Abstract

Recently, outside blockholders, external owners that hold 5% or more of their firms’ outstanding common stockholdings, have been pressuring their firms to engage in divestiture activities. This study considers whether the influence of those owners also extends to how the divestiture is implemented, whether through spin-off or sell-off. Tests of an agency theory model using data from 205 divestitures show that the adoption of spin-offs or sell-offs is associated with the amount of outstanding common stockholdings held by outside blockholders and the size of the unit divested. Spin-offs are used more frequently when outside blockholders own more of the divesting firm’s stockholdings and the divested unit is larger, while sell-offs tend to be selected when outside blockholders own less stock and the divested business is smaller. Consistent with agency theory expectations, spin-offs would allow the blockholders to decide whether to hold or sell their interests in the divested firm, a decision they could make in accordance with their individual portfolio risks. Sell-offs of small units could be used to preserve organizational diversity and produce proceeds that would help the divesting firm’s managers pursue their self-interests. Overall, outside blockholders appear to shape how divestitures are done, even if they cannot directly intervene in their firms’ operations.

Keywords

Recently, prominent external owners have pressured large companies such as Abbott, Motorola, McGraw-Hill, Marathon Oil, HP, Cargill, and ITT to use divestitures to reverse slumping financial performance records. For example, as the Wall Street Journal reported, Hedge fund Jana Partners LLC and the Ontario Teachers’ Pension Plan last month pushed the company to divide [by spin-off] into four parts . . . [calling] the announced moves “vital steps in reversing years of underperformance at McGraw-Hill, and are critical parts of what we were seeking for shareholders.” (Chon, 2011a: B1-2)

Other companies are weighing similar actions; for instance, Pepsi is considering divesting its highly successful Frito-Lay subsidiary to help raise its flagging stock price to appease growing shareholder concerns. The Wall Street Journal reports that it isn’t enough for Pepsi to lower earnings targets again. . . . Rather Pepsi would do better on its beverage unit, which has better long-term prospects . . . [as] a “spinoff of Frito-Lay would be optimal,” Mr. Laboy [of Credit Suisse] wrote. By Credit Suisse’s calculation, such a divestiture would boost Pepsi shares to $85 from their current level of about $61. (Evans, 2011: C1)

These observations indicate a new theme in divestiture activities: Large owners are not just calling for divestitures; their companies are responding by using a common implementation divestment mode, the spin-off (Chon, 2011b; Thomas, 2011). Does the reach of large owners go beyond initiating divestitures to also include how they are implemented? What are the boundaries of owner impact—are they limited to motivating the divestiture or do they extend to its execution as well?

Previous research reports that large external owners, typically referred to as outside blockholders because they do not work within the firm and hold blocks of 5% or more of a company’s common stockholdings, often serve as a driving force behind divestitures (see Brauer, 2006; Lee & Madhavan, 2010; Moschieri & Mair, 2008, for literature reviews). However, few studies consider how far the influence of these blockholders extends into the actual divestiture implementation process. Some researchers report that ownership by outside blockholders is associated with the size and relatedness of divested units (Bergh, 1995). Others find that nonduality leadership of the directory board (when the CEO does not hold the chair position) increases owner impact and leads to divestitures by spin-off rather than sell-off (Nixon, Roenfeldt, & Sicherman, 2000). Although there appears to be a connection between common agency theory constructs and divestiture (Bethel & Liebeskind, 1993; Chatterjee, Harrison, & Bergh, 2003), to date little is known about a possible link between governance entities such as outside blockholders and how divestitures are implemented. Our understanding of the reach of such owners into the divestiture process is currently underdeveloped.

The present study seeks to increase knowledge of how outside blockholding owners affect divestitures, specifically how these owners might shape the ways in which their firms divest. We focus on two divestiture implementation methods, spin-off and sell-off, as these two have long been the most popular approaches (Bruner, 2004; Chen & Guo, 2005; Gaughan, 1999) and they are widely considered to be the two main alternatives for fully divesting assets (Hite & Owers, 1983; Khan & Metha, 1996; Nixon et al., 2000). A spin-off occurs when a divesting firm redistributes ownership of a subsidiary to its shareholders, creating a company that operates independently with its own separate governance structure, while sell-offs involve the sale of assets from one firm to another in exchange for cash and/or securities (Bergh, 1995; Hite, Owers, & Rogers, 1987; Jain, 1985). Drawing from agency theory, we hypothesize that a divesting firm’s outside blockholders have different self-interests than its managers and that the selection of spin-off or sell-off as a divestiture method will be associated with whether the blockholders have more or less influence as a result of higher or lower levels of ownership concentration. The predicted relationships are expected to depend on the size of the divested unit, as we posit that larger divestitures result in greater risks to the ability of both outside blockholding owners and managers to pursue their objectives. We also consider whether owner/manager self-interest alignment schemes such as managerial equity ownership and board leadership separation (when the CEO is not the chair of the board of directors) are related to the selection of spin-off or sell-off through their impact on the relative influence of owners over managers.

The study forwards a different theoretical explanation of when firms divest by spin-off or sell-off. The results contribute by supporting a more comprehensive model of how firms divest and find that agency theory may provide an integrative model of divestitures that includes decisions from both the motive and implementation phases of the process. Most generally, the findings demonstrate that outside blockholding owners appear to have a long reach when it comes to divestiture: They seem to do more than just call for divestitures; they also seem to influence how those actions are implemented.

Theory and Hypotheses

Outside blockholder owners have strong incentives to monitor and influence the management of their firms to make decisions that favor the blockholders’ interests, while smaller, nonblock stockholders tend to “vote with their feet” when their firms do not meet expectations (Edmans, 2009; Rubin, 2007; Shleifer & Vishny, 1986).

1

More specifically, because of their large investments, outside blockholding owners tend to be highly committed to their firms’ strategies and frequently involve themselves in the decision making of their firms. For example, Bergh notes that blockholders may face costs that may increase the commitment they have to their firms: Certain conditions can impede an owner’s exit [and raise the owner’s commitment]: the costs of switching shareholdings from one company to another may be higher than the corresponding benefits, the owner may be unable to sustain the losses associated with selling the shareholdings, and/or there may be no suitable substitute into which to transfer the holdings. (1995: 223)

If an owner’s wealth and investments can be impacted by divestiture decisions (e.g., Markides, 1992; Schipper & Smith, 1983; Wright & Ferris, 1997), then it seems likely that large blockholders would ensure that their self-interests factor into how divestitures are implemented.

Agency theory provides a theoretical framework for linking owners, including outside blockholders, to the decisions of their firms. For example, agency theory has been used to explain how owners and managers approach investments in innovation (Hitt, Hoskisson, Johnson, & Moesel, 1996; Hoskisson & Johnson, 1992) and strategy decisions such as diversification (Amihud & Lev, 1981, 1999; Lane, Cannella, & Lubatkin, 1998). Agency theory assumes that principals (owners) and agents (managers) have different self-interests and that the organization’s actions will vary based on which of these groups is able to exert control relative to the other (Eisenhardt, 1989; Hill & Snell, 1988; Jensen & Meckling, 1976). An agency problem occurs when the principal delegates work to the agent in a context where the parties entertain different goals and risk preferences, when it is costly to ascertain the actions and outcomes of the agent, and when managers serve their own interests at the expense of their owners (Fama & Jensen, 1983; Williamson, 1964; Woo, Willard, & Daellenbach, 1992). In addition, David, O’Brien, Yoshikawa, and Delios note that agency problems involve conflicts of interest between owners and managers over the potentially conflicting goals of growth and profit. . . . Agency theorists contend that sales growth may provide managers with private benefits such as high pay, power, status, and prestige [and] [a]ccordingly favor higher levels of sales growth than is optimal for shareholder profit maximization. (2010: 637).

Examples of agency problems include excessive compensation, executive perquisites, aggressive but unprofitable growth strategies where a manager is predisposed toward a diversifying acquisition in order to increase managerial power or expected compensation, or reduce employment risk, regardless of whether the acquisition is in the best interests of the shareholders. (Chatterjee et al., 2003: 88)

Advocates of agency theory posit that shareholders can easily diversify their shareholdings and are expected to be risk neutral, willing to undertake any project that might result in a positive net value. . . . CEOs, on the other hand, are viewed as risk averse and opportunistic [as] they are faced with the risk of losing their jobs if they undertake risky projects. They are unable to diversify their income streams and may face personal liability. (Deutsch, Keil, & Laamanen, 2011: 213)

David et al. further note that “as weak owners are unable to sufficiently constrain managerial opportunism . . . managers implement diversification strategies that generate higher growth that benefits managers but yields lower profits for shareholders (2010: 636).

Agency theory has been used to explain why firms divest (see Brauer, 2006; Lee & Madhavan, 2010; Moschieri & Mair, 2008, for literature reviews). For example, “agency theorists believe that the reason why many companies undertake a divestiture has to do with [reconciling misalignments] between managers, owners and the board of directors” (Moschieri & Mair, 2008: 401). Indeed, several recent media announcements have linked activism by large owners in firms such as ITT, Kraft Foods, and McGraw-Hill to divestitures. For example, in response to increasing activism among its larger shareholders for higher returns, Fortune Brands recently “began its future as two companies . . . when it completed the spin-off of its home and security unit and renamed itself Beam Inc.” (Rappeport, 2011: 16). Viewed from this perspective, divestitures are used to transform highly diversified firms (what managers prefer) to what the owners seek: less diversified, more focused, and higher performing firms (Bergh, 1995; Chatterjee et al., 2003; Hoskisson, Johnson, & Moesel, 1994).

This logic can also be extended to how the divestiture action is conducted. We predict that the commonly described self-interests of owners (managing investment portfolio risk) and managers (preserving organizational diversity to lower employment risk; Amihud & Lev, 1981, 1999; Denis, Denis, & Sarin, 1997, 1999; Jensen, 1986) will be best served through adopting alternative divestiture implementation methods. Although most owners would have similar interests, outside blockholders, due to their concentrated holdings of large blocks of stock, would likely be more influential and successful than nonblockholders when pressuring managers to meet their objectives. 2 More specifically, when conditions warrant divestiture, spin-offs, compared to sell-offs, would give outside blockholders a better opportunity to pursue their self-interests. First, in a spin-off, the blockholders have the opportunity to decide whether to hold or sell their stockholdings in both the spun-off and divesting businesses independently, a decision that will likely be influenced by the divested unit’s effect on the divesting firm’s earnings streams and their combined effect on the owners’ portfolio risk (cf. Gibbs, 1993; Hill & Snell, 1988; Wright, Ferris, Sarin, & Awasthi, 1996). If either the spun-off unit or divesting firm’s revenue and earnings potential alters the outside blockholder owners’ portfolio risk beyond their particular thresholds, they can decide to sell their holdings in either firm. By contrast, sell-offs do not provide outside blockholders with this control or efficiency in the management of their investment portfolio. In sell-offs, the property rights of the divested firms are assigned to the acquiring firm, while the financial proceeds are allocated in exchange to the divesting firm. Outside blockholders therefore have to rely on managerial discretion to use the sell-off proceeds in a manner that is consistent with their investment portfolio’s objectives. Thus, through a spin-off, the blockholders are able to manage their overall portfolio risk in a direct manner that is more consistent with their investment self-interests than managers can do through sell-offs.

Second, spin-offs allow all owners to elect a governance board and leadership structure for the newly divested firm, enabling them to shape its future in a manner consistent with their objectives (Hambrick & Stucker, 1999; Miles & Woolridge, 1999; Seward & Walsh, 1996). These owner-approved managers can now pursue objectives that are consistent with the owner’s priorities, and they do not have to seek compromises with leaders of the divesting firm (cf. Seward & Walsh, 1996; Woo et al., 1992). In addition, spin-offs provide outside blockholders with improved transparency of what the divested unit’s leaders can and cannot do (Bergh, Johnson, & DeWitt, 2008). Further, spin-offs can also reduce agent monitoring costs because performance of the spin-off unit would no longer be consolidated with that of the other divisions or concealed beneath various corporate layers and arbitrary allocations. Results should be directly visible, more easily measureable and more directly linked to the efforts of the division. (Woo et al., 1992: 435; see also Allen, 2001; Krishnaswami & Subramaniam, 1999)

Further, Seward and Walsh (1996) argue that newly spun-off firms tend to create effective internal controls and more efficient market-based incentive compensation contract systems. Such actions may help “unlock” or transfer value from the divesting firm to its shareholders (Hite & Owers, 1983; Krishnaswami & Subramaniam, 1999). Considered collectively, spin-offs can enjoy a shorter distance between policy and implementation and a decrease in size and complexity of organizational structure; further, spin-offs reduce the ambiguities between owners and managers (Aron, 1991; Moschieri & Mair, 2008: 401; Seth & Easterwood, 1993). In a sell-off, the divested business becomes absorbed by another organization, and the shareholders lose all abilities to directly affect what happens to the entity.

By contrast, sell-offs may be more advantageous for managers’ self-interests. On the face of it, divestitures would seem to represent a vehicle that could reverse or threaten managers’ objectives of firm size and diversity. For example, Jensen notes that a CEO does not want to be remembered as presiding over an enterprise that makes fewer products in fewer plants in fewer countries than when he or she took office—even when such a course increases productivity and adds hundreds of millions of dollars of shareholder value. (1989: 66)

Nonetheless, divestitures become a necessary action that managers have to adopt (Taylor, 1988). In those circumstances, sell-offs represent a more advantageous method for managers to reallocate firm capital and resources to best serve their self-interests. First, sell-offs can generate cash and/or securities that can be applied to reduce the divesting firm’s debt and increase spending in innovation (Hamilton & Chow, 1993; Hoskisson & Johnson, 1992; Hoskisson et al., 1994), which lower both firm and managerial employment risk (Hill & Snell, 1988, 1989; Zuckerman, 2000). Indeed, while sell-offs produce resources that can be used to improve the productivity and financial performance of the divesting firm (Bergh, 1995; Hoskisson & Hitt, 1994; Markides, 1992, 1995), spin-offs provide no financial proceeds to the divesting firm, except a possible tax write-off (Frank & Harden, 2001; Miles & Woolridge, 1999; Nixon et al., 2000). Instead, the contribution of spin-offs to the divesting firm is often more attributable to the organizational governance savings and reduced size and complexity than any financial windfall.

In addition, sell-offs offer managers the opportunity to balance the subsidiary holdings of their firms to best reduce uncertainty in revenue streams. Amihud and Lev (1981) argued that managers use conglomerate acquisitions to diversify their firms so to reduce an overdependence on any one particular revenue source. Summarizing the agency theory and diversification strategy literature, Denis et al. conclude that “the likelihood of a firm being diversified is negatively related to the ownership of outside blockholders” (1999: 1072). For managers, who have a vested interest in building a highly diversified organization that best serves their self-interests of minimizing employment risk (e.g., Amihud & Lev, 1981, 1999; Denis et al., 1999), divestiture by sell-off would convert units into cash proceeds that could then be used to fund other activities that may better enable them to accomplish their objectives. Spin-offs offer no such advantage. Indeed, spin-offs tend to reduce the divesting firm’s size without offering a compensatory financial benefit that the managers can then apply to serving their own self-interests. Using sell-offs may serve the managerial interest of minimizing employment risk by ridding the firm of troubled assets or by generating cash that can be used by the managers for their own benefit, but sell-offs may not be in the best interest of shareholders who would prefer to make their own decisions regarding the makeup of their investment portfolios.

Further, sell-offs allow managers to alter the firm’s strategy in a manner that best preserves their own reputation and standing. For example, in their study of South African companies, Wright and Ferris (1997) argued that even when businesses are efficient and performing well, top executives may use divestitures because of personal interests and noneconomic pressures. Their finding that the significant negative abnormal returns that resulted when otherwise financially healthy companies divested implies that top managers use these actions to exploit their own self-interests rather than the interests of the shareholders (Lee & Madhavan, 2010: 1349). For example, Wright and Ferris conclude that the results are counter to the traditional theory . . . where organizations are managed in the best interests of their owners . . . and not supportive of the premise that senior executives are motivated to act in the best interests of their shareholders. . . . Managers, as agents of shareholders, may not always act in the best interests of the owners. (1997: 81-82)

Spin-offs, on the other hand, tend to be more beneficial to shareholders. Thus, sell-offs may be instruments for enabling managers to pursue their own interests over those of shareholders.

Following the conventional logic that stockholding concentration reflects whether owners or managers have the most control (Amihud & Lev, 1981; Bergh, 1995; Bethel & Liebeskind, 1993; Denis et al., 1999; Hill & Snell, 1988), we propose a hypothesis that links stockholding concentration in outside blockholdings and divestiture by spin-off or sell-off. When outstanding stockholdings are higher for those blockholders, they have higher bargaining power, managers generally need to be more responsive to owner self-interests, and divestitures are expected to occur through spin-offs. When the stockholding concentration is lower among outside blockholders, managers can more ably pursue their self-interests and divestitures through sell-offs are expected.

Hypothesis 1: Higher levels of stockholding concentrations among outside blockholders will be associated with spin-offs, while lower levels will be associated with sell-offs.

We also suggest that this relationship could depend on contextual factors. Agency theory provides a basis for considering how attributes of the divestiture transaction, alignment incentives, and the structure of the divesting firm’s governance systems could have an impact upon the relationship between outside blockholders and the choice between spin-offs and sell-offs.

Divestiture Size

Factors that might bear on owner and manager self-interests can also influence their decision making (Fama & Jensen, 1983). One such condition for divestitures is the size of the transaction (Bergh, 1995). Divestiture size is an important attribute because not all divestitures would have the same impact on blockholder portfolio risk and managerial self-interests. In particular, divestitures of larger units pose a higher threat to the blockholder owner’s portfolio and managerial risk reduction than smaller transactions, as the potential gains and losses associated with the divestiture of a large unit would be magnified and more material. Outside blockholders favor spin-offs of such businesses, as they could subsequently decide whether the financial prospects of the newly divested firm justify retaining ownership given their own individual risk thresholds. In addition, larger units may be harder and more risky to sell, as fewer potential buyers exist that can afford the purchase of such assets, creating market conditions that could precipitate a reduction in the value of the to-be divested assets (Bergh, 1995; Hite et al., 1987). Spin-offs do not carry such risks and might therefore be preferred for divesting larger units (Bergh et al., 2008). Finally, since spin-offs can “unlock” financial value for all shareholders, particularly in overdiversified and underperforming firms, outside blockholders prefer spin-offs of larger units so that they can more easily appropriate the respective monetary gains associated with such divestitures.

By contrast, managers would likely prefer selling smaller businesses, as “the sale of small units does not threaten the company’s overall stream of revenues and income as much as the sale of large units” (Bergh, 1995: 224). Such divestitures are less likely to alter the diversity and size of the divesting firm, better preserving the attributes that contribute to managerial self-interests such as large and diverse firms (cf. Amihud & Lev, 1981, 1999; Hill & Snell, 1988). Thus, outside blockholders would likely favor spin-offs for larger divested units, allowing them direct control over the riskiness of their portfolios, while managers prefer sell-offs of smaller businesses.

Hypothesis 2: The relationship between stockholding concentrations among outside blockholders and divestiture by spin-off is more positive when the size of the divested firms increases.

Alignment Incentive

Agency theory’s principal–agent problem may not necessarily reflect a permanent divide, as some have advocated the use of incentives to bring managers into the same mindset as owners. Two popular schemes that affect both incentive alignment and relative power to pursue incentives include managerial stock ownership and CEO duality, where the CEO also serves as the chairman of the directory board. We consider whether these methods serve to moderate the relationship between managers, outside blockholder owners, and the choice of spin-offs and sell-offs.

More specifically, situations in which managers have an ownership stake in their firms are believed to “discourage managerial opportunism, promote shareholder-wealth-maximizing behaviors, and achieve higher levels of firm performance” (Sanders, 2001: 477), as stock ownership by managers could both increase their sympathy toward owners and raise their commitment to their firms’ financial outcomes (Jensen & Meckling, 1976; Jensen & Murphy, 1990). 3 In the absence of stock ownership, managers often increase the size of their firms past optimal levels (Jensen, 1986), acquire other companies and expand diversity levels (Jensen & Murphy, 1990), and resist downsizing and restructuring (Dial & Murphy, 1995). Thus, Sanders (2001) observed that stock ownership can increase managers’ reluctance to engage in risky actions, as they have more to lose if the stock values of their firms declines. He finds that stock ownership appears to encourage executives to become more conservative when it comes to decisions concerning acquisitions and divestitures and to make decisions more consistent with owners’ interests.

This logic suggests a possible moderating effect of managerial stock ownership on the relationship between owner concentration of outside blockholders and the likelihood of spin-off or sell-off adoption. When managerial ownership is high, the positive relationship between outside blockholding concentration and adoption of spin-offs is likely strengthened, as managers seek to use the divestiture mechanism that best fits their goals as partial owners, which, as posited above, would more likely be spin-offs. By contrast, low levels of managerial ownership reduce the stock’s incentive alignment benefits, encouraging managers to maximize their own objectives rather than owners’. The relationship between the owner concentration of outside blockholders and divestiture by spin-offs is therefore expected to decline when managerial ownership falls, and therefore divestiture will more likely occur through sell-offs. Thus, we predict that firms are more likely to spin off when ownership concentration of outside blockholders is higher and managers hold more of the firm’s outstanding common stockholdings. By contrast, firms are more likely to sell off when ownership concentration of outside blockholders is lower and managers hold less stock.

Hypothesis 3: The relationship between stockholding concentrations of outside blockholders and divestiture by spin-off is more positive when managers hold more of the firm’s outstanding common stock.

Governance System

The structure of the divesting firm’s governance system, namely, its directory board, might also have an impact upon how divestiture decisions are implemented. In particular, whether the CEO has discretion to pursue his or her own self-interests with respect to the board’s interest of serving owners is a possible determinant of whether divestitures are conducted through spin-off or sell-off. One particularly salient way to capture whether the CEO has the power to pursue his or her self-interests is CEO duality, which occurs when a firm’s CEO concurrently chairs the board of directors. Short, Ketchen, and Palmer (2002) note that agency theory holds that firm performance tends to suffer under duality because a board’s ability to effectively monitor the CEO is reduced if its primary overseer is the person being monitored (Fama & Jensen, 1983; Harrison, Torres, & Kukalis, 1988). Also, duality increases the potential for information asymmetry between managers and owners, allowing executives to engage in opportunistic behaviors that reduce shareholder wealth (Jensen & Meckling, 1976). This concern encourages boards that are sympathetic to owners to discourage CEO duality (Finkelstein & D’Aveni, 1994). Further, Finkelstein and Hambrick observe that “CEO duality is one of the most contentious issues in public debate about the role of boards of directors, with most commentators recommending a separation of the top two positions in a firm” (1996: 213). This argument has been applied to divestitures; Nixon et al. (2000) report that when directory boards have separation of the chair and CEO, control systems are more in favor of owners, and spin-offs become more likely than sell-offs.

Going another step, CEO board duality would likely be relevant to whether outside blockholders can influence divestiture implementation decisions. When CEO duality does not exist (e.g., there is separation between the board and the firm’s leadership), the relationship between outside blockholder ownership and adoption of spin-offs is likely increased, as owners have more influence and managers will face increased pressure to use the divestiture mechanism of spin-offs because this method best meets the owners’ self-interests. By contrast, when CEO duality exists, managers have conditions that are more favorable to their self-interests, and divestiture by sell-off becomes more probable.

Stated more formally, the relationship between the stockholding concentration of outside blockholders and divestiture by spin-off is expected to increase when CEO duality does not exist. By contrast, the association between the stockholdings of these blockholders and spin-offs is predicted to decrease when the CEO is also the board chair.

Hypothesis 4: The relationship between stockholding concentrations of outside blockholders and divestiture by spin-off is more positive when CEOs and the chair of the board are held by different individuals.

Method

Sample

Testing the hypotheses required a sample of firms that had already made divestitures. This sample was determined using several stages. We first randomly identified 300 divestitures that were announced and completed between January 1, 1990, and December 31, 1999. These announcements were found in the Securities Data Corporation’s (SDC’s) Worldwide Merger & Acquisition Database. We then examined each divestiture relative to several screens: (1) The divesting firm had to be publicly held and headquartered in the United States, a necessity for data collection purposes. (2) The divestiture had to be voluntary and completed. (3) Only the first divestiture event by any of the divesting firms was included, in order to minimize potential firm bias. (4) Data had to be available for all of the study variables. (5) The spin-offs were finalized and there was a complete 100% redistribution of ownership to the divesting firm’s shareholders, to control for any direct postdivestiture influence by the divesting firm (e.g., Semadeni & Cannella, 2011). (6) Other forms of divestitures, including leveraged buyouts, equity carve-outs, and liquidations were excluded. Applying these screens reduced the sample to 205 divesting firms, of which 83 (40.5%) were spin-offs and 122 (59.5%) were sell-offs. Mean comparisons of the discarded and retained divesting firms indicated no significant differences in terms of the transaction size (dollar value of the divestiture), profitability (return on assets [ROA]), year, and debt.

Dependent Variable

A dummy variable, called divestiture type, was coded 1 when the divestiture occurred through a spin-off and 0 when it was a sell-off. The classification of spin-off and sell-off was found in the SDC’s Worldwide Merger & Acquisition Database and was cross-referenced with Mergerstat and Wall Street Journal reports and articles. No differences existed in the reporting of spin-offs and sell-offs across these three sources. In addition, no divestitures were a hybrid of the two types.

Independent Variables

Outside blockholder ownership

Outside blockholding ownership was defined as the percentage of the divesting firm’s common stock held by external shareholders that owned 5% or more of the firm’s outstanding stockholdings (Bergh, 1995; Bethel & Liebeskind, 1993; Hoskisson et al., 1994). This value was found in Compact Disclosure, SEC filings, and proxy reports.

Divestiture size

Divestiture size is the total dollar value of the divestiture, logged to account for variability in size (Hoskisson et al., 1994). This value was reported in SDC’s Worldwide Merger & Acquisition Database and cross-referenced with Mergerstat. The variable was called transaction price.

Managerial ownership

A variable called managerial ownership was computed as the percentage of the divesting firm’s outstanding common stock held by senior managers (senior vice president level and higher). The value was found in Compact Disclosure, SEC filings, and proxy reports.

CEO duality

A variable called duality was coded 1 if the CEO was also the chairman of the board. It was coded 0 if otherwise (Short et al., 2002).

Control Variables

The research design includes variables to control for extant explanations of the adoption of spin-offs and sell-offs and the motives for divestitures more generally (Achen, 1986). Prior research has shown that owners push for strategy changes through divestitures when the firm is suffering from performance problems (Bethel & Liebeskind, 1993; Chatterjee et al., 2003; Gibbs, 1993). First, we included three variables to account for the divesting firm’s predivestiture financial proceeds. (1) The divesting firm’s ROA one year prior to the focal divestiture completion year was included. (2) Financial performance can vary across industries, so the mean ROA for the divested firm’s primary 4-digit industry one year prior to the focal year was also measured. (3) Financial distress has been linked to the use of spin-offs or sell-offs (Nixon et al., 2000). We followed Nixon et al. (2000) by using the earnings before interest and taxes (EBIT)/interest expense ratio as a proxy for distress (data collected in Compustat).

Second, previous experience has been associated with the subsequent use of divestitures, including spin-offs and sell-offs (Bergh & Lim, 2008). Experience was the summed count of the divesting firm’s spin-offs and sell-offs for the 10 years prior to the focal divestiture year (reported by Thompson Financial).

Third, the divested firm’s size (log of total assets) reflects its complexity and possible information asymmetries, which also have been related to how firms divest (Bergh et al., 2008). These data were found in Compustat.

Fourth, the study covered several years, so we examined whether there were any trends in sell-off or spin-off activity that might influence the findings. We found that the differences between the two actions was relatively small for all years except in 1994 and 1995, where sell-offs outnumbered spin-offs by ratios of 3:1 and 2:1, respectively. A dummy variable was created to account for the two years with unusually high frequencies of sell-offs. We called this variable sell-off trend and coded it 0 for each year from 1989 through 1993 and also in 1996 and 1997. This variable was coded 1 for 1994 and 1995. This dummy accounts for the unusual patterns of activity in these two years.

Fifth, two possible strategic motivations for the divestiture were included. In the first, the divested firm’s diversification strategy was represented using Rumelt’s (1974) classification typology, considered the gold standard of diversification measures (Bergh, 2001; Hoskisson, Hitt, Johnson, & Moesel, 1993). We expect that firms having high levels of unrelatedness and low levels of relatedness among their product lines, such as unrelated or conglomerate businesses, are more likely to use sell-offs in order to overcome the problems associated with having exceeded their optimal levels of diversification. By contrast, firms having high relatedness and low unrelatedness among their product lines, like single and dominant businesses, are expected to use spin-offs (Bergh et al., 2008). Following Rumelt’s measurement scheme and criteria, a variable called diversification strategy was coded 1 for those divested firms meeting the single business criteria; dominant businesses were coded 2, related-constrained were coded 3, related-linked were coded 4, and unrelated businesses were coded 5. 4 Two researchers independently coded these strategy levels; reliability tests using intraclass correlations were .96. Differences were discussed and resolved until 100% agreement was reached. Data were collected from Compustat for the year prior to the focal divestiture (to include the divested assets).

The second strategic reason for divestitures is the relatedness of the divested assets. Divested assets that originated from the divesting firm’s primary (4-digit Standard Industrial Classification [SIC] code) businesses were considered to be specialized, while those outside the core were not (Bergh, 1995; Hoskisson & Johnson, 1992). The divested assets were considered using three categories to represent the multidimensional nature of a firm’s asset base: physical assets (plant, machines, equipment), human assets (staff, management, sales), and the divesting firm’s brand name (Williamson, 1991). Separate dummy variables were used for each asset type; the variables were coded 1 when the assets originated from the parent’s primary 4-digit SIC and 0 otherwise. The 4-digit SIC primary business was reported in Compact Disclosure, while the identity of the divested assets was found in articles reported in the LexisNexis database and annual reports and proxy disclosures. Two coders working independently exchanged disclosures and agreed on 94% of the values.

Analyses

The hypotheses were tested with logistic regression analysis because the dependent variable, divestiture type, is dichotomous (spin-off = 1, sell-off = 0). 5 Logistic regression analysis provides, for each variable in the equation, a nonstandardized coefficient (B) that ranges from positive to negative infinity and is distributed as a z score. The coefficients represent the effect of each independent variable on the probability that a particular event will occur, in our case the probability that a given divestiture will take the form of a spin-off rather than a sell-off. A positive coefficient indicates that an increase in the independent variable is associated with a higher probability of spin-off (and lower probability of sell-off), while a negative coefficient indicates that an increase in the independent variable is associated with a lower probability of spin-off (and higher probability of sell-off). Unlike in ordinary least squares regressions, the magnitude of the logistic coefficients does not directly indicate the marginal effect of a unit increase in the independent variable on the dependent outcome (Hoetker, 2007; Wiersema & Bowen, 2009). Additional analysis is necessary to determine the marginal effect, and the marginal effect of any individual independent variable will vary as a function of the values of all other independent variables. Interaction terms require additional analysis and interpretation.

Results

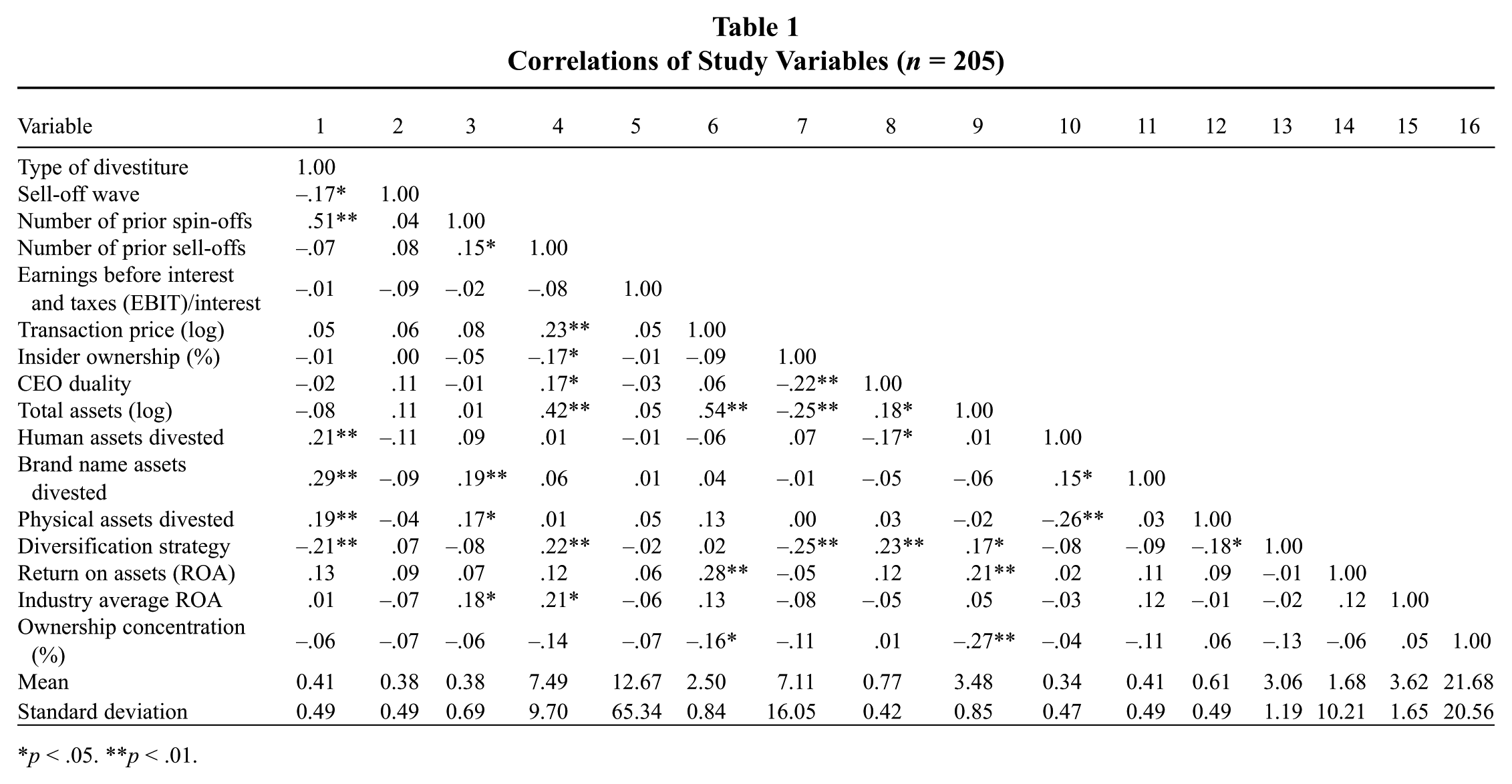

Table 1 reports the means, standard deviations, and correlations for the study variables.

Correlations of Study Variables (n = 205)

p < .05. **p < .01.

The hypotheses were tested using logit analysis techniques in the Stata statistical software package. The nonlinear nature of the logit function requires extra care in interpreting results and characterizing the size of the observed effects (Hoetker, 2007; Wiersema & Bowen, 2009). Marginal direct effects for each model were calculated using the mfx postestimation command with all variables held at their mean value. The results of the base model are reported in Table 2. The number of spin-offs and the number of sell-offs from the parent over the previous 10 years, the log of the transaction price, and whether divested assets were physical and came from the core businesses were each significantly related to the probability that a particular divestiture would be a spin-off rather than a sell-off. The marginal effect of the prior spin-off experience was especially strong, with a single prior spin-off increasing the probability of another spin-off by nearly 90%. However, the percentage of outstanding common stock held by outside blockholders is not significantly related to the spin-off or sell-off decision. Therefore, the results fail to support Hypothesis 1, that higher levels of stockholding concentration of outside blockholders will be associated with spin-offs, while lower levels will be associated with sell-offs.

Logit Regression Coefficients and Marginal Effects for the Base Model of Controls and Ownership Concentration on the Probability of Spinoff

Marginal effect is for discrete change of the dummy variable from 0 to 1.

p < .05. **p < .01.

To test Hypothesis 2, we calculated the multiplicative interaction term between the percentage of stock held by outside blockholders and the log of the transaction price. Those results are reported in Table 3. The positive and significant coefficient on the interaction term indicates that the log of the transaction price (the size of divested business) has a significant positive moderating effect on the relationship between the percentage of stock held by outside blockholders and the probability of spin-off. Because of the nonlinear nature of the logit function, it is necessary to test whether the strength and significance of the moderating effect varies across the range of other model variables (e.g., Hoetker, 2007). Table 4 shows the marginal effect of outside blockholding ownership at three different levels of the log of the transaction price, with all other variables held at their mean. For small- to medium-sized transactions, outside blockholder ownership levels have no significant impact on the spin-off or sell-off decision. For the largest transactions, the marginal effects of outside blockholding levels becomes positive and significant. For the largest transactions, a company that has a percentage of stock held by outside blockholders 1 standard deviation above the mean would be 83% more likely to spin off rather than to sell off. These provide support for Hypotheses 2, that the relationship between the stockholding concentration of outside blockholders and divestiture by spin-off is more positive when the size of the divested firms increases. The relationship between stockholding concentration of outside blockholders and divestiture by sell-off is more positive when the size of the divested firms decreases.

Logit Regression Coefficients and Marginal Effects for the Moderation Effect of Transaction Size on the Ownership Concentration–Probability of Spin-off Relationship

Marginal effect is for discrete change of the dummy variable from 0 to 1.

p < .05. **p < .01.

Marginal Effect of Ownership Concentration for a Range of Transaction Sizes

Computed at sample mean value of blockholdings.

p < .05.

The other hypotheses were tested using the same procedures. Multiplicative interaction terms for managerial ownership (%) and outside blockholding ownership concentration and for duality and outside blockholding ownership levels were tested in separate models. The results reported in Table 5 show that the interaction of managerial ownership and outside blockholding ownership concentration was not related to the adoption of spin-off or sell-off actions, a result that is consistent over the complete range of insider ownership levels (Table 6). Similarly, Table 8 reports that the interaction between duality and outside blockholding ownership concentration is not related to spin-offs or sell-offs, an association that is the same at both possible duality levels. These results provide no support for either Hypothesis 3 or 4. Apparently, neither managerial ownership nor CEO duality moderates the relationship between outside blockholding ownership concentration and whether firms divest by spin-off or by sell-off.

Logit Regression Coefficients and Marginal Effects for the Moderation Effect of Insider Ownership on the Ownership Concentration–Probability of Spin-off Relationship

Marginal effect is for discrete change of the dummy variable from 0 to 1.

p < .05. **p <.01.

Marginal Effect of Ownership Concentration for a Range of Insider Ownership Values

Computed at sample mean value of blockholdings.

Logit Regression Coefficients and Marginal Effects for the Moderation Effect of CEO Duality on the Ownership Concentration–Probability of Spin-off Relationship

Marginal effect is for discrete change of the dummy variable from 0 to 1.

p < .05. **p < .01.

Marginal Effect of Ownership Concentration for Different CEO Duality Values

Computed at sample mean value of blockholdings.

Discussion

Recently, large outside owners of firms such as McGraw-Hill, Fortune Brands, and Marathon Oil have been pressuring their managers to use divestitures to sharpen company strategies and improve financial performance returns. In this study, we test whether the impact of such owners reaches beyond the motivation for the divestiture to include how it is divested, by spin-off or by sell-off. These decisions are important for owner wealth but also for managers, as divestiture decisions carry considerable cost and risk to both parties. Drawing from agency theory, we developed a model of how managers choose among spin-offs and sell-offs. Findings indicate that when outside blockholders can more ably exercise their self-interests over managers, such as when their stockholding concentrations are higher, then divesting firms tend to adopt divestiture through spin-off but only when the divested units are large. It appears that below a certain size threshold a particular divestiture decision is too small to motivate the influence of outside blockholders. In general, spin-offs would enable both the larger blockholder and the smaller owners to decide what they want to do with their share of the divested business, allowing them to make decisions more in accordance with their individual portfolio risks and investment priorities. By contrast, when outside blockholder stock concentrations are lower, allowing managers more latitude to act on their own self-interests, they tend to use divestiture through sell-off, particularly when the businesses involved are small. Managers may prefer such actions because they do not substantially alter the size and diversity of their firms or imply that the divesting firms require changes above and beyond what the current managerial team can manage (serving to reduce their employment risk). In addition, sell-offs generate cash that can be used to pay down debt and fund additional acquisitions, both of which can further managerial self-interests.

In both cases, divesting by spin-off or sell-off seems to be related to whether outside blockholder owners or managers are better able to exploit their respective self-interests when it comes to the divestiture process. Thus, when they are motivated to do so, which appears to occur when the divested unit is larger, outside blockholders appear to influence how the divestiture is conducted. The findings also show that the incentive alignment scheme of managerial ownership had no moderating influence on the outside blockholder concentration and spin-off adoption decision, nor did CEO duality. On balance, how the firm divests depends in part on the agency conditions and the divested unit’s size at the time of the divestiture.

Implications

The study findings contribute to theoretical explanations of divestitures and the divestiture process in several key ways. First, the agency theory model posited in this study adds to current organizational focused explanations of the choice between spin-off and sell-off. After controlling for the theoretical explanations of earlier studies, including the divested firm’s financial distress (Khan & Mehta, 1996; Nixon et al., 2000), previous experiences with spin-offs and sell-offs (Bergh & Lim, 2008), and its diversification and relatedness effects (Bergh et al., 2008), owner/manager agency conditions appear to add a new concept to knowledge of when spin-offs and sell-offs are adopted as divestiture implementation mechanisms. By highlighting the role of owner and managerial self-interests, the current study advances a new factor and another theoretical perspective to the evolving framework of how managers choose among divestiture alternatives.

More specifically, our focus on outside blockholders and the moderating impact of divestiture size extends previous research on possible owner influence on divestiture decisions. Nixon et al. (2000) report that the stockholder ownership of officers, directors, and institutions has no association with the choice of spin-off or sell-off. Our initial findings reveal that outside blockholders, when considered as an independent determinant, were also not linked to how the divestiture is implemented. However, when outside blockholders and the size of the divestiture transaction are considered jointly, the combination of the two seem to impact the selection of the divestiture mechanism. Given the nonsignificance of the outside blockholding variable when it is considered independently, it appears that divestiture size represents a range of threshold points when outside blockholders matter and when they do not. Considered generally, our support for an agency theory model suggests that the interaction of outside blockholders and transaction features (size of the divested unit), diversification (e.g., a source of information asymmetry between owners and managers), and learning curve effects from prior divestiture experiences collectively represent a more comprehensive explanatory framework for the adoption of spin-off and sell-off than currently exists. Taken together, our study proposes an expanded explanation of the choice between spin-off and sell-off divestiture methods.

Second, the findings further extend the agency theory explanation of divestitures. Prior research has linked agency factors as motivation for divestitures (see Brauer, 2006; Lee & Madhavan, 2010; Moschieri & Mair, 2008). For example, Bergh (1995), Bethel and Liebeskind (1993), Chatterjee et al. (2003), and Johnson, Hoskisson, and Hitt (1993) report that owner agency pressures can influence managers to restructure their portfolios of business lines. The current study finds that agency conditions also seem associated with how managers implement the divestiture through selecting between alternative mechanisms, particularly when the divested business’s size was included. Apparently, outside blockholders have more interest in the divestitures of larger units, which are more likely to have a material effect on the divested firm’s size and blockholders’ portfolio risk. Considered collectively, previous research links agency conditions to the incident of divestitures, while our study goes another step, relating owners to implementation choices. Agency theory appears to provide an integrative explanation of the motives and means (e.g., selection of spin-off or sell-off) of divestitures. These connections suggest that agency theory offers insight into the alignment of important stages of the divestiture process.

Third, the findings show that the governance mechanisms that might bridge the principal–agent divide had no effect on how divestitures occur. These results appear consistent with Sanders’s (2001) findings that managerial alignment schemes, when cast in terms of stockholdings, were not related to large and expensive actions such as acquisitions and divestitures. Sanders argued that managers appear to become more conservative when their ownership stakes increase. Our results may support that reasoning, suggesting that when divesting, manager-owners appear to act neither in the self-interests of their blockholders (spin-offs) or what non- or low-owner managers might prefer (sell-offs). This result also applies to duality. The leadership structure of the firm, whether it favors owners (no duality) or managers (duality) is found to have no link to how firms divest or have an impact upon the relationship between ownership and divestiture method. The self-interest motivational differences between owners and managers do not seem to change when incentive alignment schemes are simultaneously considered. What does matter, it appears, is the size of the unit, as that factor could directly influence the riskiness and implications of the divestiture. Only then are managers’ and owners’ self-interests reflected in how their firms divest.

The study’s contributions should be considered with respect to limitations. First, the study considers two divestiture mechanisms, spin-offs and sell-offs. While those methods are the most popular ways to fully divest assets, the findings cannot be applied to other divestiture forms, such as equity carve-outs (partial asset sales of a subsidiary) and complete liquidations. Additional study into these other actions would produce a more complete framework of all methods of conducting divestiture implementation. Also, we limited the study to outside blockholders, drawing from previous research that they have more power than other owner types in exercising considerable influence over managers and boards. Indeed, nonblockholders usually have little influence in the absence of blockholders, and the latter type of owner is sometimes considered to be a substitute for both directory boards and the managers themselves (Edmans, 2009; Rubin, 2007; Shleifer & Vishny, 1986). Nonetheless, we cannot make attributions about the findings to nonblockholding owners. Further, we did not distinguish between different types of blockholders and instead assumed that all such owners have the same motives. This assumption is consistent with prior research in the divestiture literature that reports that different types of ownership, including equity held by officers, directors, and institutions, had no relationship to whether spin-off or sell-off was selected (Nixon et al., 2000). Further, anecdotal evidence shows that different types of owners are teaming together to push for spin-offs in order to improve financial returns, a goal common to the traditional view of owners. Contrary to this assumption is evidence that some owners are more active than others and that not all have the same objectives or investment horizons (Connelly, Tihanyi, Certo, & Hitt, 2010; David et al., 2010). Therefore, our results can be generalized only to the view that blockholder owners seek to maximize profitability, and the findings may not pertain to blockholder owners who do not hold those objectives. Given this current state of findings on heterogeneous blockholders, we call for future research to further investigate the possible trade-offs and interrelationships among owner types to determine the nature of their influence on divestitures and divestiture implementation. Future research could begin to tease apart how different blockholders may hold differential preferences for spin-off versus sell-off. Finally, the present study did not consider the future performance implications of the choice between spin-off and sell-off. Although this study helps consolidate the conditions associated with why managers appear to choose one divestiture method over the other, we cannot make any claims regarding which method is “better” with respect to financial performance. We recommend further research that would expand our model to explore how spin-offs and sell-offs differentially affect the future financial performance of the parent firms.

In conclusion, prominent owners have recently been pressuring managers to use divestitures to refocus and streamline well-known and large firms that have been experiencing performance problems. We find that outside blockholders’ interests may extend beyond calling for divestitures and also include implementation decisions. Drawing from agency theory, the present study’s findings suggest that outside blockholders and managers have different objectives that in turn appear to influence how the divesting firms’ managers differentiate between the adoption of spin-off or sell-off within the broader divestiture implementation process. These decisions, however, appear to be contingent upon the size of the divested business. The large owners have, by virtue of their investments, committed interest in the divesting firm’s financial performance, and they do not appear to sit idly by when their firms engage in divestitures, actions that could directly have an impact upon their earnings. Rather than let their managers appropriate the returns from divesting by sell-offs, these large owners push for spin-offs, which enables them to decide for themselves what to do with the divested assets. Overall, these particular types of owners seem to have a farther and more wide-reaching impact on divestitures than previously recognized.

Footnotes

Appendix

We acknowledge that in a study such as this, where the phenomenon of interest is the choice between two alternative divestiture modes, there is the possibility of endogeneity as a result of self-selection. In other words, the characteristics of the firm that drive it to divest may also influence the type of divestiture mode chosen. Failing to control for that could potentially lead to biased coefficients. We test for this possibility by conducting a two-stage Heckman procedure that accounts for possible endogeneity.

The first step in conducting a two-stage analysis is to develop a comparison sample. Since our study examines divesting firms, it was necessary to create a sample of firms that did not divest. The sampling procedure that produced the original sample in our study of divesting firms covered the time frame from 1990 to 1999 and resulted in a sample of 205 firms spanning 104 unique four-digit Standard Industrial Classification (SIC) codes. For the purpose of developing a comparison sample of nondivesting firms, we made the assumption that any firm in any of those industries over the 1990–1999 time frame would have been “at risk” of making a divestiture. Applying this assumption resulted in a comparison sampling frame of nearly 35,000 firm-year observations. Being mindful of the potential for missing variables, and wanting a nondivesting comparison sample of approximately the same size as our divesting sample, we randomly chose 500 of those firm-year observations. From that point, we made two deletions: When one firm appeared multiple times we kept the earlier instance, and we eliminated cases where a firm in our divesting sample had been randomly selected into our nondivesting comparison sample. Applying those screens reduced the comparison sample to 462 observations. We then proceeded as follows:

Acknowledgements

This article was accepted under the editorship of Deborah E. Rupp. We appreciate the helpful comments from two anonymous reviewers and the guidance and insights provided by Professor Steven Michael, the action editor.