because the BRSE-11 is focused on subjective expectations regarding retirement, deviations from external criteria would not necessarily indicate that the BRSE-11 is an invalid instrument. Moreover, these differences may indicate sources of bias in aged workers’ expectations, and ways for counseling and intervention. Also, some aspects were ignored that should be recovered in future investigations. For instance, previous levels of life satisfaction should be taken into account in order to discard its influence. Regarding outcome variables, more objective measures should be included, such as health, assessed through number of diseases or medical interventions.

Regarding internal consistency measures of the subscales, the scores could have been improved by adding more items to assess each dimension. But we had to compromise between eliminating unnecessary items and including enough items to cover all the relevant facets of RSE. In summary, we conclude that the psychometric properties of the BRSE-11 are adequate, and it can be used with sufficient guarantees in order to expand research on predictors of retirement adjustment.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article was funded as part of the actions to aid the dissemination of the Research Promotion Plan of the UNED.