Abstract

This article assesses the role of human asset quality in the internationalization of small and medium-sized family enterprises. Building on mainstream international business theory, we propose a model with three “states” of human asset quality (low, medium, and high) available to the firm that can be linked to particular levels of export intensity. Importantly, achieving higher export intensity is not always associated with higher human asset quality across the board: There is a key difference between generic (generally available) and specialized (highly firm-specific) human asset quality. We empirically test our model through Tobit panel data analyses with random effects, whereby we study a sample of 610 Spanish firms for the period 2006 to 2010. This research represents the first-ever work conceptualizing and empirically testing a nonlinear, cubic relationship between human asset quality and small and medium-sized family enterprises’ internationalization levels. We find an S-shaped relationship between both general and specialized human assets and the level of export intensity.

Keywords

Family business research has traditionally been dominated by themes such as governance, succession, and performance. Chrisman, Chua, and Sharma (2003), in their influential and early review of the family business literature, noted that only 3.2% of published articles were devoted to aspects of internationalization. More recently, Benavides-Velasco, Quintana-García, and Guzmán-Parra (2013), in their review of the literature, found only 2.5% of the articles addressing internationalization issues. The limited number of articles that did study internationalization focused on the parameters facilitating or restraining internationalization, on the managerial capabilities of the family members involved, and on the impact of internationalization on organizational growth. To the best of our knowledge, there have not been any family business studies assessing how human asset quality features, whether reflecting generic (generally available) or specialized (highly firm-specific) quality, were associated with particular levels of internationalization. In the present article, we focus on human asset quality, and we assess its impact on the internationalization of small and medium-sized family enterprises (SMFEs).

Addressing this issue is relevant because internationalization has become a common growth strategy for many family businesses (Kontinen & Ojala, 2010). However, while the role of family firms in most economies is key in terms of wealth and employment creation, the number of prior studies examining the internationalization behavior of these companies is limited (Fernández & Nieto, 2005; Graves & Thomas, 2008). The field is young and the relevant knowledge has not been consolidated.

Family firms are characterized by strong interactions between family and business (Zahra & Sharma, 2004), with family ownership and management viewed as critical features of these firms (Gallo & Sveen, 1991; Stern, 1986). Family ownership and management may confer specific “advantages” and “disadvantages” in the realm of internationalization. SMFEs supposedly have a long-term orientation (Astrachan, 2010; Claver, Rienda, & Quer, 2009). Therefore, if internationalization is important for firm growth, a strong commitment of family members to the firm, and their supposedly altruistic behavior, could promote the development of activities abroad (Zahra, 2003). At the same time, however, it has been observed that these companies often appear focused mainly on the domestic marketplace and face several idiosyncratic barriers to international expansion (Fernández & Nieto, 2006). Family firms may be prone to invest locally and exhibit risk-averse behavior (Gallo, Tàpies, & Cappuyns, 2004). Their financial capital is often limited (Olivares-Mesa & Cabrera-Suarez, 2006), and their conservative nature can have a negative impact on their international expansion (Fernández & Nieto, 2006). Important, in the context of the present article, is that SMFEs may find it comparatively difficult, relative to nonfamily firms, to upgrade effectively human asset quality, such as by recruiting and subsequently training qualified (nonfamily) professionals (Graves & Thomas, 2008).

Despite some research efforts devoted to internationalization during the past few decades, it remains unclear how internationalization in family businesses is initiated and developed (Pukall & Calabrò, 2014). It is therefore useful to examine the factors influencing the internationalization of these companies. Among these factors, human assets with attributes such as advanced knowledge, experience, and commitment often represent the most important firm-specific advantage (FSA) of SMFEs (Sirmon & Hitt, 2003). The process of accessing and deploying human resources with particular qualifications could potentially differentiate family firms from nonfamily ones, both in terms of conferring idiosyncratic competitive advantage and representing a distinct disadvantage. For example, comparatively closer relationships with employees, as compared with prevailing standards in nonfamily firms, might give family firm managers better knowledge of the human asset base they command that could be deployed for internationalization purposes. This could be the case even when these assets intrinsically possess only generally available rather than firm-specific quality features such as being related to a high education level rather than reflecting specialized R&D knowledge. The community of employees might also be nurtured more effectively than in nonfamily firms, leading workers to become culturally and psychologically better attuned to the firm’s needs in the international environment (Sirmon & Hitt, 2003). On the negative side, however, employing family members can lead to issues like suboptimal hiring and absence of professionalism, when trying to expand successfully abroad (Dunn, 1995).

Building on these issues, the main research question we try to answer in this article is the following: Is the quality of the human assets available to an SMFE associated with its level of internationalization? There has been insightful prior work on the effects of top management characteristics (Ruzzier, Antoncic, Hisrich, & Konecnik, 2007), but the quality of the broader human asset base including all employees has largely been neglected. In contrast, in the present article, we do focus on this source of potential strength, because beyond the entrepreneur and the top management team, other individuals can make key contributions to the firm’s success in the international market place (Cerrato & Piva, 2012; Rauch, Frese, & Utsch, 2005). In addition, the extant literature studying a direct causal link between the broad characteristics of the overall employee base and internationalization level is relatively scarce (Javalgi & Todd, 2011).

To the best of our knowledge, this research is the first to theorize on—and empirically test—an S-curved relationship between human capital quality and the firm’s degree of internationalization, whereby we make a distinction among three “states” of human capital quality (low, medium, and high), and also distinguish between generic and specialized human asset quality.

Specifically, in the realm of generic human asset quality, we hypothesize that in the low human asset quality “state,” the liability of outsidership (LOO) in international markets can easily be overcome. 1 This is typical for firms expanding into proximate markets only (Denk, Kaufmann, & Roesch, 2012; Eden & Miller, 2001; Moeller, Harvey, Griffith, & Richey, 2013; Zaheer, 1995). With the “state” of medium level, generic human asset quality, and especially when assuming expansion to higher distance markets, though this is not necessarily the case across the board, the home-country generic assets may actually become a (temporary) liability. Such generic assets are not able to support the firm in overcoming the LOO in the more distant markets. What should supposedly function as a competence actually becomes a rigidity, because of the weak recombination potential or inflexibility of the relevant human assets in the short run, and the firm’s excessive reliance on these ill-adapted resources. Finally, in the high human asset quality “state,” characterized by substantial firm-level investments in human asset quality, and assuming the relevant assets exhibit resilience and adaptation potential, they may help overcome the LOO. In this case, such asset quality would be linked with a higher level of internationalization.

We are cognizant of the possibility that different firms operating in different environments and faced with different customer needs might have different strategies to remain competitive, and that choosing particular strategies will affect their human resources management decisions and therefore their reservoir of human asset quality (Slocum, Lei, & Buller, 2014). However, in the present article we focus solely on international expansion through exports, as an expression of strategy. Analysis of broader interactions between business strategies and human resources practices, and how such interactions might affect export intensity, falls beyond the scope of the present article but could be considered in future research.

We find empirical support for our model in the context of generally available formal education, as a proxy for generic human asset quality. The results for the specialized human asset quality, measured in our article by the level of R&D Staff to total staff, are very different. Low R&D Staff is actually associated with strong international expansion, whereas increased R&D Staff can be linked to weaker internationalization.

The remainder of the article is organized as follows. In the next section, we develop our conceptual model and formulate our research hypotheses. In the third section, we describe the research method and empirical analysis. In the fourth section, we discuss the results of the empirical work. The last section presents our conclusions.

Theoretical Background

In mainstream international business research, the internationalization of small and medium-sized enterprises is viewed as contingent on the human assets at hand, which form the basis for possible FSAs (Verbeke, Osiyevskyy, & Zargarzadeh, 2014). Learning and related asset augmentations are instrumental to the firm’s expansion trajectory. Adaptation and learning are required to overcome the LOO (Johanson & Vahlne, 2009 ; see also Almodóvar & Rugman, 2014; Hymer, 1960/1976; Rugman, 1981).

Firms typically increase their internationalization level by their export intensity as they gradually accumulate knowledge about foreign markets. In the family firm context, it would also appear that SMFEs follow an incremental pathway to internationalization where they progressively approach foreign markets with greater psychic distance (Graves & Thomas, 2008).

Internationalization, especially of small and medium-sized firms, which may be weaker than large firms in having prior strengths in patented innovations or branding, often requires knowledge and experience embedded in human assets. Thus, if firms can strengthen their FSAs embodied in human assets, especially through making such assets nonlocation bound (Verbeke, 2013), this will allow overcoming the LOO and gaining higher international market penetration.

Conventional human capital theory (Becker, 1962, 1964/2009; Schultz, 1961) promotes the idea that education and training raise the productivity of workers by imparting knowledge and skills. Greater investment in human capital results in higher growth. Raising human asset quality can be obtained partly from education and partly from experience, typically gained in the firm itself. Therefore, it is possible to distinguish between two dimensions of human capital: (a) generic human capital derived from general education and (b) specialized, firm-specific human capital from having gained expertise in specific areas such as R&D.

Most of the mainstream literature has found a positive linear relationship between human asset quality and internationalization. For example, Wagner (1996) suggested that the proportion of jobs filled by employees with a university degree (in a sample of German firms) had a positive influence on export performance. Gourlay and Seaton (2004) found that human capital intensity, measured by the average wage paid, increased the probability of exporting in a panel of 2,134 U.K. firms between 1998 and 2001. Hitt, Bierman, Uhlenbruck, and Shimizu (2006) showed that human asset quality and relational capital have a positive effect on the internationalization of law firms. Furthermore, human asset quality was shown to moderate the relation between internationalization and firm performance.

López Rodríguez (2006), using a sample of Spanish manufacturing companies, found that generic and firm-specific human asset quality had a positive and significant effect on both the decision to enter into international markets and the subsequent intensity of sales achieved in these markets. Javalgi and Todd (2011) reported that human asset quality related positively to the level of internationalization of small and medium-sized enterprises from India. Cerrato and Piva (2012) showed that higher human capital quality and the presence of foreign shareholders in small and medium-sized enterprises positively influenced internationalization.

Recent research, however, has observed a nonlinear association between investment in human asset quality and the firm’s degree of internationalization. Onkelinx, Manolova, and Edelman (2012) found an inverted U-shaped relation between investment in highly educated employees and the firm’s degree of internationalization. They found that after an initial boost, investments in human asset quality reached a threshold impact, and then became less effective. There was a saturation point beyond which an increase in human asset quality did not translate into increased international activities.

Hypotheses Development

There has been some prior research in international business investigating the linkages between strength of FSAs, in the form of human asset quality, and the firm’s degree of internationalization. We consider three “states” characterized by low, medium, and high human asset quality, and we theorize about the possible linkages with internationalization. We focus first on generic human asset quality, and subsequently on specialized human asset quality.

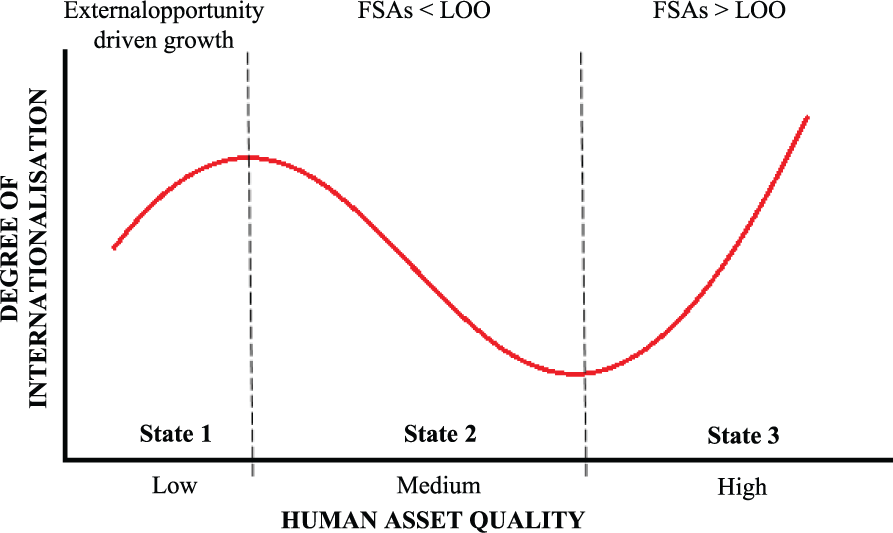

State 1: Low Human Asset Quality

Firms, especially small and medium-sized ones, expand abroad by entering psychically close countries. This “psychic distance” effect is consistent with the often-discussed home-region effect that characterizes firms going abroad. Firms first internationalize inside their home region and only after this geographic expansion attempt to move out further (Rugman, 2000, 2005; Rugman & Verbeke, 2004, 2008). When firms operate in psychically proximate markets or inside the home region, the LOO is typically small (Almodóvar & Rugman, 2014; Rugman & Verbeke, 2007). In fact, the LOO might be almost negligible if firms initiate their international activity as a response to unsolicited orders. These orders represent one of the most frequent drivers of early exports (Katsikeas, 1996; Leonidou, 1995; Leonidou, Katsikeas, Palihawadana, & Spyropoulou, 2007).

In this case, increasing low initial levels of human resources quality, especially of the generic type, reflects an opportunity-driven managerial focus, especially in family firms, on getting the job done through augmenting moderately the education level of the employee base, which consists mainly of nonfamily members (cf. Verbeke & Kano, 2012). Family ownership and managerial control may also accelerate decision making in the realm of internationalization. Family businesses can initially succeed and increase their international sales even when the somewhat augmented human resources base remains below par (Almodóvar, 2012; Almodóvar & Rugman, 2014; Collinson & Rugman, 2011; Lee, 2013; Rugman & Almodóvar, 2011; Rugman, Verbeke, & Nguyen, 2011).

Given that many family firms (a) are focused mainly on increasing family wealth; (b) begin their internationalization process as a result of unsolicited orders (Graves & Thomas, 2008; Okoroafo, 1999, 2010), typically coming from proximate markets; and (c) can engage in fast decision making on foreign expansion without being encumbered by sophisticated management routines, we hypothesize that low, but increasing, levels of human capital quality can be expected in internationalizing firms, and will support international growth. Thus, we hypothesize the following:

State 2: Medium Human Asset Quality

When moving toward more distant markets, it often appears that entrepreneurs and managers have overestimated the transferability, deployment opportunities, and profitable exploitation potential of their FSAs. To put it differently, they have overestimated the nonlocation boundedness of their FSAs. They need to invest in higher quality human assets to be recombined with resources available in foreign markets to overcome the LOO (Rugman & Verbeke, 2007; Verbeke, 2013; Verbeke & Kano, 2012).

After hiring better quality employees, the problem is matching the improved human asset base with the requirements of international expansion. The timing issue is especially salient in family firms, where family members may have been in charge of early internationalization efforts. They may have faced a low LOO, but now need to deploy new, qualified nonfamily employees to support internationalization efforts in higher distance markets.

The timing challenge should not be underestimated. Adapting new and better qualified human resources to the needs of international expansion may be hindered by a “bifurcation bias.” The bifurcation bias was defined by Verbeke and Kano (2012) as the dysfunctionality resulting from the asymmetric treatment of family members and nonfamily members. This asymmetric treatment refers to treating nonfamily members as less valuable assets, unlikely to remain in the firm in the long term, and being less loyal and less committed to the business. As a result, human resources management practices, such as training, performance evaluation, and compensation systems, are biased against nonfamily members (Verbeke & Kano, 2012). According to Verbeke and Kano (2010), this asymmetric treatment generates severe problems of bounded rationality and unreliability.

Asymmetric treatment between family members and professional employees may lead to unwarranted delays in requisite adaptation of the human assets to the needs of the business in high distance environments. In other words, even the upgrading of human asset quality to a medium level by hiring more employees in the home base with a better education will still be associated with a slowing down or even a deterioration of the firm’s international expansion trajectory. This would occur because of the requisite training/adaptation of these new resources to meet the demands of foreign markets with a high LOO and will be slow. Based on these premises, we formulate the following:

State 3: High Human Asset Quality

Family firms characterized by high, overall human asset quality have typically been successful in overcoming their intrinsic bifurcation bias. They have done so by hiring more highly educated workers across the board rather than favoring family members for specific positions, and providing opportunities to them for adaptation to the needs of foreign environments. According to Verbeke and Kano (2010), equal treatment in training opportunities and other human resources practices of both nonfamily and family employees further reduce bounded rationality by enhancing all employees’ competences and skills. Such an unbiased approach can subsequently reduce bounded reliability by improving relationships between the equally treated family and nonfamily employees.

This new equilibrium will strengthen nonfamily employees’ loyalty and motivation and is likely to support the firm’s international expansion. Furthermore, a formal international department to manage overseas expansion is more likely, and it will select the best human assets to support international expansion (Stoian, Rialp, & Rialp, 2011). Building on these arguments, we predict the following:

This model with the three “states” is shown for illustrative purposes in Figure 1.

Hypothesized S-curved relationship between human asset quality and degree of internationalization (illustrative shape).

The Case of Specialized Human Asset Quality

Do the predicted linkages between level of human asset quality and level of internationalization also hold for specialized knowledge? Recent work by Zargarzadeh, Verbeke, and Osiyevskyy (2016) would suggest a somewhat different set of linkages. These authors found that small and medium-sized entrepreneurial companies have a limited capacity on the part of their senior management teams, whereby senior managers cannot focus simultaneously on guiding and monitoring higher R&D activity and higher international expansion activity.

The aforementioned would mean that apart from a boost by having at least some internal R&D Staff so as to create requisite absorptive capacity in the innovation sphere, there will typically be an expectation that increasing further specialized human asset quality will be detrimental to the SMFE’s international presence. Attempts to increase specialized human asset quality beyond a threshold level will exacerbate the “divided attention” challenges faced by the management team and limit this team’s capacity to support international expansion.

Only in the longer run, when diversifying into product lines specifically geared to international markets, would access to higher, specialized human asset quality be useful to support internationalization. The advantages could include attributes such as better technical support for customers, better knowledge to adapt products to local requirements, and more effective response to new demand-side opportunities. However, even then it remains unclear whether management capacity will be sufficient to reach the internationalization levels that can be achieved with a low R&D Staff to total staff ratio. Especially in SMFEs, the “best case” of high internationalization would seem to be one with advanced R&D embodied in the firm’s products, but with comparatively limited R&D Staff relative to total staff, being guided and monitored by the typically small senior management team, often consisting mainly of family members.

Research Methodology

The Sample: SMFEs in Spain

According to the Spanish Family Business Institute (Instituto de la Empresa Familiar, 2009), there are 2.9 million family businesses in the country. These represent 85% of the total number of Spanish companies (comparatively, the EU has 60% of family firms, and the United States 80%). These companies generate 70% of the Spanish gross domestic product and 70% of the employment in the private sector. In each of these firms, family members serve on the board, and in 94% of the cases in executive positions.

We used data from the Survey on Business Strategies, that is, a database that includes information on a representative panel of Spanish manufacturing firms with 10 or more employees. The Foundation SEPI (Sociedad Estatal de Participaciones Industriales) gathers this information on a yearly basis with the support of the Spanish Ministry of Industry. One of the main strengths of this database is that it does not suffer from the usual common method bias associated with surveys. This is due to the usage of multiple respondents per firm, the inclusion of many questions asking for factual rather than “perceptual” information, the guarantee of anonymity, and the inclusion of more than 100 control questions to check for reliability.

Our sample covers the period 2006 to 2010 and is focused on SMFEs, defined as family firms with fewer than 200 employees (Almodóvar & Rugman, 2014; Fernández & Nieto, 2006; Golovko & Valentini, 2011). There is no generally agreed-upon definition of what constitutes a family firm in the literature (Benavides-Velasco et al., 2013; Graves & Thomas, 2008; Sharma, 2004). In our research, the SBS introduced a specific question in 2006 as to whether a family group is actively involved in the management of the company. Possible replies are yes/no. This led us to extract information for the 2006 to 2010 period on an unbalanced panel of firms, with 3,050 observations, 610 firms per year on average, from 20 distinct manufacturing industries.

Variables and Metrics

Dependent Variable: Internationalization–Export Intensity

There are several possible measures of internationalization (e.g., usage of a dichotomous variable, number of countries to which a firm exports, etc.). Rugman and Oh (2011), in their review of internationalization metrics, concluded that scale metrics, such as export intensity and foreign sales over total sales, constitute the best choices. In the present article, we use export intensity, or the ratio of exports to total sales. It is the most widely adopted measure in the literature on small and medium-sized enterprises’ internationalization (Cerrato & Piva, 2012). For smaller Spanish companies, exports are the favored entry mode choice.

Independent Variable: Human Asset Quality

Given that there is disagreement on what constitutes the most important intangible assets to support the internationalization process (Veng Søberg, 2012), we include in our study both the generic (generally available) knowledge derived from education and the much more specialized (firm-specific) knowledge tied to conducting R&D activities. Both “qualities” contribute to the absorptive capacity of firms (Cohen & Levinthal, 1990). Many studies have shown that knowledge derived from education and R&D activities is fundamental to the firm’s output in the long term (Ballot, Fakhfakh, & Taymaz, 2006). Both qualities can amount to being the essence of core FSAs critical to firm-level internationalization (Rugman, 1981). We used these measures for two reasons:

First, the employees’ education level is an observable expression of human asset quality (Rauch & Rijsdijk, 2013), since it captures their general knowledge and skills (Onkelinx et al., 2012). We calculate an index of the weighted average education level by assigning a weight of “3” to engineers and graduates from institutions of higher education, a weight of “2” to nongraduate employees with engineering and other expertise, and a weight of “1” to other personnel (Autio, Yli-Renko, & Sapienza, 1997; Onkelinx et al., 2012). In order to capture the predicted cubic relationship between this variable and export intensity, as explained in the Hypotheses section, we created two more variables, raising the original education level to the power of two, and three.

Second, we proxy the R&D knowledge embodied in the human assets by calculating the R&D Staff ratio as the number of R&D employees relative to the overall number of employees (Ballot et al., 2006 ; Wang & Chang, 2005). This ratio is relevant because the science-base of the company, embodied in its R&D personnel, can improve its capacity to absorb external knowledge/learning (Cohen & Levinthal, 1989). For example, Veugelers (1997) and Gao, Xu, and Yang (2008) included the variable R&D human capital in their studies as a proxy to measure absorptive capacity. We of course do need to take into account the insights from Zargarzadeh et al. (2016) on the dangers of divided attention facing senior management when pursuing an internal innovation strategy and an international expansion strategy simultaneously. An initial boost to a low R&D Staff ratio may increase absorptive capacity and support high internationalization levels, but a medium R&D Staff ratio will divide attention of senior management and be detrimental to internationalization. Finally, a high R&D Staff ratio may reflect the fact that innovation is the firm’s core competence, with the importance of specialized human asset quality overriding the challenge of divided attention up to a particular level of international involvement. In order to capture the idiosyncratic cubic relationship between this variable and export intensity (i.e., linking the impact of increasing R&D Staff in SMFEs in three “states,” that is, low, medium, and high), we create two more variables, raising the original R&D Staff ratio to the power of two, and three.

Control Variable (CV): External Training

Ever since the seminal work of Becker (1962, 1964/2009), the economics and management literature has acknowledged the impact of general and specific training on productivity, wages, and performance (Ballot et al., 2006; Leuven, 2005; Nguyen, Truong, & Buyens, 2011). Here, we assume that training can support internationalization by incorporating a dummy variable for on-the-job training. We code this as one when the firm invests in external training, and zero otherwise.

CV: Firm Size

We include firm size as a proxy for the resource endowments that can be deployed to support exports (Gourlay & Seaton, 2004). More specifically, adopting a Penrosean perspective, we use the number of employees in the company as a proxy for the resources deployable to aid with internationalization.

CV: Research Intensity

We include R&D intensity, measured as the ratio of R&D expenditures to total sales, because it is a proxy for new product development, a potentially important FSA supporting internationalization, according to the mainstream literature in international business.

CV: Advertising Intensity

We include advertising intensity, measured as the ratio of advertisement expenditures to total sales, another potentially important FSA supporting internationalization, according to the mainstream literature in international business.

CV: Firm Experience–Age

We measure the firm’s experience as the number of years the firm has been operating since inception. Past experience derived from the firm’s age is sometimes viewed as instrumental to internationalization, though this has been debated in the literature because experience can be embodied in the knowledge and skills sets of managers gained outside of the firm, and even before inception (Verbeke et al., 2014).

CV: Industry Effects

We introduce 20 industry dummy variables to control for industry effects. For simplicity of exposition, Table 2 shows only the significant industry effects.

Statistical Analysis

We performed a poolability test leading to the conclusion that with our data, panel data treatment was more appropriate than pooled data treatment, thereby leading the regressors to benefit from more variability and less collinearity (Baltagi, 2001; Hsiao, 1986).

Following Cassiman and Golovko (2011) and Almodóvar and Rugman (2014), we first selected random effects to control for unobserved firm heterogeneity because of potential omitted variables. Second, we checked the stationarity of our data, and because we have an unbalanced panel, we conducted the Fisher unit-root test. The null hypothesis states that all series are nonstationary. We obtained p values lower than .05, suggesting stationarity.

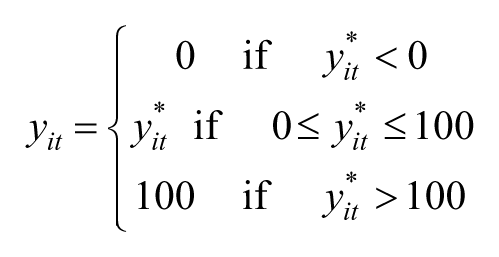

Our dependent variable (export intensity) is a percentage that ranges from 0 to 100. We formulated two-limit Tobit models in order to avoid bias for underestimating or overestimating intercepts and slopes. Considering that we work with unbalanced panel data, our final specification was as follows:

where

Here, y* is the latent dependent variable whose values range from 0 to 100. The vector of exogenous regressors is represented by x′, and the vector of unknown parameters is β; ε it is the error term and it can be decomposed in two components: ui (unobserved firm-specific disturbance) and vit (idiosyncratic error). Finally, the subscript i refers to the firm, and t represents the year (from 2006 to 2010).

Following Reeb, Sakakibara, and Mahmood (2012), we tested for endogeneity, which is a common problem in international business studies. Given the nature of our dependent variable Export Intensity, we conducted a specific test for Tobit models developed by Smith and Blundell (1986). We used “income from licenses and technical aid from abroad” as an instrumental variable. It is significantly correlated with both Education Level and the R&D Staff ratio, but it is not significantly correlated with Export Intensity. We obtained p values higher than .1, so that we can assume our model is well specified because our variables are exogenous.

Results and Discussion

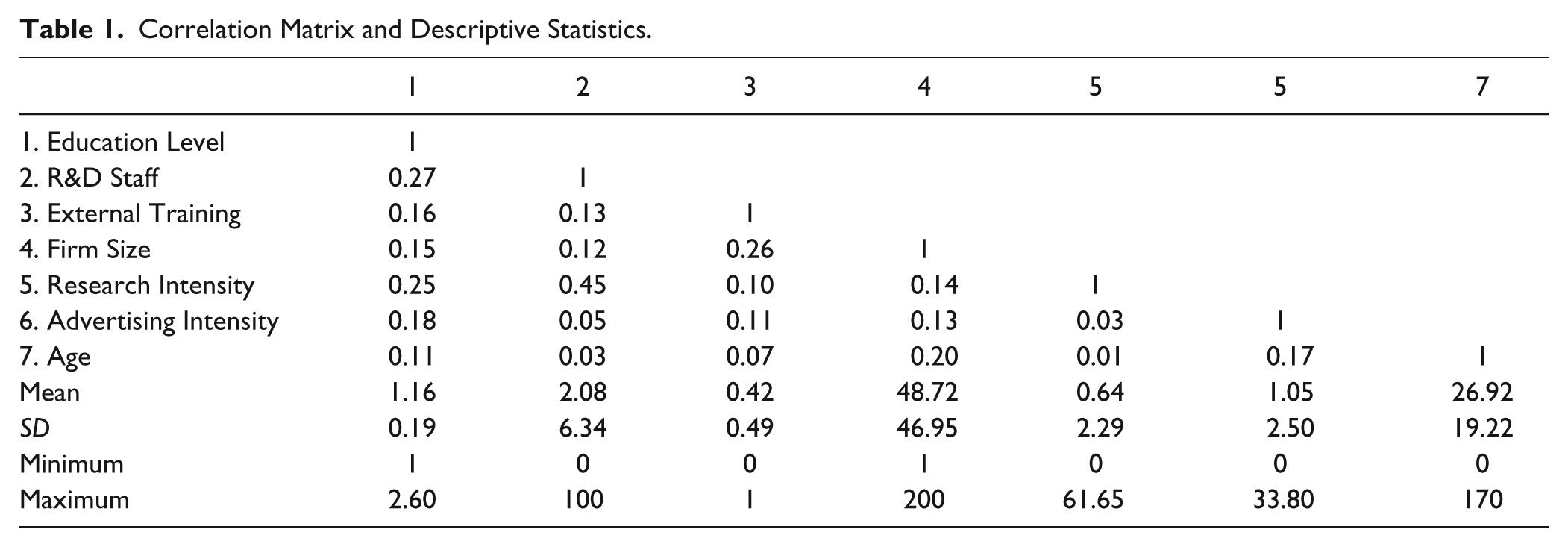

Table 1 shows the descriptive statistics and the correlation matrix with the independent and control variables. There are no severe multicollinearity problems among variables because there is no case above 0.5. We do, however, observe a correlation of 0.45 between the R&D Staff ratio and R&D Intensity. In order to examine further multicollinearity threats, we checked the variance inflation factor (VIF) and performed tolerance analyses. Individual VIF values are all smaller than 3.23, with a mean VIF of 1.65, which is much lower than the typically recommended maximum allowable value of 10 (Chatterjee & Price, 1977); tolerance analyses are well above the recommended 0.1 figure. The tests performed suggest the absence of multicollinearity issues (Neter, Wasserman, & Kutner, 1989). Nonetheless, we are aware of the fact that we do explicitly introduce some level of multicollinearity because of the nature of our model, which includes squared and cubic transformations of the independent variables.

Correlation Matrix and Descriptive Statistics.

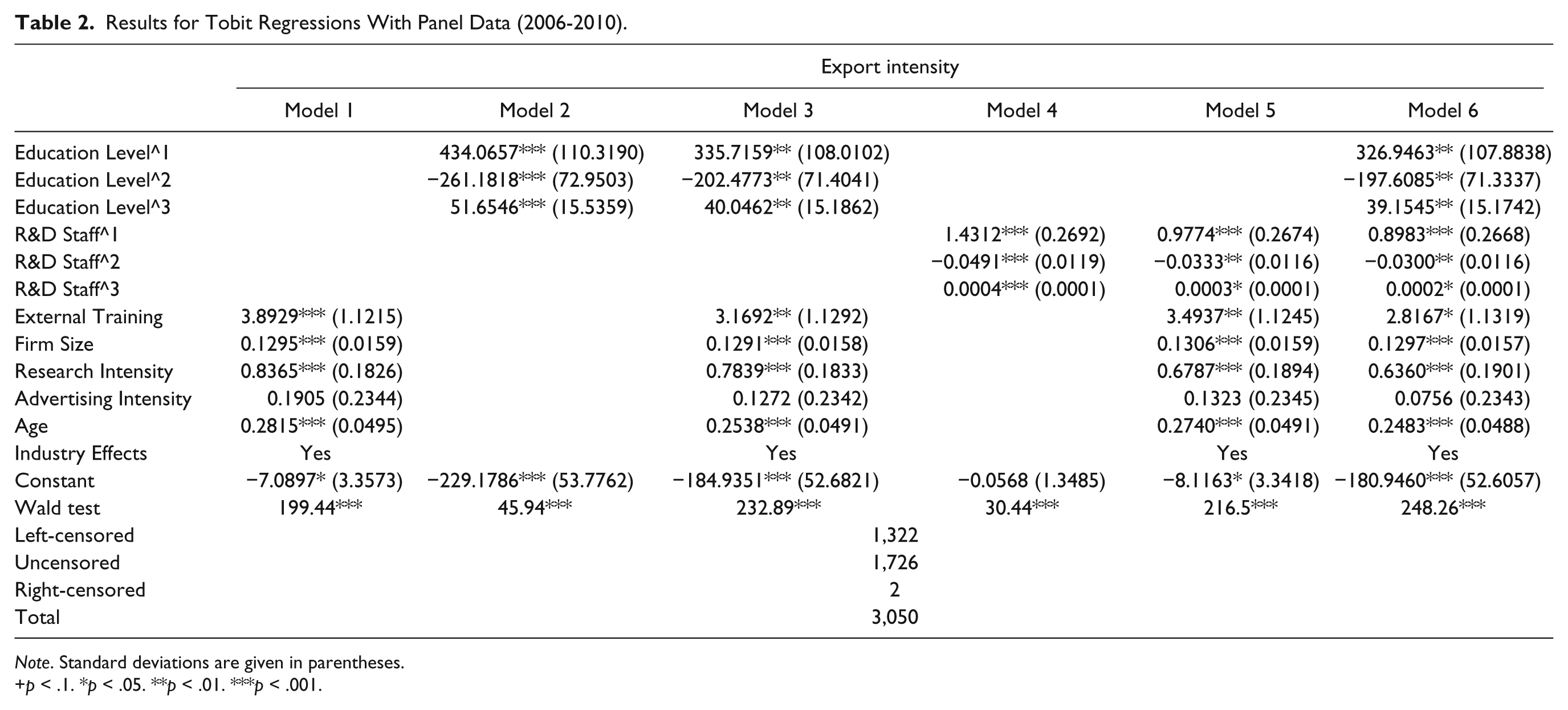

Table 2 shows six different models. Model 1 only includes the control variables. Models 2 and 4 only consider the independent variables (Education Level and R&D Staff, respectively). Models 3 and 5 display one independent variable plus the controls. Finally, Model 6 includes the full set of variables.

Results for Tobit Regressions With Panel Data (2006-2010).

Note. Standard deviations are given in parentheses.

p < .1. *p < .05. **p < .01. ***p < .001.

The Wald tests we conducted are all significant, so we can assume that at least one predictor is statistically different from zero in every model. We also conducted likelihood ratio (LR) tests to compare the models and to select the model with a significantly better fit. We tested whether Models 1, 2, and 4 are nested within the relevant Models 3 and 5, and whether Models 3 and 5 are nested within Model 6. The first set of LR tests led to p values <.001: Excluding the control or independent variables would significantly reduce the fit of Models 3 and 5. Similarly, the second set of LR tests showed p values <.001 as well, meaning that Model 6 represents the best fit. We will focus on this last model to discuss the testing of our hypotheses. As regards robustness, the significance level and coefficient signs remain stable across variables and behave homogeneously across the six models. Based on these tests, we can conclude that our models are consistent and robust.

As regards the impact of Education Level, we observe significant levels (p values <.01) for the three coefficients, thereby shaping an S curve, and supporting Hypotheses 1, 2, and 3. This means that, in the first “state” of low human asset quality, which is generally available, an increase thereof is associated with more effective internationalization outcomes, typically because only limited local adaptation is required. SMFEs with increasing human asset quality, through having employees who are better educated, obtain better results in initial internationalizing.

Firms moving to a higher general education level of their employees then see internationalization is negatively affected, meaning that this resource is clearly “location bound,” and somewhat works against further increasing export intensity. One reason may be that higher export intensity is typically associated with entering more distant markets. The LOO may require more extensively adapted resources to be successful, and general education earned in the home country may actually represent, again in the short to medium run, a core rigidity instead of an FSA.

Finally, in the “state” with the highest export intensity, it would appear that SMFEs do have an employee base with a higher education level. These firms have been able to leverage this knowledge reservoir to support effective internationalization. One interpretation is that, after having faced a higher LOO associated with the second “state,” whereby stronger home country general knowledge somewhat works against the firm adapting rapidly to more distant foreign environments, this same location-bound asset quality can be made effective again. This occurs after the human assets’ limits have been exposed, and requisite resource recombination has been achieved, reflecting these assets’ resilience and long run adaptation quality.

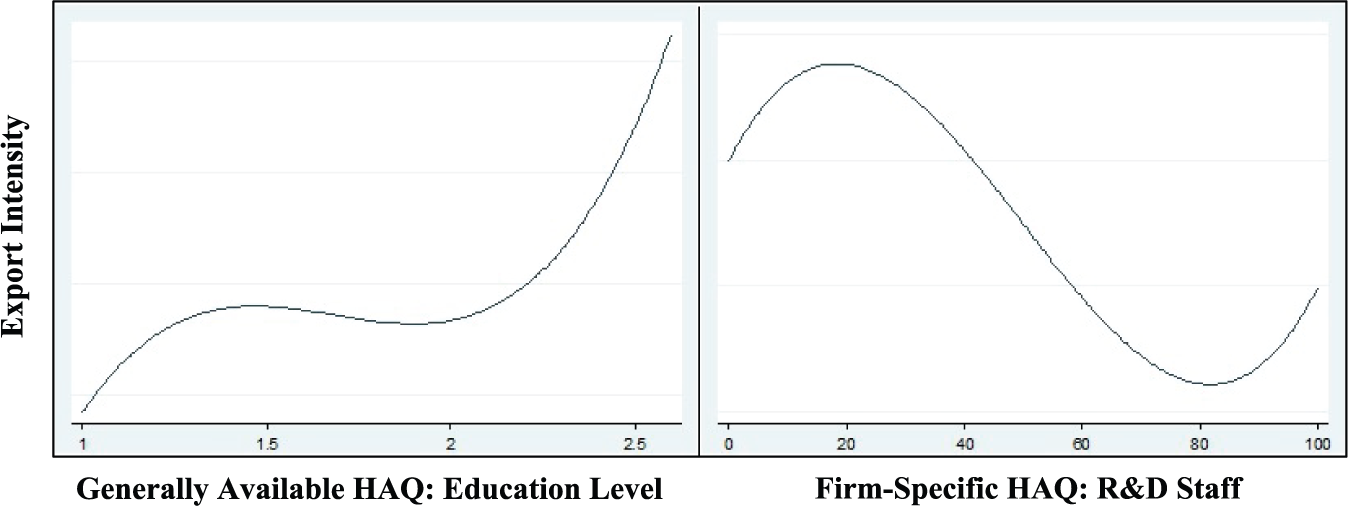

As regards the R&D Staff ratio, that is, the second metric for human asset quality, we obtained results that are somewhat similar to those of the impact of the Education Level parameter. The results indeed also suggest a curvilinear relationship between R&D Staff and internationalization, but here, the “state” of low R&D Staff is actually associated with the highest levels of Export Intensity. In Figure 2, we plot both cubic polynomials.

S-curved relationships between human asset qualities (HAQ) and internationalization (export intensity).

Figure 2 depicts the predicted linkage between Export Intensity and Education Level on the left-hand side, and the linkage with the R&D Staff ratio on the right-hand side. The different specific shapes of the curves highlight an interesting variation in the impact of both parameters. Education Level has a positive overall effect on internationalization, and the negative impact in the second “state” can likely be explained by the temporary effect of the LOO, whereby time and effort are required for adaptation. Verbeke and Kano (2016) suggest that this is a common occurrence in firms that have been highly successful at home and sometimes also in a first attempt at proximate internationalization. Here, the nonlocation boundedness of the FSAs at hand, in this case in the realm of human asset quality, is overestimated when entering higher distance markets.

The S-curve relating R&D Staff and internationalization is very different. Increasing R&D Staff in the low human asset-quality “state” is helpful when supporting already high levels of internationalization, but in the “state” of medium-level R&D Staff, further increases of such staff have a strongly negative association with export intensity. Zargarzadeh et al. (2016) reached an equivalent conclusion based on a large sample of entrepreneurial companies in the United States. From a Penrosian perspective, having more R&D Staff may actually be detrimental to internationalization and the performance thereof, because of the limited management capabilities present in smaller, entrepreneurial companies. In other words, a trade-off must be made between allocating management attention to guiding and monitoring people active in product innovation versus active in international market expansion. This might hold especially in the short and medium run, because it takes time to increase the firm’s management capabilities. Even in the longer run, when the firm’s management capacity has been adjusted, the trade-off remains, and this is especially valid in family firms, which are intrinsically slower in augmenting their management capabilities with outside, professional (nonfamily) managers than nonfamily firms.

As regards the control variables, most of these yield results consistent with the predictions from the mainstream literature. External Training has a positive and significant effect on export intensity. Firm Size (p value <.001) also has a positive and significant impact. R&D Intensity, perhaps paradoxically, has a positive and significant impact too (p value <.001), in line with mainstream international business theory. Higher R&D Intensity does not necessarily entail the usage of more management capacity, at the expense of time and effort that can be deployed for purposes of internationalization. It simply refers to more money being spent on innovation but not more management needed to guide and monitor R&D Staff. The firm’s Age, as a proxy for firm experience, exhibits the same positive and significant effect (p value <.001). Finally, there are significant Industry Effects. Posttests conducted to compare the coefficients of the control variables within the same model lead us to conclude that External Training and R&D Intensity are the most important control parameters affecting internationalization.

Conclusion

This is the first empirical study linking human asset quality available to the firm and internationalization levels. In the context of SMFEs, we have conducted an empirical analysis building on data from Spanish SMFEs for the period 2006 to 2010. Using two metrics for human asset quality available to the firm, namely, the education level of the employee base (generic or generally available human asset quality) and the ratio of R&D Staff to total employees (specialized or firm-specific human asset quality), we observed idiosyncratic S-curved relationships with internationalization.

We have offered a new perspective showing how human assets, both generally available and highly firm-specific ones, and not only managerial resources, are associated with specific internationalization levels. Our results show substantial variation in the levels of knowledge possessed by employees. Both generally available formal education and highly specialized R&D activities of employees appear important in the context of SMFE internationalization.

Our article has important implications for both researchers and practitioners. Our contribution to the academic debate emphasizes the importance of endogenous factors in explaining internationalization levels. It also shows that the association between human asset quality and the degree of internationalization is complex and does not appear to follow a linear pattern, but rather a curvilinear one, with its precise form dependent on whether generic or specialized assets are at play.

Our research also helps family business owners and managers to better understand the effects of human asset quality in the internationalization process. We show that different types of employees’ knowledge do not have a uniform association with—or impact on—international expansion. SMFEs must access and leverage human assets, especially generally available ones, in order to seize opportunities in international markets. Family business owners and managers must monitor carefully the available human asset reservoirs that can be deployed in international markets and build on these to support internationalization efforts.

In terms of avenues for future research, our empirical work was confined to Spanish firms only. Further testing of the observed relationships between human asset qualities and internationalization levels in other empirical settings should now be performed. In addition, and this holds for most research conducted on SMFEs, it would be advisable to study how differences in family firms such as the level of involvement of professional, nonfamily managers, when linked with human asset qualities of the overall employee base, could affect internationalization trajectories.

Footnotes

Acknowledgements

This article is dedicated to the memory of Alan M. Rugman for his mentorship, support, wisdom, and never-ending kindness.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.