Abstract

Corporate social responsibility (CSR) has become a popular, and even expected, strategy for promoting an organization’s public persona. CSR is particularly important in the casino industry since many customers associate the casino industry with negative images such as crime and drugs; therefore, casinos try to enhance their social image through CSR activities. This study investigated how casinos’ CSR activities (economic, legal, ethical, and philanthropic) influenced customer loyalty (CL). Partial Least Squares (PLS)-structural equation modeling analysis was used to examine the hypotheses on a sample of 251 casino’s customer in the United States. Results of this study showed that the dimensions of philanthropic and legal responsibilities had varying effects on CL. In contrast, economic and ethical responsibilities didn’t significantly affect CL.

Introduction

Corporate social responsibility (CSR) has become a popular, and even expected, strategy for promoting an organization’s public persona. A company’s CSR efforts “reflect the organization’s status and activities with respect to its perceived societal obligations” (Brown and Dacin, 1997: 68). In essence, CSR involves a company conducting its business while addressing social concerns. This is done through sound ethical principles and by encouraging positive impact through its activities, involving the environment, consumers, employees, communities, stakeholders, and all other members of the public sphere (Skarmeas and Leonidou, 2013; Zizka, 2017). Ultimately, organizations consider CSR activities essential to bringing various benefits to companies, including improved reputations, enhanced community relationships, increased profits, and augmented responsiveness to expectations of social groups (Bhattacharya and Sen, 2004; Henderson, 2007; Kim et al., 2017; Lee and Park, 2009; Park et al., 2017).

CSR is important in the casino industry. Expanded gaming in many jurisdictions has increased concerns about the negative social impacts perceived as the by-products of casino gaming such as, prostitution, criminal activity, drugs, and erosion of the local community work ethic (Hing, 2003). As indicated by Perez and del Bosque (2012), “CSR is one of the most effective tools a company can use to improve its public image” (p. 146). When customers perceive a company’s CSR initiatives positively, their evaluation of the products/services will be enhanced, their trust in the company will be reinforced, and their loyalty will be strengthened (Brown and Dacin, 1997; Kim et al., 2017; Park et al., 2017; Sen and Bhattacharya, 2001; Skarmeas and Leonidou, 2013). To ameliorate this associated bad image, casinos can enhance their image through CSR activities. For instance, Caesars Entertainment has an employee-based volunteer program that supports communities through charitable donations, partnerships, sponsorships, and especially The Caesars Foundation. As of 2015, The Caesars Foundation has gifted US$72 million since its inception, and Caesars Entertainments’ total community giving is 67.2 million, along with 260,000 reported employee volunteer hours (Caesars Entertainment, 2016). Additionally, since 2006, casinos in Pennsylvania have contributed more than US$106 million toward philanthropic initiatives (Pennsylvania Gaming Control Board, 2017d).

Casinos have been increasingly engaged and invested in CSR activities. Nevertheless, the evaluation of the impacts of various CSR efforts is not straightforward and it is difficult to “quantify real profits which derive uniquely from CSR actions” (Zizka, 2017: 74). Particularly, it is imperative for local casinos in high tax rate areas to evaluate how various CSR efforts impact customer loyalty (CL). According to two American casino experts (a casino service manager with 18 years of casino work experience and a casino shift manager with 15 years of casino work experience) who work in both low tax rate casinos in New Jersey (8% for slot and table game revenues) and high tax rate casinos in Pennsylvania (55% for slot revenues and 16% for table game revenues), the jurisdiction’s tax structure cannot be ignored. The effectiveness of casinos’ CSR efforts needs to be closely monitored in locations where the total effective tax rate is high, such as 55% in the Greater Philadelphia area (UNLV Center for Gaming Research, 2018). Because discretionary expenses, such as philanthropic responsibilities, do not pertain to daily operations, high tax rate casinos also need to be cautious of their operational expenditures. Furthermore, unique feature of the local market in which casinos compete for the same customers’ repeat business needs to be taken into consideration. When the core products (slot machines, table games, loyalty programs) are similar among different casinos, each casino needs to differentiate itself from its competitors to retain its customers. A company’s CSR initiatives are expected to boost CL (Kim et al., 2017; Liu et al., 2014; Park et al., 2017). Loyal customers’ repeat purchases directly influence a casino’s revenue and their referrals decrease a casino’s marketing costs, leading to favorable financial performance.

As revealed by Reichheld and Schefter (2000), a 5% increase in retaining loyal customers results in a 25–95% increase in company’s profits. According to the Gartner Group, 80% of a company’s future revenue will come from 20% of the existing customers (Lawrence, 2012). As verified by a local casino shift manager and a casino service manager, retaining loyal customers is especially important in local casinos where on average more than 80% of their customers are repeat customers and 80% of their casinos’ revenue comes from the 20% of those repeat customers. Hence, it is critical for local casinos in high tax rate areas to evaluate how various CSR efforts impact their loyal customers.

To the best of authors’ knowledge, only two previous studies have investigated the relationship between casinos’ CSR efforts and CL. Liu et al. (2014) conducted a study in Macau to examine whether casinos’ stakeholders and society CSR initiatives enhance premium customers’ preferences and loyalty in casinos. The results of their study supported the notion that casinos’ stakeholders and society CSR initiatives positively influence premium customers’ loyalty. Furthermore, Kim et al. (2017) assessed whether a casino’s economic, legal, ethical, and philanthropic CSR activities enhance the casino’s image, thus leading to increased customer revisit intentions in South Korea. The results of their study revealed that a casino’s philanthropic CSR has a direct impact on customer revisit intentions. Additionally, a casino’s economic, ethical, and philanthropic CSR indirectly impact customers’ revisit intention via the casino’s image.

Nevertheless, results from the previous two studies cannot be directly applied to the local casinos in high tax rate markets in America because the economic expectations of casinos, as well gaming laws and regulations, are different in each state and country. Additionally, customers in different countries might react differently to the various casinos’ CSR efforts. Most importantly, although the Kim et al.’s (2017) study evaluated the impacts of the four dimensions of CSR on customers, the survey questions in their study could not reflect the current U.S. casino CSR practices. Based on the two American casino experts’ suggestions, the survey questions should be specifically tailored to portrait daily operations and thus, the results can prioritize various CSR initiatives. For instance, in terms of casinos’ legal and ethical responsibilities, in addition to asking generic questions on whether the casino respects norms defined in the regulations, the casino experts would like to see the practice of preventing underage gambling and promoting responsible gaming to be integrated in the questions. In terms of casinos’ philanthropic responsibility, the casino experts would like to see employee volunteerism at special organizations, such as Big Brothers and Big Sisters, to be evaluated.

Moreover, identifying factors influencing CL is not only imperative to the casino industry but critical to the local government and community. Casino loyal customers have great economic impacts on the local community. In fact, during fiscal year ending June 30, 2017, the 12 operating Pennsylvania casinos generated US$3,202,670,548 in gross gaming revenue (GGR) and employed 17,736 individuals. Total tax revenue from slots machines and table games paid to the state of Pennsylvania for this same period was $1,425,022,487 (Pennsylvania Gaming Control Board, 2017b and c). The gaming industry in Pennsylvania plays an increasingly important role in the fiscal health of the community. The 55% tax rate paid by casinos benefits many constituencies such as the State and Local Government, Tourism Development, and the Race Horse Industry (UNLV Center for Gaming Research, 2018).

Furthermore, the share of gaming revenues generated from the 12 gaming properties within the state allows local governments to make improvements to healthcare, infrastructure, and public safety. For example, in fiscal year 2014–2015, over US$1.58 million was distributed to communities throughout the state. Improvements were made to county hospitals and police departments from funds generated by gaming tax revenue (American Gaming Association, 2018). Northumberland County, Pennsylvania, which does not host a casino, benefited from gaming by receiving over US$500,000 in state funds to improve its volunteer fire department (American Gaming Association, 2018).

Gaming revenues also aid in citizen tax reductions. For instance, homeowners statewide have seen a school property tax reduction of approximately US$200 annually. Additionally, gaming revenues contribute to reducing the Philadelphia city wage tax, as well as property taxes. Finally, gaming tax revenues provide rent rebates for senior citizens, widows/widowers 50 and over, and individuals with disabilities (American Gaming Association, 2018).

Additionally, there is also an indirect economic impact to the State as a result of the commercial casino industry. According to Oxford Economics (2014), Pennsylvania casinos generated a total output impact of 6.18 billion. The total employment impact was 33,000 jobs which included approximately 16,000 indirect jobs from supporting industries. The total labor impact was 1.7 billion and total tax impact was 2.4 billion (as cited in Hillario, 2014).

It is also important to note that according to Oxford Economics (2014), the state’s economy would be significantly affected without the casino industry. The unemployment rate in Pennsylvania would have increased from 5.7% to 6.6% and homeowners would have had to pay an additional US$488 dollars in their annual property taxes without the support of casinos. Finally, casinos help in covering the salary of more than 58,000 public school teachers in the state of Pennsylvania (as cited in Hillario, 2014).

The proposed Live! Casino to be built in Philadelphia, Pennsylvania, is bringing other local economic benefits for the City directly. The Live! Casino is committing that 60% of the construction and permanent workforce will be local residents and 85% Pennsylvania residents. They also are committed to a living wage for the projected new 5000 employees. There will be 3000 local construction jobs created which is projected to generate approximately 145 million in direct and indirect salaries and wages during the construction period. Furthermore, there is community support for this casino from all five of the surrounding neighborhoods. Stadium Casino has committed to a Community Charitable Fund of a minimum of 15 million in grants to local communities during construction through the first 20 years of operation (Stadium Casino, 2015).

Thus, the purpose of this study is to examine whether the casinos’ CRS initiatives indeed lead to CL in a high tax rate and local market in America. Building on previous casinos related to CSR studies, this study evaluated the relationship between customers’ perceptions toward casinos’ economic, legal, ethical, and philanthropic CSR activities and their loyalty.

Literature review

Corporate social responsibility

It is difficult to give an exact definition of CSR since activities are based on relevant issues of the day as well as managers’ perceptions of what a socially responsible company should be (Snider et al., 2003; Swaen and Chumpitaz, 2008). CSR is aimed at strengthening the fairness and honesty of business practices, promoting product safety, protecting employees’ welfare, and increasing a company’s environmental performance (Swaen and Chumpitaz, 2008). Generally, the essential component of CSR is promotion of activities that portray companies as good citizens who contribute to society’s welfare in addition to maximizing their own profits (Carroll, 1999; McWilliams and Siegel, 2001).

Two motivational forces, stakeholders and society, can put pressure on companies to be more socially responsible (Kok et al., 2001). Stakeholder theory sustains the idea that, even though companies do not have responsibilities toward society in general, they should be concerned about individuals or groups who may be directly or indirectly influenced by their actions (Salmones et al., 2005). Employees, customers, and the government are common stakeholders for a company (Liu et al., 2014). “Different stakeholders have different expectations, needs, and motivations” (Zizka, 2017: 74). Companies’ CSR efforts need to benefit multiple stakeholder groups appropriately; thus, companies should ask stakeholders to be involved in sharing their expectations of social responsibility (Kok et al., 2001; Zizka, 2017).

In terms of society motivation, Carroll’s (1979) four-dimensional conceptual model is applied in this study. Carroll (1979) declared that companies that practice social responsibility address “economic, legal, ethical, and philanthropic expectations that society has of organizations at a given point in time” (p. 499). Economic responsibilities are obligations for businesses to be productive and profitable by satisfying investors’ and customers’ needs. Legal responsibilities require businesses to meet their economic duties within the framework of legal requirements. Ethical responsibilities are defined as businesses abiding by established norms that define appropriate behavior, such as adopting morally justifiable codes of conduct. Philanthropic responsibilities of businesses involve active contributions to community welfare by investing in education and charity (Swaen and Chumpitaz, 2008). Carroll’s (1979) framework has been used by several researchers (Crane and Matten, 2004; Maignan, 2001; Pinkston and Carroll, 1994; Ramasamy and Yeung, 2009).

Economic responsibility

To elaborate on economic responsibility, Carroll (1979) asserted that “before anything else, the business institution is the basic economic unit in our society. All other business roles are predicated on this fundamental assumption” (p. 500). Economic responsibility means that managers should take control of the economic aspects of a business system according to expectations of the public. Society expects businesses to produce goods and services and sell them at a reasonable profit (Carroll, 1999). For economic responsibility, both Carroll (1999) and Yeoh (2007) state that, from different stakeholders’ viewpoints, there are different expectations for the company. For example, shareholders want financial return, employees want good pay, customers want good service, and the community wants businesses that respect environmental conservation and add to community development (Carroll, 1999; Yeoh, 2007). In 1996, former U.S. President Bill Clinton called a group of businesspersons to Washington to discuss the notion of corporate citizenship and social responsibility; he stated that “the most fundamental responsibility of any business in a free-enterprise system is to make a profit” (Clinton has challenge for CEO, 1996, G3). In essence, companies can earn money for personal profit and for their shareholders to receive a profit on their investments, while other stakeholders are assured the flow of products, services, jobs, and other profit offered by the company (Carroll, 1999).

Different from other industries, casino operations are expected to provide high tax revenue to the government and many states legalize casinos because of the tax revenue and job opportunities provided by casino operations (Bybee and Aguero, 1998). For instance, the tax rate for the slot machine revenue is 55% for Pennsylvania’s 12 casinos. The government uses that money for economic development and the tourism fund, property tax relief, and wage tax reduction (Pennsylvania Gaming Control Board, 2017a). Casinos create employment opportunities and generate tax revenue for state and local governments, while also serving as an economic stimulus for local communities (American Gaming Association, 2010).

According to the American Gaming Association (2010), the casino industry supported approximately US$125 billion in spending and provided more than 350,000 jobs in the United States, with wages and benefits totaling US$15 billion. The industry directly paid nearly US$16 billion in taxes in 2010. In 2016, U.S. state and local governments received US$8.85 billion in gaming taxes from commercial casinos. At a state level, Nevada’s 273 casinos in 2016 earned US$11.257 billion in GGR. They provided 166,631 jobs in Nevada and also contributed US$900.57 million to Nevada and local governments in terms of tax revenue. Another example of casinos contributing economic benefits is Pennsylvania. Its 12 casinos in 2016 generated revenue exceeding US$3 billion. These same casinos offered more than 16,260 jobs and contributed US$1.388 billion in gaming tax (American Gaming Association, 2018).

Legal responsibility

Carroll (1979) argues that “society expects business to fulfill its economic mission within the framework of legal requirements” (p. 500). Society expects businesses to follow the social rules that come from federal, state, and local governmental laws and regulations (Carroll, 1979, 1999; Maignan, 2001; McDonald and Thiele, 2008).

As indicated by American Gaming Association (2015b), the casino industry is one of the most highly regulated industries in the United States. There is stringent regulation in the United States of the casino industry. Each state gives casinos strict standards to follow, for example, in taxes, licenses, financial reports, chips and tokens, and gaming rules. In order to make sure the casino completely follows the rules, the government sends staff to supervise casinos. In Pennsylvania, the Bureau of Casino Compliance’s mission is to secure the integrity of gaming. Thus, casino compliance representatives are assigned to each casino to observe day-to-day gaming operations (Pennsylvania Gaming Control Board, 2017a). If the government staff finds any violations, they can report it to the bureau; hence, casinos should be especially strict with legal responsibility. If a casino breaks the rules, it could receive fines and lose its gaming license. For instance, in Atlantic city, some casinos were fined for a series of regulatory violations, including Tropicana Casino and Resort which was found guilty of a blackjack cheating scam in 2011. In 2009, Caesars Atlantic City was fined US$10,000 because its alarm system did not work when a robber stole money from the cashier’s cage (Wittkowski, 2011)

In terms of dealing with customers, a casino’s legal responsibility is to prevent underage gambling and to promote responsible gaming. As examples to the contrary, Trump Plaza Hotel and Casino, Trump Taj Mahal Casino Resort, and the Atlantic City Hilton Casino Resort all were fined for allowing underage patrons to gamble (New Jersey Real Time News, 2011). In most states, the law requires players to be 21; hence, state law would require casinos to check their customers’ ID before entering the gaming floor.

Moreover, responsible gaming is critical and thus, each state has procedures regarding this, such as self-exclusion and signage stating how to seek help for gambling addictions, and so on. For example, Pennsylvania requires each casino to post signs that include a statement similar to the following: “If you or someone you know has a gambling problem, help is available. Call 1-800-gambler.” Furthermore, these signs must be posted within 50 ft of each entrance and exit of the facility and within 50 ft of each ATM, cash dispensing, or change machine in each facility. New Jersey also has similar requirements: casinos must put the sign “gambling problem” and “call 1-800 GAMBLER” on all print, billboard, and sign advertising at their operation (American Gaming Association, 2016). Most states also maintain a self-exclusion list of names of persons who agree to be excluded and be prohibited from all gaming activities. Casinos must prevent a person on the self-exclusion list from entering the casino. They must also refuse wagers and deny any gaming privileges and casino credit, club membership, and any casino benefits to any self-excluded person. They also must ensure that the casino will not send any promotions to self-excluded persons (American Gaming Association, 2016; Caesars Entertainment, 2018).

Ethical responsibility

Raiborn and Payne (1990) defined ethics as “a system of value principles or practices and a definition of right and wrong” (p. 879). Ethics is concerned with moral decision-making regarding the rightness or wrongness of a behavior and whether it is good or bad to engage in certain behaviors. Businesses wishing to build and promote good relationships with the community should not only be economically successful and function within the boundaries of the law, but they also need to be cognizant of ethical issues regarding all aspects of the business. On the other hand, Carroll (1979) argued that “ethical responsibilities are ill defined and consequently are among the most difficult for business to deal with” (p. 500). Often, ethical decision-making is a vague and poorly defined process (Carroll, 1979).

Stodder (1998) argued that responsible businesses should function within the parameters of good ethical practices. Because a business has an obligation to its customers, a company should be honest about its products and operations, even if only to make customers feel that the business cares about them more than selling their products. Iwanow et al. (2005) indicated that businesses wishing to build and promote good relationships with the community should not only be economically successful and function within the boundaries of the law, but they also need to be cognizant of ethical issues regarding all aspects of its business. The negative results of unethical behavior on the part of firms and their agents are numerous. Moreover, some unethical behavior by employees of a firm can cause severe damage to the reputation of the company and, in some cases, can cause the company to fail.

For casinos, one of the most important ethical responsibilities is responsible gaming. Although the concept of responsible gaming has been discussed in casinos’ legal responsibilities, regulations mandated by the state should be the minimal standard for responsible gaming. The extra efforts of casinos to promote responsible gaming beyond the minimum regulations could be considered ethical behavior for the casino. According to the American Gaming Association’s code of conduct for responsible gaming (2015a), casinos must train employees who directly interact with gaming patrons in the gaming area. As indicated by American Gaming Association’s Responsible Gaming Regulations and Status (2016), the training should include the nature and symptoms of problem gaming behavior and information about problem gaming programs. Additionally, each casino should have someone responsible for training and maintaining these programs. The casino should also make responsible gaming information available to all employees and post that information at various convenient locations. Responsible gaming information should be placed on the casino’s website to give information on where to find assistance. Casinos can make appropriate signage or brochures to communicate the legal age to gamble to prevent underage gambling. Finally, casinos should not serve alcoholic beverages to an intoxicated customer and should also attempt to stop an intoxicated customer from gambling.

Caesars Entertainment Corporation, for example, has been a leader in this area since the early 1980s. Its “Operation Bet Smart” and “Project 21” programs for employees, guests, and the public emphasize the importance of responsible gaming and the prevention of underage gambling. “Operation Bet Smart” is a program to educate employees on the importance of promoting responsible gaming and to train employees about the policies and procedures of the responsible gaming program. “Project 21” raises awareness of the negative consequences of underage gambling. It provides training to casino employees on cues to identify underage gamblers (Caesars Entertainment, 2018).

Philanthropic responsibility

Philanthropy has its roots in the Latin word philanthropic, which means “love of man” (Chesters and Lawrence, 2008). Carroll (1979) indicated that philanthropic responsibilities make a company a good corporate citizen, which can only be reached after economic, legal, and ethical responsibilities have been achieved. Carroll (1998) stated that “philanthropy is essentially giving back” (p. 5). Carroll (1998) explained that communities support businesses; therefore, businesses should have an obligation to give something back to communities. Philanthropy is booming as corporations are realizing that good citizenship reaps a plethora of rewards (Porter and Kramer, 2002, 2006).

Contributions to a range of charities are also reported by a number of casinos. For example, Caesars Entertainment provides some type of sponsorship for certain diseases, such as AIDS and cancer, and supports The Red Cross. Moreover, Caesars Entertainment provides tuition reimbursement to help employees to obtain their degrees and works with local agencies to increase the supply of quality local workers (Caesars Entertainment, 2016).

Of special note, Caesars Entertainment assists those with disabilities through activities such as the Special Service School District and Disabilities Center. The casino employees also join with different organizations to directly help various groups of people throughout their communities, such as Big Brothers and Big Sisters of America. The Caesars Foundation, for example, gives about US$10 million a year nationally, with about 40% of that going to organizations in Las Vegas. The foundation supports such programs as Meals on Wheels for seniors and Opportunity Village, Three Square, the Public Education Foundation, and several other local organizations. In year 2013, Caesars Entertainment reported US$76 million in total community giving and 164,651 h volunteered in the community (Caesars Entertainment, 2014). However, due to strict governmental laws and regulations, there is no flexibility in casinos’ economic and legal responsibility practices. Nevertheless, each casino practices its ethical and philanthropic responsibilities differently.

Relationship between CSR and CL

Much research indicates that businesses have a responsibility to their stakeholders and that customers are important members of this group (Maignan, 2001; McDonald and Thiele, 2008; Ramasamy and Yeung, 2009; Swaen and Chumpitaz, 2008). Customers have an important role in encouraging businesses to adopt and advance CSR (Lou and Bhattacharya, 2006; Swaen and Chumpitaz, 2008). When customers express concern about CSR issues, companies respond by offering products or services that coincide with customer concerns (Swaen and Chumpitaz, 2008). Customers sometimes want to know about how the products they purchase are made, where they are produced, and who benefits from their purchases. Consequently, customers have advocated boycotts to dispute what they perceive to be unethical or irresponsible behavior (Perera, 2007; Wazir, 2001). In 2001, the Washington Post documented that, once customers discovered irresponsible behavior, they actively campaigned against Nike products in an effort to force them to manufacture their products in a more socially responsible manner (How to Battle Sweatshops, 2001). A similar situation involved Walmart, who was found to be paying less than acceptable and legal wages, as well as providing minimal or inadequate benefits to many of their employees. In 2005, labor advocacy groups asked Walmart to change the way it paid wages and managed employees (Vaishnav, 2005). As a result, more and more companies have joined social responsibility programs and use marketing strategies to convey that ethical image to the public (Snider et al., 2003).

Organizations’ CSR efforts have positive effects on customers, including favorable production/service evaluations, higher purchase intention, stronger confidence, and enhanced customer satisfaction loyalty (Kim et al., 2017; Maignan and Ferrell, 2001; Oberseder et al., 2013; Park et al., 2017; Skarmeas and Leonidou, 2013). When customers perceive positive CSR by the company, their evaluations of the company and attitude toward the company will be positive, which lead to higher loyalty (Brown and Dacin, 1997; Marin et al., 2009).

CL should be measured by two dimensions combining behavioral measurements and attitudinal measurements (Arikan et al., 2016; Baloglu, 2002; Mandhachitara and Poolthong, 2011; Salmones et al., 2005). Considering relative attitudinal and behavioral relationship, Dick and Basu (1994) cross-classified CL into four dimensions: (1) true loyalty, (2) latent loyalty, (3) spurious loyalty, and (4) low loyalty. True loyal customers are customers who provide repeat business and also hold a positive attitude toward the brand. Applying the composite measurement among the casino players, Baloglu (2002) indicated that true casino customers display stronger emotional commitment and trust toward the casinos than spurious and low-loyalty customers. In addition, the proportion of visits among true casino loyal customers is significantly higher than other types of loyalty customers.

Specially, in the casino industry, there are positive relationships between customers’ perceptions on casinos’ CSR initiatives and their loyalty intention (Kim and Kim, 2016; Kim et al., 2017; Liu et al., 2014). When customers perceive casino stakeholders and society CSR initiatives positively, their preferences to the brand and loyalty are strengthened (Liu et al., 2014). Additionally, a casino’s image is advanced when customers perceive its economic, ethical, and philanthropic activities positively which can lead to higher revisit intentions (Kim et al., 2017).

Accordingly, the following four hypotheses are proposed:

Hypotheses

Methodology

Survey instrument and data collection

A survey questionnaire was derived from the instrument applied by Salmones et al. (2005) and with input from two consulting casino industry experts. A screening question at the beginning of the survey was used to filter out participants who were not eligible for the study (i.e. no experience with gaming in a casino in the past 12 months). The survey instrument used a seven-point Likert-type scale for measuring the casino’s CSR performance and customer purchase intention, with 1 = Strongly disagree to 7 = Strongly agree. The participants were asked to list the name of the casino they gambled in most often and refer to that specific casino as the selected casino to answer the questions. This study collected data at a restaurant located in a metropolitan city on the East Coast in the United States that has four local casinos within a half-hour driving distance. Of 585 surveys distributed, 251 valid responses were generated, with a response rate of 43%.

Demographic profile of the participants

Most of participants were male (59%). Moreover, 29.5% of the participants were in the age group of 41–50, followed by 27.1% in age group of 21–30; 22.3% of the participants were in age group of 31–40; and 21.1% were older than 51. Most participants (37.5%) visited casinos one to three times per year, followed by 33.1% of participants who visited casinos more than seven times per year and 29.5% who visited four to six times per year. Most participants (38.2%) earned an annual income of US$60,001 to US$100,000, followed by 36.7% who earned less than US$60,000 and 25.1% who earned more than US$100,001. For a gambling budget, the majority of the participants (41.4%) spent US$201 to US$600 in the casino, followed by 31.9% who spent less than US$200 and 26.7% who spent more than US$601when they gambled. The majority of the participants had college degrees (56.6%), followed by 29.1% who had high school degrees. Only 14.3% of respondents had a master’s degree or higher.

Analysis and results

Data were analyzed using structural equations modeling in SmartPLS (Hair et al., 2017). Standardized variables were analyzed in a bootstrapping procedure using 5000 samples of 251 cases. SmartPLS was employed to assess the measurement and structural models following a two-step approach: (1) validation of the outer (measurement) models and (2) examination of the inner model (structural relations among the latent factors) (Chin, 2010). PLS-structural equation modeling (SEM) enables the simultaneous modeling of relationships among multiple independent and dependent constructs (Haenlein and Kaplan, 2004). It differs from co-variance-based SEM as it functions to “maximize the variance of the dependent variables explained by the independent ones instead of reproducing the empirical covariance matrix” (Haenlein and Kaplan, 2004: 290). PLS-SEM is advantageous when examining complex models with relatively small sample sizes (Bagozzi and Yi, 2012; Haenlein and Kaplan, 2004), as was the case for this study. It is also more powerful in calculating models with formative and reflective constructs (Haenlein and Kaplan, 2004).

Evaluation of the measurement model

To assess reliability and validity using PLS, researchers typically calculate a block of indicators’ composite reliabilities and average variance extracted (AVE) (Chin, 2010). Construct reliability of the reflective measurement model was tested by calculating composite reliability and Cronbach’s α. Interpreted like a Cronbach’s α internal consistency reliability estimate, a composite reliability of 0.70 or greater is considered acceptable for research (Fornell and Larcker, 1981). Content validity was established by visual inspection of all items and by the application of established and tested scales. Indicator reliability of the reflective measurement model also held because the item loadings were greater than the threshold of 0.7 for all items. The AVE measures the variance captured by the indictors relative to measurement error (Fornell and Larcker, 1981), and it should be greater than 0.50 to justify using a construct (Barclay et al., 1995) (see Table 1).

Outer model loadings and cross loadings.

Note: PRA: philanthropic responsibility activity; LRA: legal responsibility activity; CL: customer loyalty; ERA: economic responsibility activity; ETRA: ethical responsibility activity. t-Values are based on 5000 bootstrap runs with 251 cases.

** Level of significance is p < 0.05.

*** Level of significance is p < 0.01.

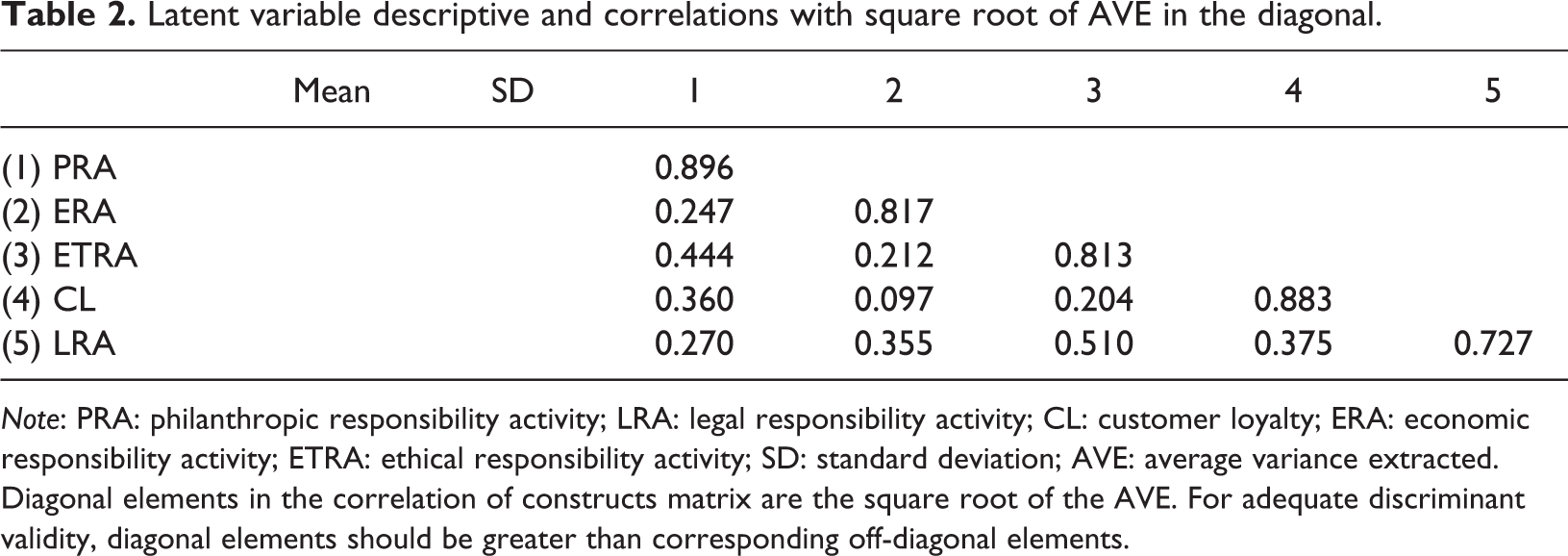

To evaluate discriminant and convergent validity, we examined the correlation of constructs and factor loadings. When the square root of each construct’s AVE is greater than the correlation of the construct to other latent variables, the correlation of constructs demonstrates discriminant validity. A second way to evaluate discriminant validity is to examine each indicator’s factor loadings (Chin, 2010). Indicators should load higher on the construct of interest than on any other variable. The model’s correlations of constructs (see Table 2) and factor loadings (see Table 3) demonstrate adequate discriminant and convergent validity. All five local quality criteria were fulfilled above the appropriate thresholds; thus, validity and reliability of the measurement models could be confirmed.

Latent variable descriptive and correlations with square root of AVE in the diagonal.

Note: PRA: philanthropic responsibility activity; LRA: legal responsibility activity; CL: customer loyalty; ERA: economic responsibility activity; ETRA: ethical responsibility activity; SD: standard deviation; AVE: average variance extracted. Diagonal elements in the correlation of constructs matrix are the square root of the AVE. For adequate discriminant validity, diagonal elements should be greater than corresponding off-diagonal elements.

Factor loadings and cross loadings for the measurement model.

Note: PRA: philanthropic responsibility activity; LRA: legal responsibility activity; CL: customer loyalty; ERA: economic responsibility activity; ETRA: ethical responsibility activity. Negative affectivity was included to demonstrate discriminate validity for the items. Because it is an additive scale, it was collapsed into a single indicator in the final mode.

Evaluation of the structural model

The hypothesized inner-model relationships among latent variables were examined through PLS-SEM to determine (1) the estimates of the path coefficients and effect sizes (f 2) and (2) the coefficient of determination (R 2) of the endogenous latent variables (Henseler et al., 2009). The R 2 values of four endogenous latent variables were 0.232 for customer purchase intention. Effect sizes above 0.35, 0.15, and 0.02 indicate substantial, moderate, and weak effects, respectively (Cohen, 1992). The effect sizes of the endogenous variables in this model range from 0.010 to 0.127. Cohen’s f 2 values for the significant paths in the inner model were all above 0.02, suggesting satisfactory effects for the endogenous latent constructs (Henseler et al., 2009) (see Table 4). Finally, the Stone-Geisser Q 2 values obtained through the blindfolding procedures for customer purchase intention (Q 2 = 0.178), ethical responsibility activities (ETRAs; Q 2 = 0.662), philanthropic responsibility activities (PRAs; Q 2 = 0.802), economic responsibility activities (ERAs; Q 2 = 0.673), and legal responsibility activities (LRAs; Q 2 = 0.526) were larger than zero, supporting the predictive relevance of the model (Hair et al., 2017).

Path estimates of the structure model.

Note: PRA: philanthropic responsibility activity; ERA: economic responsibility activity; ETRA: ethical responsibility activity; CL: customer loyalty; LRA: legal responsibility activity. t-Values are based on 5000 bootstrap runs with 251 cases.

**Level of significance is p < 0.05.

Evaluation of the overall model

The validity of the overall PLS model was established by examining the quality measures of the outer measurement models and the inner structural model (Götz et al., 2010). The results illustrate that PRAs and LRAs were positively and significantly related to CL, supporting hypotheses 2 and 4. However, ERAs and ETRAs were not significantly related to CL, rejecting hypotheses 1 and 3 (see Table 4 and Figure 1).

PLS model with significant effects.

Discussion

Theoretical implications

The results of this study confirmed that a casino’s legal responsibilities and philanthropic responsibilities positively influence its customers’ level of loyalty. Legal responsibility refers to carrying out the companies’ activities within the limitations of legal requirements. The laws address social issues, such as positive action, product safety toward legalistic documents focused on harmful actions, suitable process procedures for violations, and sanctions (Knouse et al., 2007). Moreover, those laws are viewed as the baseline that society expects the business to follow. Multiple negative consequences come along when companies fail to practice their legal responsibilities, including unfavorable customer attitudes toward the companies, tarnished reputations, and decreased revenues (Stanisavljevic, 2017). The results of this study show that when customers perceive a casino’s legal responsibilities positively, they will demonstrate loyal behavior. The participants in this study indicated that they trust casinos are operating honestly when they witness the casinos following governmental laws and regulations, such as checking identification to prevent underage gambling; thus, these actions result in their loyalty behaviors.

However, a casino’s legal responsibility does not contribute to CL in South Korea (Kim et al., 2017). As indicated by the panel of six casino industry experts, the possible explanation might be that the survey questions in Kim et al. (2017)’s study are relatively general, such as “the casino resort properly implements casino game rules and regulations” (p. 77). On the other hand, the survey questions in this study described that the exact legal responsibility casinos are practicing, such as “the selected casino employees always check IDs to make sure customers on the gaming floor are 21 and older.” The specific questions presented concrete concept to customers what legal responsibilities casinos have.

Philanthropic responsibility refers to voluntary or philanthropic activities aiming to raise well-being (Carroll, 1998). According to Chesters and Lawrence (2008), corporate philanthropy is a part of CSR, and it serves as a link between the corporation and the communities; it serves through cash gifts, product donations, and employee volunteerism. Therefore, philanthropy has become a tool to develop a relationship with the community, build CL, and improve staff morale. The result of this study is consistent with Kim et al. (2017)’s study, where a casino’s philanthropic efforts indeed positively impact its customers’ level of loyalty in both South Korea and the United States. Generally speaking, after a company fulfills its economic, legal, and ethical responsibilities, it can proactively give back to the community and society because “the economic and legal responsibilities are ‘required’, the ethical responsibilities are ‘expected’, and the discretionary/philanthropic responsibilities are ‘desired” (Carroll and Shabana, 2010: 90). Hence, those discretionary philanthropic efforts are particularly effective in creating positive brand image and thus lead to CL (Huang et al., 2014; Kim et al., 2017; Liu et al., 2014; Marin et al., 2009).

In contrast, the results of this study indicate that a casino’s economic responsibilities did not influence CL. Mittal et al. (2008) indicated that a firm’s strong financial performance can enhance brand image and reputation, increase sales and CL, increase productivity and quality, as well as other benefits. Nevertheless, the result of this study is consistent with Kim et al. (2017)’s study, where a casino’s economic responsibility did not impact its customers’ loyalty in both South Korea and the United States. The fundamental issue might be that “the economic behavior of firms is not perceived to be a component of corporate social responsibility by consumers” (Salmones et al., 2005: 376). As suggested by Aupperle et al. (1985), Maignan and Ferrell (2001), Salmones et al. (2005), and Perez and del Bosque (2015), it is logical to measure the three non-economic components (legal, ethical, and philanthropic) separately from the economic component since the results will be much clearer and “social responsibility has generally been associated more with ethical, legal and philanthropic actions” (Salmones et al., 2005: 376).

Additionally, the participants in this study were all local residents who should be very familiar with the expected economic benefits casinos brought to the community. For instance, Harrah’s Philadelphia had multiple public hearings to explain the increased tax revenues and job opportunities the casino would bring to the local community before its opening. As reported by Milford (2006: para. 13) Harrah’s plans to create 800 to 900 new jobs, a big boost for a city with just 6,000 private-sector jobs. What’s more, the gambling legislation guarantees Chester a minimum $10 million in revenues, which represents almost 29% of the city’s current budget.

Furthermore, it seems there was no consensus in the relationship between a company’s ethical responsibilities and CL. Solaiman et al. (2007) stated that ethical practices can help companies develop a market reputation and create customer sympathy. When competitive offerings are similar in technical, economic, or service facets, customers start to look for points of difference, such as a firm’s ethical reputation which can give the firm an edge by providing a “point of difference” (Anderson et al., 2006). However, the results of this study indicate that a casino’s ethical responsibilities did not influence CL. Additionally, the Stanisavljevic’s (2017) and Kim et al.’s (2017) studies in which a mobile company’s ethical responsibilities did not influence its users’ loyalty in Kragujevac and a casino’s ethical responsibility did not impact its customers’ level of loyalty presented the same results as this study. The cause might be that although Carroll (1998) classified four facets of corporate citizenship: economic, legal, ethical, and philanthropic, it is not easy to clearly distinguish the differences between legal responsibilities and ethical responsibilities. Carroll (1979) considered a company’s ethical responsibilities to be the responsibilities that go above and beyond the legal framework; thus, legal responsibilities are the benchmarks for ethical responsibilities. Hence, several studies evaluated ethical and legal responsibilities under the same construct (Choi and La, 2013; Salmones et al., 2005). Additionally, the distinction between legal and ethical responsibilities is particularly difficult to define in the casino industry since each state has its own laws and regulations. Finally, as verified by the panel of six casino industry experts, in this study, a casino’s ethical responsibilities were measured by what degree a casino promotes responsible gaming beyond the government standards and it is possible that the customers might not have this kind of information.

In conclusion, the results revealed that a casino’s economic responsibility practices might not serve as a differentiator when most customers are local residents who take casinos’ economic contributions for granted. The results also demonstrated the importance of constantly and clearly communicating to customers about a casino’s legal responsibility practices to earn customer trust for retention. The results also discovered that customers might not be aware of the ethical efforts casinos put forth that are above and beyond governmental laws and regulations. Finally, the results asserted that a casino’s philanthropic responsibilities indeed had positive impact on CL.

This study contributes to the advancement of academic theories, thereby generating results that can be applied to business practices. The authors started with identifying the issues or difficulties that casino industry practitioners encounter in their implementation of CSR initiatives. Then, the appropriate academic theories were applied to evaluate those practical problems. Various models have been used to investigate a company’s CSR efforts; some researcher apply CSR to society and CSR to stakeholders’ concepts (Arikan et al., 2016; Liu et al., 2014; Perez and del Bosque, 2015), while other researchers apply Carroll’s (1979) four-dimensional CSR model (Kim et al., 2017; Stanisavljevic, 2017). In this study, the authors applied Carroll’s (1979) four-dimensional CSR model because two casino experts considered that the CSR to society and CSR to stakeholders’ models would not evaluate the exact CSR programs they are practicing daily. Furthermore, casinos are currently practicing the four types of CSR activities identified by Carroll’s (1979) four-dimensional conceptual model. Carroll’s model is “useful in identifying specific kinds of benefits that flow back to companies” (Carroll and Shabana, 2010: 90).

Additionally, although Carroll’s (1979) four dimensions of CSR concept have been widely accepted, the empirical application of this concept was inconsistent. For instance, recognizing the four dimensions of CSR, Salmones et al. (2005) evaluated a company’s CSR with only three dimensions: economic, ethical-legal, and philanthropic responsibilities. Choi and La (2013) assessed CSR focused only on ethical and legal categories. Huang et al. (2014) measured CSR with only three dimensions: economic-legal, philanthropic, and ethical responsibilities. Stanisavljevic (2017) and Kim et al. (2017) measured CSR with the complete four dimensions: economic, legal, ethical, and philanthropic responsibilities. The results of this study confirm the appropriateness of applying Carroll’s (1979) four-dimensional CSR concepts to evaluate how casinos’ various CSR efforts impact CL in a high tax rate local market in the United States.

Managerial implications

First, the panel of six casino industry experts whose casino work experience ranges from 5 to 25 years and whose positions of casino operation shift managers, casino service manager, table games supervisors, slot supervisor, and to beverage supervisor were not surprised by the results that casinos’ economic responsibility practices do not lead to CL. Granted, the ultimate goal of legalizing casinos was to benefit the community economically. For instance, in Pennsylvania, the state government and local government received tax revenues from casinos, and numerous jobs were generated from the casino industry. Thus, a casino’s economic performance contribution to the community has been evident. Particularly, the participants in this study were local customers instead of tourists; therefore, the casino’s economic performance facilitates local development which has been witnessed by the residents. Nevertheless, it is possible that local customers have expected casinos to be economic energizers to the local economy; thus, casino economic responsibilities did not significantly contribute to CL. Additionally, as a casino shift manager stated, casinos pay a high tax rate to the governments. However, the state or local governments never indicate how the casino tax revenue is used. Thus, the general public is simply not aware of how the tax money is used. Casino operators should let the local customers know how the local community benefits from the casinos’ economic contributions.

For example, in Pennsylvania, the gaming industry plays an increasingly important role in the fiscal health of the community. The 55% tax rate paid by casinos benefits many constituencies such as the State and Local Government, Tourism Development, and the Race Horse Industry (UNLV Center for Gaming Research, 2018). Furthermore, the share of gaming revenues generated from the 12 Pennsylvania gaming properties allowed local governments to make improvements to healthcare, infrastructure, and public safety. Improvements were made to county hospitals and police and fire departments from funds generated by gaming tax revenue, even in those counties that do not host a casino (American Gaming Association, 2018). In Pennsylvania, gaming revenues also assisted in reducing property and school taxes of approximately US$200 annually. Finally, gaming revenues contributed to reducing the Philadelphia city wage tax, as well as provided rent rebates for senior citizens, widows/widowers fifty and over, and individuals with disabilities (American Gaming Association, 2018).

This study also showed that there is a relationship between legal responsibility and CL. Because there are so many negative stereotypes of the casino industry, such as its connection with crime and violence, casinos must show that they indeed operate in an obedient fashion under strict laws and regulations. As validated by a panel of six casino industry experts, a casino needs to be able to earn customers’ trust that they are operating honestly. Trust is a prominent antecedent for CL. A company needs to effectively convey its commitment to CSR to its customers to build the trust that will result in their loyalty (Park et al., 2017). When customers put their trust in a casino, they expect the promises and statements made by the casinos to be reliable (Baloglu, 2002; Bowen and Shoemaker, 1998; Park et al., 2017). The current task for the casino industry is to effectively communicate with the public that casinos comply with the governmental laws and regulations. For instance, casinos could make an extra effort to practice responsible gaming, by educating their customers and employees about responsible gaming. This is especially important for repeat customers. Then, the most noticeable actions for casinos to demonstrate to their customers that they are following regulations in checking IDs to prevent underage gambling and clearly displaying problem gambling signage around the casino floor.

In terms of ethical issues in the casino industry, even the National Council on Problem Gambling indicates that the majority of customers in casinos gamble for entertainment purposes; however, a certain percentage of people are compulsive gamblers (National Council on Problem Gambling, 2012). Therefore, casinos recognize their responsibility in making customers aware of this issue. It is reasonable to conclude that the results of this study indicated that casinos’ ethical responsibilities do not influence CL because a casino’s ethical responsibilities were measured by the degree to which a casino promotes responsible gaming beyond the government standards, and it is not easy for customers to have this kind of information. Therefore, the task for the casino managers is to educate customers about all the ethical efforts they go to, above and beyond the laws required. Furthermore, casinos need to encourage their employees to share the information with customers about the Gaming Code of Conduct on its website and provide incentives to employees when they actively promote responsible gaming, such as providing customers information on where to locate confidential and professional counseling assistance for problem gambling or presenting the responsible gaming and toll-free help number to customers.

Finally, there is indeed a relationship between casinos’ philanthropic activities and CL. Usually, casino commercials or advertisements show customers that they can have fun and win money, but customers seldom made aware of any information about casinos donating money to charities or supporting any humanitarian organizations. It is critical for the casino industry to actively promote their philanthropic activities. In addition to broadcasting commercials or advertisements showing people having fun in a casino, they should also demonstrate to the customers that they donate money to charities and support humanitarian organizations. Moreover, casinos can focus on particular social events that relate to the casino industry with regard to donating money or giving humanitarian support. Casinos can also focus on non-profit organizations that help people deal with gambling problems or drug problems. If they focus on those kinds of philanthropic activities, they can help build a stronger image that casinos really care about society; in addition, they could also try to fix any bad effects gambling might bring to society. There are many successful promotions of PRAs in other industries, which casinos can learn from. For instance, corporate giving and employee volunteer programs have a direct effect on customer evaluations of companies (Sen and Bhattacharya, 2001). Hess et al. (2002) argued that long-term community involvement in corporate giving produces a positive business image. As verified by the same panel of casino experts, customers will not visit a casino merely because of a casino’s charity work; however, many casinos are involved in local communities’ volunteer and charity work and should constantly remind customers of their presence. For instance, when Harrah’s Philadelphia employees volunteer to clean the local streets and paint the local church, all the employees wear a T-shirt with Harrah’s logos to remind customers of their contribution to the community.

Limitations and recommendations for future research

The major limitation of this study is that there are no existing reliable and valid measurement tools for the four dimensions in CSR tailored specially for casinos. In this study, the authors started with following the common questions used in Salmones et al.’s (2005) study. However, casino industry experts believe those questions used in previous instruments are too general. Furthermore, they suggested it would be beneficial to casino operators if questions were designed to be specific to address particular laws and regulations and different philanthropic activities posted on the four casinos’ websites. Thus, the questions in this study were tailored specifically to the casinos in the study and should not be generalized to other casino sites. Additionally, studies should work on reliable and valid measurements for the four dimensions in CSR for the casino industry.

The second limitation in this study is that the data were collected in a restaurant located in a metropolitan city on the East Coast of the United States with four local casinos within a half-hour driving distance. The authors started with asking permission from the casinos, but none of the casinos agreed to let the authors distribute surveys to their customers, and thus the casino managers recommended that the authors collect data in the participating restaurant. The casino manager told the authors that based on his observation, many of his players gather in the restaurant before or after they visit the casino. Thus, there was a screening question at the beginning of the survey to ensure that participants were casino players who gambled within the past 12 months.

Finally, future researchers are recommended to demonstrate the benefits that the results of such a study could yield to casino operators. It is with this in mind that casinos will be more open to working with researchers to collect data in a responsible manner from their players. In addition, further research is also needed to broaden the sample by including casinos from different areas of the country. This study has been restricted to the eastern region of the United States based on time and money constraints and is not generalizable in other areas.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.