Abstract

Due to the complexity of real security market, sometimes the future security returns can only be valued based on experts’ estimations. Meanwhile, there are transaction costs and minimum transaction lots requirement in the real transaction process in the trading market. This paper discusses the portfolio selection problem in such a circumstance. Security returns are considered as uncertain variables, and a new mean-variance model with transaction costs and minimum transaction lots is established. In addition, the impact of minimum transaction lots requirement and transaction costs on optimal portfolio is discussed and a genetic algorithm for solving the optimization model is given. As an illustration, a numerical example is provided.

Keywords

Introduction

Portfolio selection is concerned with the investment of one’s money in a variety of securities so that maximum return is obtained and investment risk is controlled. Markowitz [26] first proposed the mean-variance model. In the mean-variance model, the expected return was regarded as the investment return and variance the risk. The investment strategies should be achieved on the efficient frontier of the return and risk. Since Markowitz, portfolio selection models have been put forth in extensive studies and a wealth of research results have been obtained. There are some important examples including safety-first models [19, 37], single-factor models [33, 38], multi-factor models [8, 34], mean semi-variance models [4, 27], expected absolute deviation methods [18, 35], Value at Risk models [17, 28], Conditional Value at Risk models [1, 36], mean semivariance-CVaR model [29], worst conditional expected value model [5], Expected Shortfall model [3], mean-risk curve model [9], etc.

In classical portfolio theory, the security returns are considered as random variables and their characteristic values such as expected value and variance are calculated based on the sample of available historical data. This calculation method implies that historical data are sufficient and can well reflect the future security returns. However, due to the complexity of the security market, historical data are sometimes insufficient or unable to reflect the future security performances. In this situation, security returns have to be given mainly by experts’ estimations rather than historical data and thus contain much subjective imprecision rather than randomness. Since men’s estimations are not random in nature and usually contain much wider range of values than the imprecise parameters really take, if we inappropriately use probability theory to deal with men’s estimations, paradoxes might appear [22]. To deal with the portfolio selection problem in this situation, Huang [10] initiated an uncertain portfolio selection theory using uncertainty theory proposed by Liu [20] as the tool. By using the uncertainty theory, no paradoxes appear. Since then many studies have been done on the development of uncertain portfolio selection theory. For example, Huang [11] further investigated the uncertain mean-variance model in depth. Huang [12] proposed a risk index model for uncertain portfolio selection, and Huang and Ying [13] further developed the model which considered portfolio adjusting problem. Li and Qin [24] studied the interval portfolio selection problem under the uncertain environment. Huang and Zhao [14] established a mean-chance model within the framework of uncertainty theory. Furthermore, Huang and Di [15] proposed and studied an uncertain portfolio model which considered not only uncertain security returns but also uncertain background assets. Qin [31] studied a portfolio selection problem in the simultaneous presence of random and uncertain returns.

In Huang’s paper [10], the transaction costs of purchasing and selling were not taken into consideration. However, there are costs such as stamp duty, transaction fees, and commissions in the procedure of purchasing and selling securities in the real life market. The transaction costs are inevitable [2]. Therefore, the ignorance of transaction costs in the model may lead to the invalid portfolio. Meanwhile, in Huang’s model [10], all securities were assumed to be infinitely divisible. Under such assumptions, the share and weight of each stock are continuous, and the corresponding efficient frontier is a continuous, uninterrupted curve. However, in the actual transaction process, each security market requires minimum transaction lots. In this case, the assumption of infinite division may result in significant error which makes it impossible for investors to achieve their target of investment, and may even bring them a loss. Therefore, it is significant to consider the minimum transaction lots in the model for practical application. The purpose of this paper is to discuss the portfolio selection problem which considers transaction costs and minimum transaction lots requirement in the uncertain environment.

The paper proceeds as follows. In Section 2, some necessary knowledge about uncertain variables will be introduced for easy understanding of the paper. In Section 3, an uncertain portfolio selection model with transaction costs and minimum transaction lots requirement in the uncertain environment will be proposed and discussed. In Section 4, the genetic algorithm will be designed for the nonlinear integer programming model we proposed. In Section 5, we will provide and discuss a numerical example to demonstrate the effectiveness of our proposed algorithm. Finally, we will conclude the paper in Section 6.

Necessary knowledge about uncertain variable

Necessary knowledge about the uncertainty theory used in the manuscript will be introduced in this section.

(Normality) M { Ω } = 1; (Self-duality) M { Γ } + M { Γ

c

} = 1; (Countable subadditivity) For each countable sequence of events {Γ

i

}, We have:

(Product measure) (Liu [21]) For uncertainty spaces (Ω

i

, L

i

, M

i

), i = 1, 2, …, the product uncertain measure is:

For example, a normal uncertain variable is the one that has the following normal uncertainty distribution

The operational law of the uncertain variables is given as follows:

To tell the size of an uncertain variable, Liu defined the expected value of uncertain variables.

It indicates that at least one of the two integrals is finite.

It can be calculated that the variance value of a normal uncertain variable ξ ∼ N (μ, σ) is V [ξ] = σ2.

In applications, we call

The product of a normal uncertain variable N (e, σ) and a scalar number k is also a normal uncertain variable in Equation (5).

Uncertain model

As discussed in the introduction, when security returns are given mainly by experts’ estimations, it is better to use uncertain variables to describe the security returns. Meanwhile, transaction costs and minimum transaction lots requirement usually exist in the actual transaction process in the trading market. Therefore, we take them into account in this paper.

Let ξ i denote the uncertain returns of the ith securities which are defined as ξ i = (pi1 - pi0)/pi0, i = 1, 2, …, n, respectively, where pi1 are the selling price of the ith securities, pi0 are the purchasing price of the ith securities. Let a be the transaction cost rate of purchasing and b the transaction cost rate of selling. Due to transaction costs, the real yield of the security is not equal to the nominal yield. The actual expenditure of security is pi0 (1 + a) and the actual income of the sale of security is pi1 (1 - b). Real yield taking transaction costs into account should be as follows:

We call R i the real yield of the ith securities.

Let q

i

be the minimum transaction lots of the ith securities and x

i

a positive integer which is the number of minimum transaction lots of risk asset i. It is easy to know that the transaction lots of risk security i is q

i

x

i

. Then the cost of purchasing risk security is q

i

x

i

pi0 (1 + a). Let B be the total available funds of investors. Then the investment weight of security i is w

i

= q

i

x

i

pi0 (1 + a)/B. Because of the existence of minimal transaction lots requirement, it is possible that

Then, the return rate of the portfolio with transaction costs and minimum transaction lots requirement can be expressed as:

The expected value and the variance of the return rate of the portfolio are as follows:

The mean-variance model aims at finding out the most desirable portfolio only by the first two moments. Expected value of the total return is regarded as the investment return, and the variance is used to measure the investment risk. A typical mean-variance model is to compromise between risk and return. For example, we may choose a portfolio with minimum investment risk on the condition that the acceptable return level is given. We may also choose a portfolio with maximum investment return on the condition that the tolerable risk level is given.

However, in practice, an alternative way is to provide a factor representing the risk preference by trading off between return and risk. Thus, we can establish the following compromise model:

Among them, λ ∈ [0, 1] is the risk preference coefficient. The lower the λ, the more risk preference of the investors.

In order to solve the proposed model (7), we convert it into its equivalent when each security return rate is a normal uncertain variable.

As ξ

i

, i = 1, 2, … n are independent normal uncertain variables, from Theorem 3, we know that O is a normal uncertain variable and

In addition, 0 < b < 1, then

Thus the theorem is proved.

To consider the transaction costs and the minimum transaction lots requirement, it is necessary to analyze the impact of the minimum transaction lots requirement and transaction cost rate on the optimal value of portfolio objective function.

From model (8), it can be seen that the solving space of the problem which considers the minimum transaction lots is smaller than non-considering one. Therefore considering the minimum transaction lots will lead to the optimal value lower than the value without considering the minimum transaction lots.

Below we analyze the situation considering transaction costs. When there are no transaction costs, the model (8) is translated into the following one:

Although transaction costs will reduce the return of the portfolio, they also will reduce the risks of the portfolio. Theorem 5 gives the condition on which the value of optimal portfolio would diminish when considering transaction costs.

Assume that the optimal solution of model (8) is

If λ ≠ 0, we can get:

Since a ≥ 0, we have 1 + a ≥ 1. Then we can get:

Since

So

if λ = 0

Thus, the theorem is proved.

The equivalent model (8) is a complex integer nonlinear programming model and it is difficult to be solved by traditional methods. The advantage of genetic algorithm (GA) is that it can solve complex optimization problems. Based on the Darwin principle “the fittest survive” in nature, genetic algorithm (GA) was first initiated by Holland [16] and has rapidly become the best-known evolutionary techniques [7, 30]. So the GA is designed for solving the integer nonlinear programming model we proposed. The design of GA will be described below.

Chromosome representation

A feasible solution of model (8) is represented as a chromosome C = (g1, g2, …, g

n

) where g

i

, i = 1, 2, …, n represent x

i

, i = 1, 2, …, n, respectively. Since the total amount of funds is fixed, then the range of values for g

i

should satisfy the constraint:

Generate the initial population

Initialization is used to generate the first population. Define an integer pop_size as the size of the population. The procedure is described as follow:

First, generate a chromosome C = (g1, g2, …, g n ) randomly where for each i, g i ∈ Z.

Second, check the feasibility of chromosome by identifying if

Generate the position j randomly where g

j

needs to be adjusted. To ensure the effectiveness of the adjustment process, g

j

must be nonzero. Calculate the total current assets value corresponding to position j. If

Third, repeat the above steps for pop_size times. Then pop_size feasible initial chromosomes are generated.

The objective function in model (8) is a max-value function that is consistent with the largest fitness principle. Therefore, the objective function of the proposed model is taken as the fitness function. GAs require the fitness to be positive [25]. However, in our model, the objective function may be negative within the domain of definition. We should process the objective function to make it positive. The fitness function of chromosome

The roulette wheel selection method is used in the selection operation in this research. The individuals with higher fitness values are taken as parents. The elite mechanism is used to prevent the loss of high-quality individuals. The process is as follows:

First, calculate fitness value of each chromosome C k , k = 1, 2, …, pop _ size, of the population. The maximum fitness value is F fitness (C max ) and C max is the corresponding chromosome.

Second, calculate propagation probability of chromosome C

k

as:

Third, calculate the single cumulative probability of chromosome C

k

as:

Fourth, generate a random number r in the from the open interval (0, 1) and then select the kth chromosome C k if P (C k ) < r ≤ P (Ck+1).

Fifth, repeat the fourth step for pop _ size - 1 times, and combine with C max . Then pop _ size chromosomes are selected as the parents population.

The Single-point crossover operator is used to generate intersections in this research. Determine a parameter rc ∈ (0, 1) as the probability of crossover. Pair of parents are selected for crossover in the population according to the crossover rate rc. The crossover operator performs the exchange of segments between pair of parents [25]. The chromosome C

k

is selected as a parent when the randomly generated real number r from (0, 1) is less than rc at the kth selection, where k = 1, 2, …, pop _ size. Let

First, generate a random integer l from the open interval (0, n). Crossover operation on each pair is illustrated on

Second, as the switched new chromosome may not satisfy the constraints of the model (8). Let

Generate the position j randomly where

Third, repeat the above steps until all parents are crossed, then replace the parents with the feasible children.

The Single point mutation operator is used in mutation operation in this research. The mutation operator performs the change of a gene of parents. Determine a parameter r

m

∈ (0, 1) as the probability of mutation. The chromosome C

k

is selected as a parent when the randomly generated real number r from (0, 1) is less than r

m

at the kth selection, where k = 1, 2, …, pop _ size. Let

Repeat the above operation until all parents have mutation, then replace the parents with the feasible children.

After the selection, crossover and mutation steps, the new population is ready for its next evaluation. The GA will keep running until it reaches the maximum number of iterations we specified. The process of the entire algorithm is as follows (Please also see Fig. 1):

Flowchart of the GA in this research.

Data and calculation results

To illustrate the proposed approach for the uncertain portfolio selection with transaction costs and minimum transaction lots, we give a numerical example here. According to the experts’ estimations, the 30 risk assets’ quarterly return rates are normal uncertain variables, r i ∼ N (μ i , σ i ). The initial holding number of minimum transaction lots on risk assets, together with the prediction of the prices and the quarterly return rates of the 30 securities are given in Table 1.

The prices and returns of the 30 risk assets

The prices and returns of the 30 risk assets

According to the requirements of Chinese securities market, for each risk asset, the minimum transaction lots is 100 shares. That means the investor must hold multiples of 100 shares of each risk asset. The cost transaction rate of purchasing is 0.08%, and the cost transaction rate of selling is 0.1%. The risk preference coefficient of investors is 0.3, and the total investment capital is 1,000,000.

Then a practical experiment is implemented. Parameters are placed according to the complexity of the problem: pop _ size is 100, the number of cycles is 2000, r c is 0.7 and r m is 0.1. The calculation is conducted with Matlab R2013a on the Intel Core i3-3120M processor with 2.50 GHz RAM. Computation time of the example is 3.601 seconds. The result converged and stabled after 1300 cycles. The procedure of convergence is shown in Fig. 2.

The procedure of convergence.

We get the optimal combination of risk assets as follows

The maximum expected return rate is 4.09%, and the corresponding risk level is 1.97%. The maximum fitness value is 0.0226, the funds invested in the portfolio is 999966.1263.

To verify the robustness of GA, ten tests were taken. The results are shown in the following table. As we can see in Table 2, the optimal results verified little during ten repeated tests. So the algorithm is believed to be robust.

The optimal values the 10 experiment

Model (8) includes the risk preference coefficient λ, the transaction costs of purchasing a and the transaction costs of selling b. We analyze the impact of these factors on the portfolio through simulation.

Figure 3 shows the impact of the risk preference coefficient λ on the gain of investment portfolio, Fig. 4 shows the result of influence of the risk preference coefficient λ on the risk of investment portfolio, and Fig. 5 shows the impact of the λ on portfolio objectives.

Impact of λ on the benefit.

Impact of λ on the risk.

Impact of λ on the objective function.

It can be seen from Figs. 3–5 that when λ is zero; the investor prefers to fully accept the risk. Thus, the penalty term in corresponding objective function is not binding to investors. In this case, investors only focus on the pursuit of maximum benefit. The target is equal to investment income, and all funds are put into the third asset which has the largest income. As the risk preference coefficient λ increases, the penalty term in the objective function is beginning to take effect that it lead to the value of the objective function reduced. When λ is small, the influence of penalty term is not obvious, therefore portfolio earnings are not affected. When it comes to 0.2, the revenue becomes insufficient to cover the risk caused by penalty term in the objective function, and the investors have to change investment strategy and choose less risky assets investment. When this happens, because of the low income of less risk assets, the optimal of both earnings and portfolio objective function value will reduce. When λ reaches up to 1, investors will not accept the risk at all and they will not invest in any assets.

This section studies the influence exerted by a and b. The optimal values with different transaction rates are shown in Table 2. In this numerical example, there are

The optimal values with a and b

The optimal values with a and b

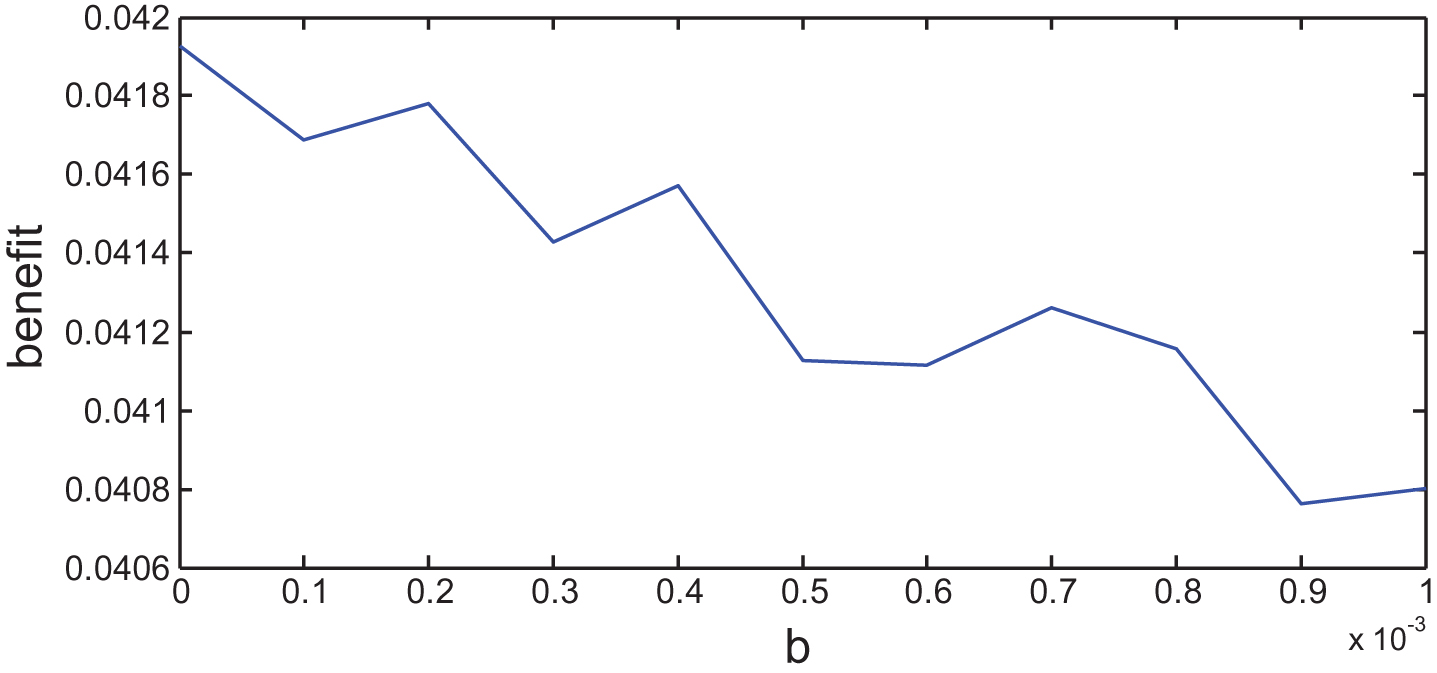

Figure 6 shows the impact of a on the optimal value of investment portfolio. Figure 7 shows the impact of b on the optimal value. The axis y indicates the optimal value. It can be inferred that the transaction costs lead to decrease of the objective and the larger the transaction costs, the lower the optimal fitness value would be.

Impact of transaction cost rate a on benefit.

Impact of transaction cost rate b on benefit.

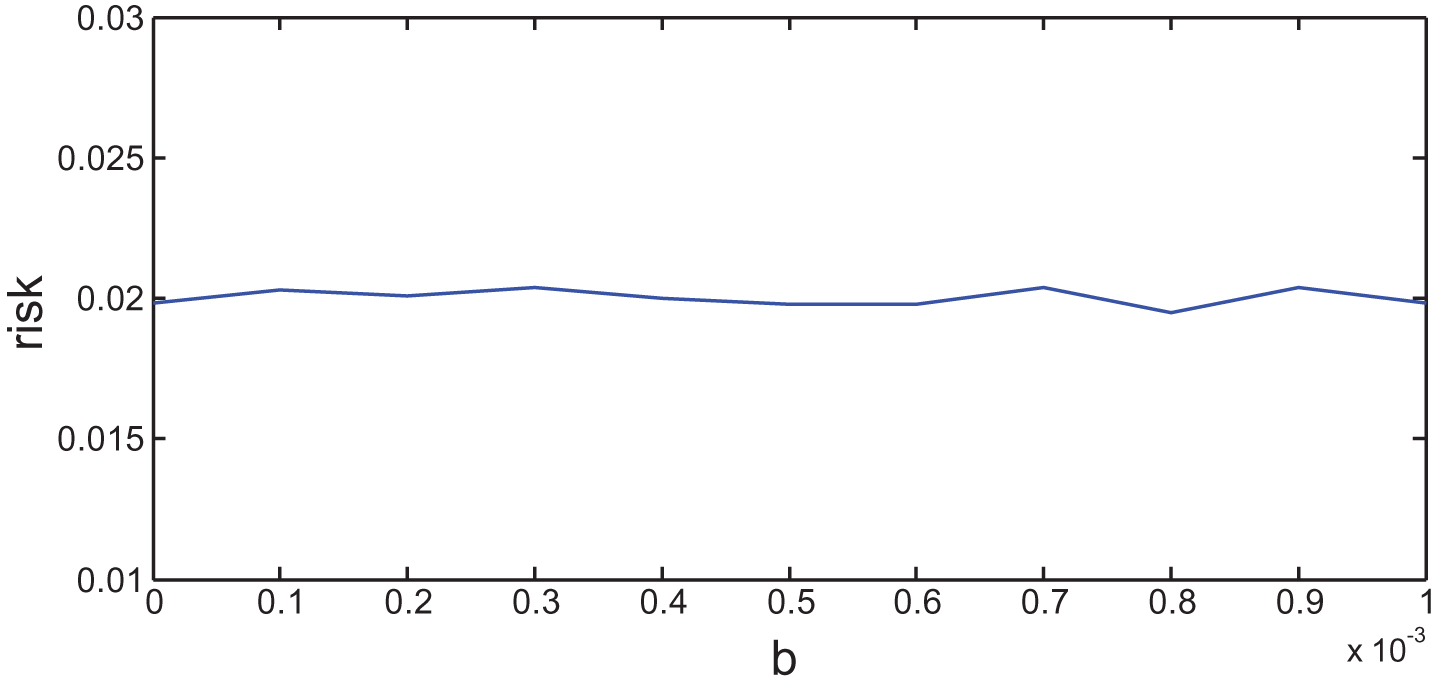

Figure 8 shows the impact of a on the risk of investment portfolio, and Fig. 9 shows the impact of b on risk. These graphs reveal that the effect of transaction costs rate of purchasing a and transaction costs rate of selling b mainly focus on the earning. The greater the transaction costs, the lower benefit of the portfolio. Meanwhile, these graphs reveal that both a or b have little effect on the risk. The transition costs have little influence over the investment risks.

Impact of transaction cost rate a on risk.

Impact of transaction cost rate b on risk.

The risk preference coefficient λ represents investors’ preference level for risk. As λ increases, the investors’ willingness of taking risk is dropping. Investors are reluctant to invest in risk assets. Generally speaking, the less risk assets the less earnings, therefore the optimal value of gains and portfolio objective function decrease with increase of the risk preference coefficient λ.

Transaction cost rate has an effect on the benefit of portfolio. And the larger the transaction rates, the lower the investment portfolio benefit. In contrast, the transaction cost rate of selling has greater effect on portfolio return than on the purchasing. Transaction cost rate has little impact on risks.

Conclusions

This paper has discussed the portfolio selection problem which considers transaction costs and minimum transaction lots requirement in the uncertain environment where security returns are given by experts’ estimations rather than historical data. Uncertain variables are used to describe the security returns. A new mean-variance model has been given. The impact of minimum transaction lots requirement and transaction costs on optimal portfolio has been discussed and a genetic algorithm for solving the optimization model has been provided. A numerical experiment has been given to illustrate the application of the proposed model and check the efficiency and robustness of the proposed algorithm. The computational results indicate that the proposed model is meaningful and able to be applied in reality.