Abstract

Although early-stage finance is critical to the growth of most ventures, it is even more important for social ventures as they face the challenges of balancing their social and commercial objectives. Drawing on institutional logics and signaling theory, this study uses a panel data set of 3,401 nascent social ventures to investigate the important role philanthropic grant funding plays in the organizational and financial development of social ventures. We find mixed results, with positive effects on employment and subsequent access to debt finance, but no effects on revenues and access to equity. Our findings connect these theories by suggesting philanthropic grants provide social ventures with flexibility to invest in human capital without pushing them to pursue short-term financial objectives, and that receiving a philanthropic grant provides a signal that is interpreted differently by debt and equity financiers. These findings are especially relevant as funders increasingly use grants to support social entrepreneurship.

Many early-stage ventures struggle to access financing due to liabilities of newness and smallness (Zimmerman & Zeitz, 2002), and information asymmetry (Plummer et al., 2016; Wiklund et al., 2010). 1 Much more than their commercial venture counterparts, the limited access to early-stage finance represents a business challenge for social entrepreneurs, with many investors wary of investing in ventures with dual objectives (Bridgstock et al., 2010; Scarlata et al., 2016), or having unrealistic financial return expectations (Dichter et al., 2013; Koh et al., 2012). Like their commercially oriented counterparts, ventures with a prosociality focus (Branzei et al., 2018; Shepherd, 2015), or what we call social ventures in this study, need a constant infusion of capital to scale their social and financial impact (Bildner, 2017), which is a key reason why financial sustainability is cited as the critical link between growth and maximizing social impact (Dees, 2008; Scarlata & Alemany, 2010; Smith & Besharov, 2019). These challenges are even more pronounced for ventures that specifically target markets at the base of the pyramid, where the road to profitability is often long and tenuous (Koh et al., 2012; Kolk et al., 2014; Renko, 2013). The global COVID-19 pandemic is revealing the interdependence of business and society, and the pressing need to tackle global social challenges more clearly than before (Bapuji et al., 2020). With capital sources likely to dry up in the wake of the pandemic, social ventures will face even greater challenges in accessing the right mix of flexible finance they need to grow (Global Impact Investing Network [GIIN], 2020; Winkler, 2020). Philanthropic funding is likely to play a critical role in tackling the public health challenge and recovery (Murray, 2020), making this study both timely and relevant.

In this study, we ask whether philanthropic grants can help social ventures grow, either by improving their own financial performance, or by signaling legitimacy to other stakeholders that provide commercial capital in the form of debt or equity. We build on the emerging entrepreneurship literature that focuses on purpose-driven entrepreneurship and take a holistic perspective on social entrepreneurial development (Doherty et al., 2014; Nason et al., 2018; Saebi et al., 2019; Short et al., 2009; Thompson et al., 2018) by examining interactions between different analytical levels (Saebi et al., 2019). To be more effective in tackling the most daunting social and environmental challenges (Kolk et al., 2014; Thorgren & Omorede, 2018), we recognize that social entrepreneurs will need support from a wide range of funding sources, with special priority at early stages (Branzei et al., 2018; Easterly & Miesing, 2009; Weidner et al., 2016). In doing so, we answer the calls for greater scholarly attention to funding for prosocial organizations (Daggers & Nicholls, 2016; Wry & Haugh, 2018), which is considered to lag practice (Daggers & Nicholls, 2016). We contribute to the emerging literature on the capital mix for hybrid ventures and mechanisms of social venture financing (Cobb et al., 2016) such as crowdfunding and peer-to-peer innovations (Calic & Mosakowski, 2016; Lehner, 2013), governments and foundations (Bosma et al., 2016), venture philanthropy and philanthropic venture capital (Gordon, 2014; Ingstad et al., 2014; Mair & Hehenberger, 2014; Scarlata & Alemany, 2010; Scarlata et al., 2016), developmental venture capital (Rubin, 2009), impact accelerators (Lall et al., 2020), and impact investing (Höchstädter & Scheck, 2015).

The use of grant funding has received increasing attention in entrepreneurship more generally (Lall et al., 2019; McKenzie, 2017), as well as social entrepreneurship more specifically (Dees, 2008; Smith & Besharov, 2019). Governments, aid agencies, and donors have long provided grants and subsidized technical assistance for research and development (R&D) in emerging industries (Fleming et al., 2019; Howell, 2017; Islam et al., 2018), to marginalized entrepreneurs in the United States (Carpenter & Loveridge, 2018; Mauldin, 2012), to microfinance institutions in developing countries (Dees, 2008; Dugan & Goodwin-Groen, 2005), and to social enterprises (Bosma et al., 2016; Smith & Besharov, 2019). Grants are the most common financial instrument used by donor agencies, to help accelerate market development in nascent social ventures (Rogerson et al., 2014), and provide the type of flexibility that other forms of capital often cannot (Smith & Besharov, 2019). The Global Entrepreneurship Monitor (GEM) estimates that between one quarter and more than half of all social ventures (depending on the region) receive grant financing (Bosma et al., 2016). Unlike other forms of finance such as debt or equity, grant financing is typically provided as a gift and does not require repayment or giving up a share of the firm. Grant finance ostensibly helps nascent ventures improve organizational performance by allowing them to enhance innovation, invest in hiring, and move closer to financial sustainability (Dees, 2008; McKenzie, 2017; Smith & Besharov, 2019), which is regarded as an important milestone for social ventures in and of itself (Hehenberger et al., 2019; Koh et al., 2012; Wry & Haugh, 2018). Receiving substantial funding may also enhance the reputation of nascent ventures and serve as a signal of credibility to other prospective funders (Ahlers et al., 2015; Balboa & Marti, 2007; Howell, 2017; Islam et al., 2018). Finally, unlike other forms of capital such as debt and equity, which may be motivated by financial considerations, grant financing can help the venture expand its social mission and serve as guardrails to ensure its preservation (Smith & Besharov, 2019).

As a theoretical frame, we use institutional logic theory to explain how social ventures operate in a space of organizational hybridity, where the acquisition of finance from both commercial and philanthropic sources provides important flexibility and legitimation benefits (Chertok et al., 2008). Although most private financial providers are driven primarily by commercial institutional logic (e.g., traditional venture capital, banks), others such as philanthropic foundations, governments, and donor agencies are closer to the social-welfare or values-led end of the spectrum (Nicholls, 2010), and primarily concerned about social impact (Smith & Besharov, 2019). We also use signaling theory (Alsos & Ljunggren, 2017; Connelly et al., 2011) to help explain how philanthropic grants can be used by social ventures to communicate signals of “quality” to other key stakeholders (Howell, 2017; Islam et al., 2018), which can then improve the likelihood of acquiring external investment capital by reducing inherent informational asymmetries in the social venture–investor relationship (Yang et al., 2020).

We contribute theoretically to the social entrepreneurship literature by connecting institutional logic theory and signaling theory to better understand what role philanthropic grant financing plays in strengthening what Smith and Besharov (2019, p. 1) refer to as “structured flexibility” of social ventures and more broadly, advance research on the underexamined role philanthropic grant financing might play in “scaffolding” organizational approaches to tackle multidimensional, complex, and interlinked societal challenges (Mair et al., 2016). We test our hypotheses using a rich longitudinal data set of 3,401 early-stage social ventures that applied to 77 social accelerator programs (Roberts & Lall, 2019) from around the world. Our findings offer mixed evidence of the impact of philanthropic grant finance on social venture performance, with positive effects on employment and on ventures’ subsequent ability to access debt finance, but not on revenues or acquiring equity. Our study contributes to the broader literature on social finance and social entrepreneurship by providing a more nuanced picture of how different commercially oriented stakeholders perceive the signal of receiving grant funding, with important implications for social entrepreneurs seeking support from different sources. The positive effects on access to debt finance suggest that investors that are simply seeking fixed returns on their investment are likely to view grants as a positive signal, whereas those that expect outsize returns (equity investors) do not hold that view. Thus, our null results on equity investment support the assertion of Hehenberger and colleagues (2019) that philanthropy may be devalued in some parts of the social finance space. By embarking on a large-scale quantitative study (one of the first that we are aware of) on the topic, we contribute to the literature on the capital mix for hybrid ventures (Cobb et al., 2016) and connect institutional logics to signaling theory in the context of social entrepreneurship finance.

Literature Review

Philanthropic Grants and the Social Finance Spectrum

Although philanthropic funders have at times been depicted as interested only in the social performance of the ventures they support, there is an emerging strand of literature that argues otherwise. Recent scholarship (Salamon, 2014; Scarlata & Alemany, 2010; Smith & Besharov, 2019) suggests that philanthropic finance support of social ventures can enable the pursuit of commercial objectives to ensure greater and more effective scaling opportunities, while helping to preserve their social mission. Philanthropic grant, even when offered by financiers that straddle dual institutional logics, is capital that is provided with no expectation of financial return.

Although strategic philanthropy by firms to nonprofit organizations in the context of corporate social responsibility has been widely studied (Barnett, 2007; Liket & Maas, 2016; Saiia et al., 2003; Shumate et al., 2018; Yin, 2017), the role of philanthropic grants for social entrepreneurship is comparatively underresearched and undertheorized. Teasdale (2010) and Chertok et al. (2008) suggest that social ventures draw on different aspects of their dual identity to attract different sources of commercial and philanthropic capital. We have some empirical (both qualitative and quantitative) evidence of this duality. According to the GEM special report on social entrepreneurship covering 58 countries (Bosma et al., 2016), philanthropic funding sources such as government programs, donations, and grants represent the second largest source of social entrepreneurship finance after the social entrepreneurs themselves, underscoring the importance of these socially oriented stakeholders at a global level. Using data from the GEM, Sahasranamam and Nandakumar (2018) observe that the presence of more philanthropy-oriented finance is an important factor in supporting financial capital investment toward social entrepreneurship entry.

As Dees (2008) notes, Philanthropists and social entrepreneurs are in a position to pursue business opportunities that do not appear to have a high profit potential but that constructively engage the poor, because profits are not their primary consideration and measure of success. They can take the risks, subsidize higher cost structures, and be more patient than profit-seeking investors and entrepreneurs. (p. 125)

Receiving philanthropic capital can help these nascent social ventures attract larger pools of capital from commercial and social investors and reach higher level of economic as well as environmental and social sustainability (Desjardins et al., 2014; Scarlata & Alemany, 2010; Scarlata et al., 2016). Finally, as Smith and Besharov (2019) argue, external stakeholder relationships can act as “guardrails” (p. 13) for each mission, moderating the hybrid organization’s path between the extremes of either institutional logic. As they describe in the case of Digital Divide Data, philanthropic grants gave the venture the flexibility to prioritize its social mission, while continuing to earn sufficient revenues and attract other forms of finance. Social ventures are especially at risk of suffering mission drift (Ebrahim et al., 2014), so the combination of socially motivated philanthropic grants and commercially oriented debt and equity can help social ventures attain financial sustainability and maximize their social impact (Smith & Besharov, 2019). It is no surprise, then, that international development agencies (e.g., the Global Innovation Fund, the International Finance Corporation, United States Agency for International Development [USAID]), foundations (e.g., Omidyar Network, the Case Foundation), and other funders have developed extensive programs to support social entrepreneurship through philanthropic grants that promote the pursuit of financial performance (Gordon, 2014; Rogerson et al., 2014; Shaw et al., 2013).

Philanthropic grants are one of the range of financial instruments used in the emerging field of social finance, which have grown in parallel to and are intrinsically interlinked with social entrepreneurship (Miller et al., 2010; Nicholls & Pharaoh, 2008; Ormiston & Seymour, 2014). Although there is rapidly emerging scholarship on a wide range of social finance issues in management and development literature (Hehenberger et al., 2019, for impact investing; Cobb et al., 2016 for microfinance; Mollick & Robb, 2016, for the role of crowdfunding in democratizing innovation; and Lall et al., 2020, for impact accelerators), there has been comparatively less scholarly attention paid to the relationship between social finance and social entrepreneurship (Daggers & Nicholls, 2016; Lall, 2017). Much of the academic literature in social entrepreneurship focuses on the entrepreneur and the organization (Saebi et al., 2019), without examining how different stakeholders (with heterogeneous motives) influence their actions (Bridoux & Stoelhorst, 2014; Nason et al., 2018). Although some scholars have examined the direct influence of external resource providers such as philanthropic and other social finance organizations on social entrepreneurs (Nicholls, 2010; Roberts & Lall, 2019; Spiess-Knafl & Aschari-Lincoln, 2015; Zhao & Lounsbury, 2016), rigorous quantitative research on the topic remains limited, especially when we consider the spectrum of social finance options described by Nicholls (2010).

Some of the gap in academic scholarship on social finance and social entrepreneurial finance issues has been filled in recent years by practitioner groups and consulting firms, including the Impact Management Project, the GIIN, the Aspen Network of Development Entrepreneurs, the Monitor Group, and Acumen Fund. For instance, in a widely cited report by Acumen and the Monitor Group (now part of the Foundation Strategy Group), Koh and colleagues (2012) describe the importance of philanthropic grants to fill the “pioneer gap” (p. 10) in social entrepreneurship—helping nascent social ventures in a new field attain self-sufficiency and become investment-worthy. Similarly, several of the GIIN’s examples of “catalytic first-loss capital” illustrate the use of philanthropic grants as a way to address the systemic underinvestment in early-stage social entrepreneurs and harder-to-fund social dilemmas (e.g., homelessness; GIIN, 2013). 2 Whether one labels the financial instrument as catalytic finance, innovative development funds, or technical assistance, many social finance practitioners believe some type of philanthropic grants are necessary to drive these hybrid ventures to financial sustainability and to legitimize them to other key stakeholders (Desjardins et al., 2014; Koh et al., 2012; Rogerson et al., 2014).

Dual Institutional Logics of Social Ventures and Social Finance

The concept of dual institutional logics (social and commercial) is the most widely used theoretical framework for studying social entrepreneurship, reflecting the inherent tensions and instability of the construct (Battilana & Dorado, 2010; Ebrahim et al., 2014; Pache & Santos, 2013; Zhao & Lounsbury, 2016) in management literature. Most important, social ventures do not exist in a vacuum, and the institutional logics that influence their behavior may be internal as well as external (Besharov & Smith, 2014; Lee & Battilana, 2013; Nicholls, 2010; Ometto et al., 2018; Zhao & Lounsbury, 2016). As noted by Greenwood and colleagues (2011), “organizations face institutional complexity whenever they confront inherent incompatible prescriptions from multiple institutional logics” (p. 317).

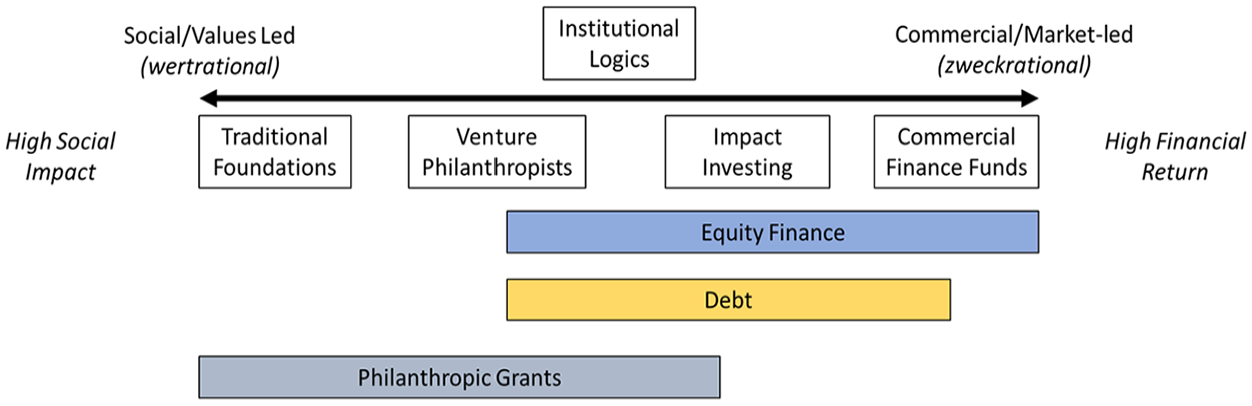

To address such institutional complexity, scholars and practitioners generally agree that the dual institutional logics of social ventures might be easier to understand if social finance providers were to be viewed as a spectrum based on their emphasis on expected social and/or financial returns. Conceptually, philanthropists and other grant providers tend to focus primarily on social impact, with no regard to financial returns, although at the other end of the spectrum, commercial rate investors may invest in social ventures only if they expect a market-rate return (Nicholls, 2010; Nicholls & Pharaoh, 2008). Nicholls (2010) describes the two dominant institutional logics among social entrepreneurship investors: a mainstream market-based logic (zweckrational) and a values-led logic (wertrational), which place equity and debt closer to the commercial end of the spectrum and philanthropic grants closer to the values-led or “social” end.

Nicholls (2010) observes that financial instruments such as bank loans and venture capital are both embedded in the market-based logic and primarily motivated by financial objectives. Social venture capital funds, impact investors, and community lending institutions that employ debt or equity typically expect some financial returns but are primarily motivated by social objectives (Miller et al., 2010; Rubin, 2009). Within the social finance spectrum, these types of funders have typically been studied the most, particularly with respect to their motivations (Miller et al., 2010), their investment approaches (Mair & Hehenberger, 2014; Rubin, 2009; Spiess-Knafl & Aschari-Lincoln, 2015), and their financial performance (Gray et al., 2015). Further along the social finance spectrum lies the “venture philanthropy” model (Letts et al., 1997; Mair & Hehenberger, 2014), which is an even more socially motivated, patient and risk-tolerant source of capital for social entrepreneurs (Gordon, 2014; Nicholls, 2010). Although there are several types of funding mechanisms available to social entrepreneurs (e.g., philanthropy, business plan competitions, government sources, donor agencies), a key characteristic of philanthropic finance providers (as compared with traditional and commercial-oriented impact investors) is that they are even more rooted in the social welfare logic, because they primarily seek a social impact outcome, and no direct financial return. Finally, some hybrid social finance providers use multiple financial instruments, depending on the specific investment. 3 Figure 1 accordingly updates the spectrum from Nicholls (2010) and Balbo and colleagues (2016) to reflect the dualism of social finance practice, and the distribution of financial instruments employed by different actors, ranging from traditional foundations to commercial finance funds.

The social finance spectrum.

Nascent social ventures, such as their commercial counterparts at similar stages, are likely to be capital constrained, resulting in an underinvestment in human resources and reduced revenue growth (Davidsson & Honig, 2003; McKenzie, 2017). Therefore, we expect philanthropic grants to help social ventures scale their business impacts by giving them the necessary organizational and financial resources to invest in hiring additional workers and to expand their core business. As Harvey and colleagues (2011), Shaw and colleagues (2013), and Balbo and colleagues (2016) observe, grants are tied to performance outcomes, and philanthropic funders often make future grants contingent on achieving certain social and commercial milestones. Hehenberger and colleagues (2019) describe the evolution of dominant ideologies in impact investing over time, highlighting the prioritization of the commercial logic over the social logic. In a rich descriptive study, they find that early in the field’s development, social finance providers began devaluing certain aspects of traditional philanthropy such as the close dependent relationships between donors and grantees, leading to an emphasis on financial self-sufficiency. This devaluing meant that grants came to be viewed as a subservient form of social finance to be employed primarily in the pursuit of commercial performance (Hehenberger et al., 2019). Thus, drawing on Smith and Besharov’s (2019) conceptualization of “guardrails,” we suggest that philanthropic grant financing (typically from stakeholders rooted in the social logic) can help protect the organization’s social objectives against mission drift, while encouraging the pursuit of financial performance. 4

Examples of this perspective abound in practice: USAID’s (2016) Development Innovation Ventures provides a structured, multistage grant program for social entrepreneurs in various social and sustainable sectors. Similarly, foundations such as the U.S-based Draper Richard Kaplan Foundation, whose core mission is to support high-impact social ventures, provide extensive guidance to help their portfolio ventures reach their full growth potential. Consequently, even though these funders are enacting a social welfare logic, the outcomes they seek to stimulate are both social and commercial in nature. Grants are structured in multiple stages, requiring social ventures to meet certain organizational performance milestones (both social and financial) before receiving additional rounds of funding (Gordon, 2014; Scarlata et al., 2016; Shaw et al., 2013; Smith & Besharov, 2019). Consequently, we propose the following hypotheses:

Philanthropic Grants as Signals to Prospective Investors

Even for traditional entrepreneurs in the United States (where the financial ecosystem is much stronger for entrepreneurs) and countries around the world, it should be noted that the lack of access to capital is often cited as the one of the greatest barriers to entrepreneurship. For instance, although bank lending, venture capital, and other forms of private institutional capital dominate the investment landscape and receive the greatest attention in both the scholarly and practitioner research, 81% of traditional entrepreneurs in the United States do not receive bank loans or venture capital (Hwan et al., 2019).

In the absence of credible information on the prospects of future performance, many investors rely on what might be best referred to as “signals” of venture quality and legitimacy, especially the actions of third-party institutions such as other financiers (Balboa & Marti, 2007; Ebbers & Wijnberg, 2012; Gompers, 1996; Islam et al., 2018). We believe that signaling theory (Connelly et al., 2011; Spence, 2002) offers some guidance on this interplay between social ventures and investors. Within the entrepreneurship literature, signaling theory has been used to argue that capital providers assess the underlying quality of ventures by looking for signals that suggest the viability and promise of the venture (Ebbers & Wijnberg, 2012; Eddleston et al., 2016; Gimmon & Levie, 2010; Islam et al., 2018). These signals help potential investors overcome inherent informational asymmetries in the venture–investor relationship. As Spence (2002) argues, acquiring information to resolve an informational asymmetry may be costly and unreliable because these signals may not be readily available. In addition, the signal must be receivable and interpretable by the potential investor in the manner it was intended (Connelly et al., 2011). As a result, entrepreneurs who can provide credible signals of quality can help overcome these barriers and improve their likelihood of acquiring external capital.

One key signaling mechanism is the endorsement of external actors such as investors (e.g., venture capital, angel investment, accelerators, debt, and crowdfunding; Ahlers et al., 2015; Ebbers & Wijnberg, 2012; Hallen & Eisenhardt, 2012; Plummer et al., 2016; Robson et al., 2013). Ebbers and Wijnberg (2012) note that in fields with higher levels of uncertainty about quality (e.g., art auctions), the signals of credibility from experts are greatly valued. Hallen and Eisenhardt (2012) show how startups tend to focus their interactions with investors when they are best able to signal an important milestone that is validated by a reputable third party.

Islam et al. (2018) find that receiving government grants can act as valuable signals of quality for startups in their study of the clean energy sector in the United States. Research grants from the public sector are not new, and governments have long supported startups in emergent industries such as semiconductors, telecommunications, the internet, and clean energy (Fabrizio et al., 2007; Fleming et al., 2019; Howell, 2017). Islam and colleagues (2018) suggest that receiving a grant introduces some form of credible third-party validation, which would arguably prevent low-quality startups from falsely acquiring that stamp of approval. They find that clean energy startups that received U.S. government research awards were 12% more likely to subsequently receive venture capital funding, and that receiving a grant acted as a substitute for intellectual property in the investor assessments. Similarly, venture capitalists in the United States have valued grants from public agencies as a signal of quality in environmental startups (Howell, 2017).

Multiple practitioners (and some scholars) have argued that one of the primary objectives of many philanthropic grant funders in social entrepreneurship is to make these ventures more viable and attractive to commercial investors, while serving as guardrails for the social mission (Dees, 2008; Koh et al., 2012; Scarlata et al., 2015; Smith & Besharov, 2019). For example, in the case of the energy access social venture Husk Power, the Shell Foundation not only provided grants but also introduced the social venture to potential investors, and served as a reference, providing a strong signal of potential quality (Desjardins et al., 2014). Carlson and Koch (2018) provide similar examples in their descriptions of successful social ventures such as Grameen Shakti (energy access), Sankara Eye Care (health care), and Ziqitza Health Care (health care). They find a consistent pattern of social ventures receiving philanthropic funding at early stages, followed by more commercial sources such as equity and debt. For example, the social enterprise Ziqitza Health Care Limited, which provides affordable ambulance services across social venture cities in India received an initial grant of US$270,000 from the Ambulance Access for All Foundation in 2005, followed by infusions of debt (US$5.94 million in 2006) and equity (US$1.5 million over 2006 and 2007) from investors such as Acumen. The reputational gains from receiving prestigious and substantial grants can help social ventures obtain commercial capital, leading us to propose the following hypotheses:

Method

Sample

Our study tests these hypotheses using a new data set of 3,401 nascent social ventures from 77 different social accelerator programs 5 around the world. The data set was aggregated by the Entrepreneurship Database Program (EDP) at Emory University, as part of the Global Accelerator Learning Initiative (GALI), between January 2013 and December 2016 6 . Participating acceleration programs implemented an online survey as part of their application process, and applications from more than 8,000 ventures that agreed to have their data shared with researchers were anonymized and aggregated. Follow-up surveys were conducted approximately 1 year after the programs started and include data on key financial performance variables such as revenues, external debt and equity raised, and job creation. This follow-up survey was sent to all the ventures that applied to these accelerator programs, not only the ones that were selected for participation, with an overall response rate of 51%.

We limited the sample to those that broadly fit the definition of social ventures by excluding those that did not report a specific social or environmental objective. 7 In addition, although we recognize the role of nonprofit social ventures, our analysis focuses on only those ventures that were not registered as nonprofits because we are interested in their ability to acquire equity and debt finance as well as philanthropic grants. After discarding ventures that did not provide complete data on our key variables of interest, as well as some observations with invalid data (e.g., entering 55,000 for founding year), our final sample is comprised of 3,401 social ventures from 77 different programs. These ventures were from 15 different sectors, with the majority focused on agriculture (17.5%), education (13%), and health (12.3%), and smaller numbers in financial services (8.9%), information and communications technology (ICT; 7%), and energy (7%). A substantial minority (15%) of ventures reported being in the “Other” category, suggesting a fairly heterogeneous sample overall. The ventures operated in 124 different countries, with the largest groups coming from the United States (857), Kenya (366), Mexico (301), India (246), Uganda (186), and Nigeria (170). Given the heterogeneity of the sample, we use the country groupings based on per-capita income levels developed by the World Bank (explained in the following section) to control for differences in levels of economic and institutional development in our analysis. 8

This data set overcomes several challenges that are typically associated with collecting information on nascent social ventures, as described by Bloom and Clark (2011). The lack of a consistent legal definition of social entrepreneurship makes it difficult to develop a representative sample (particularly across countries), and researchers tend to rely on curated lists of “successful” social ventures developed by one third-part intermediary (Grimes et al., 2018), or on larger representative samples of entrepreneurial perceptions, but without corresponding venture-level performance indicators (Bosma et al., 2016; Lepoutre et al., 2013). Although these approaches have their benefits, they tend to lack critical entrepreneur and venture-level information on nascent social ventures, and the ability to examine performance over time.

This data set includes observations from all the social entrepreneurs that applied to these programs, not only the ones that were accepted, giving us a considerably more inclusive sample than several previous studies. In addition, because these applications are drawn from 77 different social accelerator programs, they also represent a more diverse group of social ventures than if they were from a single intermediary. However, we emphasize that this study does not specifically examine social accelerators (Lall et al., 2020; Pandey et al., 2017; Roberts & Lall, 2019; Yang et al., 2020). Rather, we use rich application data from these social accelerators to examine the effects of philanthropic grant finance on social venture performance. 9

Measures

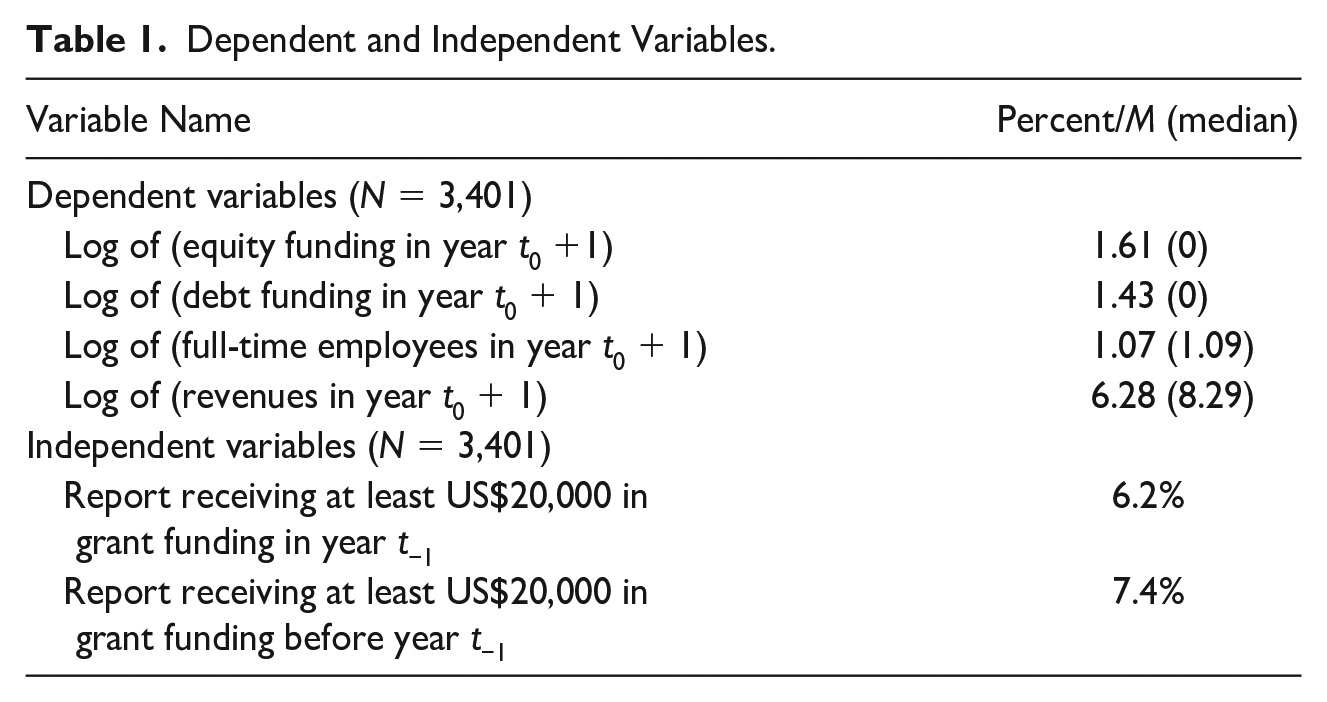

The social ventures in our sample represent a wide range of sectors and countries of operation. Therefore, we suggest that a single measure of venture performance such as revenues or job creation may not be sufficient to capture the varying performance objectives of these ventures within the time frame of this study. For example, it is likely that a social venture in the sustainable agriculture sector may take longer to generate positive revenues compared with a venture in the ICT sector but may generate greater employment for agricultural workers. Equity funding from venture capital providers may be more easily available for clean energy startups compared with those working in education. We therefore use four common measures of commercial performance as our dependent variables in this study, that have also been used in past research on social and commercial entrepreneurship (Islam et al., 2018; Kolk et al., 2014; McKenzie, 2017): financial revenues (US$), amount of equity funding raised (US$), amount of debt funding raised (US$), and the number of full-time employees, as reported in the follow-up year t0. 10

Consistent with the approach adopted by Fafchamps and Owens (2009) and Suárez and Gugerty (2016), we add 1 to the values, and use the logged form of these variables to reduce the effects of outliers, and to also avoid losing observations with reported zero values. In addition, following Roberts and Lall (2019), we calculate the year-over-year changes in the levels of these four variables, which provide us with the difference in the amount of equity, debt, revenues, or job creation in the follow-up year, compared with the baseline year. For each of our four dependent variables, we calculate the difference between year t0 and year t−1, which allows us to compare the change in financial performance of these ventures in dollar amounts, which is especially useful when considering the cost-effectiveness of philanthropic grants as an intervention, and comparing it with alternatives (Roberts & Lall, 2019).

Although a significant proportion of the ventures in our sample have received small grants, past research (McKenzie, 2017) suggests that only grants that are sufficiently large are likely to help ventures improve their organizational performance. In addition, in terms of signaling, Islam et al. (2018) suggest that the prestige of a grant would offer a positive signal of quality to prospective funders. Because our sample does not include information on the source of the grant, we suggest that using a relatively high threshold of grant size (US$20,000) would both allow for sufficient investment in organizational performance and provide a substantive signal of quality to commercial financiers. We acknowledge that the literature on the topic in social entrepreneurship is largely conceptual, and therefore does not offer prescriptions on this matter, but our threshold is also consistent with practitioner descriptions of the “missing middle” in impact investing, described as the funding gap for social ventures that require between US$20,000 and US$200,000 in capital (Aspen Network of Development Entrepreneurs, 2016). We also conduct sensitivity analyses for smaller and larger grant sizes (US$10,000 and US$30,000) to improve the robustness of our results.

Because we are interested in the organizational and signaling effects of receiving a substantive grant, rather than the specific relationship between grant amounts and financial performance, we follow the approach of Islam et al. (2018) and use dummy independent variables. Our first dummy variable takes the value 1 if a social venture reports receiving a grant of at least US$20,000 in the year t−1. In addition, because it is possible that the effects of philanthropic capital on performance may only be observable over a longer period, we use a dummy variable that takes the value 1 if a social venture reports receiving a grant of at least US$20,000 at some point before the year t−1, which allows us to examine some longer term effects of grant finance. Summary statistics of our dependent and independent variables are displayed in Table 1.

Dependent and Independent Variables.

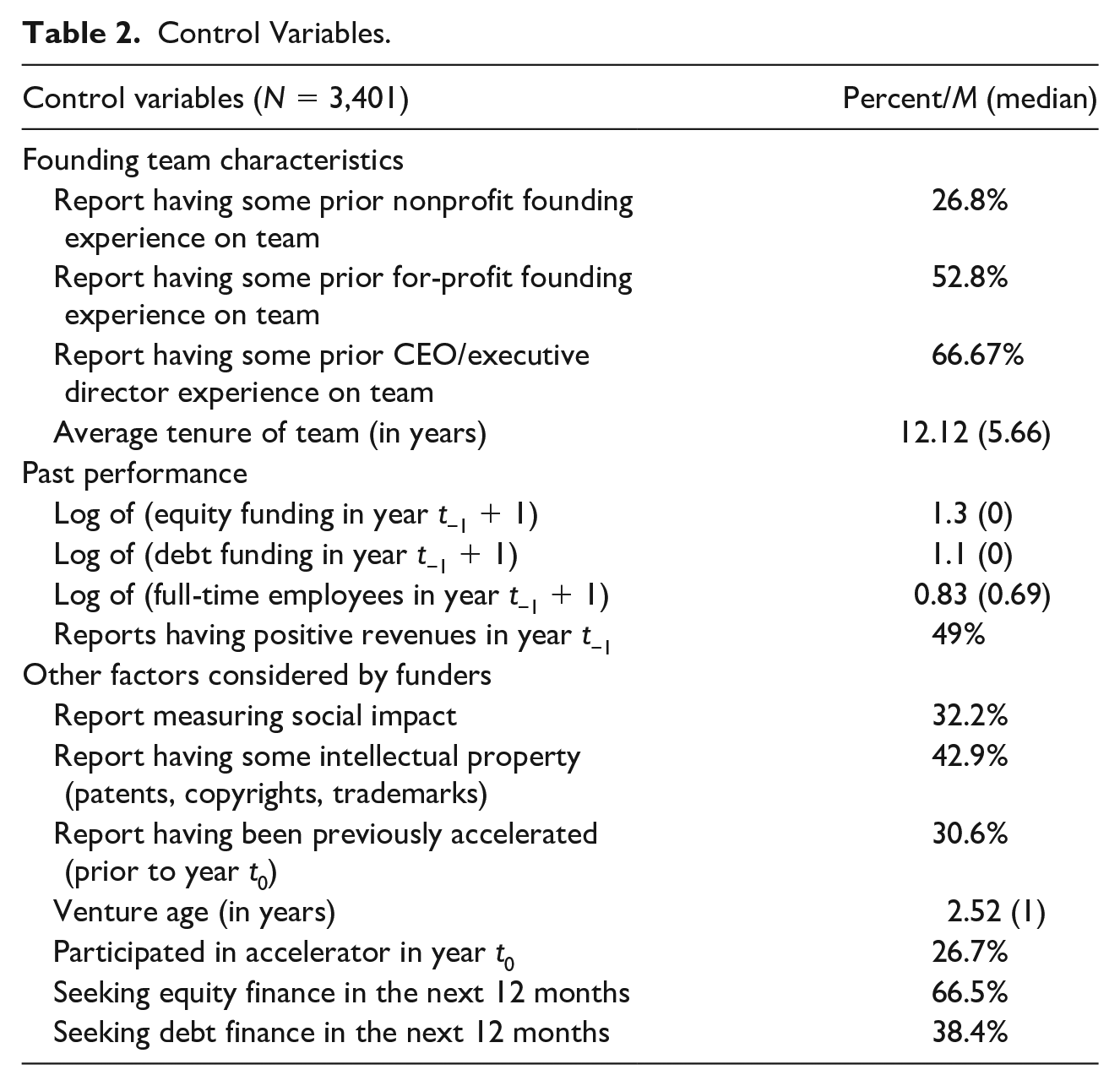

We recognize a number of factors that are likely to be correlated with future financial performance may also be plausible reasons for philanthropic funders to select ventures for support. For instance, we note that according to both conceptual and empirical research on philanthropic venture capital and social finance, funders tend to value the quality of the founding team over many other criteria (Gordon, 2014; Scarlata & Alemany, 2010). Therefore, we include several measures of human capital, including prior founding experience on the team (both for-profit and nonprofit), prior CEO/senior management–level experience, and the average work tenure of the team (in years), which helps us control for the quality of human capital on the founding team (Marvel et al., 2016).

In addition, philanthropic funders are likely to view the use of impact measurement as a positive sign that the venture is committed to its social mission (Lall, 2017). Participating in an accelerator program (either the one for which they are currently applying, or a previous program) may also be viewed as a favorable signal by potential funders (Kim & Wagman, 2014; Pandey et al., 2017; Plummer et al., 2016; Roberts & Lall, 2019). Intellectual property (in the form of patents, trademarks, and copyrights) may also be considered a signal of future promise by potential funders (Baum & Silverman, 2004). Finally, not all ventures may be seeking debt or equity finance. We therefore include dummy variables for the use of impact measurement practices, participation in an accelerator (current and prior), the possession of intellectual property, and whether they report seeking debt and equity finance in the next 12 months.

We control for other factors such as the age of the venture and include lagged values of the four dependent variables from the year t−1, which are likely to be correlated with future performance. We include fixed effects for the different country–income level categories, as defined by the World Bank’s 2013 classification, to control for possible variation across the different countries in our sample. Finally, we also test our results by including fixed effects for sector, to account for unobserved variance across sectors; and for the year in which the data were collected. Summary statistics of our control variables are provided in Table 2.

Control Variables.

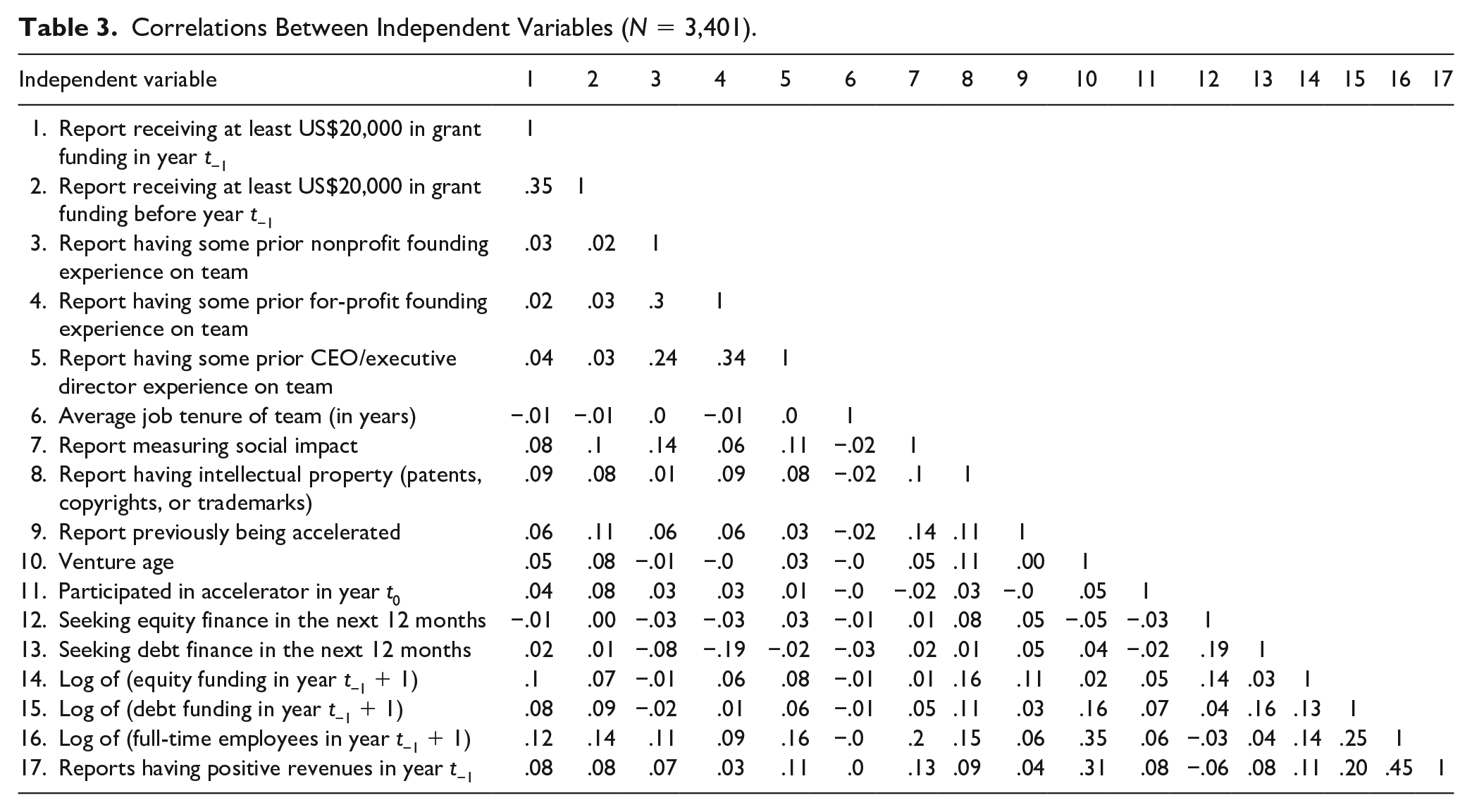

We examine correlations between our key independent and control variables in Table 3, and do not observe any instances of multicollinearity. All correlation coefficients are below .5.

Correlations Between Independent Variables (N = 3,401).

Results

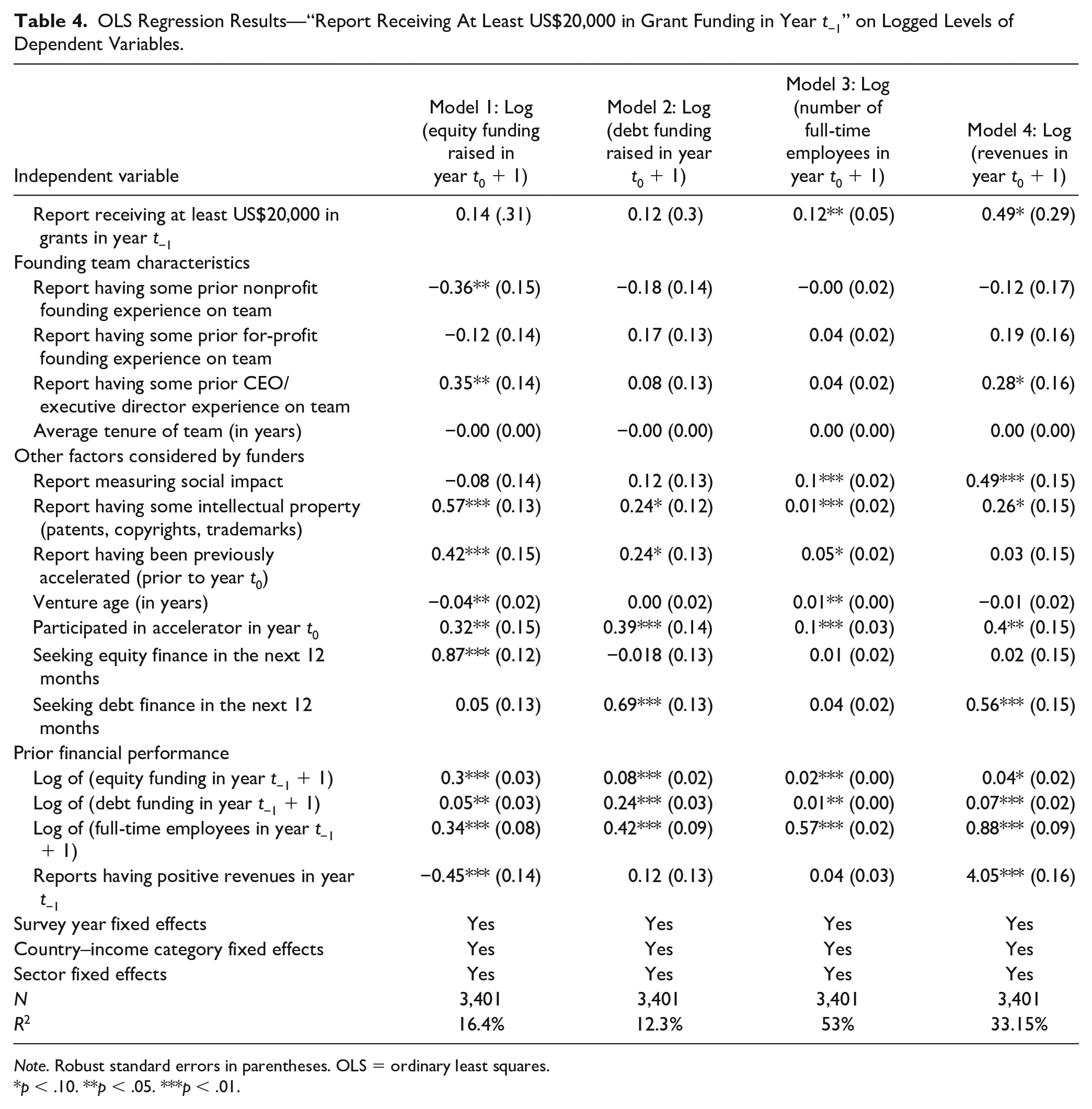

Our results suggest some nuanced effects of philanthropic funding on subsequent financial performance. In Table 4 (Models 1–4), we look at the effect of receiving at least US$20,000 in philanthropic funding in year t−1 on logged values of our dependent variables, and find that both revenues (at the p < .1 level) and employment (at the p < .05 level) in year t0 are positively and significantly related to getting a grant in the prior year. In particular, ventures that received a grant of at least US$20,000 in year t−1 grew by about 12% more than ventures that did not. However, we do not see any effects for debt and equity funding. It is plausible that the signaling effect of receiving a grant on external finance may only be observable after a substantive amount of time.

OLS Regression Results—“Report Receiving At Least US$20,000 in Grant Funding in Year t−1” on Logged Levels of Dependent Variables.

Note. Robust standard errors in parentheses. OLS = ordinary least squares.

p < .10. **p < .05. ***p < .01.

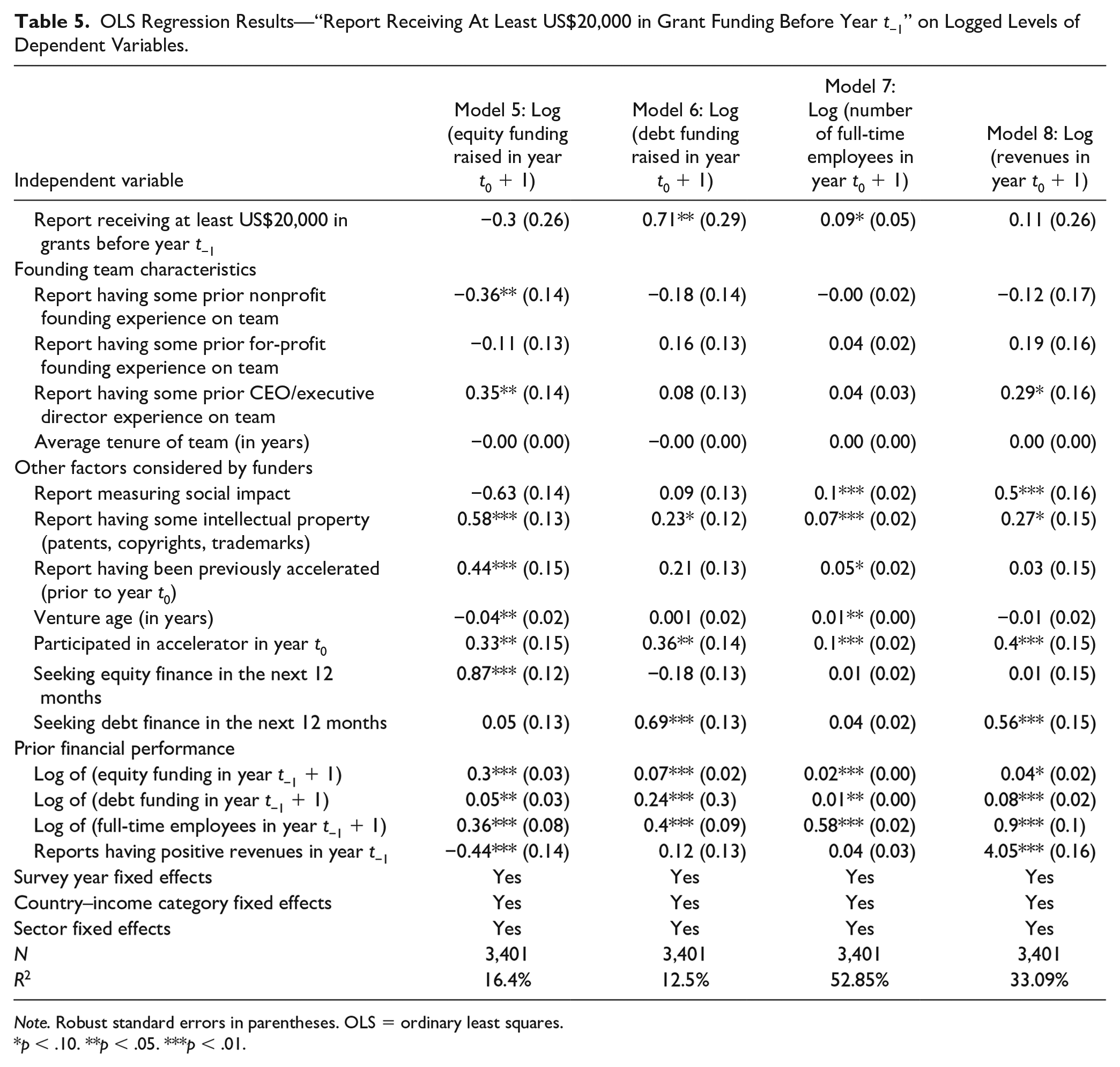

Therefore, we look at the effect of receiving a grant prior to year t−1 in Table 5, and find significant effects on levels of debt finance (at the p < .05 level) and weakly significant (p < .10 level) effects on employment. Ventures that received grants raised about 70% more in debt finance compared with those that did not obtain grants. Somewhat surprisingly, we do not see any effects on levels of equity finance or revenues. Among our control variables, we find that founding teams with some management experience are more likely to raise equity finance, as are ventures that possess intellectual property (consistent with past research on entrepreneurship). Naturally, seeking a particular type of finance (debt or equity) is predictive of actually receiving that type of finance. Accelerator participation also has positive and significant effects on all aspects of commercial performance, suggesting the importance of acceleration in stimulating social entrepreneurial growth. Somewhat surprisingly, we do not see strong differences across sectors. Finally, as expected, the lagged values of the four dependent variables are also highly significant predictors of subsequent performance.

OLS Regression Results—“Report Receiving At Least US$20,000 in Grant Funding Before Year t−1” on Logged Levels of Dependent Variables.

Note. Robust standard errors in parentheses. OLS = ordinary least squares.

p < .10. **p < .05. ***p < .01.

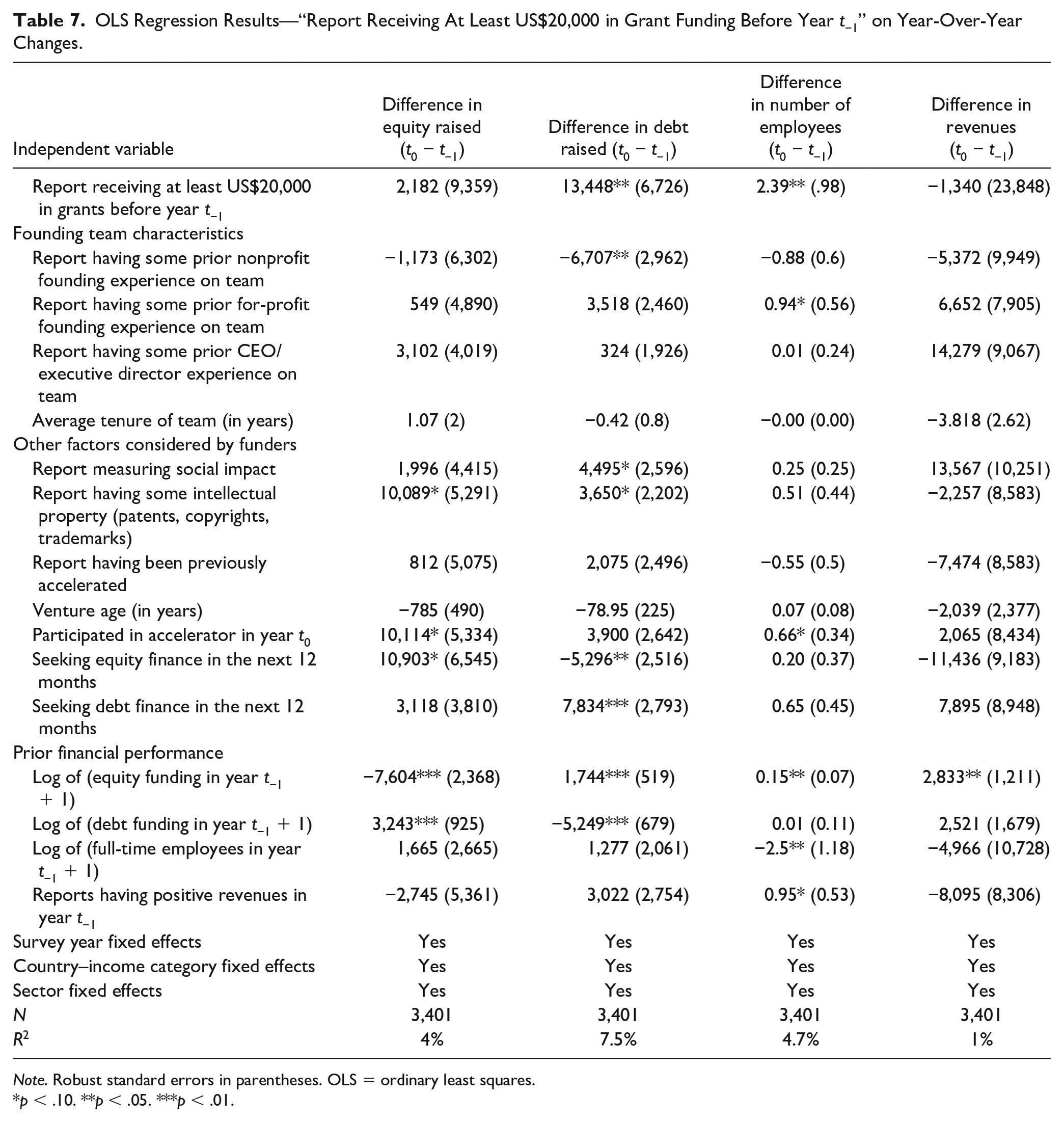

We add to this analysis by looking at effects on year-over-year changes in these four performance indicators in Tables 6 and 7, and find similarly positive effects on debt finance. We find that on average, ventures that received a grant in year t−1 raised US$12,717 more in debt in year t0 compared with those that did not receive a grant (p < .1). In addition, social ventures that received a grant before year t−1 raised US$13,448 more in debt in year t0 compared with those that did not receive a grant (p < .05). Receiving a grant prior to year t−1 was also associated with higher levels of job creation. Ventures that received a grant prior to year t−1 on average hired two additional full-time employees in year t0 compared with year t−1 (p < .05).

OLS Regression Results—“Report Receiving At Least US$20,000 in Grant Funding in Year t−1” on Year-Over-Year Changes.

Note. Robust standard errors in parentheses. OLS = ordinary least squares.

p < .10. ** p < .05. ***p < .01.

OLS Regression Results—“Report Receiving At Least US$20,000 in Grant Funding Before Year t−1” on Year-Over-Year Changes.

Note. Robust standard errors in parentheses. OLS = ordinary least squares.

p < .10. **p < .05. ***p < .01.

Therefore, we see some support for the hypothesis related to job creation (H2), and more support related to debt finance (H4) across the different models. However, we do not find support for H1 and H3, related to financial revenues and equity finance, respectively. In additional robustness checks, we also conducted ordinary least squares (OLS) regressions with the unlogged values in Models 1 to 8, with no changes in levels of significance or directions. We also tested these models using two different thresholds of grant amounts—US$10,000 and over, and US$30,000 and over, with similar overall results, which we include in Online Appendix A. 11 Finally, we also substituted the use of country–income level fixed effects and used fixed effects to control for the 77 different programs from which the sample is drawn. Once again, our results were broadly similar (minor differences in magnitude and significance, but no changes in direction), with support for the hypotheses related to debt finance and job creation.

Discussion

Our study makes several important scholarly contributions to the theory and practice of social entrepreneurial growth and development. We advance research on the capital mix in social venture finance by studying the underexamined role philanthropic grant financing might play in “scaffolding” organizational approaches to tackle multidimensional, complex, and interlinked societal challenges (Mair et al., 2016). We draw on and connect institutional logic theory and signaling theory to better understand the role of philanthropic grants in strengthening what Smith and Besharov (2019, p. 1) refer to as “structured flexibility” of social ventures by promoting growth while providing “guardrails” for the social mission. We offer a nuanced link between signaling theory (Connelly et al., 2011) and institutional logics by showing how the signal of obtaining a substantial grant (based in a social logic) may be interpreted differently by different stakeholders (Nason et al., 2018) rooted in a commercial logic. Finally, we make some useful empirical contributions by documenting the effects of philanthropic grants on social venture performance, providing mixed support for many of the arguments by practitioners (Koh et al., 2012) and qualitative research by scholars (Carlson & Koch, 2018; Dees, 2008; Smith & Besharov, 2019).

Our first two hypotheses examine the effect of philanthropic grants on employment and revenues. Philanthropic grants and other types of patient capital sources may be important because social ventures now have the resources to make the necessary organizational investments (e.g., by strengthening human resources) to better handle the competing social/business dynamics that confront many dual logic organizations (Smith & Besharov, 2019). Past literature shows how grants have been widely used to support R&D in commercially oriented science-based ventures (Howell, 2017), to support marginalized entrepreneurs (Mauldin, 2012), and to support economic development in certain regions (Carpenter & Loveridge, 2018; McKenzie, 2017). Our work contributes to this body of literature by describing how philanthropic grants function as “guardrails” by enabling social ventures to invest in human capital, without the urgency to pursue short-term revenue gains. We find that, on average, social ventures that received US$20,000 or more in philanthropic funding prior to year t−1 can hire two employees more than the previous year. This represents a substantial increase in employment for nascent social ventures that often start out with one to two full-time staff. At the same time, we do not observe any increases in revenue for ventures that received these grants, which suggests that entrepreneurs are spending these funds to invest in human resources, a key constraint for early-stage social ventures (Dimov, 2010; Marvel et al., 2016), rather than using the grants to boost organizational revenues and sales. In this regard, our findings challenge many of the descriptive narratives provided by scholars and practitioners that argue philanthropic grant financing can help social ventures improve their revenues (Dees, 2008; Koh et al., 2012), which does not seem to be the case, at least in the short term. Although other forms of finance may allow social ventures to make similar investments, they are more likely to be motivated by commercial returns and could lead to ventures drifting away from their social mission in the pursuit of short-term commercial performance (Ebrahim et al., 2014; Smith & Besharov, 2019).

We have similarly mixed results when it comes to the signaling effect of philanthropic grants for social ventures. Our study shows ventures that received a grant of at least US$20,000 in year t−1 raised US$12,717 more in loans in year t0, and the effect is even stronger over time (US$13,488 for grants received before year t−1). It is possible that receiving philanthropic capital provides social ventures with enough boost in their cash reserves to appear more credible and legitimate borrowers for debt financing. It is also possible that grant funding has a positive effect on debt financing because social ventures are able to borrow against the value of the philanthropic grant received, or perhaps the steadier revenue flows due to grant funding make them more attractive to debt financiers, who expect a fixed rate of return on their investment. In general, receiving grant funding acts as a positive signal of credibility to potential debt financiers, which is a common financial instrument in the rapidly growing impact investing sector (Mudaliar et al., 2018), and widely used by foundations and aid agencies (Rogerson et al., 2014).

However, we observe a null effect for equity financiers, suggesting that they interpret the signal differently. As Hehenberger and colleagues (2019) explain in their historical narrative, the charity or philanthropic logic was subjugated and devalued by impact investors and other social finance providers, while the commercial logic was elevated and advanced over time. Therefore, in contrast to research on equity investment in other sectors (Howell, 2017; Islam et al., 2018), philanthropic grants may be perceived as signals of dependency and less worthy of equity investment in social entrepreneurship. It is possible that equity financiers may view grant financing as a signal that the venture is too close to the social side of the spectrum, and less likely to produce the outsize financial returns typically expected in venture capital–style investing. Here, we explicitly connect institutional logics to signaling theory in social entrepreneurship finance by highlighting a specific type of challenge social ventures may face when trying to attract capital across different institutional logics. The same signal of credibility rooted in a social logic—a sizable philanthropic grant—may be interpreted positively, negatively, or simply ignored by financiers rooted in commercial logics. Social entrepreneurs must, therefore, carefully consider the benefits of seeking socially rooted philanthropic support, depending on the capital mix they desire for their ventures.

We acknowledge that there may be alternative explanations for our results and note two points of caution when interpreting our findings. Past research (Arthurs & Busenitz, 2003; Tyebjee & Bruno, 1984) suggests that venture capital and angel investors conduct due diligence over several months, so the effects of philanthropic grants on equity finance may not be fully captured in the 1-year time frame of our study. It is possible that some of the potential outcomes may only become evident over a 3- to 5-year period, as ventures move out of an exploratory stage and start to seek equity finance. Many promising social ventures fail to reach the investable stage of social venture development (Bosma et al., 2016; Teasdale, 2010) because they are not able to overcome the “pioneer gap” financing dilemma described in practitioner literature (Global Innovation Fund, 2016; Koh et al., 2012; Milligan & Schöning, 2011; USAID, 2016). Our study results show that philanthropic grants can help social ventures in the nascent stage by helping to catalyze debt financing, but without similar improvements in access to equity finance. Consequently, whether the increased debt financing can be a catalyst for obtaining enough equity financing to overcome the “pioneer gap” problem will not be known without a longer time frame for data analysis, which unfortunately fell outside the scope of our study.

Second, it is possible that we did not fully examine all the factors that may influence social venture performance. After interviewing 30 chief sustainability officers, Kaplan et al. (2018, p. 128) argue that there are three important design strategy principles to create “inclusive, sustainable, and profit-generating ecosystems”: Companies need to have “systemic, multisector opportunities; mobilize complementary partners; and obtain seed and scale-up financing.” It is clear that startup and scale-financing are critically important, but it remains unclear what type of coenabling or “scaffolding” (Mair et al., 2016) factors are necessary to accelerate social entrepreneurial performance. Many social ventures try to scale their social impact through organizational growth, but the pursuit of this growth may have the unintended consequence of undermining the dual logic mission of the social venture, and leading to mission drift (Ebrahim et al., 2014; Siebold et al., 2019). Therefore, we caution against drawing strong causal inferences between philanthropic grants and overall social venture performance at this stage. Similar to what Barnett et al. (2020) proposed in terms of designing corporate social responsibility initiatives for greater social impact, we believe a more long-term, “big data” quantitative research approach to social entrepreneurial finance might enable future studies to better determine causation.

Our results also offer some interesting directions for future research. Building on the management literature examining the institutional configuration of social entrepreneurship (Stephan et al., 2015) and viewing entrepreneurial organizations within a “complex, evolving ecosystem . . . ” (Autio et al., 2018, p. 73), our study provides a more nuanced understanding of the role finance (and particularly early-stage finance in the form of philanthropic grants) plays within the complex interlinkages of an entrepreneurial ecosystem (Liguori et al., 2018; Spigel, 2017; Thompson et al., 2018). Here, we note the ancillary finding that although philanthropic grants do not help social ventures obtain equity finance, participating in an accelerator program does. This finding is consistent with emerging research on impact-oriented accelerators (Lall et al., 2020), which finds significant and positive effects of acceleration on equity finance. Because most impact-oriented accelerators are supported by public or philanthropic sources (Roberts & Lall, 2019), it may be advisable for donors to use philanthropic grant financing to support accelerators, though further efforts are needed to ensure that these programs are as effective for more marginalized social entrepreneurs and those in less developed ecosystems (Lall et al., 2020).

Finally, we draw attention to the fact that these effects hold even after controlling for different social and environmental sectors. Although philanthropic grants should not be viewed as a “silver bullet” solution for social venture growth, the fact that the effects for debt finance hold after controlling for different sectors suggests that this form of social finance may provide a promising signal of credibility that deserves more focused attention in social entrepreneurship scholarship. Future research may also delve deeper into the cost-effectiveness of philanthropic grants in stimulating debt financing—for instance, what amount of grant acts as a sufficient positive signal to debt financiers, and do these effects grow over time? How can different financial instruments be blended and staged in the capital mix for social ventures? And, how do specific types of grants (restricted vs. unrestricted) serve as different types of “guardrails” that help or hinder social venture performance?

Conclusion

As scholars studying nonprofits, social movements, and philanthropy have noted (Francis, 2019; Jung et al., 2018), philanthropic funding is critical to the creation and operation of impact-oriented organizations worldwide; yet, there has been relatively little attention paid to its role in social entrepreneurship. In many ways, this omission reflects Hehenberger and colleagues’ (2019) description of devaluing the “social” side of the social finance spectrum. Whether we are discussing large social movements such as the mobilization of civil rights organizations like the National Association of Advancement of Colored Peoples (NAACP) in the United States (Francis, 2019), or nascent social ventures providing rural energy access in India like Husk Power (Desjardins et al., 2014), there is a critical need to improve our understanding of how we fund long-term solutions to multidimensional, complex, and interlinked societal challenges (Mair et al., 2016; Wry & Haugh, 2018). Securing the necessary funding to scale the impact of social ventures is widely considered to be one of if the critical organizational challenge confronting social entrepreneurs; yet, academically rigorous and practice-oriented research on social entrepreneurship finance has, to date, been limited. 12 We strongly agree on the growing call among businesses, governments, and foundations for a radical shift from funding individual projects or social ventures to supporting “more sustained, deeper-level transformations in society” (Grady et al., 2017, p. 2). To achieve this goal of sustained, deeper level transformations in society, our study clearly demonstrates that greater priority needs to be placed on more rigorous analyses of the most promising interventions that help drive social entrepreneurial growth. In a postpandemic economic landscape, how we finance social ventures and the next generation of social entrepreneurs is likely to become even more of a critical topic in social entrepreneurship theory and practice.

Supplemental Material

sj-pdf-1-bas-10.1177_0007650320973434 – Supplemental material for How Social Ventures Grow: Understanding the Role of Philanthropic Grants in Scaling Social Entrepreneurship

Supplemental material, sj-pdf-1-bas-10.1177_0007650320973434 for How Social Ventures Grow: Understanding the Role of Philanthropic Grants in Scaling Social Entrepreneurship by Saurabh A. Lall and Jacob Park in Business & Society

Footnotes

Acknowledgements

We are grateful to the editors and to three anonymous reviewers for their thoughtful comments and guidance through the review process. We thank the teams working on the Global Accelerator Learning Initiative (www.galidata.org) and the Entrepreneurship Database Program (![]() ) at the Aspen Network of Development Entrepreneurs and the Social Enterprise @ Goizueta Center for providing us with access to the data set used in this study. Finally, we appreciate the feedback from session participants at the 2017 Social Enterprise @ Goizueta Research Colloquium, the 2018 Sustainability, Ethics & Entrepreneurship (SEE) conference, and the 2019 Nonprofit Academic Centers Council Conference.

) at the Aspen Network of Development Entrepreneurs and the Social Enterprise @ Goizueta Center for providing us with access to the data set used in this study. Finally, we appreciate the feedback from session participants at the 2017 Social Enterprise @ Goizueta Research Colloquium, the 2018 Sustainability, Ethics & Entrepreneurship (SEE) conference, and the 2019 Nonprofit Academic Centers Council Conference.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: J.P. acknowledges the research grant support from China’s Chongqing Business and Technology University.

Supplemental Material

Supplemental material for this article is available online.