Abstract

Organisational changes of the public sector have led to increased decentralisation of public services. Only fully fledged financial accounting and reporting systems guarantee the consolidated information needed by executive and legislative bodies to fulfil their duties in financial management and the supervision of network entities. Consolidated financial statements may serve to increase accountability and transparency towards internal and external stakeholders. The article aims at giving an overview of consolidation approaches in Organisation for Economic Co-operation and Development countries. It will focus on the methods applied and the guiding principles followed to define the perimeter of consolidation. The analysis is carried out through a comparison of legal requirements and standards for consolidation, and the published consolidated financial statements, taking the International Public Sector Accounting Standards as a benchmark.

Points for practitioners

The analysis of consolidation practice in Organisation for Economic Co-operation and Development countries reveals that while the use of consolidated financial statements is increasing, there are still significant deviations from the perspective of international accounting standards. The results show that the equity method plays a crucial role as it is used in a transition period to full consolidation and/or for organisations having major influence on the statements of financial position. These findings are of interest in the ongoing debate of international standard-setting in the field of consolidation, as well as for the discussion of European Public Sector Accounting Standards.

Keywords

Introduction

Changes to the organisational composition of the public sector introduced by New Public Management-style reforms, leading to contracting-out and privatisation in their various forms, have led to an increased decentralisation of responsibilities in accounting in the public sector (Grossi and Reichard, 2008; Torres and Pina, 2002). Not only have these reforms been done for reasons of finding adequate forms of organising public sector activities, but, very often, the ‘escape out of the budget’ (to use a German-speaking world expression) was pursued for the purpose of hiding public debt.

It has now become widely accepted by those investigating financial reporting requirements in the public sector that the Consolidated Financial Statement (CFS) is a useful instrument for governments dealing with publicly owned entities because it presents a clear picture of the current economic status and functioning of the whole interrelated group (Chow et al., 2007; Grossi and Newberry, 2009; Wise, 2010).

As in the private sector, a need for more harmonised accounting practices in the public sector has also arisen among countries. Maybe the best way to reach the aim of more harmonisation of financial reports is to follow the International Public Sector Accounting Standards (IPSAS), issued by the International Public Sector Accounting Standards Board (IPSASB), which provide rules for preparing both annual statements and CFS. The IPSAS 6, 7 and 8 suggest control as the leading criterion to define the scope of consolidation, and by operationalising it, they adapt the concept for the specific characteristics of the public sector. With the rising importance of these single public sector accounting standards being used internationally, it can be expected that more and more countries will also switch to the respective suggestions for CFS. However, is it really this way? This article therefore aims to answer the following research questions:

What is the diffusion of CFS in Organisation for Economic Co-operation and Development (OECD) countries? Which consolidation methods are in use? Are they influenced in any way by the guiding principles to define the scope of consolidation or by the purpose that CFS should fulfil?

The aim of this article is to give an overview of actual consolidation practices in OECD countries and to identify major trends in consolidated financial reporting. Therefore, the article will be structured as follows: the second section will give a literature review of needs and users of CFS in the public sector and different consolidation theories and approaches. In the third section, the research design and terms and concepts of consolidation will be introduced. Results are mainly generated by document analysis, which was followed by semi-structured, in-depth interviews with accounting experts from 13 OECD countries that, at the moment, either produce CFS or will do so in the near future. The findings were contrasted with practice in 10 more OECD countries who answered to a short questionnaire. The fourth section will present findings, which will be summed up in the conclusion. Results show that CFS is an essential element of public sector financial reporting in OECD countries with modern financial management systems.

CFS link micro- (financial accounting) and macro-perspectives (statistical perspective) on the public sector and potentially present information for management decisions, on the one hand, and for financial and fiscal policy decisions, on the other. As such, they form a neuralgic interface between different economical perspectives, between different systems and different user groups. However, not much light has been shed on the users’ perspectives of CFS so far.

While the reasons for implementation are very different, it can be stated that the topic gains importance with the increasing use of internationally comparable, generally accepted accounting principles and, today, is a building block of modern financial management. If IPSAS is taken as a benchmark, consolidation scope, as well as methods and perspectives, deviate from it considerably due to different reasons.

Literature review

Utilising multiple theoretical perspectives to explain the needs for and users of CFS

The Agency Theory offers one possible explanation as to why consolidation in the public and private sector is significant in terms of accountability. It describes the information asymmetry between the agent and the principal and the problem of the pursuit of different interests by those parties. In order to address the issue of an imbalance of power between principal and agent (mostly in favour of the latter), Wise (2010) suggests that requirements for accountability and reporting to a superior can be a sufficient measure to benefit the principal’s interest.

Applied to the issue of consolidation, there are several layers of principal–agent relationships. The agent can be a department that is controlled by a superordinate entity, which is the principal. The principal may also have the role of an agent on an upper level and has to report to another superordinate entity (principal), and so on. Eventually, the governing body of the organisation or its holding organisation has the role of an agent that has to report to its stakeholders (e.g. the public or shareholders), acting as the principal (Greiling and Spraul, 2010). On all of these layers, the principal may control multiple agents. However, Agency Theory has received severe criticisms, while Stakeholders Theory is considered to be more substantial than Agency Theory (Robé, 2011).

Stakeholders Theory defines organisations as multilateral agreements between an enterprise and its stakeholders (Clarke, 2004) and offers another possible explanation as to why consolidation is significant in terms of accountability. However, due to the formal separation of the annual accounts of the governments and the providers of services, the creation of legally separate government-owned entities has often translated into an actual reduction in the degree of accountability and decision usefulness of public sector accounts. In fact, the annual accounts of governments may disclose only a partial view of their economic and financial activities because the financial situations and results of subsidiaries, joint ventures and associates are not necessarily included in the traditional annual reports of the government. CFS are therefore useful to provide relevant and undistorted financial information to internal and external stakeholders that encompasses every subsidiary or department and clears out any internal transactions, as well as mutual assets and liabilities. Otherwise, internal and external users of financial information would not be able to base their decisions on reliable and relevant information about the financial position, financial performance and cash flows of the ‘whole’ government, or they might find it more difficult to form an idea on it. Indeed, it must be recognised that CFS are not mutually exclusive of financial statements or financial information of other kinds. However, this might translate into more fragmented information. In order to avoid this lack of information, CFS have often been presented as a necessary step (Grossi and Mussari, 2008; Heald and Georgiou, 2000; Lande, 1998).

Internal stakeholders, namely, politicians and public managers, consider CFS as a useful tool for steering and controlling the direct and indirect provision of public services. They are a relevant tool for public decision-making in programming and controlling the different public policies.

CFS might also to be considered useful by external stakeholders (e.g. citizens, voters, taxpayers, suppliers, other public administrations, international organisations, banks, financial institutions and rating agencies) since CFS help to give a comprehensive view of the ‘whole’ government and its publicly owned corporations. In particular, banks are interested in CFS in order to understand the real and effective opportunities of creditworthiness of the governments and their owned corporations. Moreover, CFS could be a useful and informative tool for rating agencies to determine solvency and financial risks.

The benefits for the internal and external users and the potential improvement of public sector accounting systems have to be compared with the costs and obstacles involved in the implementation of consolidated financial reporting (such as personnel costs, costs for training and consulting, information technology (IT) systems, etc.). There are some problems with implementing and using CFS in the public sector, including the difficulty of comparing consolidated information across different levels of government and in defining the scope of consolidation (Grossi and Pepe, 2009; Heald and Georgiou, 2000; Robb and Newberry, 2007).

A relevant difficulty in the public sector to be overcome is the harmonisation of the financial statements of the different decentralised entities drawn up according to different accounting standards (Brusca and Montesinos, 2009). The figures and financial information produced by the government (as the controlling entity) and decentralised entities (as the controlled entities) are not always homogeneous and fully comparable. Therefore, the need to make individual financial statements more comparable, and the growing pressure for introducing CFS, is stimulating the adoption of IPSAS by public sector entities and of International Financial Reporting Standards (IFRS) by decentralised entities. Doing this would increase accounting homogeneity between the entities included in the consolidation (Grossi, 2009).

Private sector consolidation theories

There are different consolidation theories in the private sector. The Parent Company Theory focuses on the parent company’s shareholders and considers the interests of minority shareholders of its subsidiaries as liabilities. The CFS should therefore be prepared for the benefit of the parent company’s shareholders (Kam, 1990). In contrast to the Parent Company Theory, the Entity Concept of Group emphasises the economic unity of all enterprises and treats all shareholders similarly, whether controlling or not (Nobes and Parker, 2011). All interests are considered equally, so are all the assets and liabilities of the consolidated entity (Aceituno et al., 2006). Many standard-setters have found inspiration in the Parent Company Theory approach as a theoretical model of accounting rules for CFS (e.g. the Financial Accounting Standards Board (FASB), the International Accounting Standards Board (IASB) and also IPSASB) but the Entity Concept of Group theory seems to be more suitable for public sector organisations and the information needs of their stakeholders (Bisogno et al., 2014). The Ownership Theory discusses the situation in which the parent company only controls a part of a subsidiary and therefore only these partial assets and liabilities are consolidated with the entire parent company (Alfredson et al., 2009). The non-controlled interest does not belong to the group CFS and is therefore not disclosed in the statements.

Perspectives and scope of consolidation in the public sector

Although the theoretical foundation of financial consolidation in the public sector is rather poor (Wise, 2010), private sector consolidation, with their economic focus, may easily be applied to certain public sector entities (e.g. government-owned corporations), whereas different perspectives, scopes and methods have to be adopted in order to appropriately consolidate others. Brusca and Montesinos, (2009) point out that care is advised when business accounting is being adopted in the public sector. While the interest in private sector consolidation more or less lies in the ‘big picture’ sketched by one balance sheet and one profit and loss statement, which are quite easily compiled as ownership and control are clear, most of the time, things are not so easy due to public sector peculiarities, such as the importance of the budget, financial sources (i.e. non-exchange transactions), infrastructure and heritage assets, or the public service emphasis instead of profit-making.

Economic perspective (concept of control)

This concept of control is described as an economic perspective on the consolidation scope; political aspects of defining the boundaries of the public sector are not taken into account. Due to the government’s ability to exercise its power over many public entities, the control-driven economic perspective would allow the consolidation scope to be relatively large (Bergmann, 2009). Basically, an economic perspective (based on control) is the noticeable dominant factor in all those theories of financial consolidation in the private sector, and IPSAS are also based on such a perspective. IPSAS 6 1 names a number of requirements that must be met by a controlling entity in order to control another entity and thus consolidate this entity from the economic perspective that is dominant in the private sector. The entity must have the power to govern the financial and operating policies of another entity. This power must be presently exercisable and legally constituted. That does not mean, though, that the controlling entity is directly responsible for the operational management of the subordinate entity.

IPSAS 6 also specifies the power and benefit conditions that must be given in order to control another entity. The power element of control can be obtained by possessing the majority voting interest and by having the power to appoint or remove members of the governing body and cast a majority of the votes at a general meeting and meetings of the governing body in the other entity. Other indicators of control in terms of power are veto rights for budget decisions or the influence on human resources of the other entity. In terms of the benefit factor of control, the controlling entity must ‘obtain a significant level of the residual economic benefits or bear significant obligations’ and/or have access to the assets of the other entity. The benefit element of control can also be a non-financial gain from the activities of another entity (IFAC, 2011).

The power to set regulations by a public entity in this matter is not seen as control over the entities that are affected by the regulations, neither is economic dependence (e.g. a public entity being the single customer of a private entity) considered as being controlled (IFAC, 2011). This is maybe most obvious with universities, which are not consolidated in many countries for the reason of academic freedom in research and teaching though they would be economically dependent on taxpayers’ money.

In this sense, while it is easy to consolidate public corporations, such as railroad companies or postal services, or even central government entities, like ministries, because ownership and therefore control is clear, this might not be the case for a lot of organisational units (of which many even have their own legal status) because, as Montesinos and Brusca (2009) argue, the operationalisation of ‘control’ is not always distinct. Due to the complex structure of the public sector and its variety of forms of decentralised entities (i.e. state-owned enterprises, foundations, institutions, public and private partnerships, etc.), the following consolidation perspectives have emerged.

Budgetary perspective

According to the budgetary perspective, entities should be consolidated if they are relevant for the budget or budgetary decisions are influential or even critical for them. The budgetary perspective includes the control principle, but adopts it in a more rigorous way as it requires budgetary influence. Therefore, the scope of consolidation is smaller and excludes entities that are neither receiving funds from government budgets nor contributing to them (Bergmann, 2009; Brusca and Montesinos, 2009).

Organisational and legal perspective

CFS following the organisational perspective would group entities according to the organisational structure set by legislation (Bergmann, 2009). The consolidation would therefore include all public entities that are legally dependent on a superordinate entity (Brusca and Montesinos, 2009).

Statistical perspective

CFS on the basis of financial statistics follow the definition of the so-called general government sector (GGS). GGS exclude entities with more than 50 percent market revenue (Eurostat, 1996: 44). GGS includes all levels of government, even in a federal setting in which states are clearly not controlled by the national government. Economic control is not a prerequisite (Bergmann, 2009). Public corporations should be differentiated in the statistical groups of financial (e.g. government-owned financial institutions) and non-financial corporations and accordingly consolidated (Brusca and Montesinos, 2009).

Risk perspective

Adopting the risk perspective would lead to a scope of consolidation comprising all entities that could cause financial risk to a government. This can be a very large group of entities that would be at least as large as in the economic perspective. It would also include large private sector corporations that would get a government bail-out in case of financial difficulties (‘too big to fail’). The control criterion is no prerequisite (Bergmann, 2009).

Research design and consolidation methods used

Research design

This article seeks to give an overview of consolidation practices in OECD countries. The main focus of this analysis is the 13 OECD member states that are known to follow an accrual basis of accounting (e.g. IPSAS or comparable National Accounting Standards) and currently compile (and present) CSF or will conduct similar reforms in the near future. These countries have been analysed in detail. They were complemented with another set of OECD countries to abstract for anything like general OECD practice. This set was made up of 10 countries who answered a short questionnaire. For two out of these 10 countries – Demark and Slovakia – it turned out that they are currently applying accrual accounting as well. They were not included in the further analysis, however, because while Denmark consolidates its national accounts according to financial statistics, in our findings, it does not do so according to financial accounting rules. Slovakia was not included due to technical problems because it is at an early stage of consolidation. These two countries are marked in italics. Figure 1 presents the research scope in detail.

Assessment Framework

The findings are based on the comparison of the different consolidation standards and other legal requirements, as well as the published financial statements, of the 23 OECD member countries taking the IPSAS as a benchmark. For each country that has been analysed in detail, the findings were completed and validated through semi-structured telephone interviews with one or two high-ranking public finance experts of the respective OECD country alongside a questionnaire that was sent and received beforehand. These experts were chosen from the ministry of finance, the national audit office and/or a standard-setting body. The interviews took between 30 minutes and one hour, depending on the details already available from desk research and from the questionnaire. The questionnaire asked for the following information:

standards applied (international or national) by the central government for financial reporting; compilation of CFS (Yes/No); scope of the reporting entity for CFS; underlying perspective or criterion of the reporting entity for CFS; application of different consolidation methods for different entities; recent changes/changes in the near future to the reporting entity for CFS (scope of consolidation) purposes of the CFS (main internal/external users of the CFS and what kind of information is being provided to them; online availability of CFS); and existence of interim reports.

These interviews have been complemented by a brief survey of the rest of the OECD countries based on a structured questionnaire to which the aforementioned 10 countries responded. The questionnaire was sent to an expert pool from OECD representatives on this topic. If no answer was received, for some countries, there was a backup solution, with researchers from the country who would answer instead. The brief survey asked for information about the standard applied by central government for financial reporting, for the compilation of CFS, for the scope of the reporting entity and for the underlying perspective or criterion of the reporting entity for CFS.

Consolidation methods versus technical aggregation

Differing to the IPSAS, in this article, the term ‘consolidated financial statements’ is used in the sense of financial statements being compiled on the basis of accrual accounting, using the methods of international accounting standards according to consolidation, including full consolidation (or line-by-line consolidation), the equity method of consolidation and/or proportional consolidation. In this respect, the methods correspond to international accounting standards with the following meaning:

Line-by-line consolidation or full consolidation: The financial statements of a controlling entity and its controlled entities are presented as if they were single financial statements by combining identical or similar items of assets, liabilities, net assets/equity, revenue and expenses on a line-by-line basis. The underlying financial statements shall be compiled on the basis of the same underlying accounting standards and with the same date. Transactions between the entities are eliminated and minority interests are identified and presented separately. This method corresponds to IPSAS 6. Equity method: The shares of an entity are initially recognised at cost and subsequently adjusted for the post-acquisition change in the reporting entity’s share of the net assets/equity of the entity. The equity method is outlined in IPSAS 7. Proportional consolidation: A partner’s share of each of the assets, liabilities, revenue and expenses of a jointly controlled entity is combined line by line with similar items in the partner’s financial statements or reported as separate line items in the partner’s financial statements (method for joint ventures). This method is outlined in IPSAS 8.

In contrast to these methods, more traditional approaches towards the technically compiled single financial statements of an economic entity are often based on the (modified) cash principle. These aggregations are used for a consolidated presentation of budgets while unsystematic or totally missing eliminations of transactions lead to intransparent totals. Such approaches towards aggregation are not used in the meaning of CFS in this article.

Research findings

Overview and development trends

Country cluster description

Consolidation practice in OECD countries

Table 2 presents the main development trends in consolidation practices in OECD countries. They can be summarised as follows:

For the OECD countries, a trend towards accrual accounting and the presentation of CFS according to international accounting standards is obvious. A remarkable number of countries – the so-called ‘pioneers’ – have implemented accrual accounting and present CSF. They follow the approach of the elimination of internal transactions, the disclosure of minority interests or the audit of CFS. In reference to criteria of consolidation and methods, different practices can be found, ranging from the UK’s whole-of-government approach following the control criterion, to the Swedish example of consolidation of controlled entities, applying the equity method on the basis of organisational law. This makes a general judgement more difficult. Nevertheless, countries that are explicitly following international accounting standards, like Australia, Canada, Estonia, New Zealand, the UK and, in the near future, Spain and Chile, seem to be clearly oriented towards the control criterion. Countries with a looser link to international standards by tendency show a scope of consolidation that can rather be explained by historical developments or that has been defined later on (e.g. Denmark, Sweden and the USA) and therefore lacks the stringency and taxonomy that it would have following accounting standards. A second group of countries (e.g. Austria and Belgium), the ‘reform followers’, is reforming national accounting standards at the moment or will be doing so in the near future. The implementation of accrual accounting according to IPSAS or IFRS, as well as the presentation of CFS, is at the heart of these reforms. These countries therefore follow the group of pioneering countries mentioned earlier and, with them, the trend of modern, transparent public sector financial statements. Recent practice of OECD countries shows a correlation between the accounting method (cash or accrual) and the presentation of CSF. For countries with accrual accounting, the presentation of CFS is more or less state of the art. Except Hungary, all countries with accrual accounting compile CFS, or at least plan to do so, while countries on a cash basis typically present aggregated statements of income and expenditure (especially as part of budget execution reporting), but no CFS as suggested by international accounting standards. A last group of countries – the so-called ‘reform refusers’ – are not open towards international developments and defy any attempts towards accrual accounting reforms, sticking to the cash principle. At a closer look, with Norway, the Netherlands, Germany and Luxembourg, rather prosperous countries are part of the group, and the switch to accrual accounting is either politically contested or has failed, as in the case of Germany, or the pressures on the financial system and performance are simply not high enough. On the other hand, in Norway, Germany and the Netherlands, the systems at sub-national levels are significantly further developed than at the national level. Nevertheless, the recent developments in OECD countries or discussions at Eurostat concerning the compulsory implementation of IPSAS for the countries of the European Union (EU) demonstrate that most of the countries of the last group will also have to address the topic of accrual accounting sooner or later.

The benefit and use of CFS

While different users of CFS could be identified by the questionnaire, there is no focus on the possible benefits or the expectations of different user groups presented here. The main reason for this is the absence of systematic user surveys from which such information could be extracted, at least in the context of public organisations compiling CFS; however, in academia, there has been some, though not too much, research on this topic (e.g. Kober et al., 2013; for Australia, see also Wise, 2010).

New Zealand is the only exception as a survey was recently conducted on behalf of the Treasury comprising around 30 interviews with representatives of the most important user groups (industries, economy, science, politics, financial institutions and the media, as well as international organisations) (Colmar Brunton, 2012). The aim of the survey contracted by the Treasury is to reflect upon the current form of financial reporting to better align it with user needs. Unfortunately, CFS are not treated in detail, but only as part of financial statements. In summary, it can be stated that financial reporting contains useful information, therefore generating benefit to users. Special highlights of the survey include demonstration of exceptional willingness towards high transparency and high data quality, as well as detailed data preparation and presentation. The extensive documentation of information sends important signals to national and international stakeholders regarding transparent reporting, and is the basis of satisfying heterogeneous information needs.

Synthesis

The analysis of consolidation methods and scope leads us to three main statements:

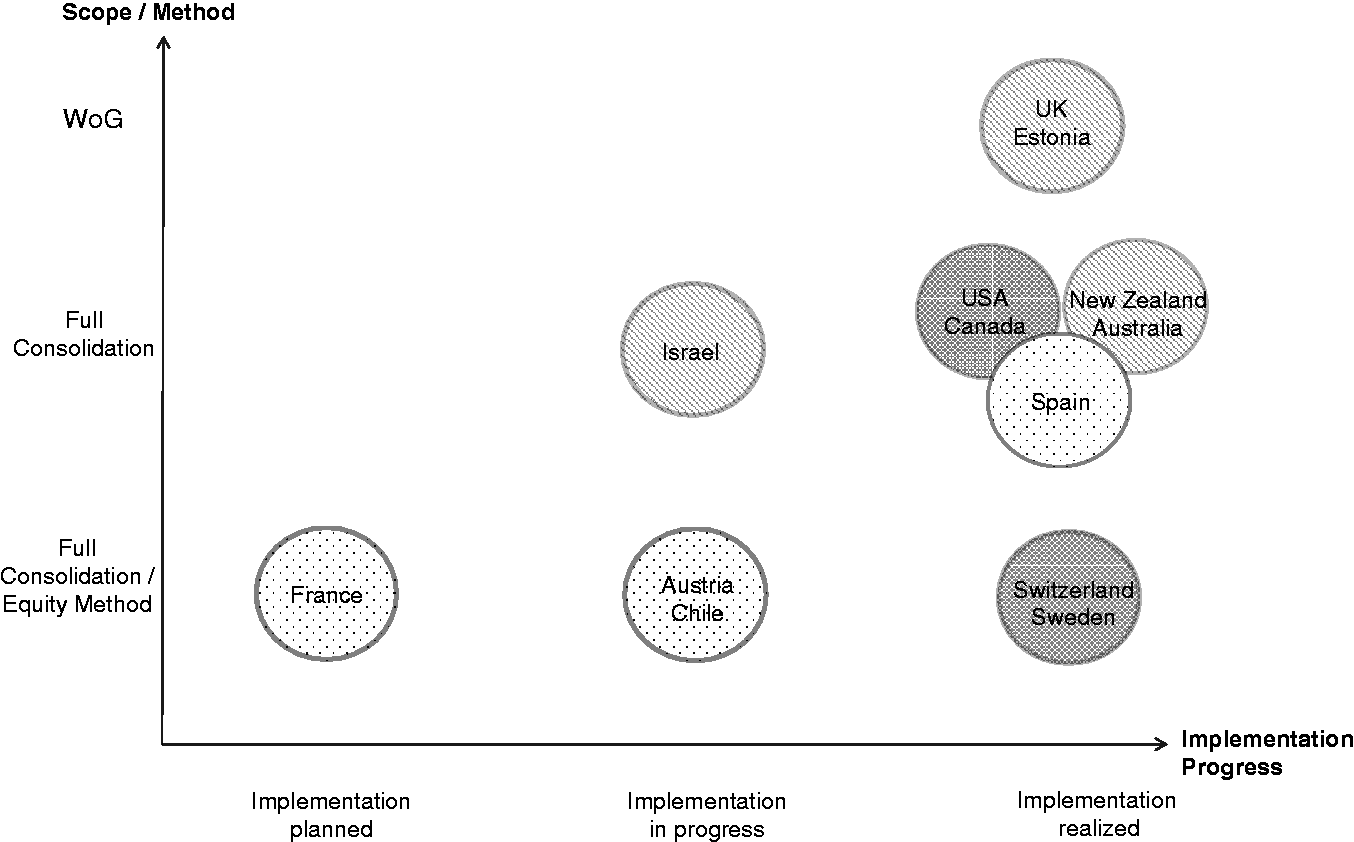

The whole-of-government approach as implemented in the UK or Estonia can be seen as the most consequent approach to CFS for countries with either a centralised state architecture or that have experienced it traditionally, like in the case of the UK. Whole-of-government, especially in the UK, means that consolidation comprises all state levels.

2

The case of Estonia seems to be especially remarkable as both the National Bank and other entities with a strong balance sheet are consolidated at the highest level, with two CSF reflecting, on the one side, the public sector without public enterprises and financial institutions (GGS) and, on the other side, the total of the public sector with all controlled entities. For federal states, the whole-of-government approach as it is used in the UK is less useful because of their state architecture. For this group of states, a clear tendency towards full consolidation following the control criterion is obvious. The group is made up of the Anglo-Saxon countries, traditionally being innovative regarding financial management, but also Spain, of which this would be less expected. Regarding the consolidation of entities with a strong balance sheet, namely, commercial banks and insurance companies, even countries generally following full consolidation due to the control criterion use the equity method (e.g. Spain or – still, though this will change – the UK regarding commercial banks). While Canada follows the control criterion to define the scope of consolidation, financially independent (though economically controlled) enterprises are consolidated by applying the equity method. A slightly deviating path from the control criterion is followed by the USA, where financial accountability, as well as historical, organic developments, defines the scope of consolidation. A third cluster is made up of those states that currently are strongly oriented towards the equity method, either as an intermediate step towards full consolidation (like in Austria or in Chile) or as a consolidation method planned in the medium term (like in Sweden or Switzerland), where organisational criteria dominate the definition of the scope of consolidation and controlled entities are consolidated by applying the equity method. Consolidation methods and implementation process

In Figure 2, the countries have been arranged according to their position against the axes of the scope and method of consolidation (y) and the implementation of CFS (x). The scope and method of consolidation were combined on one axis to allow for a two-dimensional picture. In the figure, the country clusters in light grey represent countries in transition. Country clusters in dark grey represent countries following the organisational perspective of consolidation or other dominant approaches (like stewardship for the USA or financial statistics for Canada). The other clusters represent countries oriented towards international standards with a clear orientation towards the control criterion.

Conclusion and outlook

CFS and the information presented form a neuralgic interface between different economical perspectives, between different systems and different user groups. They link micro- (financial accounting) and macro-perspectives (statistical perspective) on the public sector and potentially present information for management decisions, on the one hand, and for financial and fiscal policy decisions, on the other. These considerations were of importance at the early implementation stages of the whole-of-government approach in the UK, at least in the beginning, though a more pragmatic approach was followed in later stages (Chow et al., 2007; Heald and Georgiou, 2009, 2011), and have shaped the Australian whole-of-government approach. As not all countries presenting CFS follow that kind of textbook-like design, the article closes with some answers on the three research questions presented at the beginning.

The status of consolidation practice in OECD countries

CFS are state of the art in financial reporting and an essential element of public sector financial statements in OECD countries with modern financial management systems. Experiences with CFS on an accrual basis range back as far as into the early 1990s in the Anglo-American countries Australia and New Zealand. While the reasons for implementation are very different (i.e. macroeconomic perspectives; full microeconomic perspective; the harmonisation of financial accounting with financial statistics), it can be stated that the topic gained importance with the increasing use of internationally comparable, generally accepted accounting principles and, today, is a building block of modern financial management. This trend is being followed by countries that had followed more traditional approaches of aggregation up until now (i.e. Austria, Chile, France or Spain). The only user survey available conducted by a ministry of finance, dating from 2012 (New Zealand), sketches a positive picture of CFS. Users of CFS appreciate its rich information (transparency, data quality and detailing). However, some users also criticise high complexity, which is hardly avoidable though.

The scope of consolidation and consolidation methods

In most OECD countries examined, the control criterion is the dominant principle used to define the scope of consolidation. This is even true in the light of most of these countries orienting themselves to or even fully implementing the IPSAS. Even New Zealand, which uses sector-neutral accounting standards, is going to follow the IPSAS in respect of consolidation, starting with the budget year 2014/15. However, the different ways to operationalise the term ‘control’ show that the concept, originating from private sector accounting standards, has to be adapted by public sector institutions, therefore reflecting national characteristics to a certain degree.

Deviating from the control criterion, in the USA, financial accountability, stewardship and the control of financially dominated entities are the leading principles used to define the scope of consolidation. In Sweden, the organisational perspective is followed. Both approaches share the fact of dealing with this issue more on an individual basis than showing the rigour of the control criterion, which could also be seen as the negative effect of the organisational perspective.

Concerning the consolidation of national banks and social insurance companies, research findings give a mixed picture. Those countries that are clearly oriented towards international accounting standards, by tendency, consolidate both the national bank and social security (i.e. Australia, Estonia, New Zealand, the UK (where the consolidation of the national bank is at least planned for the near future) and Canada (applying the modified equity method)). Due to the early stage of accrual accounting reforms, at the moment, neither Austria nor France consolidate national banks or social security institutions. For all other countries, no general statements can be made. However, concerning national banks, the two conflicting criteria of economical control and statutory independence from executive and legislative bodies have brought up different solutions, namely, either consolidation (like in the countries just mentioned) or separate presentations outside CFS (i.e. Chile and the USA). From the countries examined, only in the USA and in Switzerland is the national government not the owner of the national bank.

Even if the control criterion is the dominant criterion used to define the scope of consolidation, this does not necessarily mean that all entities controlled are also fully consolidated. In specific cases, it seems reasonable to favour the equity method instead of full consolidation.

When arguing in favour of the equity method, it is stated that shares are presented as individual asset items, and therefore more transparent, as if all items would be added up, like in the case of full consolidation. This could lead to a blurred picture of central government.

Therefore, in many countries, entities with a strong balance sheet and gaining significant revenues from market activities (mainly commercial banks and financial intermediates), are not fully consolidated, but consolidated according to the equity method. However, consolidation by the equity method does not lead to a clear picture concerning liabilities and the respective financial risk associated with controlled entities.

Canada presents an interesting example as it also follows statistical considerations besides the dominating criterion of control. Financially independent but economically controlled companies are not fully consolidated, the reason for this being the fact that the activities of the companies have commercial character no matter whether they are controlled by the government or not. The relationship between the government and companies therefore better resembles an investment, which is better reflected in financial statements using the equity method.

To conclude, it can be argued that although, with the spread of international accounting standards, control is the dominant criterion in public sector CFS, the resulting full consolidation is not satisfying information needs in the sense that the full consolidation of entities with large balance sheets is blurring the picture. This is especially true for financial companies. In any of the examined cases, the equity method is used instead of full consolidation. However, as argued, this has disadvantages in the sense of limited information concerning liabilities.

From the perspective of clear information about the financial performance and position of a government, the best approach would be different CFS showing different perimeters of consolidation. This would start with CFS for the central government, where all separate financial statements of single entities, for example, ministries, are consolidated to show the financial situation of the central government. Within separate financial statements, IPSAS 6 suggests three methods to account for investments in controlled entities (equity, cost or fair value), of which the equity method is the most applicable. On the level of quasi-government, further controlled entities (e.g. public companies) would be included in the consolidated statement of central government in order to show the full picture of financial information. In the light of the current crisis, however, any approach, being either full consolidation or equity consolidation, would have given a better and clearer information basis for those governments switching to a risk perspective overnight in an attempt to save their financial sectors under risk.

As the discussion with international standard-setters on the topic of equity consolidation or full consolidation goes on, it will be interesting to observe further developments – especially in the context of the current debate about introducing harmonised public sector accounting standards for EU countries (European Public Sector Accounting Standards (EPSAS)). Although the European Commission recognises the IPSAS as a reference for potential EU harmonised public sector accounts, they address several concerns regarding IPSAS – for example, the possibility of choosing between different accounting treatments. However with respect to CFS, IPSAS 6 follows a distinct approach with a clear direction towards full consolidation of all controlled entities. IPSAS 6 should therefore act as an indisputable guideline for the development and adoption of EPSAS. Although equity consolidation may be a reasonable concept of presenting CFS in a first step (e.g. Austria and France) or with respect to specific entities (e.g. central banks), any medium-term approach should clearly follow the full consolidation of controlled entities, including social insurance companies.

Footnotes

Acknowledgement

This work was conducted on behalf of the Swiss Federal government. The article only gives a summary of the results. For any further details concerning the countries examined, please contact the authors.

Funding

This work was funded by the Swiss Federal government.