It is well known that the arithmetic mean of two possibly different copulas forms a copula, again. More generally, we focus on the weighted power mean (WPM) of two arbitrary copulas which is not necessary a copula again, as different counterexamples reveal. However, various conditions regarding the mean function and the underlying copula are given which guarantee that a proper copula (so-called WPM copula) results. In this case, we also derive dependence properties of WPM copulas and give some brief application to financial return series.

For two given copulas and we consider the function

on , where and . Letting , Eq. (1) reduces to the weighted geometric mean of and ,

Assuming that is again a copula – which is not guaranteed at all – it is governed by – beside of the specific copula parameters of and – by two additional parameters and which may allow for more flexibility regarding dependence modelling. In this case, will be denoted as weighted power mean copula, or briefly WPM copula.

Certainly, there are single results on weighted arithmetic, geometric or harmonic means of two specific copulas (see, e.g. Nelsen, 2006; Fischer & Dörflinger, 2010). Nelsen even shows, that certain copula families are closed with respect to the operation in Eq. (1), i.e. belongs to the same copula family as and for a fixed . But a systematic proof that is a copula for all can only be found for the weighted power mean of the maximum- and independence copulas (see Fischer & Hinzmann, 2014).

On the other hand, we will provide counterexamples within this paper, where the weighted power mean of two copulas fails to satisfy the postulates of the copula definition. This motivates the derivation of certain criteria for and such that is again a copula. Therefore, our objective is to give solutions for broad classes of copulas and and possibly comprehensive domain of .

For this reason, the paper is organized as follows: First of all, we restrict ourselves to benign copulas and , where the copula densities exist and, consequently, the two-increasing condition is valid if is non-negative. Up to a few special cases (see, for instance, Fischer & Hinzmann, 2014), the direct proof of the two increasing-condition seems to be impossible without assuming the existence of the density. We then show that this sufficient (but not necessary) condition is satisfied for extrem value copulas and positive . Applying weighted power means with positive to max-id copulas will also result in proper copulas. As the max-id property of Archimedean copulas can be easily checked, we will provide results for various Archimedean copulas. It will also be shown that combining a copula with a specific positive dependence structure (i.e. left-tail decreasing property) with the independence copula gives again a copula. For , we are only able to derive single results for specific copulas. Afterwards, we investigate how the dependence structure of and transforms to the WPM-copula. For the positive quadrant ordering of Lehmann, 1966 and the stronger positive ordering of Colangelo, 2006, which is based on the concept of tail dependence (so-called LTD-ordering) it will be shown that the WPM-copula (with respect to these orderings) measures a strength/degree of positive ordering which lies between those of and . This implies that well-known dependence measures like Spearman’s and Kendall’s (which both satisfy these orderings) of WPM-copulas lie also in between those of and . However, only numerical approximation to these measures are available because no closed formula can be derived in general. After that, general formulas for the weak and strong tail dependence coefficients of WPM copulas are derived. Finally, we discuss the joint estimation of the WPM parameters and together with the copula parameters of and and apply the estimation formula to empirical data.

The following Table 1 summarizes the results of this contribution.

Let . A function is said to be -increasing if its -volume

for all and . If, additionally, and satisfies the boundary conditions

for arbitrary , is commonly termed as copula and we write , instead.

Putting a different way, let and denote two random variables with joint distribution and continuous marginal distribution functions and . According to Sklar’s Sklar, 1959 fundamental theorem, there exists a unique decomposition

of the joint distribution into its marginal distribution functions and the so-called copula

on which comprises the information about the underlying dependence structure. From Eq. (5) it becomes obvious that a copula is a bivariate distribution function of a pair of random variable defined on . Assuming that is differentiable with respect to both arguments, Eq. (3) is satisfied if

Moreover, it is known that

Later on, we will frequently use the independence copula which corresponds to bivariate distributions with independent marginals, the maximum copula , associated to random variables which are co-monotone and, thus, constituting an upper bound for all copulas and the minimum copula , associated to random variables which are counter-monotone and, thus, constituting a lower bound for all copulas. A copula which comprises minimum, maximum and independence copula is commonly called comprehensive.

For a general introduction to copulas we refer to Nelsen (2006) or Joe (1997). A recent overview on the multivariate case is provided by Fischer (2010) or Fischer and Köck (2012). Applications to finance are given, for instance, by Fischer et al. (2009).

Examples and counterexamples

In the literature there are numerous examples of copulas which are specific means of other copulas. Joe (1997), for instance, considers copula B11

which composes as weighted arithmetic mean of the maximum copula and of the independence copula. Similarly, copula B12 in Joe (1997)

results as the corresponding geometric mean of both copulas. Nelsen (2006) investigates whether the mean of two copulas with a specific building law is again a copula with the same building law. Consider, for example, the weighted arithmetic mean of two Farlie-Gumbel-Morgenstern copulas with the building law

which results again in a Farlie-Gumbel-Morgenstern copula:

A similar result is proven by Nelsen (2006, p. 107) for weighted geometric means and Gumbel-Barnett copulas which are defined by

Consequently, the geometric mean of and ,

is again a Gumbel-Barnett copula. Also the weighted harmonic mean can be successfully used to construct new copulas. Starting from Ali-Mikhail-Haq copulas (see Nelsen, 2006, p. 82) of the form

the weighted harmonic mean

is again a Ali-Mikhail-Haq copula. Fischer and Hinzmann (2014) turn away from concrete means and consider the broad class of so-called power means which are of the form

where . Included as special and limiting cases are the weighted arithmetic (, B11), the weighted geometric (, B12) and the weighted harmonic mean (). Fischer and Hinzmann (2014) proved that is again a copula for all . Due to the simple structure of both copulas, the authors succeed in verifying the -increasing-condition even without using the copula density.

In contrast, the question whether in general the weighted power mean of two copulas is again a copula has to be negotiated. Consider, for instance, the following simple counterexamples:

(Counterexamples).

1. Given the specific power mean of the minimum and the maximum copula, i.e

with and (harmonic mean). Plugging , , and into the formula above,

Hence, and the -increasing condition is no longer valid, i.e. is no copula.

2. Consider , where denotes the independence copula and the minimum copula. It can be checked that the -volume of is negative: , , , and hence

Sufficient conditions

Obviously, the boundary conditions of a copula are easily checked for the weighted power mean of two given copulas:

for . The crucial point is the proof of the -increasing condition. If we focus on copulas with existing densities, it suffices to show that the second mixed derivative of is non-negative. In the general case of WPM copula the mixed derivative of is given by

where ,

Whether , and are non-negative depends in particular on the sign and amount of . For it immediately follows that both , (according to Eq. (6)) and (due the existence of the copula density of , ) are non-negative. On the other hand, the sign of is non-positive for . However, using the equivalent representation

with

and where denotes the copula density of for , we derive the sufficient condition

that is a copula for all . In toto, we proved a very general result for :

.

For two copulas , with Eq. (9) the weighted power mean of and is again a copula for all .

Remark: The construction in Eq. (1) is actually a special type of ”pointwise composition of copulas” in Durante (2009). In particular, by using Theorem in Durante (2009) with , , , equal to the identity function, the prove of Theorem above can be done without any assumption on the densities of the copulas , .

.

Consider two Gumbel-Barnett copulas with different parameters . For ,

Hence, the expression in brackets in Eq. (10) are positive for and negative for . In both cases, the condition from above is satisfied.

Remark: In case of , and and hence are non-negative; the term may be also negative if the first expression (summand) is negative. For , and are non-positive and, consequently, not non-negative. The sign of is again undetermined, because . To sum up, for we obtain no general result for copulas , . Additional requirements have to be put on , to obtain a specific result.

Remark: Finally, let’s consider the special case of the weighted geometric mean which results for . For

we derive that

where

and

However, the sign of the expression is undetermined.

Results for specific copula classes

Extreme-value copulas

Consider now the first restriction that , are extreme-value copulas. In this case for and . For expression we obtain

such that holds and we can state the following theorem.

.

The weighted power mean of two arbitrary extreme-value copulas and is again a copula for .

(WPM-logistic).

Assume that and . Combining two possibly different logistic extreme-value copulas by means of a weighted power mean function, the resulting four-parameter copula has the form

with

Max-id copulas

Instead of restricting to extreme-value copulas, we extend our analysis to copulas which are maximal infinitely divisible (max-id). Originally, the max-id property for distribution functions is intensively discussed by Joe (1997). As copulas can be simply extended to distribution functions, we can apply the max-id property direct to copulas. A copula will be denoted as max-id, if satisfies the properties of a bivariate distribution function for all . Note that is not a copula for because the boundary conditions are no longer valid. Consider a bivariate copula with copula density . In order to be max-id it has to be shown that

Replacing by in Eq. (14) and after some re-arrangement we obtain

This expression is positive, if and satisfy condition Eq. (14), i.e. are both max-id. Obviously, this assertion also holds for , because and if are both max-id we obtain , notation as in Eq. (13). Hence, we derived the following result:

.

Assume that and are two max-id copulas and . Then is again a copula.

We conclude with two examples of max-id copulas.

.

The logarithm of the Galambos copula with parameter is given by

and hence

.

Taking the logarithm of the FGM-Copula with parameter ,

The corresponding derivatives are given by

which means that the max-id property depends only upon the sign of the parameter.

In particular, Archimedean copula with continuous, convex and strictly monotone decreasing generators – which guarantees that the inverse function exists – are max-id if and only if where

The following table summarizes Archimedean copulas for which the max-id property has already been verified (Nikoloulopoulos & Karlis, 2010) and own calculations), the names and equations are adopted from Nelsen (2006).

Selected Archimedean max-id copulas

Name

Copula function

Parameter

Clayton

AMH

Gumbel

Frank

Joe

()

()

()

()

()

Left tail decreasing property and independence copula

Both copulas B11 and B12 in Joe (1997) and the copula discussed in Fischer and Hinzmann (2014) result as a mixture of a copula with the independence copula . For the independence copula we easily conclude that and , respectively. Hence, condition Eq. (9) re-writes as

This condition is closely related to a property of positive dependence: Assume that and are random variables with copula as bivariate distribution function. given is called “left-tail decreasing” (briefly: LTD) if is non-increasing in . Exchanging the part of and , we say that given is “left-tail decreasing”. If LTD and LTD holds for the underlying copula , is briefly denoted as “left tail decreasing” (LTD-) copula. An equivalent condition for the LTD-property of a copula is

Hence, for a LTD-copula we state the following result:

.

The weighted power mean of a LTD-copula and the independence copula is again a copula for .

The following example illustrates the procedure for a specific Archimedian copula which is max-id for .

.

Consider the copula () in Nelsen (2006):

with partial derivatives

Consequently,

We are also able to derive the result of Fischer and Hinzmann (2014) as a special case because the maximum copula is a LTD-Copula.

.

For we have

Hence,

for . This explains why the weighted power mean of the maximum and the independence copula is always a copula (for the direct proof we refer to Fischer & Hinzmann (2014)).

Finally, we consider a copula which is not max-id.

.

The Gumbel-Barnett-Copula is of the form

I.e. it is a LTD-copula. Therefore,

which implies that the weighted power mean of the Gumbel-Barnett copula and the independence copula is a copula for all . Moreover,

and

For we have

Note, that for

such that the weighted power mean of the Gumbel-Barnett-copula and the independence copula is a copula for , too.

Complementary results for

The difficulty for of the proof that the power mean of two copulas is again a copula will again be illustrated by means of the Gumbel-Barnett copula, where we can prove the result only for a restricted range of the parameter set.

.

Again, we focus on a Gumbel-Barnett copula

The series representation of the exponential expression reads as

and contains completely positive addends if and . Subtracting from times the first addend of this series representation we obtain such that

This difference is positive if . That means in this special case where either the range of the dependence parameter is restricted or the range/domain of the weighting factor is restricted, the weighted power mean of a Gumbel-Barnett and the independence copula is again a copula for .

Properties of positive dependence and ordering

The LTD-property is only one form of positive dependence of random variables. For a detailed treatment of that topic we refer to Joe (1997) or Nelsen (2006). From these properties we can derive orderings of positive dependence. Probably the most famous one is the positive dependence ordering (briefly: PQD-ordering) of Lehmann (1966). In this context, a copula is said to be less positive dependent than a copula (in short: ) if for all Similarly, based on the LTD-property, we can introduce a LTD-ordering of positive dependence. According to Colangelo (2006), has less positive dependence than (in short: ) if is monotone decreasing in for all . For differentiable copulas it suffices to show that for all . It can be shown that LTD-ordering implies PQD-ordering.

Assume now that the positive dependence of is weaker than that of in the sense of one of that orderings. It raises the question whether the positive dependence of the corresponding WPM-copula is stronger than that of and weaker than that of . The answer turns out to be very simple for the PDQ-ordering due to the fact that every weighted power mean lies in between the minimum and the maximum of all values. Not so simple is the answer for the LTD-ordering as the next theorem shows.

.

For given copulas and with let denote the corresponding WPM-Copula with parameters and . Then holds

Proof: Note first that for every copula holds

After some simple re-formulations we obtain

with weight

Therefore, is a weighted arithmetic mean of and which implies that

It follows from the property of PQD-orderings that and, consequently,

and

Measures of dependence

Copula-based dependence measures are nothing else but specific mappings from the space of bivariate copulas to the interval . As an essential requirement to such a mapping we have to proclaim that it preserves elementary dependence orderings. In case of the LTD-ordering we have to make sure that

In this case, the domain of for the WPM-copula is determined by . The most prominent representatives of global dependence measures which only dependent from the underlying copula and preserve the LTD-ordering are Spearman’s rank correlation coefficient Kendall’s rank correlation coefficient and, recently introduced by Blest, .

Now assuming that is a WPM copula, we face the problem of solving integrals over non-linear functions in and for . Hence, a closed and analytic form cannot be expected (as a function of , and ). Solely for , it is well-known that Spearman’s is given by , Kendall’s is given by and Blest’s coefficient by General results for Spearman’s and Kendall’s have been derived by Fischer and Hinzmann (2014) only for the weighted power mean of the independence- and the maximum copula, basically using the linear structure of these copulas.

Tail dependence

In contrast to the linear correlation coefficient, Kendall’s or Spearman’s which measure dependence on an overall level, tail dependence coefficients (TDC) measure dependency only in extreme situations and rare events which correspond to the tail of a distribution, see e.g. Fischer and Dörflinger (2010).

Notions of tail dependence

Whereas the LTD-property deals with conditional properties of the form

for varying and , the lower strong tail dependence coefficient considers the asymptotic behavior of this conditional probability for and :

Similarly, the upper strong TDC is usually defined as

Provided their existence, these limits vary between and . If () the pair is commonly termed as upper (lower) strong tail independent.

In general, there are a lot of copulas (e.g. Gaussian copula, hyperbolic copula, FGM copula) which admit upper and/or lower tail independence but nevertheless allow a certain dependence between the variables and in the tail areas (see, e.g. Heffernan, 2000). A measure to quantify “dependence within tail independence” is suggested in Coles et al. (1999) who define the weak upper tail dependence coefficient as

provided the existence. It can be shown that , in case of upper tail dependence (i.e. for ), in case of being the independence copula and for copulas with upper tail independence (i.e. with ), increases with the strength of dependence in the tail area. In the sequel, we speak of weak upper tail independence if , and of weak upper tail dependence if . It should be again pointed out that it is not necessary to calculate in case of strong upper tail dependence, because then holds. Instead of analyzing the limit behaviour for , one usually considers the bivariate transformation and . The variables and have so-called uniform Fréchet marginals with

Applying a Taylor approximation for large , and . Ledford and Tawn (1996) showed that for uniform Fréchet marginal distributions and under weak conditions

holds, where is a slowly varying function in , i.e. with for each . Moreover, the coefficient quantifies a weak upper tail dependence coefficient because . Furthermore, it can be shown that in case of and and in case of . Moreover, using

the relation between the uniform Fréchet marginal distributions and the copula can be established. Thus one has to check if there is a function slowly varying in and a satisfying

Likewise, the weak lower tail dependence coefficient equals the limit of

for . For the (bivariate) Gaussian distribution, .

In the next step we show that the TDC of a WPM copula (provided its existence) is independent from the type of mean (i.e. ) and easily derived from the individual TDC’s of and .

Strong tail dependence

.

Assume that the strong upper (lower) tail dependence coefficients of and are given by () and (), respectively. If

is again a copula, the corresponding strong upper and lower TDC of are given by

Proof: At first, we focus on the upper case. It holds that

Applying the rule of de l’Hospital, the following representation holds:

Noting that for every copula ,

The result for strong lower TDC is straightforward.

Weak tail dependence

In contrast to the strong TDC, it will be shown that the weak TDC depends on (i.e. on the type of mean) to some extent. Moreover, only in case of geometric means (i.e. for ) we also come across to the dependence of .

.

Assume that and have weak lower TDC and . If is again a copula, the corresponding weak lower TDC of is given by

Proof: At first, assume that . Now,

and we obtain for the weighted power mean

with . Secondly, assume that . W.l.o.g. we assume that and

Hence, for large ,

such that

Consequently, and .

Finally, assume that and set . Then

Now the denominator can be treated similar to the positive case (but where and are exchanged): For large and small ,

Assume :

For we obtain

Finally, for we have

.

Assume that and have weak upper TDC and . If is again a copula, the corresponding weak upper TDC of is given by

Proof: First note that we have for the survival copula of

Assume at first that . In this case, for and therefore

for large . Consequently,

Assume . Then

with

Assume . Because of for large with we obtain

such that

with and .

Assume . Then, obviously and .

Secondly, assume that . Using the approximations for and for ,

To sum up, for all cases , and we obtain the same result for .

.

The weak TDC of the geometric mean of two (arbitrary) extreme value copulas and is given by

where denotes the dependence function of which underlies the extreme value copula , i.e. Additionally, , i.e. . Hence, the dependence function of is given by

and we obtain after some re-formulations

which corresponds to the formula from Theorem 7, above.

Exchange rates.

Application to exchange rate data

Data

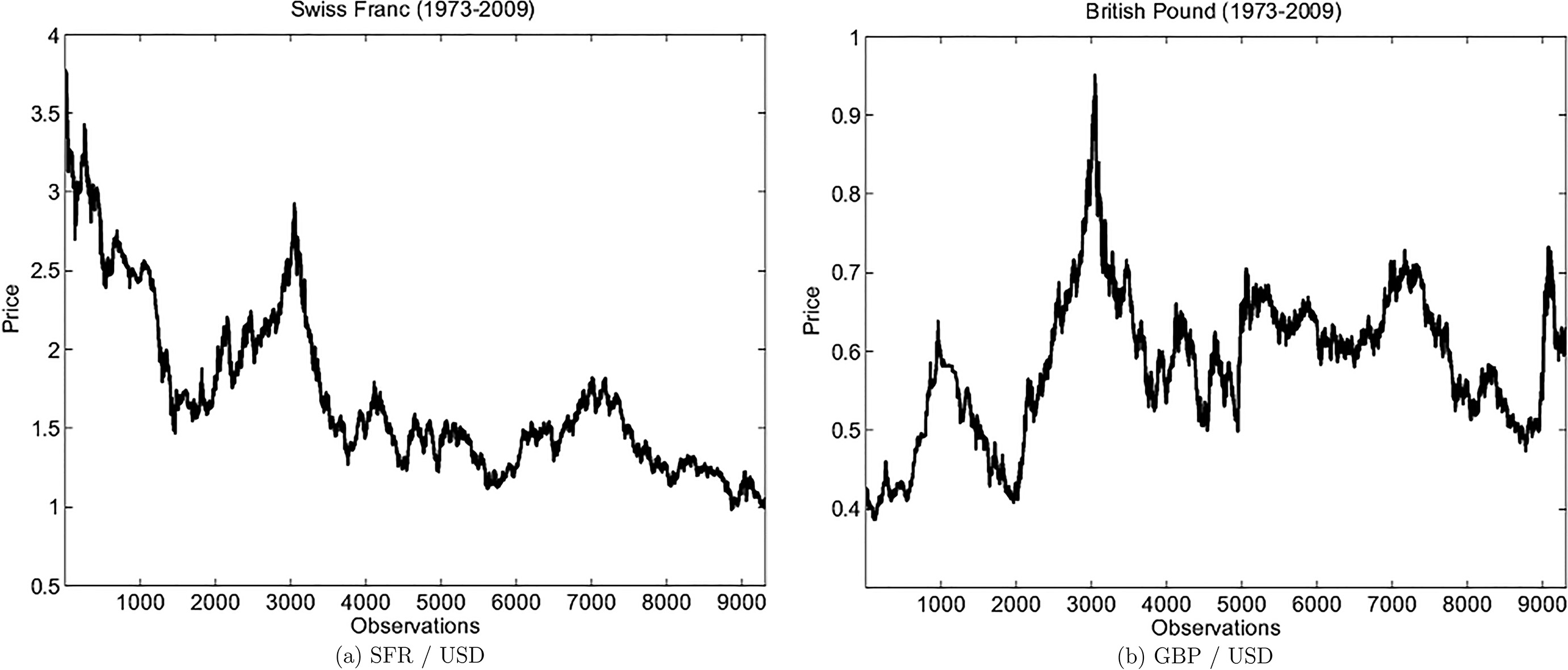

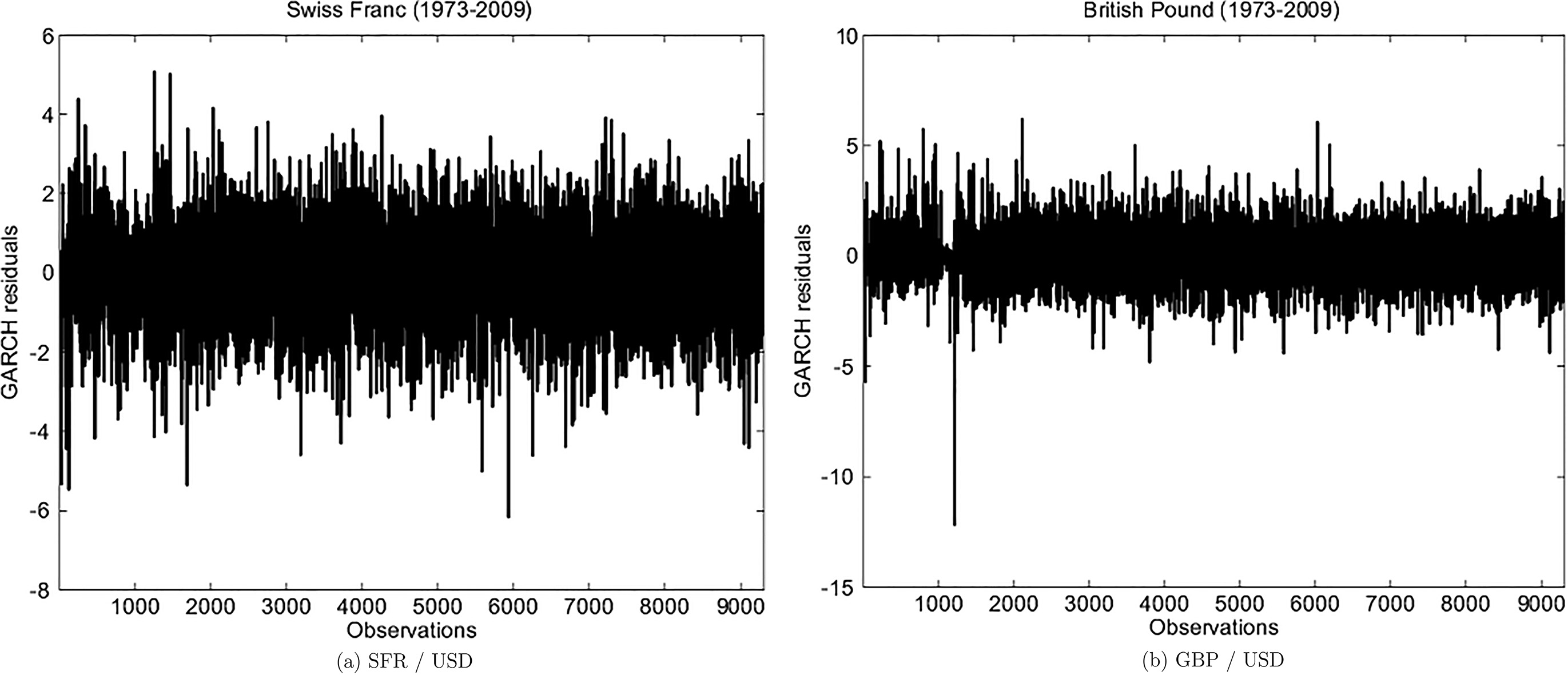

In order to illustrate the benefits of our new construction method, consider two data series from foreign exchange markets (FX-markets) which are available from the PACIFIC Exchange Rate Service (http://pacific.commerce.ubc.ca). In contrast to the volume notation, where values are expressed in units of the target currency per unit of the base currency, the so-called price notation is used within this study which corresponds to the numerical inverse of the volume notation. All values are expressed in units of the base currency per unit of the target currency. For reasons of brevity, we focus on the Swiss Franc/US-Dollar (SFR) and the British Pound/US-Dollar (GBP) henceforth, with daily observations from Feb 2, 1973 to Dec 31, 2009 (see Fig. 1). Instead of using exchange rates itself we consider log-returns (i.e. differences of log-prices), instead which are displayed in Fig. 2.

Log-returns.

A first insight into the structure of the return series may be gained through Table 3, below. It contains some basic descriptive and inductive statistics of the daily time series: the number of observations (), arithmetic means (Mean), standard deviations (Std), third and fourth standardized moments (). Moreover, tests on normality (i.e. Jarque-Bera test, ) and tests of GARCH effects (i.e. Ljung-Box test for the squared returns with lag and Engle’s LM test , where is the coefficient of determination of the regression ), complete the summary statistics (-values are cited for all statistical tests).

Descriptive statistics

Mean

Std

SFR

9307

0.014

0.712

0.055

6.257

0.000

0.000

0.000

GBP

9307

0.004

0.617

0.144

7.332

0.000

0.000

0.000

Caused by the strong evidence of GARCH effects, we apply a data filter, which means that we fitted GARCH models to the time series in a first and calculate GARCH residuals in a second step.

GARCH residuals.

Scatter plot.

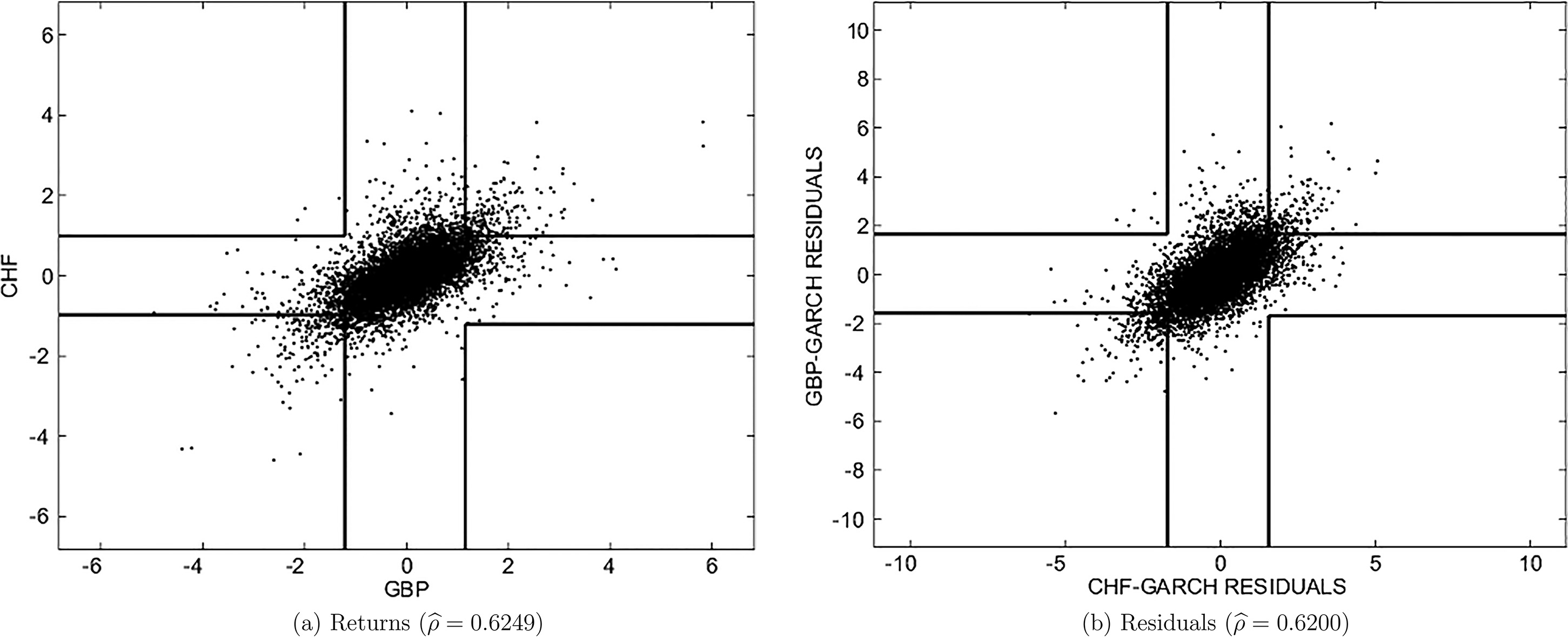

The scatter plot for both returns and GARCH residuals is dedicated to Fig. 4. As to be expected, empirical correlations are essentially equal around in both cases.

Estimation

Within this work we apply semi-parametric maximum likelihood (SML) estimation which is treated, for example, by Hu (2002) and Genest et al. (1995). Without any parametric assumptions for the margins, the univariate empirical cumulative distribution functions are plugged in the parametric log likelihood function, instead. In other words, after transforming the observed data pairs to uniform data pairs , the SML estimator of the copula parameter maximizes the log likelihood function:

Copulas

The copulas under consideration are chosen on the basis of Theorem 1. Exemplarily, the Clayton copula (denoted by ), its rotated counterpart () and the Gumbel copula () are selected, all of them being exchangeable. For reasons of brevity we introduce some abbreviations, in particular WPM denotes the weighted power mean of the two copulas and with parameter and (see also Table 4, above).

Copulas under consideration

Abbr.

Copula

Parameter

C1

Clayton

C2

Rotated Clayton

C3

Gumbel

C4

WPM(C1,C2;)

see

C5

WPM(C1,C3;)

see

Finally, Table 5 contains the estimation results from the SML estimation for both original returns and GARCH residuals. In addition to the classical log-likelihood-values () and the parameter estimators we also calculated Akaike’s criterion which takes the number of parameter into account. In both cases, the goodness-of-fit can be clearly improve for both WPM copulas under consideration. In addition, parameter estimators for GARCH residuals and return series are very similar. In both cases, WPM outperforms the GAUSS copula and is very close to the Student-t copula with degrees of freedom which were added as reference. We chose for the Student-t distribution because this is a typical value observed for financial return pairs. Above that, it is guaranteed that at least mean and variance exist. Finally, we observed no significant changes of the log likelihood value if is modified slightly. For data with more skewness one could imagine that C4 and C5 even may outperform the Student-t distribution.

Estimation results

Copula

AIC

Returns

GAUSS

t()

C1

C2

C3

WPM(C1,C2;)

WPM(C1,C3;)

GARCH residuals

GAUSS

t()

C1

C2

C3

WPM(C1,C2;)

WPM(C1,C3;)

Conclusion

In general, the weighted power mean of two arbitrary copulas is not necessary a copula again. We establish sufficient conditions which guarantee that this is true and give several examples of new copulas. Moreover, dependence measures for so-called weighted power mean (WPM) copulas are derived and calculated exemplarily for some copulas. Finally, application of WPM copulas to financial return data is given which highlight the flexibility of our new approach.

Footnotes

Acknowledgments

We thank an anonymous reviewer for the thorough review and highly appreciate the comments and suggestions, which significantly contributed to the quality of the publication.

References

1.

Colangelo,A. (2006). Some positive dependence orderings involving tail dependence. Working Paper University of Insubria.

2.

Coles,S.Heffernan,J., & Tawn,J. (1999). Dependence measures for extreme value analyses. Extremes, 2, 339-365.

3.

Durante,F. (2009). Construction of non-exchangeable bivariate distribution functions. Statistical Papers, 50, 383-391.

Fischer,M., & Dörflinger,M. (2010). A note on a non-parametric tail dependence estimator. Far East J. Theor. Stat., 32, 1-5.

6.

Fischer,M., & Hinzmann,G. (2014). A new class of copulas with tail dependence. South African Statist. J., 48, 229-236.

7.

Fischer,M., & Köck,C. (2012). Constructing and generalizing given multivariate copulas: A unifying approach. Statistics, 46, 1-12.

8.

Fischer,M.Köck,C.Schlüther,S., & Weigert,F. (2009). An empirical analysis of multivariate copula model. Quantitative Finance, 9, 839-854.

9.

Genest,C.Ghoudi,K., & Rivest,L.-P. (1995). A semiparametric estimation procedure of dependence parameters in multivariate families of distributions. Biometrika, 82, 543-552.

10.

Heffernan,J. (2000). A directory of coefficients of tail dependence. Extremes, 3, 279-290.

11.

Hu,L. (2002). Dependence Patterns across Financial Markets: Methods and Evidence. Working Paper, Ohio State University.