Abstract

We analyze the compliance costs of individual taxpayers resulting from the German income tax (tax year 2007). Using survey data that have been raised between December 2008 and April 2009, we find evidence for a considerably higher cost burden of self-employed taxpayers. Taxable income and a higher education (university degree) are positively correlated with compliance costs, while the time effort of female taxpayers is significantly lower. By contrast, joint filing of married couples reduces the burden of tax compliance. The aggregate cost estimate of German income taxpayers amounts to €6 to €9 billion, respectively, 3.1 to 4.7 percent of the income tax revenue in 2007. This estimate is higher than latest projections in a number of other European countries like Spain and Sweden, but lower than estimates for the United States and Australia.

The economic costs of taxation not only consist of the tax payment itself and the excess burden but also of the time effort and the monetary expenses spent on tax compliance and tax planning. As these operations are at least partially caused by tax regulations and compliance obligations, they are to be interpreted as an additional “tax effort” reducing the economic resources of individuals without increasing the fiscal budget of the government. Therefore, compliance costs have a negative impact on the efficiency of a tax system (Alm 1996) and increase the marginal costs of funds (Slemrod and Yitzhaki 1996). They may also affect tax evasion and tax avoidance (Alm 1999; Erard and Ho 2003).

In spite of a comprehensive literature on the compliance costs of individuals in countries like Australia, Canada, Spain, the United Kingdom, and the United States (for a review of the literature see, e.g., Evans 2003, 2008), empirical evidence for Germany as the largest EU economy is scarce. There have been two studies on compliance costs of individuals that are exclusively available in German language (Tiebel 1986; Rheinisch-Westfälisches Institut für Wirtschaftsforschung [RWI] 2003; for research on business taxpayers, see Kayser et al. 2004; Eichfelder and Schorn 2012). The analysis of Tiebel (1986) is outdated and rather poorly documented. The survey data of RWI (2003) has not been used for an analysis of the key cost drivers or for projecting an aggregate cost estimate and is publicly not available. Therefore, the compliance burden of German individuals resulting from the personal income tax is still an open question of research.

There are specific properties of the German income tax that might be interesting from an international perspective. In contrast to self-reporting systems like in the United States, German taxes on income are calculated by the fiscal authorities. Hence, the taxpayer is committed to declare the taxable earnings and deductions, but not to calculate the taxable income and the tax payment. This may reduce compliance costs of private households by cost of the administration. Furthermore, German wage earners are typically not obliged to file an income tax statement if their income does not include a significant amount (more than €410 per year) of nonwage earnings. This is due to the detailed German pay-as-you-earn (PAYE) system and implies a reduction of compliance costs of private households by cost of the employers. Another important aspect is the possibility of married adults to file jointly. In these cases, the sum of taxable incomes of both spouses is divided by two to calculate the average tax rate and the tax payment.

In addition to cost measurement, the identification of the key cost drivers is an important question of research. If the compliance burden is correlated to sources of income, one may expect that tax complexity not only affects the household’s resources but also the economic decision making. For example, Blumenthal and Slemrod (1992) observe higher compliance costs for self-employed taxpayers that might negatively affect self-employment and impair economic growth (Djankov et al. 2002; Grilo and Irigoyen 2006). Furthermore, the identification of the key cost drivers may help simplify the tax system.

In our contribution, we analyze the time effort and the monetary expenses of German self-employed persons and wage earners resulting from the personal income tax. Our investigation is based on survey information raised between December 2008 and April 2009 within a project that was funded by the German Ministry of Finance. The data include cost estimates as well as socioeconomic information on private taxpayers and allow us to approximate the aggregate income tax compliance burden of German households. Furthermore, we investigate for the first time the key cost drivers of the compliance burden in Germany.

We find that the compliance costs of German households amount to €6 to €9 billion or 3.1 to 4.7 percent of the personal income tax revenue in the tax year 2007 (including solidarity tax surcharge as a supplement of 5.5 percent to the German personal income tax). This is higher than latest empirical results for Sweden and Spain, but lower than cost estimates for Australia and the United States. Combining our result with previous research, it can be stated that compliance cost estimates of US households are significantly higher compared to studies for other countries.

Regarding the key cost drivers, we find a clearly positive effect of taxable income, education, and self-employment, while the positive effect of age is only significant in a Heckman specification. We also find a lower time burden for females. In addition, the compliance burden of married dual-income earners is considerably lower compared to other households with an identical taxable income. This can be taken as evidence that the joint taxation of married couples not only accounts for horizontal equity but also enhances the cost-efficiency of the income tax.

This article is organized as follows. In the second section, we exemplify our database including the sampling and the methodology of cost measurement. In the third section, we describe the multivariate analysis identifying the determinants of the compliance cost burden. The aggregate burden of the German income tax is projected in the fourth section including a comparison to international estimates. The fifth section presents our conclusions.

Data Set

Methodology, Sampling, and Cost Measurement

Similar to previous research (Evans 2003, 2008), our analysis is based on a survey of private households. As documented by the literature (Sandford 1995; Blažić 2004; Evans 2008), mail surveys on tax compliance costs may be significantly biased by misunderstandings and mistakes of survey participants. In addition, nonresponse is an important problem. In Germany, response rates of the latest surveys on compliance costs of households and businesses lie in a range of 7.3 percent to 8.6 percent (RWI 2003; Kayser et al. 2004; Eichfelder and Schorn 2012).

According to the literature on cost measurement, personal interviews are typically regarded as more reliable (Sandford 1995; Blažić 2004). In addition, nonresponse is expected to be lower. Therefore, it was decided to select the cost data by face-to-face interviews. All interviewers were informed on the term tax compliance costs and other aspects of the questionnaire by a training seminar. The data were collected between December 2008 and April 2009 as part of a policy–advisory project funded by the German Ministry of Finance.

While the use of face-to-face interviews in general can be regarded as a major benefit of our database, there is also a number of disadvantages. First of all, funding was not sufficient to conduct interviews in all parts of Germany. Thus, sampling was focused on the German member states Berlin and Brandenburg. From our perspective, this does not greatly affect our results, as there are no regional disparities with regard to the German income tax law and our analysis controls for important socioeconomic parameters (see the `Multivariate Analysis' and the `Estimation of the Aggregate Burden' sections).

A bigger challenge emanates from the typically low-response rates of Germany (usually below 10 percent) in conjunction with the project’s budget constraints. As the generation of a representative random sample with a sufficient number of usable responses for all relevant household types was not regarded as realistic, interviewers had to select subjects based on a quota plan considering gender, age, education, and monthly net income. The corresponding frequency in the population was taken from the 2008 statistical yearbook for Germany (German Federal Statistical Office 2008b).

While quota sampling has been frequently used in economic research (e.g., Throsby and Withers 1986; Gallopel-Morvan et al. 2010), it does not result in a probability sample. This might affect the representativeness of cost estimates if cost-relevant characteristics have not been considered by the quota plan. For example, taxpayers with certain cost-relevant characteristics may have been neglected. Nevertheless, there is some evidence that quota sampling does not differ significantly from random sampling (e.g., Cumming 1990).

While the use of quota sampling is clearly a “second best” strategy, it may nevertheless be a convenient approach to analyze the tax compliance burden of private households in Germany. As already mentioned, response rates of German cost surveys are typically low. In addition, nonresponse may be related to the compliance burden (e.g., Allers [1994] reports evidence for an underestimation of costs due to nonresponse) and other observable and unobservable characteristics and could, for example, be lower for self-employed taxpayers with a limited amount of spare time. In a recent survey, Hansford and Hasseldine (2012) report a response rate of only about 1 percent for self-employed taxpayers and small and medium-sized enterprises in the United Kingdom. Hence, while the master sample of a representative mail survey will be statistically random, the usable response will probably not be. In addition, quota sampling is less costly and face-to-face interviews may increase the validity of cost estimates.

Notwithstanding, using a non-probability sample might be a problem. To account for this, we tested for the representativeness of our sample with regard to seven socioeconomic characteristics: level of net income, gender, age, self-employment, education, marital status, and the fact if a tax return has been filed. While we find no significant differences regarding the level of net income, gender, age, education, and the amount of non-filers, we detect deviations concerning profession and marital status. As suggested by Berinsky (2006), we calculate weighting factors for adjustment.

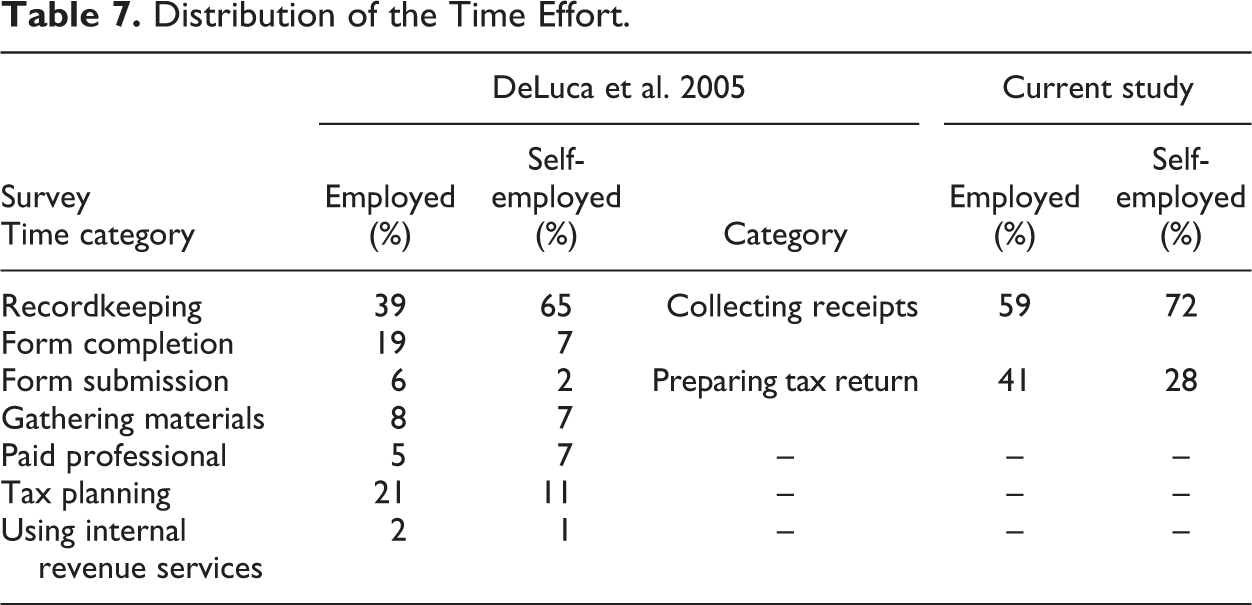

Similar to previous research (Evans 2003, 2008), costs are measured by the monetary equivalent of the compliance effort and additional monetary expenses (e.g., for a tax advisor). The questions in the survey instrument were based on previous German research on tax compliance costs (RWI 2003). Therefore, the measurement of the time effort was mainly focused on the preparation of the income tax return and the collection of receipts for compliance purposes. The questionnaire asked also for the monetary expenses allocated to tax compliance (paid preparation, software, etc.) and for the person who prepared the income tax return (taxpayer, spouse, tax preparer, and other person).

In addition, the survey instrument included questions on socioeconomic information (age, marital status, sex, educational level, and number of children), and the occupation of the taxpayer and the taxpayer’s spouse (self-employed, employed, public official, other). Information on income was regarded to be a sensitive issue that could negatively affect survey response. Therefore, the survey instrument asked not for the household’s taxable income but for monthly net income classes. Using additional information on the employment status, we were able to construct a proxy variable for taxable income. For the corresponding methodology and an English version of the survey questionnaire, see Blaufus, Eichfelder, and Hundsdoerfer (2011).

While the applied approach of compliance time measurement should have been appropriate to capture the main compliance activities (filing the tax return as well as collecting receipts and related bookkeeping activities, see DeLuca et al. 2005), the number of requested compliance activities is smaller than in previous studies and the cost definition is more narrow (e.g., Blumenthal and Slemrod 1992; Vaillancourt 2010). For example, the questionnaire did not include a precise question on tax planning or tax accounting in the broader sense. As a result, the aggregate burden might have been underestimated if corresponding cost elements have not been regarded by the survey participants.

On contrary, it may be argued as well that survey instruments with a high number of cost categories may result in overestimated cost burdens. The reason is that compliance activities, as mentally represented, are usually not exclusively related to one compliance-cost category. Therefore, if compliance hours are allocated to more than one category, double counts are possible. For example, there has been criticism that general accounting obligations (bookkeeping, etc.) might have been declared as tax compliance costs (Sandford 1995; DeLuca et al. 2005). In addition, theoretical and empirical accounting research suggests that measurement error might increase in the number of cost categories due to misallocation bias (Cardinaels and Labro 2008). With regard to (tax) compliance cost measurement, Klein-Blenkers (1980) provides evidence that cost estimates increase in the number of cost categories. 1 Therefore, while it is not certain that more categories increase the reliability of cost estimates, a different number of cost categories affects in any case the comparability of results among different cost studies.

An additional problem of cost measurement results from the monetization of the compliance time effort. There is no universally accepted method regarding this aspect and this is one reason why international comparisons of compliance burdens are delicate. For example, Slemrod and Sorum (1984) rely on the taxpayer’s post-tax earnings per working hour, Sandford, Godwin, and Hardwick (1989) on subjective estimates of the taxpayer, Allers (1994) on average gross domestic product per working hour and Vaillancourt (2010) on the taxpayer’s gross earnings per working hour.

According to Wallschutzky (1995), taxpayer’s own valuations of the time burden may not be consistent over a number of repeated interviews and could be biased. From this perspective, the taxpayer’s wage rate appears as a more appropriate method to obtain a monetized time burden. Assuming a neoclassic choice between labor and leisure, a rational taxpayer would assess the marginal working hour with its marginal value of consumption, respectively the net wage. However, this value does not hold from a society perspective if the alternative to compliance work is another income-generating activity (e.g., self-employment; Tran-Nam et al. 2000).

Due to the problems of time measurement and monetization, we decided to calculate a lower- and an upper-bound estimate of the compliance burden. A corresponding approach accounts for the possibility of measurement error and enhances the comparability of our results with other studies. Furthermore, we are able to control for the approach of cost measurement in our multivariate analysis. To calculate a lower-bound estimate, we use the time estimates as reported in our survey instrument and rely on average after-tax earnings per working hour (Blumenthal and Slemrod 1992; Blažić 2004). For the monetization of the upper-bound estimate, we rely on pretax earnings per working hour (Vaillancourt 2010). In addition, we use previous evidence on the allocation of the compliance time effort (DeLuca et al. 2005) to adjust for a potential underestimation of time estimates. 2

The pretax and the post-tax incomes per working hour for different income classes have been calculated on the basis of the German Socio-economic Panel (GSOEP; for a thorough description of the GSOEP, see Wagner, Frick, and Schupp 2007). We use the wage based on the actual working hours instead of the contractual working hours. 3 As our article focuses on compliance costs from a society perspective, we do not account for the (partial) tax deductibility of monetary expenses in the German income tax code. We also do not consider cash flow benefits resulting from the delay between the generation of profits and the payment of tax installments (for a detailed description of these effects, see Blažić 2004).

Sample Selection and Descriptive Statistics

Our gross sample consists of 1,009 interview questionnaires. We excluded all cases with inconsistent cost estimates and missing information on parts of the compliance burden and other important variables (115 observations). Thus, the remaining total sample includes 894 subjects. As has been mentioned in the previous section, we use weighting factors to account for a potential sample selection bias.

It has been stated that not all members of the German working population are obliged to file a tax return by reason of the PAYE system. As all necessary compliance activities of non-filers are conducted by the employer, this group does not bear a significant compliance burden. In our data, 265 participants did not file an income tax return (26.3 percent of all 1,009 survey respondents), while the other households may have filed either by choice or by obligation. 4 This demonstrates a significant cost reduction of German households resulting from the PAYE system. As our focus is on households with a compliance burden, we excluded non-filers from our final sample leaving 629 subjects with full information on compliance time and monetary expenses.

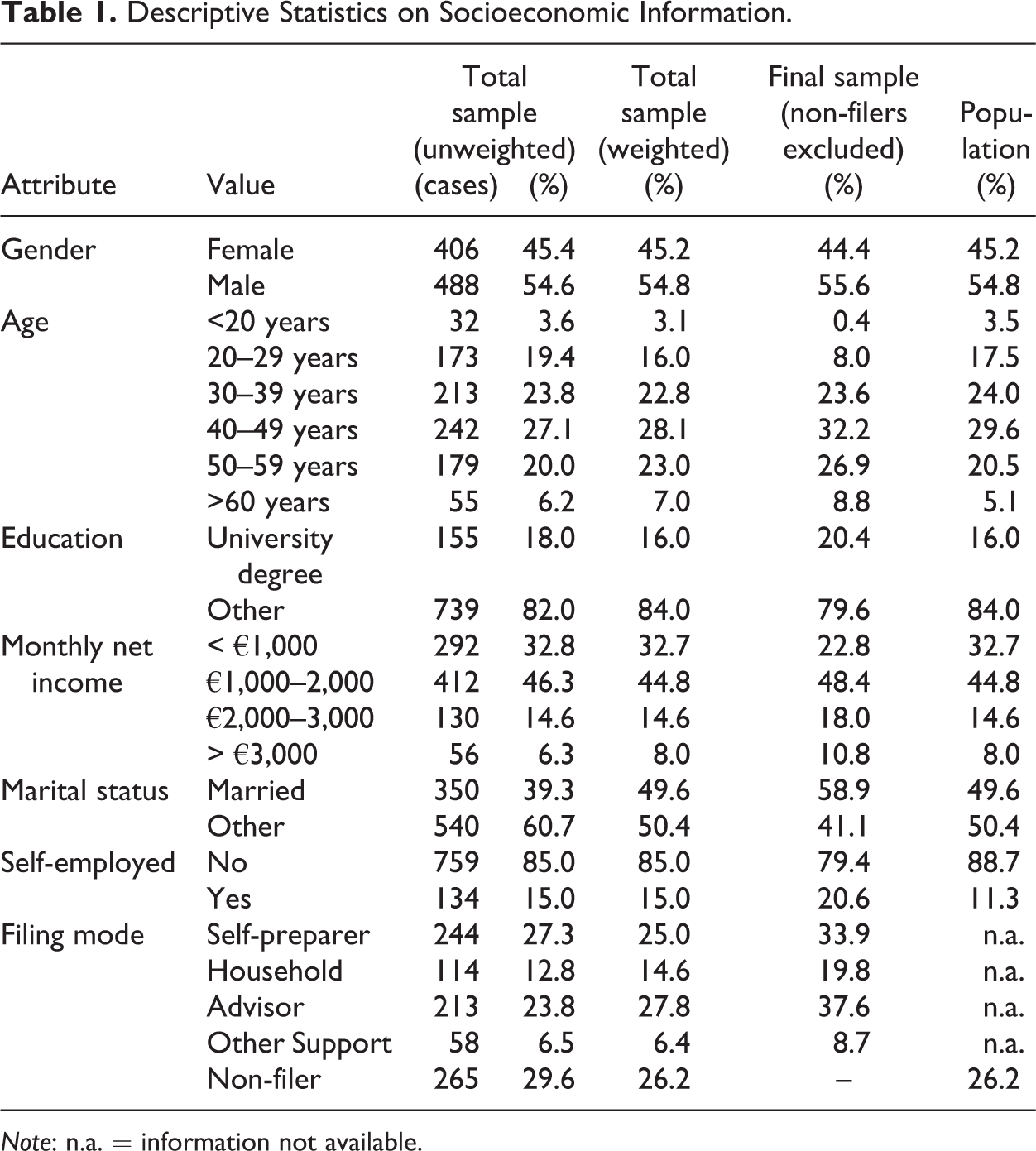

The descriptive statistics on socioeconomic factors of our total sample (894 subjects, unweighted and weighted), the final sample (629 subjects, weighted), and the underlying population are displayed in table 1.

Descriptive Statistics on Socioeconomic Information.

Note: n.a. = information not available.

Most of the respondents in our final sample are males (56 percent), are employees (79 percent), are married (59 percent), and have an age between 30 and 59 years (83 percent). About 20 percent have a university degree. The widest deviations from the population can be observed with regard to marital status. As previously mentioned, we adjust for these deviations by the calculation of weights.

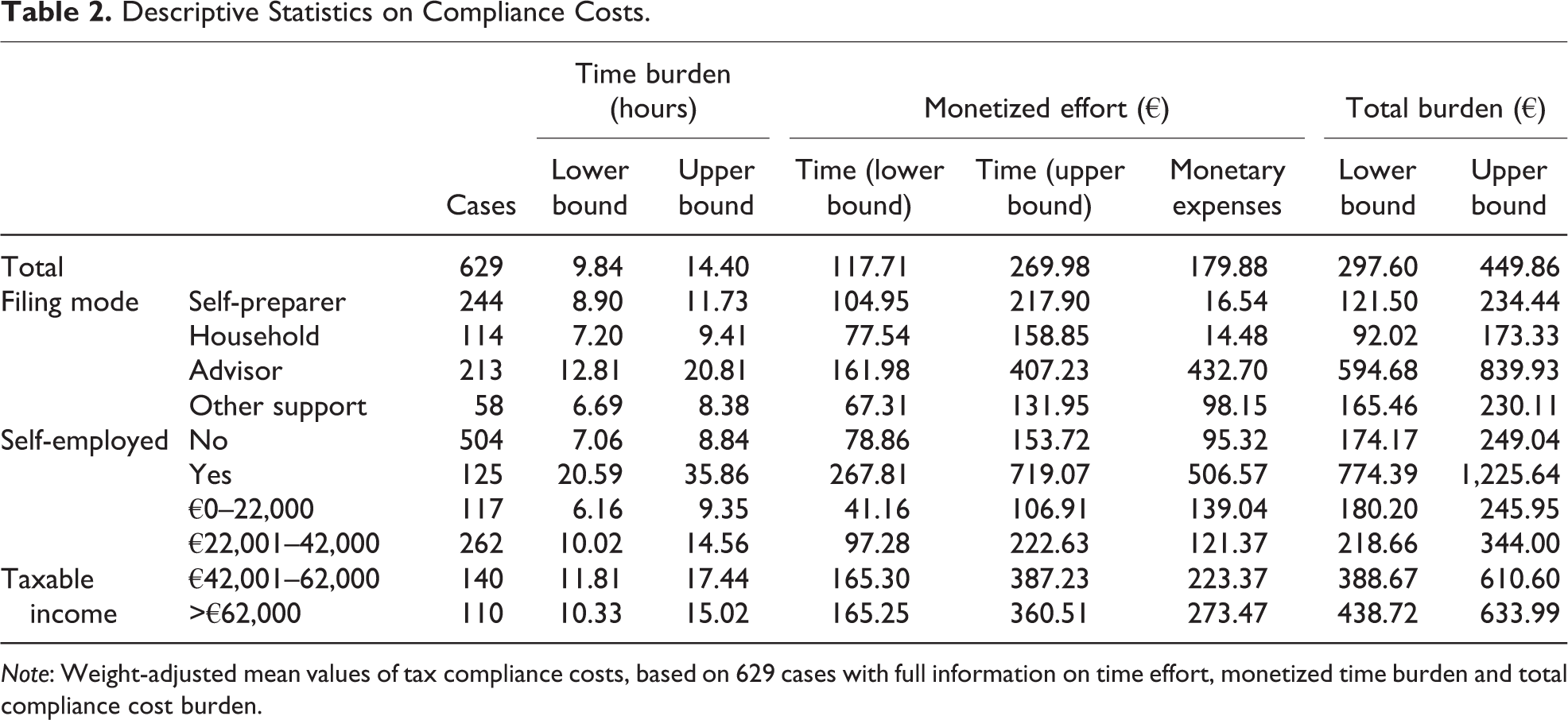

In table 2, we present weight-adjusted mean values of the lower-bound and the upper-bound cost burden for a number of subsamples of our final data set. The four income groups have been selected to include a sufficient number of taxpayers per employment-income cell (see table 3). On average, a survey respondent spends between 9.8 hours (lower-bound estimate) and 14.4 hours (upper-bound estimate) on collecting receipts and preparing the income tax return. This is in line with previous research. Tiebel (1986) reports on average 11.2 hours for a German household (including the compliance costs of the German wealth tax), while RWI (2003) estimates the time effort with 15.8 hours (not adjusted for weights). In addition to the time effort, an average respondent in our data has monetary expenses amounting to €180.

Descriptive Statistics on Compliance Costs.

Note: Weight-adjusted mean values of tax compliance costs, based on 629 cases with full information on time effort, monetized time burden and total compliance cost burden.

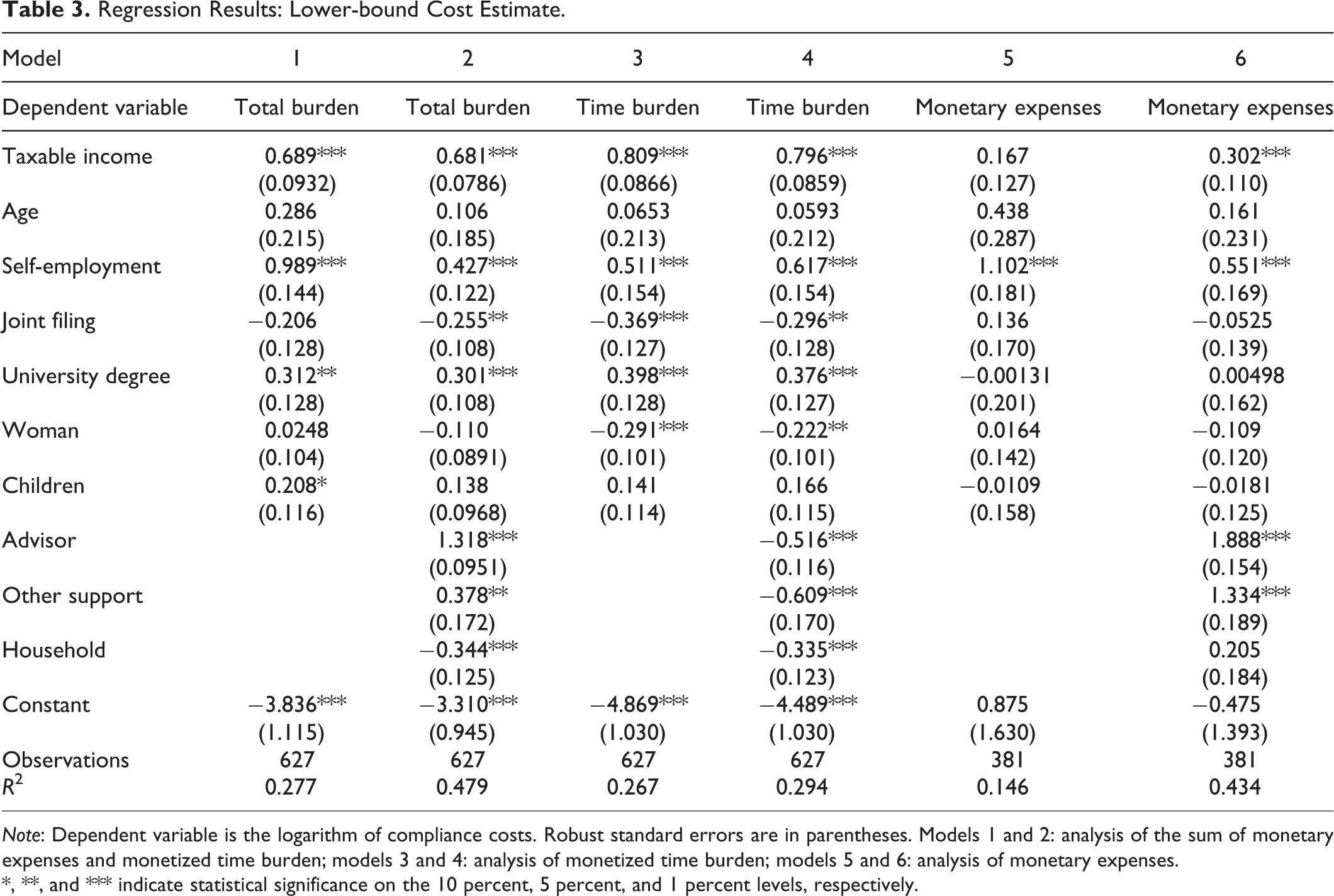

Regression Results: Lower-bound Cost Estimate.

Note: Dependent variable is the logarithm of compliance costs. Robust standard errors are in parentheses. Models 1 and 2: analysis of the sum of monetary expenses and monetized time burden; models 3 and 4: analysis of monetized time burden; models 5 and 6: analysis of monetary expenses.

*, **, and *** indicate statistical significance on the 10 percent, 5 percent, and 1 percent levels, respectively.

About 64.4 percent (6.3 hours) of the time burden result from the collection of receipts (lower-bound estimate). Therefore, the documentation requirements in calculating taxable income are the most time-consuming compliance activity. This corresponds to previous research on the compliance costs of income taxation in Germany (RWI 2003) and other countries (Vaillancourt 1989; Blumenthal and Slemrod 1992; Delgado Lobo, Salinas-Jiménez, and Sanz Sanz 2001). Total average compliance costs range from €298 to €450. Average monetary expenses are making up 40.0 to 60.4 percent of the total burden. While the upper bound (60.4 percent) corresponds to Sandford, Godwin, and Hardwick (1989), the lower bound is in line with Allers (1994), Delgado Lobo, Salinas-Jiménez, and Sanz Sanz (2001), and RWI (2003) with a monetized time effort of about two-thirds of the compliance burden.

As has been reported by previous research (Blumenthal and Slemrod 1992; Tran-Nam et al. 2000), the burden is unequally distributed among taxpayers. From table 2, it becomes obvious that compliance costs are positively related to taxable income and self-employment. The average cost of an employee lies in a range of €174 to €249, while the corresponding burden of a self-employed is about four to five times higher (€774–1,226). In addition, we observe a correlation between total costs and the filing mode with considerably higher costs for taxpayers using a tax advisor. By contrast, cost differences are limited if the tax return has been filed by the survey respondent (Self-preparer), by another household member (Household), or by another person (Other support).

Multivariate Analysis

Estimation Approach

In line with the literature (Vaillancourt 1989, 2010; Blumenthal and Slemrod 1992), we analyze the compliance burden of German households by an ordinary least squares model. Due to economies of scale within the compliance process, we choose a log–log specification. This specification ensures the normality of the model’s residuals (tested by a Kolmogorov–Smirnov test) and allows for an interpretation of regression coefficients as elasticities. For example, a regression coefficient of −0.3 implies that an increase in the exogenous variable of 1 percent reduces compliance costs by 0.3 percent. In case of dummy variables, this reasoning does only hold approximately, due to the fact that a marginal increase in a dummy variable is not possible (like a 1 percent increase in being a woman). Therefore, the estimated coefficients have to be recalculated to obtain the correct relative effect on the compliance burden. 5

As income measure, we rely on a proxy for taxable income (for the calculation, see Blaufus, Eichfelder, and Hundsdoerfer 2011). From an accounting perspective, the number of required tax calculations and relevant tax positions will increase in pretax earnings. The same holds for the number of income sources (e.g., capital earnings). In addition, standard deductions and blanket allowances are more relevant for low-income taxpayers. Therefore, taxable income accounts also for the complexity of a tax return. The baseline model can be described by

The error of the individual i is described by

CCOST: Compliance costs are calculated as the logarithm of the sum of monetary expenses and the monetized time burden (lower-bound estimate and upper-bound estimate). In addition, we analyze the logarithm of the cost components (time burden and money burden).

TAXABLE INCOME: Logarithm of our taxable income proxy.

AGE: Logarithm of the age of our survey respondents.

SELF-EMPLOYMENT: Dummy variable for self-employed taxpayers.

JOINT FILING: Married couples in Germany are entitled to a joint tax return. Due to economies of scale, this could result in a decrease of the cost burden. That holds especially if both household members are income earners (in other cases, the second spouse would simply not file a tax return). Thus, we include a dummy variable for married couples in case of dual-income earners.

UNIVERSITY DEGREE: Dummy variable for respondents with a university degree.

WOMAN: Dummy variable for female taxpayers. If the return has not been filed by another household member, we rely on the sex of the survey respondent.

CHILDREN: TheGerman tax law provides child benefits depending on the number of children, child age, and the occupation of a child. Therefore, we include the logarithm of the number of children entitled to child benefits increased by one (this is to prevent undefined logarithmic values).

A problem of equation (1) lies in the fact that we control for the complexity of a tax return only to a limited extent (mainly by TAXABLE INCOME and SELF-EMPLOYMENT). This issue, which is typical to corresponding analyses (apart from Vaillancourt [2010] controlling for an impressive number of tax characteristics), could bias our result. To mitigate this problem, we construct additional complexity proxies.

According to the literature (e.g., Slemrod and Sorum 1984; Eichfelder et al. 2012), the demand for external advice is positively correlated to tax complexity. Therefore, we may interpret the demand of a taxpayer for external support as a proxy for the subjective complexity of a tax return (see Eichfelder and Schorn [2012] for an analytical model). Our data include four filing modes: (1) self-preparation by the survey respondent, (2) preparation by another household member (HOUSEHOLD), (3) preparation by a certified tax advisor (ADVISOR), and (4) preparation by another third person (OTHER SUPPORT). Apart from self-preparers as our reference group, we include dummy variables for each filing mode and expect higher compliance costs if the support of tax advisors or other third persons has been requested (as proxies for tax complexity). These dummy variables account also for the reliability of compliance time estimates if the tax return has not been filed by the survey respondent (especially in case of HOUSEHOLD and OTHER SUPPORT).

We account for heteroscedasticity by the calculation of heteroscedasticity-robust standard errors (Huber/White estimator). We also tested for linearity (by a Ramsey Regression Equation Specification Error Test [RESET] for linearity in variables), collinearity (by the calculation of variance inflation factors), and the normality of the model’s residuals. We did not find evidence for a misspecification or bias of our regression models.

Results

Table 3 documents the regression results for the lower-bound cost estimate regarding total compliance costs, monetized time burden, and monetary expenses. For each dependent variable, we estimate one baseline model and one model including dummy variables on filing mode (ADVISOR, HOUSEHOLD, and OTHER SUPPORT) with self-preparation as the reference case.

Corresponding to Vaillancourt (1989, 2010), and Blumenthal and Slemrod (1992), we find a positive impact of taxable income. A 1 percent increase in taxable income increases the total burden by 0.68 to 0.69 percent. This should be driven by three different aspects. (1) The complexity of a tax return increases in taxable income. For example, bookkeeping obligations and claimed deductions should be positively correlated to gross earnings and business transactions. (2) The interest in tax planning is positively correlated with the marginal income tax rate, which increases in taxable income (e.g., Eichfelder et al. [2012] provide evidence for a positive correlation of the marginal tax rate and tax advice). (3) The value of time allocated to tax compliance (opportunity costs) is on average higher for taxpayers with a higher taxable income.

As a result from (3), the impact of taxable income on the monetized time burden is stronger than the effect on monetary expenses. In addition, the regression coefficients for TAXABLE INCOME are clearly smaller than one confirming the well-known economies of scale of tax compliance activities. Hence, the relative cost burden per taxable income is higher for taxpayers with a low taxable income.

In line with the literature (e.g., Vaillancourt 2010), we also find a strong and positive effect of self-employment. This can be explained by the more complex and burdensome compliance and bookkeeping requirements in case of business earnings. Furthermore, the German PAYE system implies a cost reduction for wage earners. While German employers are obliged to comply with the information requirements of wage taxes and social insurance contributions, their employees may use the information of payroll accounting to file their income tax return.

As SELF-EMPLOYMENT and the dummies on filing mode act as complexity proxies and are correlated to each other, it seems to be appropriate to concentrate on the models 1, 3, and 5 to quantify the partial increase of compliance costs resulting from self-employment. Therefore, self-employment increases the cost burden by 166 percent, the time burden by 65 percent, and monetary expenses by 196 percent with the corresponding regression coefficients (marginal effects) of 0.989, 0.511, and 1.102.

We further find a negative coefficient for JOINT FILING, especially in case of the time burden. Therefore, compared to households with one income earner and similar taxable income, the compliance burden of households with two income earners filing jointly is lower. While the effect is partially driven by the valuation of the time burden per hour (the net wage per hour is lower for households with two income earners filing jointly), it implies a reduction of the aggregate compliance burden of the income tax.

This is due to economies of scale within the compliance process. As already mentioned, the estimated elasticity of TAXABLE INCOME with regard to compliance time is smaller than one. Therefore, tax returns for high-income earners are relatively cheap in relation to income. The negative coefficient of JOINT FILING implies that this effect holds even stronger in case of married joint filers. For that reason, joint filing reduces the aggregate burden of tax compliance. Our outcome is to some extent supported by (weak) empirical evidence on the effect of marital status of Slemrod and Sorum (1984) and Vaillancourt (1989). Vaillancourt (2010) finds on the contrary higher compliance costs of married Canadian taxpayers.

We find an increase in the compliance burden and the time burden by about one-third for taxpayers with a UNIVERSITY DEGREE, while the corresponding coefficient for the money burden is not significant. Our result is supported by Slemrod and Sorum (1984), Vaillancourt (1989, 2010), and Mathieu, Waddams Price, and Antwi (2010). From our perspective, there are two possible explanations for this outcome. (1) Taxpayers with a university degree are more interested in compliance work and, especially, in tax planning. By reason of a higher awareness of tax planning opportunities (Alstadsæter and Jacob 2012), they may increase their effort. (2) Due to their higher qualification, taxpayers with a university degree may be less interested in external support (Slemrod 1989). However, self-preparation is not necessarily the most cost-efficient tax compliance strategy (Eichfelder and Schorn 2012). Therefore, if taxpayers with a high qualification are overconfident (do-it-yourself-man), they might demand for external support to an insufficient extent.

Similar to Vaillancourt (1989, 2010), there is further evidence that the time burden of female taxpayers is significantly lower (see Mathieu, Waddams Price, and Antwi [2010] for a somewhat different outcome). Assuming that male taxpayers are more risk-seeking and interested in aggressive tax planning strategies (Croson and Gneezy 2009), our result could be driven by higher planning costs of male taxpayers. Another possible explanation is that women have a different and less complex structure of income. In this case, WOMAN could act as a proxy for tax complexity.

While regression coefficients are typically positive, we do not find significant results for AGE and (apart from model 1) for children entitled to child benefits (CHILDREN). Hence, we cannot provide evidence that the number of children or age is positively correlated with the cost burden. Vaillancourt (2010) reports similar results for age but also weakly significant and positive effects for education deductions in Canada.

We find a higher burden for households demanding for external support from a certified tax advisor (ADVISOR) or another third person (OTHER SUPPORT). This fits well with our hypothesis that both dummies act as tax complexity proxies. The effect is stronger for tax advisors with higher tax knowledge and a higher price level. Corresponding to model 2, ADVISOR (OTHER SUPPORT) increases the total burden by 272 percent (44 percent). For both variables, we observe a reduction of the time burden and a strong increase in the monetary expenses. Therefore, the use of external support substitutes time effort with monetary effort.

In case of tax returns filed by another household member (HOUSEHOLD), there is a significantly lower cost burden. This result is partially driven by lower earnings per hour of households with two adults. Nevertheless, there is also an effect on the number of compliance hours (not reported in table 3). From our perspective, there are two potential explanations for that outcome. (1) Households with two income earners are more cost-efficient due to within-household economies of scale and specialization advantages (similar to the effect of JOINT FILING). (2) If the tax return has been filed by another person in the household, the compliance process is not fully observable by the survey respondent. Therefore, HOUSEHOLD may act as a control variable for a potential underestimation of the compliance burden.

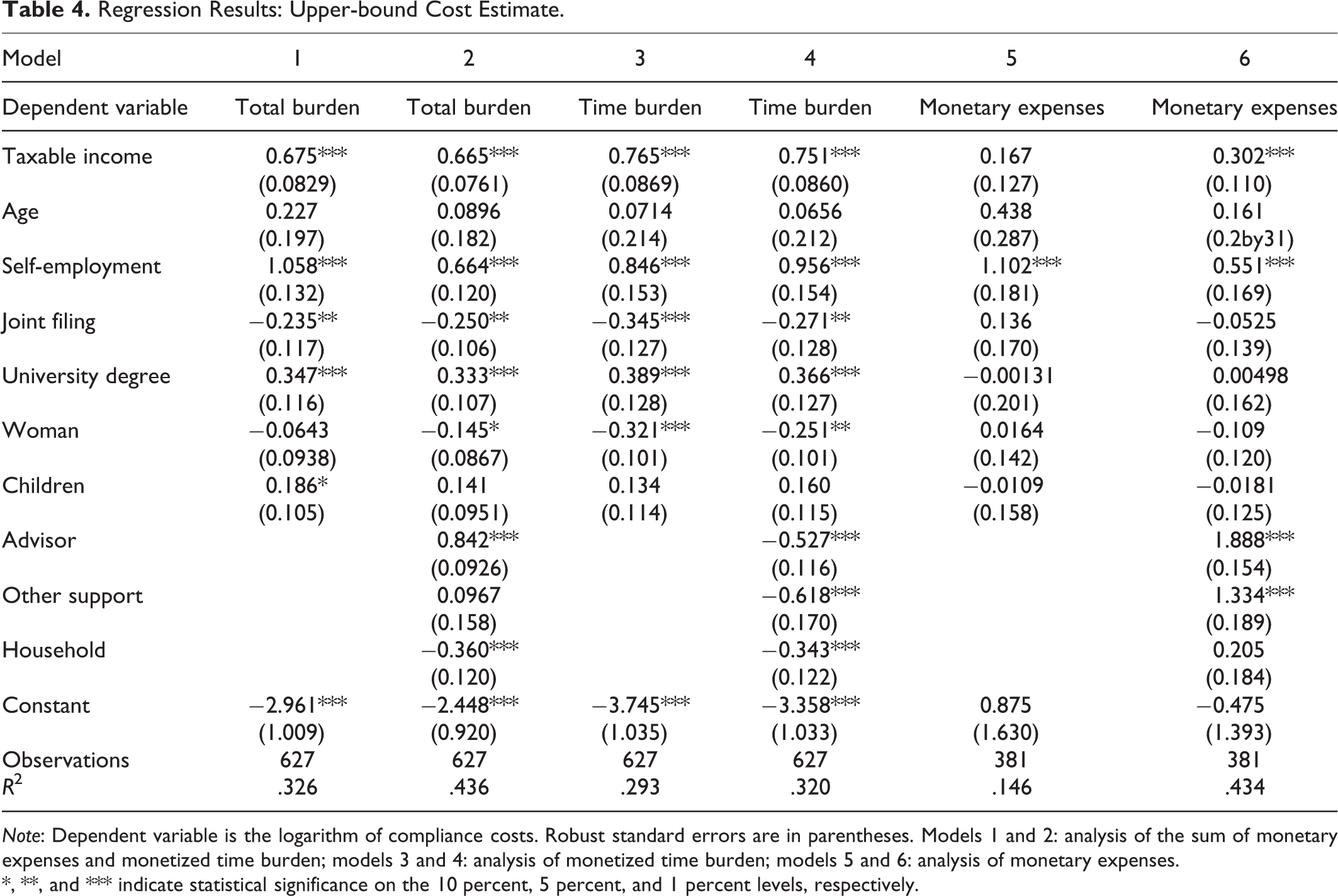

Table 4 documents the corresponding results for the upper-bound cost estimate. It can be demonstrated that our findings are broadly independent of the definition and the valuation of the time burden. Nevertheless, a number of findings are somewhat different. For example, the increase in total compliance costs (monetized time effort) due to self-employment amounts to a higher value of 186 percent (130 percent). Furthermore, there is no significant effect of OTHER SUPPORT on total compliance costs.

Regression Results: Upper-bound Cost Estimate.

Note: Dependent variable is the logarithm of compliance costs. Robust standard errors are in parentheses. Models 1 and 2: analysis of the sum of monetary expenses and monetized time burden; models 3 and 4: analysis of monetized time burden; models 5 and 6: analysis of monetary expenses.

*, **, and *** indicate statistical significance on the 10 percent, 5 percent, and 1 percent levels, respectively.

In addition to our primary results, we calculated a number of cross checks (see also Blaufus, Eichfelder, and Hundsdoerfer 2011). It has already been stated that questionnaire information might be less reliable if the tax return has been filed by another household member or another third person (see also the negative coefficient for HOUSEHOLD in table 4). Therefore, we recalculated our regression models excluding these observations. The results remain generally unchanged. We abstain from reporting these results.

In addition, one might argue that the decision to file a tax return results in a self-selection of households. Therefore, we also estimated a Heckman model using respondents without a tax return for the sample selection equation. Overall, the Heckman results are fairly in line with our baseline case. Therefore, we refrain from reporting these estimates that can be provided upon request. In line with table 1, the Heckman results provide evidence that tax filing is positively correlated with self-employment, taxable income, education, and age. In addition, if we account for the self-selection, we find a positive effect of age (significant) and the number of children (weakly significant) on the cost burden. This fits well with Vaillancourt (2010) and Eichfelder et al. (2012).

Estimation of the Aggregate Burden

In this section, we use the information of our data to project the aggregate burden of the German income tax for private households. Comparing this cost burden to tax revenue, we are able to derive an estimate of the relative burden of the German income tax lying on German households. We discuss our outcome with regard to previous findings.

The calculation of the aggregate burden is based on a microsimulation approach using the scientific use file of the German Income Tax Statistics 2004 (GITS 2004; see German Federal Statistical Office [2008a] for a description). This database includes information on tax returns of about 3.5 million German taxpayers (representative 10 percent random sample). Thus, it is a comprehensive database for the population of German income taxpayers. The GITS 2004 file does not account for education but includes detailed information on the number of tax returns and the filing method.

To use the comparative advantages of both databases (our survey sample adjusted for weights regarding the statistical yearbook 2008 and GITS 2004 file), we derive our aggregate estimate in two steps. In the first step, we use our survey information to calculate the weight-adjusted compliance burden per taxable income for different groups of taxpayers. In a second step, we use the price-adjusted GITS 2004 file to calculate the compliance burden per tax return. Thus, we use the taxable income in the GITS 2004 to simulate the compliance burden by the proportion of compliance costs to taxable income for each household in the scientific use file. An advantage of this approach is that it accounts for potential differences in the distribution of income. Hence, it will be more robust with regard to sample selection.

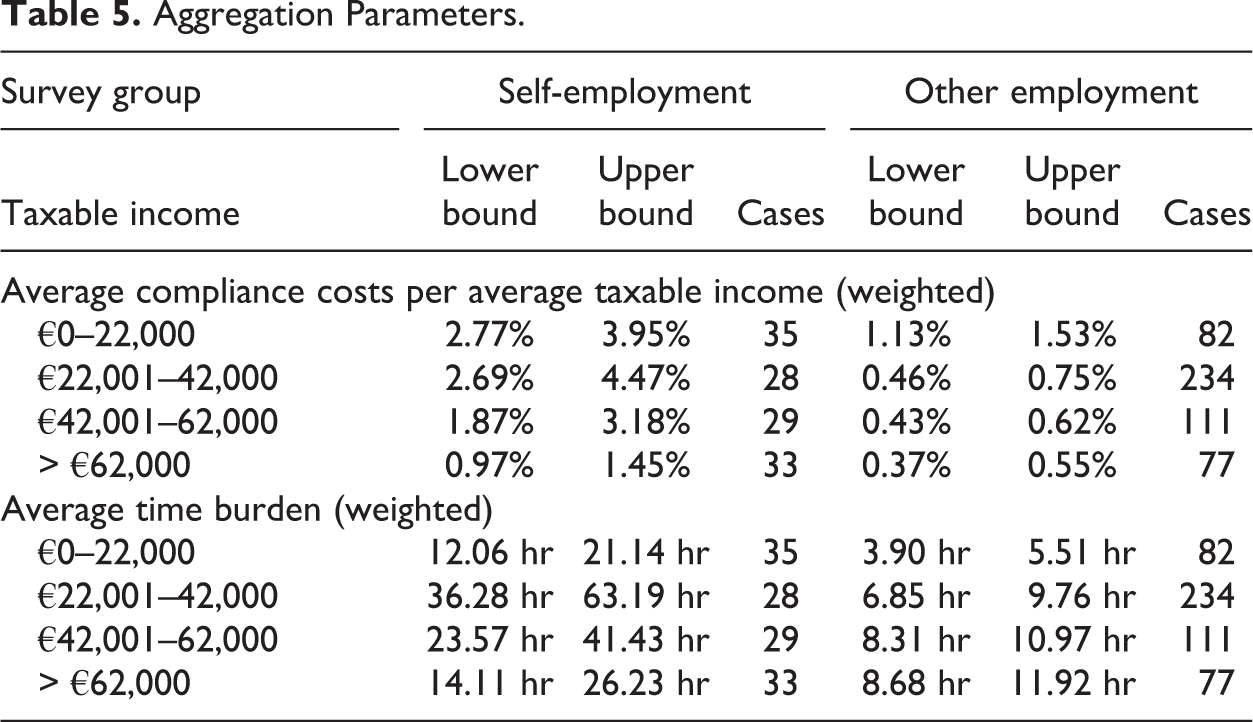

Taking into account that self-employment has been identified as an important cost driver (Slemrod and Sorum 1984; Tran-Nam et al. 2000; Guyton et al. 2003), we differentiate between the compliance costs of self-employed persons and other taxpayers (almost exclusively employees and public officials) with regard to four classes of taxable income (€0–22,000, €22,001–42,000, €42,001–62,000, above €62,000). In order to prevent cost projections to be driven by outliers, our income classes have been selected to include a minimum of twenty-five observations per employment-income cell.

An implicit assumption of our approach is that the compliance burden of other income sources can be approximated by our survey information. It has to be considered that almost all taxpayers in the GITS 2004 file rely either on business income or on employment income as a substantial income source (96.9 percent of all taxpayers and 95.8 percent of all tax filers). Taking further into account that respondents with business and employment income as major income source will have other income sources as well (e.g., capital income, rent income), we do not expect a significant bias of our results.

It has already been mentioned that cost burdens might have been underestimated if the tax return has been filed by another person of the household and not by the survey respondent. Accounting for that aspect, we increase the upper-bound estimate (as our measure for the maximum compliance burden) for these observations using the regression results for the HOUSEHOLD dummy in table 4 (model 2). Furthermore, we compute the ratio of mean compliance costs to mean taxable income instead of the mean of ratios in order to mitigate the effects of potential outliers. The relative cost burdens used for extrapolation are presented in table 5.

Aggregation Parameters.

We find higher relative cost burdens for self-employed persons and households with a low taxable income. That corresponds to economies of scale that have been documented in the literature (Tran-Nam et al. 2000; Blažić 2004). The economies of scale regarding other taxpayers do not seem to be as strong as for the self-employed. This conforms to the literature as well (Sandford, Godwin, and Hardwick 1989; Pope and Fayle 1990).

We use the official income tax statistics to simulate the burden for each tax return. The latest microfile available is from 2004. As our data were collected in 2008 and 2009, we increase the taxable income in the GITS 2004 file by the index of gross wages in Germany from 2004 to 2008 (7.49 percent).

The burden is calculated by the proportion of compliance costs to taxable income (table 5). Households with negative income are assumed to have the same burden as households with an identical amount of positive income. This fits well with the result of Eichfelder et al. (2012) that the demand of German taxpayers for tax advice increases in negative income and accounts for the compliance costs of a tax loss relief. Regarding cases with zero taxable income, we use the average burden for households in the lowest income class (€0–22,000). The lower-bound (upper-bound) value is €401 (€572) for the self-employed and €96 (€130) for other taxpayers. Compliance costs are assumed to be zero in case of no tax return (26.1 percent all cases in the GITS 2004 file).

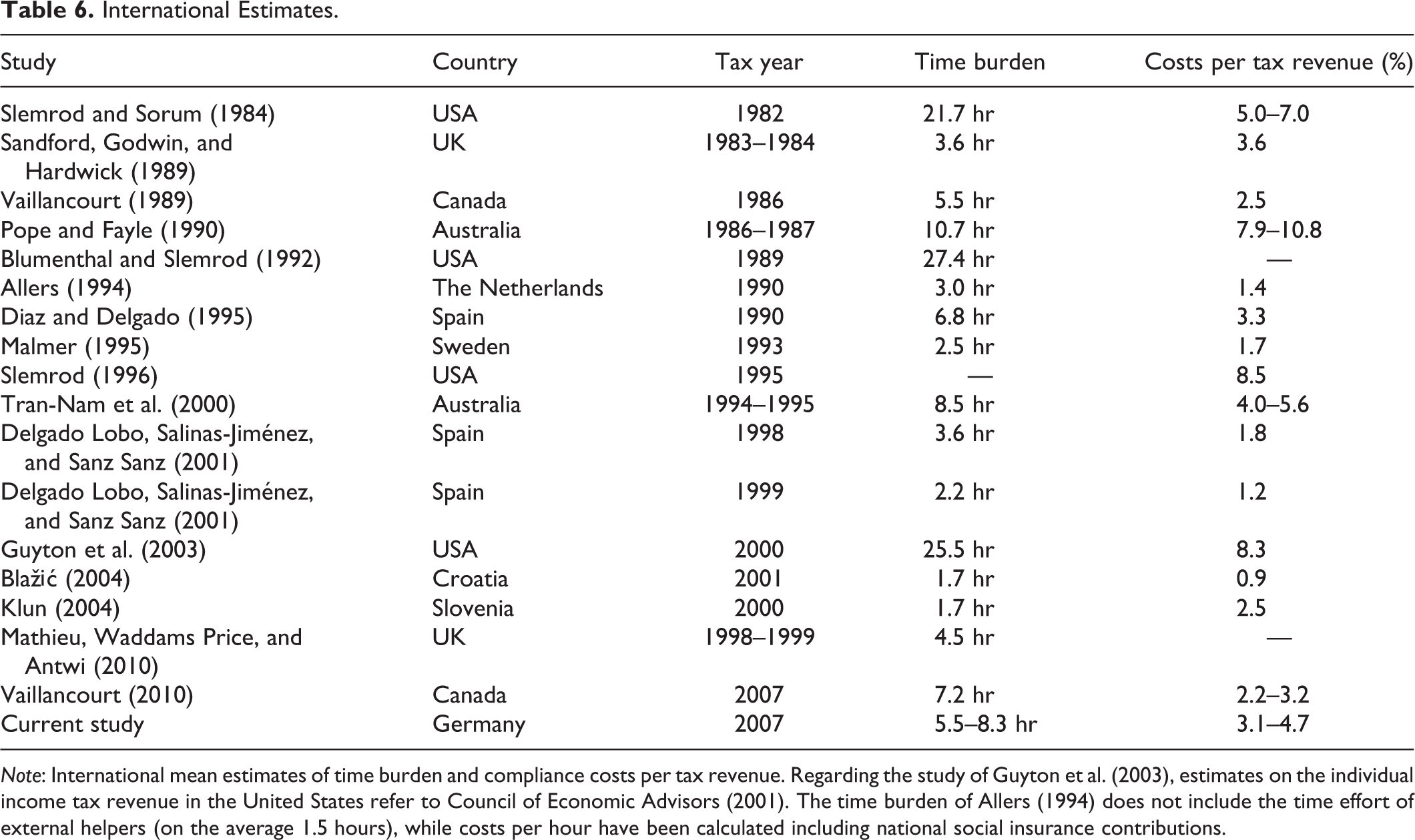

We obtain an overall projected compliance burden of the German households ranging from €6.0 billion (lower-bound estimate) to €9.0 billion (upper-bound estimate). This amounts to 3.1 to 4.7 percent of the German income tax revenue in the tax year of 2007 (including solidarity tax surcharge). By a similar procedure, we calculate a weighted average compliance time per German taxpaying household ranging from 5.5 to 8.3 hours (see table 5 for the corresponding average time effort within each employment-income cell). 6 Table 6 compares these estimates to international evidence.

International Estimates.

Note: International mean estimates of time burden and compliance costs per tax revenue. Regarding the study of Guyton et al. (2003), estimates on the individual income tax revenue in the United States refer to Council of Economic Advisors (2001). The time burden of Allers (1994) does not include the time effort of external helpers (on the average 1.5 hours), while costs per hour have been calculated including national social insurance contributions.

We find that the compliance costs of German households are in the upper middle. While households in latest studies in Canada, Croatia, the Netherlands, Slovenia, Spain, Sweden, and the United Kingdom seem to have a lower burden resulting from the income tax, cost estimates for the United States and Australia are generally higher. In addition, it becomes obvious that cost estimates for the United States are considerably higher compared to all other studies. Taking into account the diversity of survey designs between the various Australian, Canadian, European, and US studies, it is not likely that this outcome is driven by methodological issues. Hence, the results of table 6 can be taken as evidence for higher income tax compliance costs of US households.

A possible explanation for this outcome could be the self-assessment system of the US federal income tax. US citizens are obliged to calculate their tax payments themselves. By contrast, German households are exclusively obligated to file their tax statement, while the tax payment is calculated by the administration. Furthermore, a fraction of about 26.1 percent of the German taxpaying population does not file an income tax return at all by reason of the German PAYE system. German wage earners may also use the information of payroll accounting as basis for filing their tax return. Furthermore, there are a number of complex issues within the US income tax system (divergent state income taxes, alternative minimum tax, a high number of complex tax credits like the earned income tax credit, etc.) that do not exist in Germany. Taking into account the joint effects of the complexity of calculations (e.g., the alternative minimum tax) and the requirements of the self-assessment system, the high tax compliance burden for private households in the United States should not be unexpected.

Nevertheless, it has to be considered that international comparisons on the basis of existing studies can be biased by methodological and theoretical issues. There are at least five aspects of a potential bias: (1) there are differences in sampling methodologies; for example, Klun (2004) and Blažić (2004) do not include self-employed taxpayers with a high cost burden. Therefore, the estimates for Slovenia and Croatia will be biased downward compared to studies including self-employed taxpayers. (2) There are differences in the definition of the cost burden and the design of the survey instrument. (3) The valuation of the time effort is not standardized. For example, Pope and Fayle (1990) use a considerably higher cost value per hour than Tran-Nam et al. (2000). (4) The cost burden per tax revenue is significantly affected by the tax rate. Hence, a low tax rate implies a comparatively high proportion of compliance costs in relation to tax revenue (as tax revenue typically increases in the tax rate). (5) There exist additional compliance costs, costs of the tax administration and tax revenues that are not included within the cost estimates in table 6. Regarding Allers (1994), the cost fraction is biased downward by the fact that this study accounts also for the burden and revenue of national social insurance contributions. In our study, we do not account for the costs of German employers to comply with the income tax. As there is no appropriate data to isolate the compliance burden of German employers resulting from the PAYE system, we refrain from discussing this aspect in more detail.

Conclusion

Within our article, we analyzed the compliance burden of German households resulting from the income tax. To account for the fact that compliance cost estimates may be biased, we calculated a lower- and an upper-bound estimate. We found strong evidence that self-employment increases the burden of tax compliance to a considerable extent. While the average costs of self-employed taxpayers lie in a range of €774 to €1,226, other taxpayers (almost exclusively employees and public officials) bear on average €174 to €249. Accounting for other control parameters, self-employment increases the cost burden by 166 to 186 percent.

Taking into account that the tax obligations of German small businesses and self-employed persons not only include compliance activities for income tax purposes but also duties resulting from the value-added tax, local business taxes, and (in case of an employer) wage taxes, and social insurance contributions, the burden of tax compliance may not only affect the economic resources of private households but also interfere their economic decision making. According to Djankov et al. (2002), market entry costs can negatively affect economic efficiency. Grilo and Irigoyen (2006) find evidence that administrative complexity may impair self-employment.

We also find that income and the demand for external advice positively affect the compliance burden. Furthermore, the time burden of taxpayers with a university degree is significantly higher, while the time effort of female taxpayers is considerably lower. This outcome could be partially driven by the fact that some groups of taxpayers are more interested in tax planning. If well-educated or male taxpayers have lower marginal planning costs or a preference for aggressive planning (Alstadsæter and Jacob 2012), this might result in higher cost burdens. However, Murphy (2004) finds for Australian taxpayers a negative correlation between education and the probability to have an aggressive tax agent.

There is also evidence that joint filing of dual-income earners results in a significant reduction of compliance time. This outcome can be explained by economies of scale that have been also documented in relation to other aspects of the compliance process (Sandford, Godwin, and Hardwick 1989; Allers 1994). This can be taken as an argument that joint tax returns are not only an instrument to ensure tax equity but also a method to enhance the cost-efficiency of a tax system.

Interpreting our results, it should be considered that our data are based on self-reported information of German income taxpayers. Therefore, measurement error is a relevant problem. Furthermore, our database is of limited size (altogether 894 usable observations including non-filers and 629 tax filers) and based on quota sampling. In addition, there are less cost categories than in previous contributions. We rely on face-to-face interviews and post-stratification weights to address these issues. Furthermore, we calculate lower- and upper-bound cost estimates and cross checks for our regressions.

Our aggregate cost estimate of private households resulting from German income taxation lies in a range of 3.1 to 4.7 percent of the income tax revenue (including solidarity tax surcharge). This proportion is higher than the latest cost estimates in other European countries like Sweden and Spain, but considerably lower than corresponding results for Australia and especially the United States. The high cost estimates and time burdens of the US households in relation to Germany and other European countries could partially be driven by the US self-assessment system as well as by the German PAYE system implying a cost reduction for wage earners. Furthermore, the US income tax system includes a number of complex aspects and regulations that are not part of the German tax system (alternative minimum tax, state income taxes in addition to the federal income tax, earned income tax credit, and other issues).

It has to be considered that international comparisons on compliance cost burdens are typically biased by methodological issues including the sampling of taxpayers and the valuation of the time burden. From this perspective, comparative studies will be necessary to get a deeper understanding of the main causes of tax complexity as well as the main possibilities for tax simplification. A corresponding approach should be promising to answer the question of Slemrod (1996), which is the simplest tax system of them all.

Distribution of the Time Effort.

Footnotes

Acknowledgments

We are thankful to James Alm, Timm Bönke, Martin Jacob, Michael Overesch, Kerstin Schneider, François Vaillancourt, and three anonymous referees for helpful comments and support. In addition, we are thankful to the participants of the VHB Annual Meeting in Kaiserslautern 2011. All remaining errors and deficiencies are our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.